PonyWang

The PGIM International Excessive Yield Fund (NYSE:GHY) is a closed-end fund that income-focused traders can buy as a technique of reaching their objective of incomes spendable earnings from the belongings of their portfolio. This can be a want of many retirees and others who’re residing off of their financial savings versus primarily incomes cash from an everyday job. It’s also a typical want of many different people making an attempt to take care of their way of life in right this moment’s inflationary surroundings, as the price of nearly every thing that we buy right this moment has been rising extra quickly than incomes (regardless of what the patron value index says). That is significantly the case for meals and different requirements. The PGIM International Excessive Yield Fund does this job fairly nicely, as its 11.22% yield compares fairly nicely to only about another fund available in the market right this moment. It definitely compares nicely to its friends, as we are able to see right here:

|

Fund Title |

Morningstar Classification |

Present Yield |

|

PGIM International Excessive Yield Fund |

Fastened Revenue-Taxable-Excessive Yield |

11.22% |

|

AllianceBernstein International Excessive Revenue Fund (AWF) |

Fastened Revenue-Taxable-Excessive Yield |

7.84% |

|

Allspring Revenue Alternatives Fund (EAD) |

Fastened Revenue-Taxable-Excessive Yield |

9.79% |

|

Barings International Brief Length Excessive Yield Fund (BGH) |

Fastened Revenue-Taxable-Excessive Yield |

9.04% |

|

RiverNorth Capital and Revenue Fund (RSF) |

Fastened Revenue-Taxable-Excessive Yield |

11.15% |

|

Western Asset Excessive Revenue Alternative Fund (HIO) |

Fastened Revenue-Taxable-Excessive Yield |

11.33% |

As we are able to clearly see, the PGIM International Excessive Yield Fund is likely one of the highest-yielding funds on this listing. It isn’t absolutely the highest by way of yield, however it is rather shut. That is one thing that would show very enticing to these traders who’re looking for to maximise the earnings that they earn from the belongings of their portfolios. Nevertheless, it is very important take into account that there are occasions when a excessive yield suggests concern from the market in regards to the fund’s potential to pay its distribution. Nevertheless, the truth that the PGIM International Excessive Yield Fund’s yield isn’t ridiculously out of line with its friends means that that is in all probability not the case right this moment. Nevertheless, it’s nonetheless one thing that we need to examine as we do need to be sure that the fund can afford the distribution that it’s paying out. We are going to talk about this in additional element later on this article.

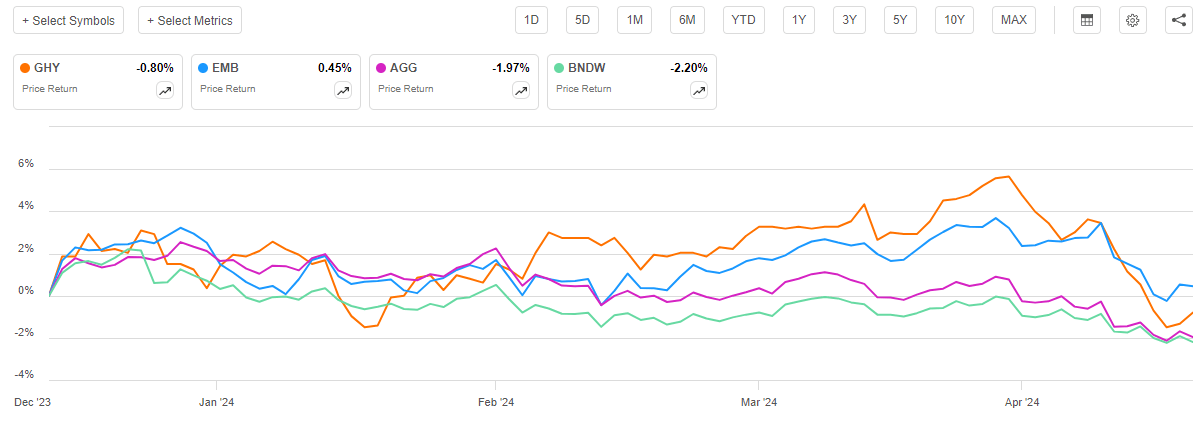

As common readers can seemingly keep in mind, we beforehand discussed the PGIM International Excessive Yield Fund in mid-December 2023. The bond market since that point has been considerably weak, though it was pretty robust for about two weeks following the discharge of that article. For many of December, numerous market contributors have been anticipating that the Federal Reserve would quickly cut back rates of interest over the course of 2024. As such, these market contributors have been aggressively shopping for up bonds and different income-producing securities with a view to front-run the Federal Reserve and lock in fairly enticing yields over the long run. Nevertheless, latest financial and inflation knowledge proceed to disappoint these traders who anticipate price cuts as inflation is getting worse and the financial system stays robust. Briefly, with every passing month, it turns into tougher and tougher for the central financial institution to justify a discount within the federal funds price. As such, the bond market has been promoting off year-to-date to mirror the fact that the market was overly optimistic at the beginning of the yr. That is precisely the situation that common readers anticipated, as I’ve been stating for a while now that price cuts aren’t justified. As such, we are able to in all probability anticipate that the share value efficiency of the PGIM International Excessive Yield Fund has not been particularly good for the reason that date of the earlier article’s publication. That is the case, as shares of the fund are down 0.80% since December 12, 2023 (the date of the prior article’s publication):

Looking for Alpha

As we are able to see, the fund’s shares have outperformed each the Bloomberg U.S. Mixture Bond Index (AGG) and the Vanguard World Bond ETF (BNDW) over the interval. Nevertheless, the fund has underperformed rising market bonds (EMB), which have really risen in value. Rising market bonds are one thing of a special animal than developed market or home bonds, nonetheless, as they really profit from a declining greenback. As now we have seen within the value of gold, traders around the globe are starting to doubt that the Federal Reserve will be capable to get inflation below management and have been making an attempt to maneuver away from a declining greenback. The PGIM International Excessive Yield Fund holds each home, overseas developed, and rising market bonds so we might anticipate that its efficiency would considerably mirror each tendencies. That is certainly the case as its value efficiency has been between rising market and developed market bonds.

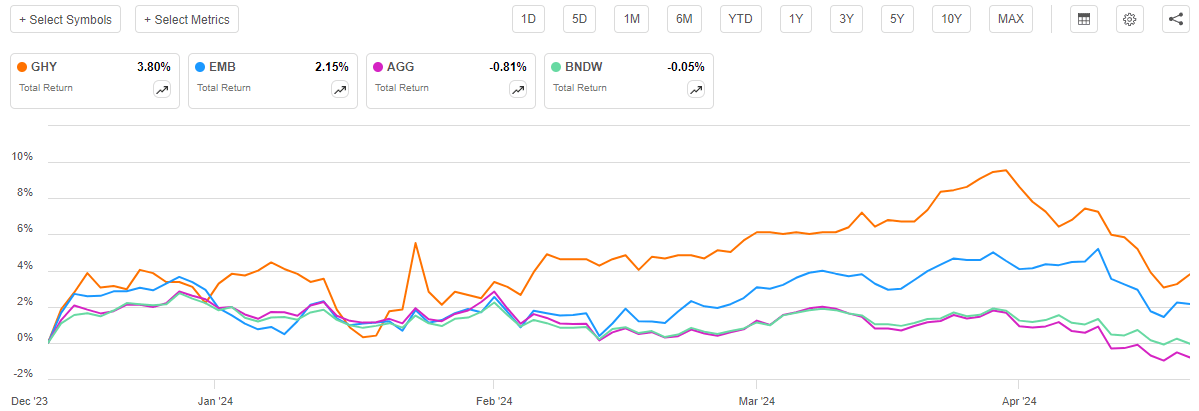

A easy have a look at the value efficiency of the PGIM International Excessive Yield Fund doesn’t inform us the entire story, nonetheless. As I’ve identified quite a few instances up to now, a closed-end fund equivalent to this one usually pays out most or all of its funding income to the shareholders by way of distributions. The essential enterprise mannequin is to maintain the dimensions of the portfolio comparatively secure over time whereas giving the shareholders all the income which might be derived from that portfolio. As such, the distribution will account for a major proportion of the return supplied by the fund, and it’s not seen in share value actions. As such, we should always embody the distributions paid by the fund in any dialogue of its efficiency. Once we do this, we see that traders within the PGIM International Excessive Yield Fund benefited from a 3.80% acquire for the reason that date that my earlier article on the fund was printed:

Looking for Alpha

That is higher than any of the three indices delivered over the identical interval, together with the rising market bond index. Rising market bonds nearly at all times have considerably increased yields than developed market bonds, however even they solely managed to ship a 2.15% whole return over the roughly four-month interval. This could enhance the attractiveness of this fund additional and, at the least on the floor, means that it could possibly be a great possibility for traders who’re looking for world diversification and a doable hedge in opposition to U.S. greenback devaluation.

Nevertheless, we do must have a better have a look at the fund to find out how nicely it’s really doing and the way nicely it’s more likely to do sooner or later. In spite of everything, previous efficiency isn’t any assure of future outcomes, and traders who buy the fund right this moment aren’t affected by previous outcomes. The fund launched its semi-annual report a couple of weeks in the past, so that ought to help in our evaluation. Allow us to proceed onward and see if buying this fund right this moment makes any actual sense for income-seeking traders.

About The Fund

In keeping with the fund’s website, the PGIM International Excessive Yield Fund has the first goal of offering its traders with a really excessive stage of present earnings. In contrast to many different funds from different sponsors, the fund’s web site doesn’t present any actual perception into how the fund expects to realize this goal. Quite, all it states is:

The Fund seeks to supply a excessive stage of present earnings by investing primarily in beneath investment-grade fastened earnings devices of issuers situated around the globe, together with rising markets.

This isn’t as in-depth because the technique descriptions that we get from the web sites of another closed-end funds. Nevertheless, it does nonetheless inform us what we actually must know in regards to the fund’s methods to realize its objectives. Briefly, the fund invests its belongings in high-yield securities issued by entities anyplace on the planet. Principally, it is a junk bond fund that doesn’t have the nation constraints of an American-specific bond fund. As such, the fund’s goal of offering its traders with a really excessive stage of present earnings appears applicable. As I identified in my earlier article on this fund:

Bonds by their very nature are earnings autos. Buyers buy bonds at face worth, which they obtain again when the bond matures. As such, there aren’t any web capital beneficial properties over a bond’s lifetime. In spite of everything, a bond has no inherent hyperlink to the expansion and prosperity of the issuing firm or authorities.

As such, any pure bond fund goes to have present earnings as its major goal. It’s because bonds don’t produce any web capital beneficial properties over their lifetimes. Nevertheless, as now we have seen in numerous previous articles, plenty of bond funds aren’t pure bond funds as their belongings could embody different kinds of fixed-income securities and even widespread shares. This one isn’t any exception to this because the semi-annual report gives the next asset allocation:

|

Asset Kind |

Share of Whole Portfolio |

|

Asset-Backed Securities |

4.0% |

|

Convertible Bonds |

0.0% |

|

Company Bonds |

94.9% |

|

Floating Price and Different Loans |

4.5% |

|

Sovereign Bonds |

20.5% |

|

Widespread Shares |

2.1% |

|

Most popular Inventory |

0.1% |

|

Cash Market Fund |

0.2% |

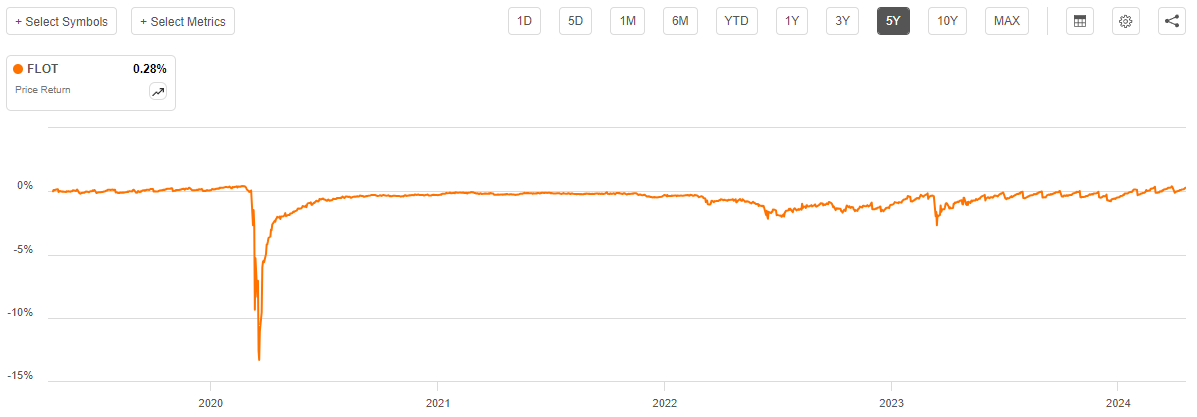

The 0.0% allocation to convertible bonds doesn’t imply that there are none of those securities current within the fund’s portfolio. The fund has a small convertible bond place in Sunac China Holdings, however this place represents such a small proportion of the fund’s whole portfolio that it rounds off to a 0.0% weighting. The large factor that we see right here is that the PGIM International Excessive Yield Fund has allocations to each widespread shares and floating-rate bonds that may exhibit vastly completely different efficiency available in the market than odd bonds. Floating-rate securities, for instance, don’t expertise the value actions that bonds do when rates of interest change. We will in a short time see this by trying on the five-year value chart of the iShares Floating Price Bond ETF (FLOT):

Looking for Alpha

As we are able to see, with the notable exception of the panic at the beginning of the COVID-19 pandemic, the fund has been remarkably secure even supposing rates of interest modified quite a bit over the interval in query. In reality, the slight variations that we see the fund exhibit in latest instances is because of timing variations between the fund’s receipt of funds from the securities that it holds and the date that it pays its distributions. Briefly, these securities is not going to change a lot when rates of interest change so their presence within the portfolio of the PGIM International Excessive Yield Fund will add a level of stability to the fund’s portfolio. After all, the weighting that the fund has to those securities is so low that the affect of their presence is not going to be readily obvious. They may nonetheless make the fund barely much less risky by way of value than it will in any other case be, although.

The truth that this fund has a small allocation to widespread shares might additionally change its efficiency profile barely from one that’s completely invested in bonds. In spite of everything, widespread shares are affected by issues equivalent to financial progress charges, authorities insurance policies, client demand, and quite a few elements which might be distinctive to the issuing firm. Listed here are all the widespread shares on this fund’s portfolio:

|

Firm |

Nation |

|

Digicel Worldwide Finance (DCEL) |

Jamaica |

|

Intelsat Emergence SA (INTEQ) |

Luxembourg |

|

CEC Leisure |

United States |

|

Chesapeake Vitality Corp. (CHK) |

United States |

|

Cornerstone Chemical Co. |

United States |

|

Ferrellgas Companions (OTCPK:FGPR) |

United States |

|

GenOn Vitality Holdings |

United States |

|

Heritage Energy LLC |

United States |

|

TPC Group |

United States |

|

Venator Supplies PLC (OTCPK:VNTRD) |

United States |

Many of those are firms that I might not contact proper now, as corporations equivalent to Ferrellgas Companions have been struggling for years. Fortuitously, they solely account for very small positions within the fund and individually they won’t have any noticeable affect on the fund as a complete. Nevertheless, we are able to nonetheless see that the fund isn’t solely a bond fund because the floating-rate securities and the widespread shares account for six.6% of its belongings in combination. That 6.6% weighting is sufficient to trigger the fund’s efficiency to be barely completely different from a pure bond fund.

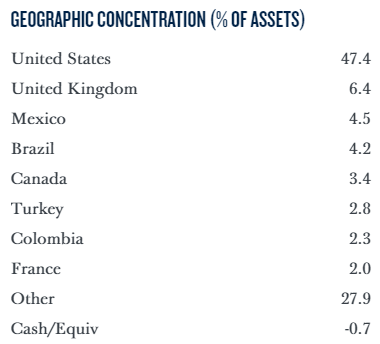

In my final article on this fund, I identified that the PGIM International Excessive Yield Fund is much less weighted in the direction of the US than many different world bond funds. That is partly because of the 20.5% allocation to sovereign bonds, as there aren’t any junk-rated sovereign bonds issued inside the US. This chart breaks down the fund’s portfolio by nation as a proportion of belongings:

PGIM

America is essentially the most closely weighted particular person nation within the fund’s portfolio, which isn’t stunning. The nation has the most important nationwide financial system on the earth on a nominal foundation (however not on a buying energy foundation) and is by far the most important issuer of debt on the earth. The Vanguard World Bond ETF at the moment has a 51.10% weighting to the US:

Vanguard

I’ll confess that I’m uncertain of how nicely this really displays the worldwide bond market as I can’t discover any details about the precise dimension of any given nation’s bond market. Nevertheless, that is nearly as good as info that now we have to go on, and if we assume that that is right then American issuers challenge simply over half of all the bonds which might be traded within the world market.

We will due to this fact see that the PGIM International Excessive Yield Fund seems to be underweight to the US. This was the identical state of affairs that we noticed the final time that we mentioned the fund. In reality, its weighting to the US has declined considerably over the previous 4 months since we final mentioned it. Within the earlier article, I discussed that the fund had a 48.4% weighting to this nation. This weighting discount is one thing that may enchantment to some traders right this moment. As I’ve famous in numerous earlier articles, one of many greatest issues that the common American investor has is that their portfolios are inclined to have outsized publicity to the US. That is comprehensible because the American fairness markets have outperformed nearly any overseas market over the previous fifteen years. Within the case of bonds, it’s troublesome to even get most overseas bonds in the US as most brokers don’t carry them. Anecdotally, the final time that I known as the bond buying and selling desk at a significant U.S. dealer and inquired about buying overseas sovereign bonds, I used to be instructed that the minimal buy was a quantity that’s out of attain for many retail traders. As such, the one real looking method that Individuals can get publicity to those belongings is by buying a world bond fund, and people don’t get a lot protection within the American media. Thus, nearly by default, most American traders have very restricted and even no publicity to those belongings.

The actual fact is, although, that American traders may be nicely served by investing in overseas bonds right this moment. One motive for that is that the monetary state of affairs of many different nations, significantly rising nations, is a lot better than that of the US. For instance, take into account the debt-to-GDP ratio of the most important nations whose securities are held by the PGIM International Excessive Yield Fund:

|

Nation |

Debt-to-GDP |

|

United States |

129% |

|

United Kingdom |

97.1% |

|

Mexico |

49.6% |

|

Brazil |

72.87% |

|

Canada |

107% |

|

Turkey |

31.7% |

|

Columbia |

63.6% |

|

France |

112% |

(All figures are supplied by World Inhabitants Overview utilizing knowledge from the United Nations).

There are a couple of sources that present completely different figures for a few of these nations as there are a couple of methods to calculate the debt-to-GDP ratio. Nevertheless, all of those sources agree that the US has a better debt-to-GDP ratio than many of the different nations of the world and that it’s rising pretty quickly. The Committee for a Accountable Price range projects that the 2025 funds request that President Biden submitted final month would lead to a cumulative deficit of $17.7 trillion over the subsequent ten years. Traditionally, estimates like this are typically decrease than what really happens however regardless we are able to see that the fiscal state of affairs in the US is not going to enhance anytime quickly. In the meantime, now we have a state of affairs through which the Federal Reserve appears to be dedicated to rate of interest cuts regardless of the headline inflation price going up each single month this yr:

Buying and selling Economics

On prime of that, overseas commodity exporters and manufacturing nations which have traditionally funded the deficits of the US equivalent to Russia, China, and Saudi Arabia have gotten more and more reluctant to take action. That is one motive why we’re seeing overseas central banks lowering their holdings of U.S. {dollars} in favor of gold or different currencies (such because the Chinese language renminbi). I’ve pointed this out in a couple of articles going again over the previous few many years. If the Federal Reserve have been to really reduce rates of interest whereas inflation is worsening, it will weaken the greenback versus different currencies and will speed up this course of.

This can be a web damaging for American bonds usually because the buying energy of the coupons paid by these bonds will decline over time. In the meantime, a declining greenback really will increase the worth of bonds that pay their coupons in different currencies, as considered from the angle of an American investor. In spite of everything, the overseas forex that’s acquired from these bonds converts into extra {dollars} when the investor conducts the forex trade. This is likely one of the the reason why rising market bonds are inclined to outperform American ones when the U.S. greenback is declining.

The PGIM International Excessive Yield Fund seems to be positioned to reap the benefits of the declining greenback by advantage of its underweight place in American bonds relative to the index. The truth that the fund’s weighting to the US has been reducing might even counsel that its administration is making an attempt to reap the benefits of this example. Total, that is one thing that traders ought to admire, and it could possibly be worthwhile to have a fund such because the PGIM International Excessive Yield Fund in your portfolio as a hedge in opposition to a declining greenback.

Leverage

As is the case with most closed-end funds, the PGIM International Excessive Yield Fund employs leverage as a technique of boosting the efficient yield that it receives from the securities in its portfolio. I defined how this works in my earlier article on this fund:

Principally, the fund borrows cash after which makes use of that borrowed cash to buy high-yield bonds and related income-producing belongings. So long as the bought belongings have a better yield than the rate of interest that the fund has to pay on the borrowed cash, the technique works fairly nicely to spice up the efficient yield of the portfolio. As this fund is able to borrowing cash at institutional charges, that are significantly decrease than retail charges, that may often be the case.

Sadly, the usage of debt on this trend is a double-edged sword. It’s because leverage boosts each beneficial properties and losses. As such, we need to be sure that the fund isn’t using an excessive amount of leverage as a result of that might expose us to an extreme quantity of danger. I often would love a fund’s leverage to be below a 3rd as a proportion of its belongings because of this.

As of the time of writing, the PGIM International Excessive Yield Fund has leveraged belongings comprising 21.52% of its belongings. That is fairly affordable when in comparison with lots of the fund’s friends, as we are able to see right here:

|

Fund Title |

Leverage Ratio |

|

PGIM International Excessive Yield Fund |

21.52% |

|

AllianceBernstein International Excessive Revenue Fund |

18.05% |

|

Allspring Revenue Alternatives Fund |

30.30% |

|

Barings International Brief Length Excessive Yield Fund |

25.81% |

|

RiverNorth Capital and Revenue Fund |

46.20% |

|

Western Asset Excessive Revenue Alternative Fund |

0.00% |

(all figures from CEF Information)

As we are able to clearly see, the PGIM International Excessive Yield Fund typically compares fairly nicely with its friends with respect to leverage. It isn’t the least leveraged fund of the group by any means, however many of the different funds right here have a leverage ratio that compares pretty nicely with it. This implies that the fund is at the moment using an inexpensive and applicable stability between the dangers and potential rewards from the usage of leverage. We should always not want to fret an excessive amount of in regards to the fund’s excellent debt right this moment.

Distribution Evaluation

As talked about earlier on this article, the first goal of the PGIM International Excessive Yield Fund is to supply its traders with a really excessive stage of present earnings. In pursuit of this goal, the fund primarily invests its belongings right into a portfolio consisting of company and sovereign high-yield bonds issued by entities which might be based mostly everywhere in the world. The fund does have a couple of belongings that fall into different classes, however for essentially the most half, the belongings which might be held by this fund will ship the vast majority of their funding returns within the type of direct funds to their homeowners. On this case, that proprietor is the fund, and the fund collects the coupon funds on behalf of its traders. This fund then takes issues a step additional and borrows cash that it makes use of to buy extra bonds, permitting it to obtain funds from extra securities than it might management solely by way of reliance by itself fairness capital. The fund combines all the cash that it receives from these coupon funds with any beneficial properties that it manages to acquire by way of the sale of bonds which have gone up in value. Lastly, the fund pays out all the cash that it receives from these numerous actions to its shareholders, web of its personal bills. As rates of interest right this moment are near the best ranges that now we have seen in a technology, we are able to anticipate that this course of would enable the fund’s shares to boast a decent yield.

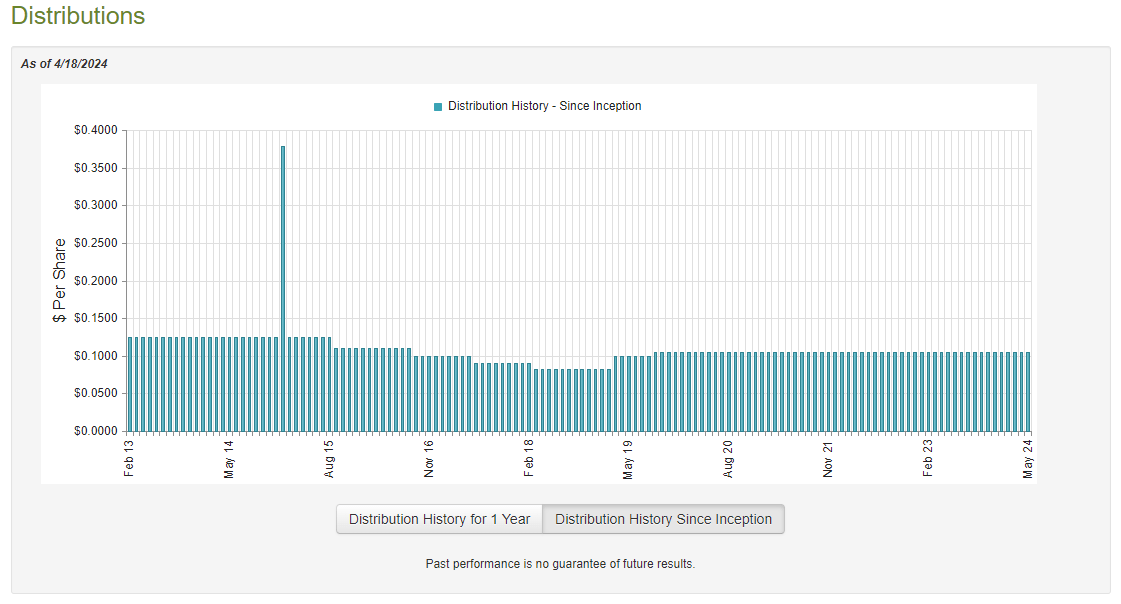

That is definitely the case because the PGIM International Excessive Yield Fund at the moment pays a month-to-month distribution of $0.1050 per share ($1.26 per share yearly), which supplies the fund an 11.22% yield on the present share value. As we noticed within the introduction, it is a very respectable yield that compares fairly nicely to the fund’s friends. This fund has been pretty in keeping with respect to its distribution over time, nevertheless it has definitely not been good as we are able to see right here:

CEFConnect

As clearly proven, the fund each raised and lowered its distribution a couple of instances over its historical past. Nearly all of these adjustments got here within the latter half of the earlier decade as this fund has been remarkably constant within the 2020s. Certainly, we might nearly say that it has been too constant as most different funds have been pressured to cut back their distributions following the Federal Reserve’s aggressive rate of interest hikes in 2022 and early 2023. These rate of interest hikes brought about the value of American bonds to fall and thus brought about most closed-end funds that have been invested in them to undergo each realized and unrealized losses. This fund doesn’t make investments completely in American bonds, nevertheless it nonetheless nearly definitely took some losses as most central banks around the globe additionally elevated their rates of interest following the pandemic. As well as, roughly half of the bonds which might be held by this fund are American so are nonetheless affected by the insurance policies of the Federal Reserve. As such, it’s curious that this fund was capable of preserve its distribution throughout a interval through which most different funds couldn’t. That is one thing that we should always examine additional.

Fortuitously, now we have a really latest doc that we are able to seek the advice of for the needs of our evaluation. As of the time of writing, the latest monetary report for the PGIM International Excessive Yield Fund is the semi-annual report that corresponds to the six-month interval that ended on January 31, 2024. A hyperlink to this report was supplied earlier on this article. This can be a a lot newer report than the one which was out there to us on the time of our earlier dialogue so we are able to anticipate it to have extra up-to-date info. Specifically, this report ought to give us a good suggestion of how nicely this fund dealt with the 2 disparate market environments that existed within the second half of 2023. The primary of those environments was current in the course of the summer season and early autumn months of that yr, and it was characterised by typically falling asset costs and rising bond yields. This was resulting from market contributors starting to comprehend that the struggle in opposition to inflation was a great distance from being gained, and they also have been adjusting their portfolios and asset costs for an surroundings through which excessive rates of interest can be a mainstay of the monetary system for fairly a while. This market surroundings could have resulted within the PGIM International Excessive Yield Fund taking some realized or unrealized losses. It might have offset these losses by beneficial properties over the past two months of 2023 although, as traders skilled a euphoria and bid up asset costs within the expectation that the Federal Reserve and different central banks would quickly cut back rates of interest over the course of 2024. This monetary report ought to give us a good suggestion of how nicely this fund dealt with these two differing market environments.

For the six-month interval that ended on January 31, 2024, the PGIM International Excessive Yield Fund acquired $19,811,125 in curiosity and $510,524 in dividends from the belongings in its portfolio. This gave the fund a complete funding earnings of $20,321,649 for the interval. It paid its bills out of this quantity, which left it with $13,858,713 out there for shareholders. That was, sadly, nowhere close to sufficient to cowl the distributions that the fund paid out over the interval. For the six-month interval, the PGIM International Excessive Yield Fund distributed a complete of $20,951,736 to its shareholders. At first look, this could possibly be fairly regarding as we’d ordinarily choose {that a} fixed-income fund absolutely cowl its distributions solely out of web funding earnings. This one clearly failed to perform that job.

Nevertheless, there are different strategies {that a} fund can make use of to acquire the cash that it must cowl its distributions. For instance, it might need been capable of earn some cash by promoting bonds that went up in value resulting from falling rates of interest. These are realized capital beneficial properties and realized capital beneficial properties aren’t thought-about to be funding earnings for tax or accounting functions. Nevertheless, they do characterize cash coming right into a fund that could possibly be paid out to the traders.

Fortuitously, the fund did have some success at acquiring cash by way of these different sources in the course of the interval. For the six-month interval that ended on January 31, 2024, the PGIM International Excessive Yield Fund reported web realized losses of $15,734,609 however these have been greater than offset by $26,498,320 web unrealized beneficial properties. Total, the fund’s web belongings elevated by $3,670,688 after accounting for all inflows and outflows in the course of the interval.

Because the fund’s web asset worth elevated over the interval, it did technically handle to cowl its distributions. Nevertheless, it was solely capable of accomplish this due to the big unrealized beneficial properties that it achieved within the interval. As everybody studying that is little question nicely conscious, unrealized beneficial properties might be erased by any market correction or related occasion. Due to this fact, we are going to need to control the fund’s web asset worth with a view to be sure that it doesn’t start declining an excessive amount of. I’ll admit that I’m slightly extra assured that this fund’s web belongings will maintain up than I’m many others due to its substantial overseas holdings. Nevertheless, we should always not get complacent at any time and will be sure that all the belongings in our portfolio are sustaining the efficiency that we anticipate.

Valuation

As of April 18, 2024 (the latest date for which knowledge is at the moment out there), the PGIM International Excessive Yield Fund has a web asset worth of $12.72 however the shares solely commerce at $11.26 every. This offers the fund’s shares an 11.48% low cost on web asset worth on the present value. This can be a very giant low cost that’s fairly a bit bigger than the 8.35% low cost that the shares have averaged over the previous month. As such, the present entry value seems to be a really affordable value at which so as to add this fund to your portfolio when you want to personal it.

Conclusion

In conclusion, the PGIM International Excessive Yield Fund is a closed-end fund that invests in speculative-grade securities issued by entities which might be situated everywhere in the world. That is a lovely proposition proper now contemplating the threats that the U.S. greenback is dealing with because of the strained monetary state of affairs of the American authorities and the will for diversification that has been expressed by some overseas central banks. This fund is likely one of the few methods to acquire publicity to overseas bonds with out having a major asset base and its yield is increased than index funds or exchange-traded funds. The truth that it trades at a reduction is one other profit.

Total, this fund will in all probability show to be a winner over the long run however after all, it might undergo some short-term weak spot if right this moment’s interest-rate surroundings causes an financial shock.

Editor’s Observe: This text covers a number of microcap shares. Please concentrate on the dangers related to these shares.