da-kuk/E+ by way of Getty Photos

Shares of jail proprietor/operator The GEO Group, Inc. (NYSE:GEO) have rallied forcefully since June 2021, shortly after suspending its dividend, finally reorganizing right into a C-Corp to pay down debt. The transfer away from the actual property funding belief, or REIT, construction was compelled by a Biden administration government order that prohibited the renewal of federal contracts with privately owned prisons. With high-interest charges on its debt however a secure, seen, albeit tepid outlook that might enhance markedly on Election Day 2024, the current insider shopping for merited a deeper dive. An evaluation follows beneath.

Looking for Alpha

Firm Overview:

The Geo Group, Inc. is a Boca Raton, Florida-based proprietor, lessee, lessor, and supervisor of prisons, processing facilities, and reentry amenities. The corporate’s footprint encompasses ~81,000 beds at 100 areas within the U.S., Australia, and South Africa. Geo Group was based as a division of Wackenhut Company in 1984 and went public as Wackenhut Corrections Company in 1994, elevating web proceeds of $17.6 million at $0.50 per share (after giving impact to 4 inventory splits). It modified to its current moniker in 2004, transformed to a REIT construction in 2013, and again to a C-corp in 2021. Its inventory trades simply above $15.00, translating to an approximate market cap of $1.95 billion.

March 20224 Firm Presentation

Working Segments

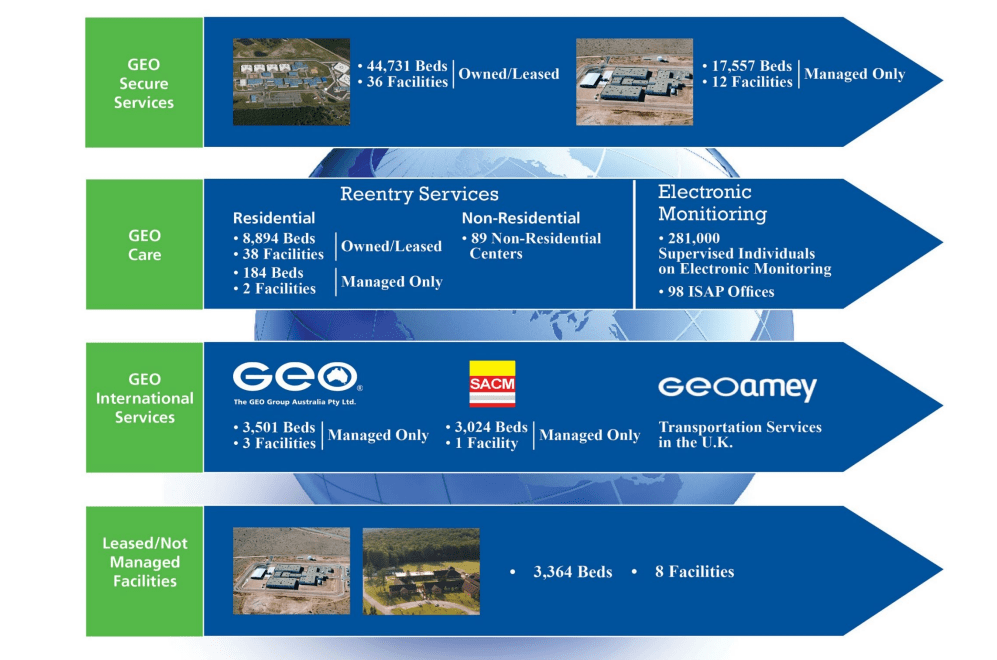

Geo earns the preponderance of its income from federal, state, native, and worldwide authorities contracts that payout on a per diem per inmate foundation, working below 4 reportable enterprise segments: U.S. Safe Providers (USSS); Reentry Providers; Digital Monitoring and Supervision (EMS), and Worldwide Providers.

March 20224 Firm Presentation

USSS entails the executive, rehabilitative, instructional, safety, transportation, and meals companies at home prisons by public-private partnerships. The section owns or leases 36 amenities encompassing 44,731 beds, manages 12 prisons comprising 17,557 beds, and leases out however doesn’t handle one other eight with 3,364 beds. The division was chargeable for FY23 working revenue of $270.0 on income of $1.52 billion, down 4% and up 6% from FY22 (respectively), in addition to 63% of its complete FY23 high line. The rise on the high line was a operate of elevated per diem charges offset by a lower in compensated man-days from 17.5 million in FY22 to 16.7 million in FY23, which drove occupancy at its working amenities from 87.8% all the way down to 85.9%.

Along with authorities businesses within the public sector, USSS companies compete with the likes of CoreCivic, Inc. (CXW) – its largest rival – in addition to Administration and Coaching Company, amongst others. By way of complete beds throughout all its segments within the personal sector, Geo holds the primary market share at 40%, adopted carefully by CoreCivic at 38%.

Reentry Providers primarily owns, leases, and operates 40 residential reentry facilities and midway homes encompassing 9,078 beds, in addition to 89 non-residential facilities. It supplied FY23 web revenue of $48.7 million on income of $275.1 million, representing 14% and eight% enhancements, respectively, in addition to 11% of complete income. The will increase on the high and backside traces had been primarily a operate of upper visitors by its amenities.

EMS encompasses non-residential day reporting facilities, residential reentry and youth companies, rehabilitation applications, in addition to monitoring applied sciences for ~281,000 parolees, probationers, and pretrial defendants primarily out of 98 Intensive Supervision and Look Program (ISAP) workplaces. The section accounted for FY23 web revenue of $212.9 million on income of $425.9 million, reflecting declines of 11% and 14%, respectively, as members counts within the ISAP dropped all through FY23. EMS’s high line represented 18% of Geo’s complete.

Worldwide Providers is actually the U.S. Safe Providers division in Australia and South Africa, masking a complete of 4 felony detention amenities and 6,025 beds. It additionally supplies detainee transportation companies within the UK. The section contributed FY23 web revenue of $11.5 million on income of $193.9 million, representing a 39% lower at backside line on a 4% enhance on the high versus FY22, as will increase within the Australian inhabitants had been offset by greater per prisoner bills, together with these from a brand new well being care contract.

March 20224 Firm Presentation

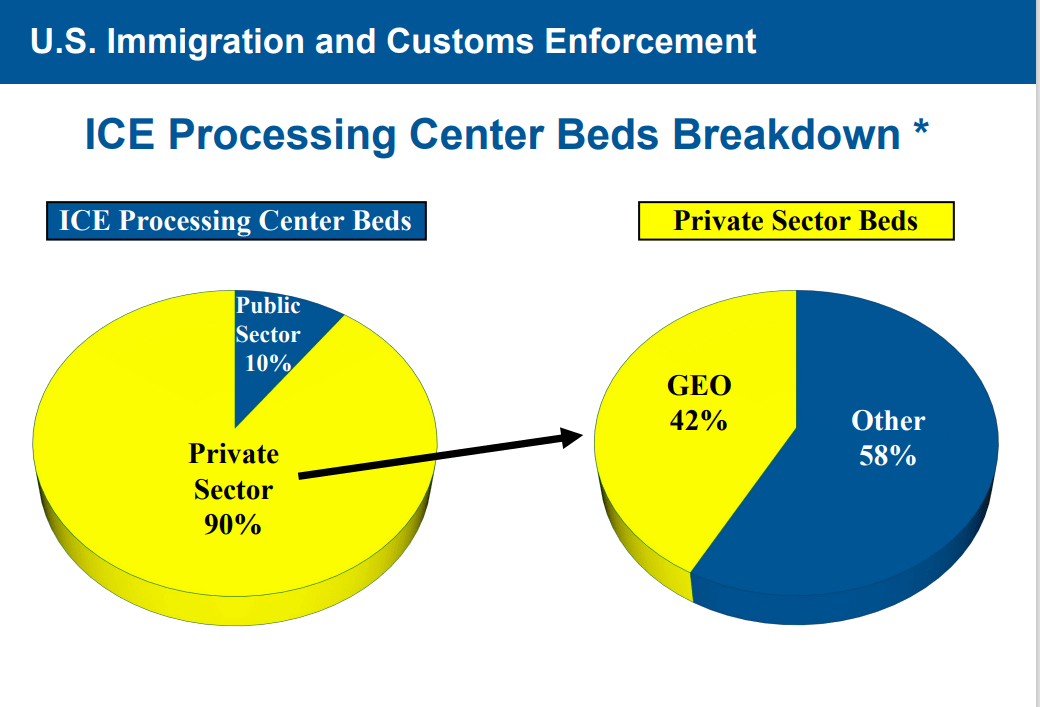

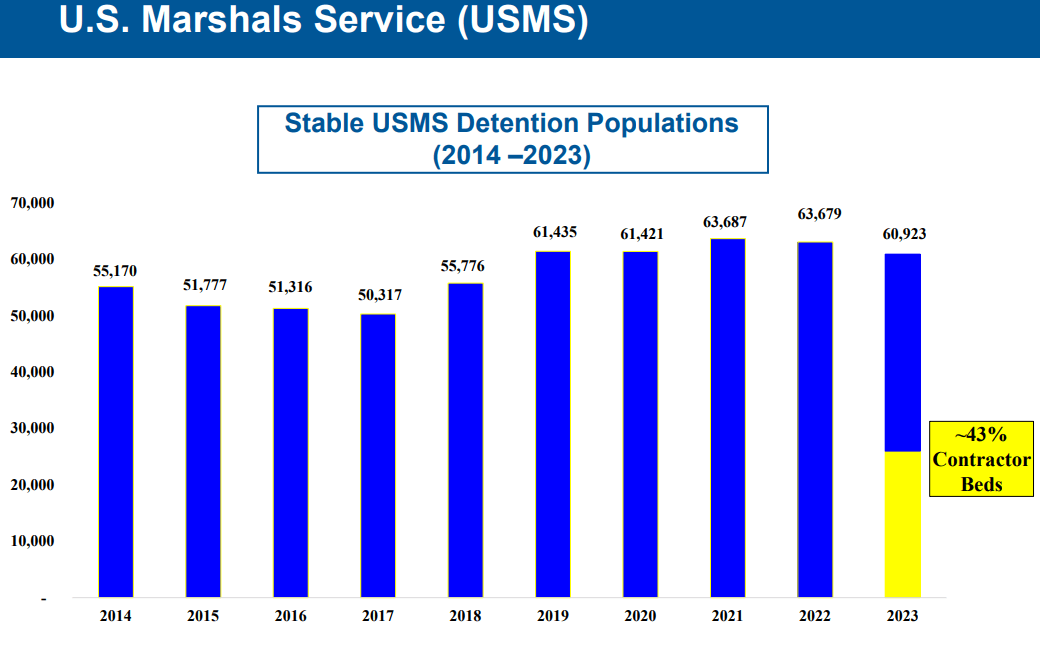

With the public-private partnerships by which Geo engages, it isn’t a stunning that 62% of its high line is derived from numerous businesses of the U.S. Federal Authorities with Immigration and Customs Enforcement [ICE] (43%) and U.S. Marshals Service (16%) the biggest benefactors. The opposite would-be main federal buyer, the Bureau of Prisons, solely accounted for 3%. Extra on this growth beneath.

March 20224 Firm Presentation

It needs to be famous that at YE23, Geo’s USSS section had seven idle edifices representing a complete of 9,732 beds, whereas its Reentry Providers unit has three unoccupied buildings that housed one other 1,689 beds. The money carrying value of those buildings quantities to $8.3 million. Extra importantly, at FY23 per diem and occupancy charges, they characterize unexploited income of ~$350 million and annual earnings of ~$0.30 per share.

FY23 Financials and FY24 Outlook

After factoring in company overhead, the 4 segments of Geo generated FY23 earnings of $0.95 per share (non-GAAP) and Adj. EBITDA of $507.2 million on income of $2.41 billion, versus $1.40 per share (non-GAAP) and Adj. EBITDA of $540.0 million on income of $2.38 billion, representing declines of 32% and 6% (respectively) on a top-line enhance of two%. The biggest issue within the bottom-line weak spot was considerably greater web curiosity expense, which was up $61.9 million, or $0.50 a share, as almost half the corporate’s debt is floating charge.

As a part of its 4Q23 and FY23 monetary report of February 15, 2024, administration launched its outlook for FY24, which included non-GAAP earnings of $0.93 a share and Adj. EBITDA of $500 million, with the previous metric impacted by web curiosity expense of $195 million, or $1.54 a share. From an operational standpoint, the marginally downward Adj. EBITDA estimate displays issues relating to ICE funding. All projections are based mostly on vary midpoints.

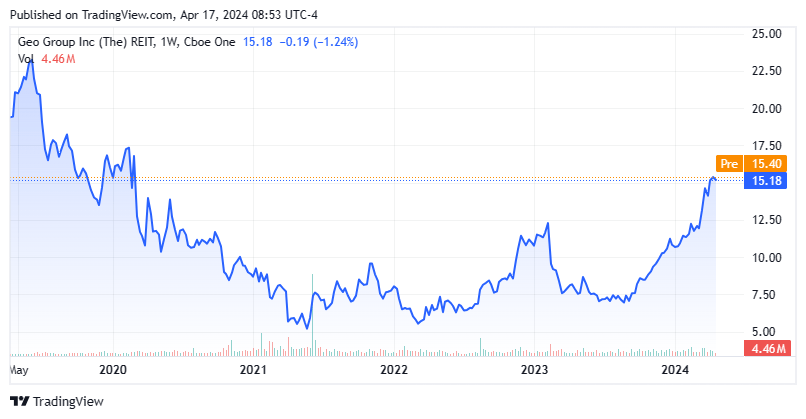

Share Worth Efficiency

The web curiosity expense line merchandise considerably unlocks the story of Geo and its present standing as a non-REIT. After attaining REIT standing in 2013, Geo grew its high line at an 8.5% CAGR by 2019, principally by way of the idea of extra debt which elevated at a virtually an identical 8.6% CAGR throughout the identical interval. It paid a $0.47 or $0.48 quarterly disbursement throughout a lot of the Trump administration, however its working mannequin was negatively impacted primarily on account of a web lower in detainees at its ICE amenities and a drop in courtroom sentencing at federal courts – each brought on by the pandemic – leading to a FY20 income decline of 5% to $2.35 billion whereas long-term debt rose 6% to $2.6 billion. Figuring out that a few of its barely diminished money circulate can be higher employed within the discount of its debt, administration determined to chop the corporate’s quarterly dividend in October 2020 from $0.48 to $0.34.

Then on January 26, 2021, newly elected President Biden signed an government order banning the renewal of any federal authorities contracts with privately operated felony detention amenities, that means no additional income from the Bureau of Prisons (BOP) or (theoretically) the U.S. Marshals Service (USMS) past the phrases of Geo’s present contracts. In response to this motion, the corporate lower after which suspended its dividend and restructured as a C-corp. The web impact of the chief order left Geo with no BOP safe correctional facility contracts at YE23, however as a result of the USMS (in contrast to the BOP) doesn’t personal or function detainee housing and had no place to accommodate prisoners awaiting trial, virtually received out, and it has renewed contracts with Geo.

That stated as a result of its ICE enterprise has picked-up significantly in the course of the Biden administration, income has remained comparatively flat since FY18, in a decent vary of $2.26 billion (2021) to $2.48 billion (2019). Aside from FY23, the identical slender vary applies to non-GAAP web revenue, which spanned from $1.30 (2020) to $1.60 a share (2019). Nevertheless, shares of GEO had been on a protracted decline from shortly after President Trump’s 2017 inauguration, peaking at an all-time excessive of $34.32 in April of that yr, solely to backside out at $4.96 in Might 2021, down 86%.

This nadir carefully coincided with the upheaval from turning over most, if not all of its shareholder base when it lower after which suspended its dividend and later reorganized as a C-corp. That realignment supplied (at the moment) a brand new administration staff a chance to make use of free money circulate and asset gross sales –predominantly reentry amenities totaling ~$150 million up to now – to scale back the corporate’s web leverage, which at the moment was ~4.4, based mostly on its FY21E Adj. EBITDA.

Stability Sheet & Analyst Commentary:

And to that finish, administration has had some success, reducing its debt by $197 million to $1.85 billion throughout FY23 and its leverage to three.3, though that metric is up from 3.1 at YE22. Between its unrestricted money and untapped revolving credit score facility entry, Geo had accessible liquidity of $283 million. With half its debt floating charge, its weighted common rate of interest in FY23 was north of 10%, punctuating the necessity to retire it as rapidly as attainable and proceed to forego paying a dividend. Its publicly traded bonds are rated junk (CCC+/Caa1) by S&P and Moody’s, respectively.

In direction of that finish, earlier this month, the corporate raised $1.275 billion in combination notes in addition to opened a brand new $450 million credit score facility. The proceeds from these two funding sources might be used to retire $1.5 billion in present debt and push out debt maturities to 2029.

To this point in 2024, Wedbush ($14 worth goal), Northland Securities ($15 worth goal) and Noble Monetary ($17 worth goal) have all reissued Purchase rankings on the inventory. On common, they expect (like administration) the corporate to earn $1.01 a share (non-GAAP) on income of $2.45 billion in FY24, adopted by $1.37 a share (non-GAAP) on income of $2.52 billion in FY25.

Additionally, bullish is Founder, former CEO, and present Government Chairman George Zoley, who bought 50,000 shares at a median worth of $12.48 on March 14, 2024, marking the primary insider purchase since June 2021.

Verdict:

Possessing a gentle, safe, and considerably capped income base, Geo will proceed to slowly pay down its high-interest debt. With its fill up 164% from its low in Might 2021, it’s all about whether or not the market will broaden or compress its multiples. Its P/E on FY24E EPS is at the moment 15 and its EV/FY24E Adj. EBITDA is below eight. These are truthful valuations, albeit not overly compelling.

Nevertheless, they are going to look so much higher if there’s a Republican sweep on Election Day 2024, which might possible reverse the Biden government order whereas concurrently rising sources for the corporate’s federal company consumer base, that means potential employment of its idle amenities or a rise in ISAP. Perceptions of a possible sweep will possible put a flooring in its inventory, making it a strong covered call candidate till the election. I additionally want this technique to holding straight fairness for its draw back threat mitigation and because the inventory is hitting up towards analyst agency worth targets. In any other case, I’d wait till the inventory pulled again across the $12 – $13 degree, the place the CEO lately added to his stake within the firm, earlier than initiating an preliminary holding in The GEO Group, Inc. shares.