Kindamorphic/iStock by way of Getty Pictures

GigaCloud Know-how (NASDAQ:GCT) is a fast-growing firm at an inexpensive valuation. Nonetheless, there’s plenty of controversy surrounding the inventory, and it ought to see some near-term headwinds the following few quarters.

Firm Profile

GCT is a logistics and business-to-business (“B2B”) market operator for big parcel merchandise, corresponding to furnishings and health gear. Its B2B platform connects consumers within the U.S., Europe, and Asia with Asian producers, and it’ll transport merchandise from a producer’s warehouse to finish prospects.

The corporate’s income comes by three main sources. Its GigaCloud 3P income comes from service income for things like warehouse providers, final mile supply, ocean transport providers, and by way of transactions by its B2B market. The corporate additionally sells its personal product stock by its platform. Lastly, it additionally generates off-platform e-commerce income by the sale of its stock on third-party web sites.

On the finish of Q3, the corporate had 31 warehouses in 5 international locations, together with the U.S., Japan, Germany, U.Ok. and Canada.

The corporate was previously often known as Oriental Normal Human Assets Holdings Restricted, and it went public within the U.S. in August of 2022.

Alternatives & Dangers

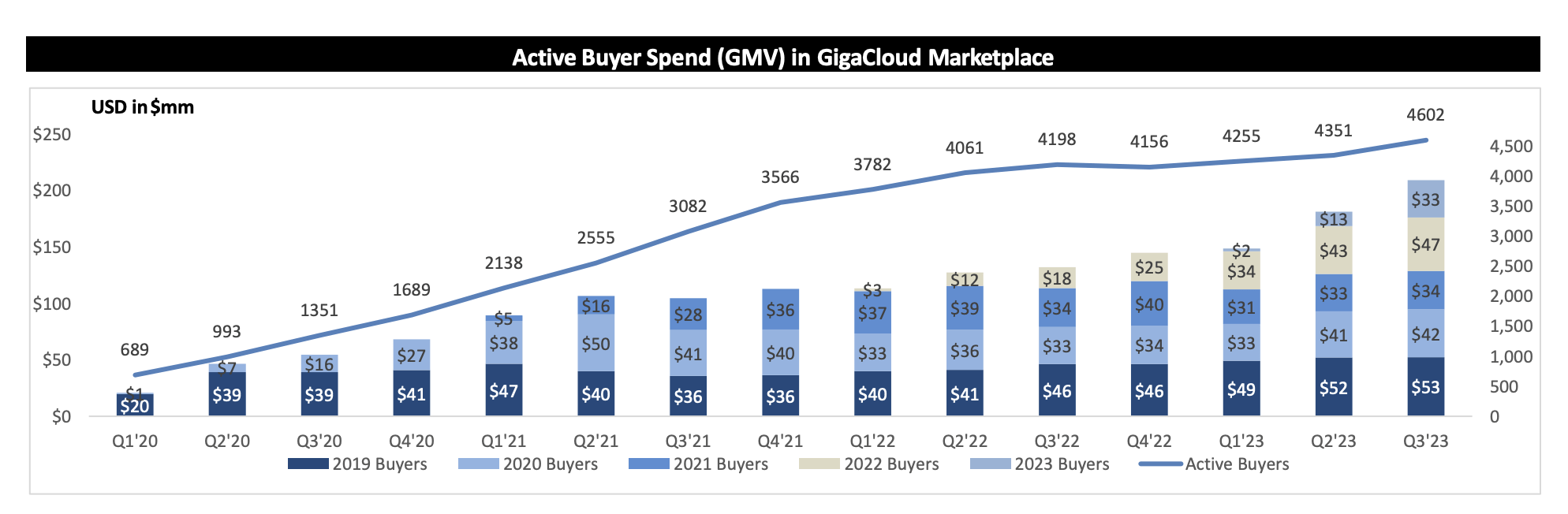

GCT has been rising quickly, propelled by including extra consumers to its platform and consumers spending more cash over time. Final quarter, the corporate added practically 10% extra consumers 12 months over 12 months to 4,602 from 4,198 a 12 months in the past. The corporate says that the majority of its new consumers come from referrals or phrase of mouth, maintaining buyer acquisition prices low.

In the meantime, lively purchaser cohorts spend more cash over time. For instance, lively consumers from its 2019 cohort spent $39 million in Q3 2020, whereas in Q3 2023 they spent $53 million. Spend per lively purchaser has gone from $112,777 in 2020 to a projected $149,000 in 2023.

Firm Presentation

Fueling the corporate’s robust development amongst its cohorts is its provider fulfilled retailing mannequin. This mannequin reduces the variety of contact factors in fulfilling orders when retailers typically should make preparations for final mile supply themselves, whereas GCT handles the whole course of, from the producer to the ocean transport, to the merchandise’ final mile supply to the top person. This reduces general transport prices, which ends up in greater margins for consumers and sellers.

As well as, GCT has began to get into different giant merchandise classes. It initially centered on furnishings, however has since added residence home equipment, residence health gear, and gardening. The corporate sees future alternatives in auto equipment, seasonal décor, and pet provides. Furnishings represents its largest class by far, so these different areas have plenty of potential runway.

GCT can also be seeking to broaden its presence with retailers by two current acquisitions. After the quarter, the corporate acquired the property of B2B furnishings distributor Noble Home from chapter, in addition to digital signage and digital catalog administration Wondersign. Noble Home had relationships with high retailers together with Amazon (AMZN), Goal (TGT), Wayfair (W), Lowe’s (LOW), Past (BYON), and Walmart (WMT) that GCT will look to leverage promoting its items on. In the meantime, with Wondersign, the corporate is trying to make use of its know-how to have the ability to course of e-commerce drop ship transactions in bodily shops.

Total, GCT has been seeing robust development. Income jumped 39.2% in Q3 to $178.2 million. Product income rose 45% to $178.2 million, whereas service income grew 27% to $40.5 million. Adjusted EBITDA , in the meantime, surged 150.4% to $29.8 million.

With regards to dangers, being tied to the furnishings trade is an enormous one. This has been one of many worst performing classes popping out of the recession because of the lack of motion within the housing trade. That is by far GCT largest class, and it’s getting over 75% of its income from first social gathering gross sales. Industrywide furnishings and residential furnishing gross sales have been down –7.3% in November and -4.7% in December.

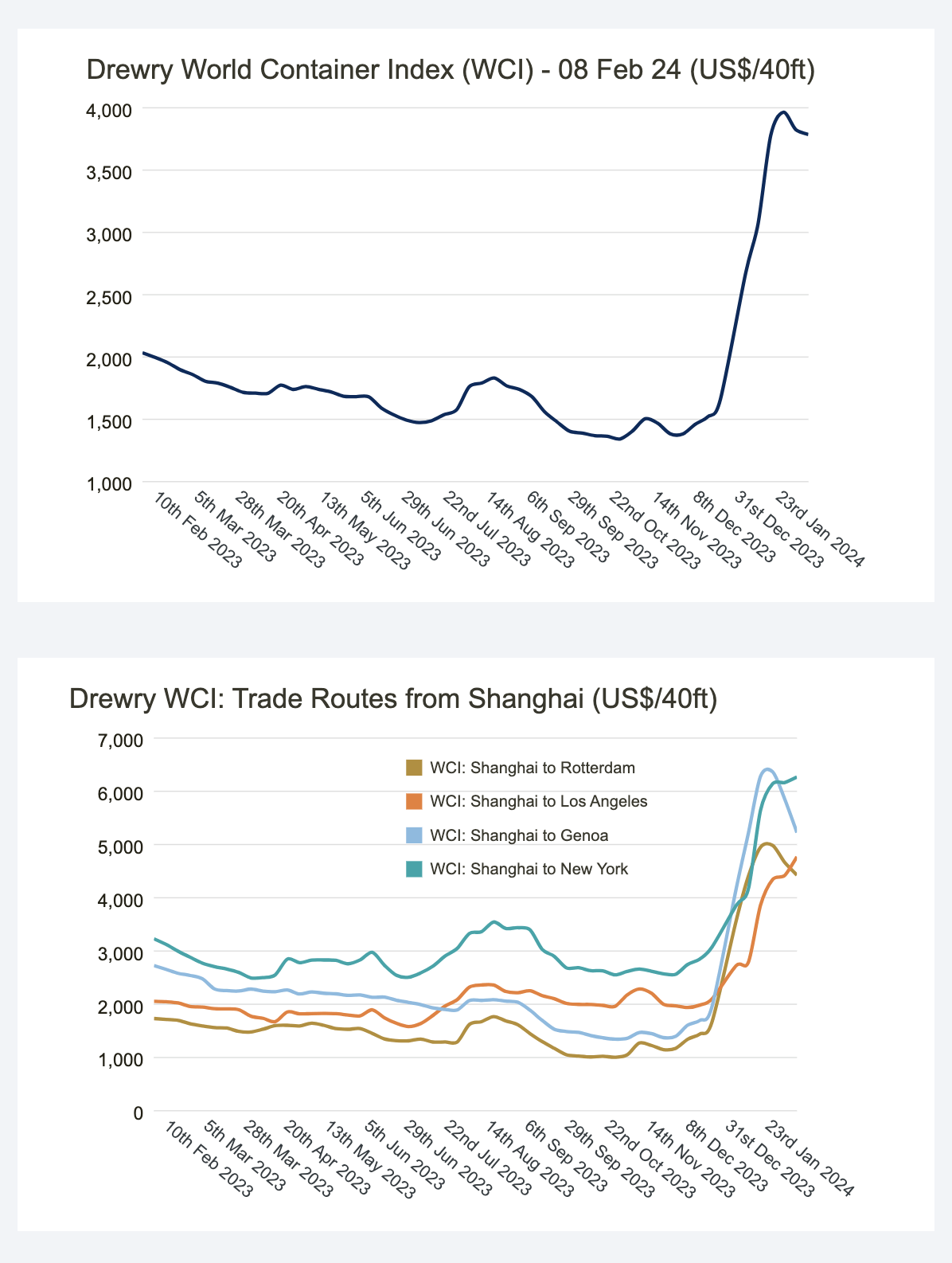

Ocean freight charges is one other danger. GCT had been getting a lift to its gross margins the previous couple of quarters as ocean freight charges had come down from pandemic highs to extra regular stage. Nonetheless, a mixture of points with the Panama Canal and, particularly, ships being diverted from the Crimson Sea because of Yemeni Houthis rebels attacking delivery vessels has seen containership costs skyrocket. Delivery charges from China to the U.S. have continued to remain elevated.

Drewry

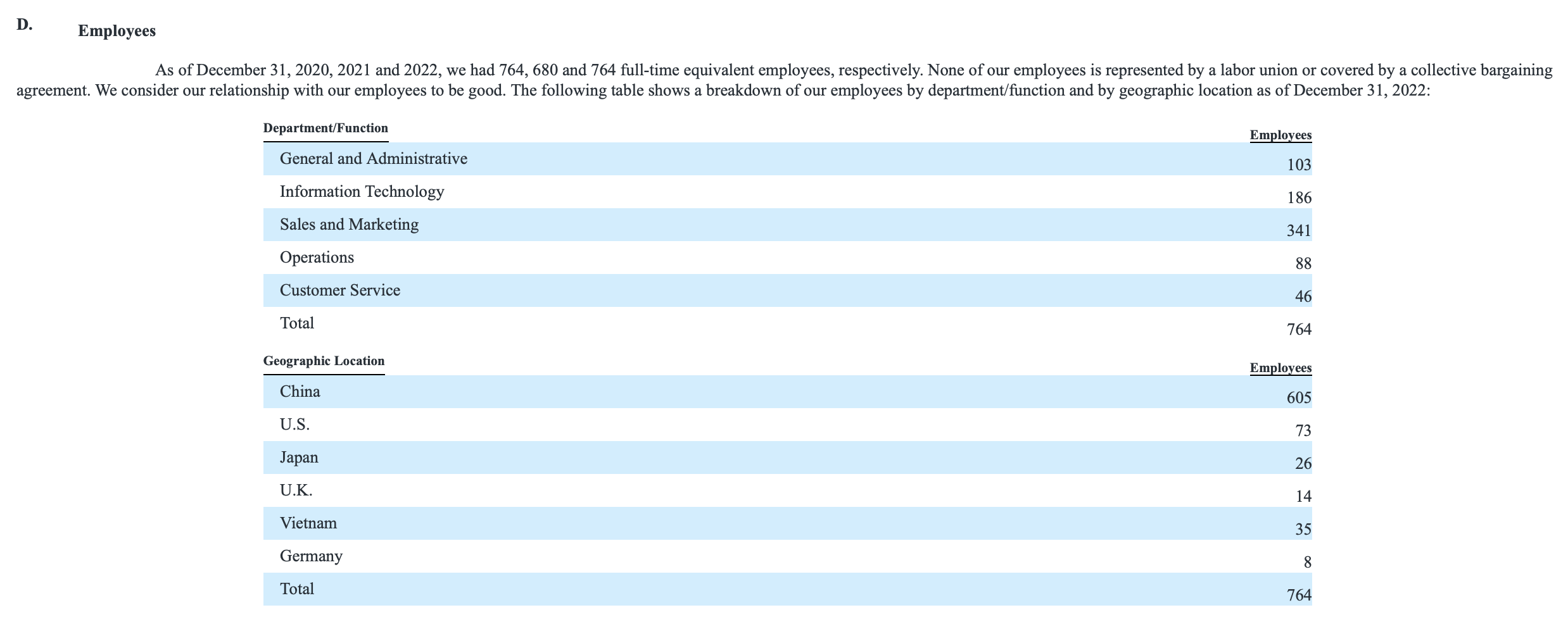

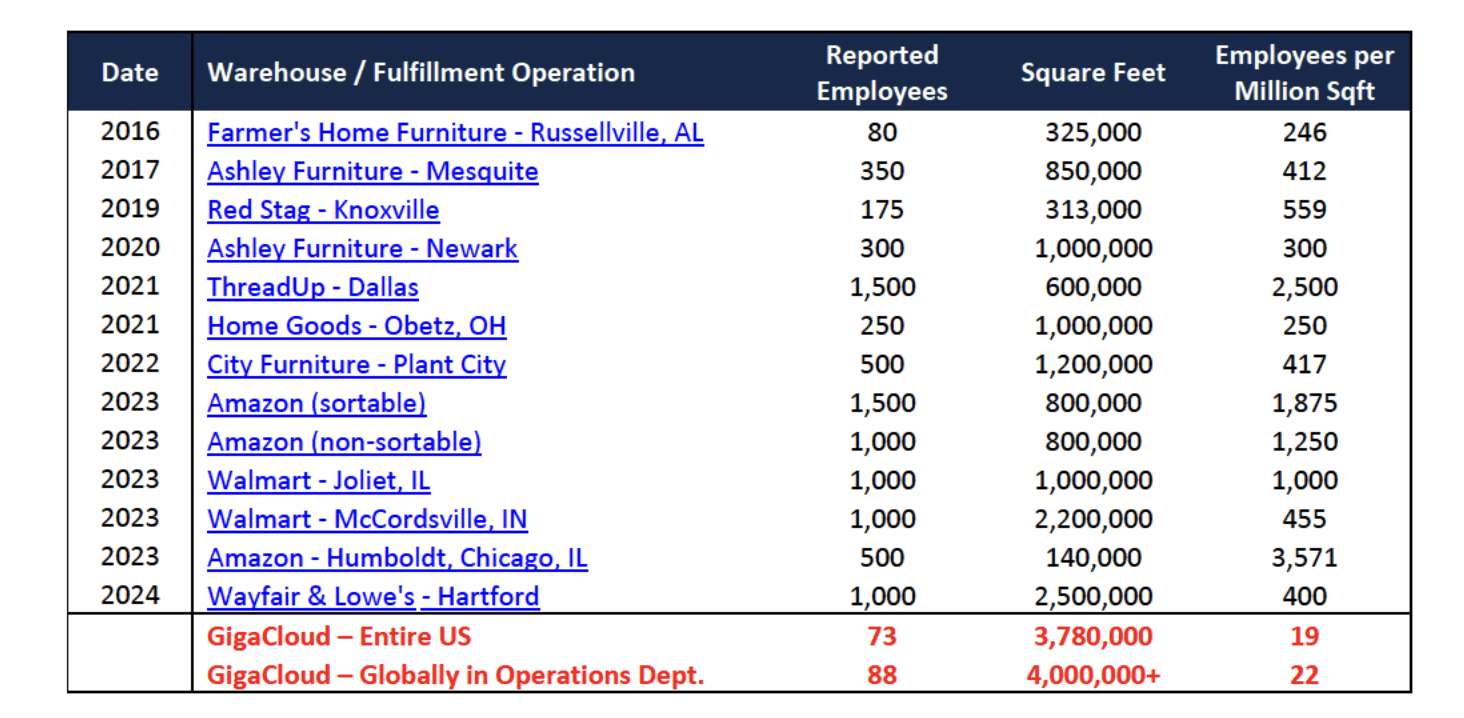

GCT has additionally been the topic of a scathing short report by Culper Analysis. The report accommodates some very intriguing detective work, though except you will spend time sitting exterior GCT’s warehouses, it’s tough to confirm. Nonetheless, one fascinating truth the agency brings up is GCT’s lack of warehouse staff. Culper notes that GCT solely has 73 staff for its 14 U.S. warehouses, which the places in its final annual report final April. That simply doesn’t appear to make any sense in any way, particularly when not all its U.S. staff are warehouse staff, provided that it has an HQ in California. The company’s replies to the quick report, in the meantime, have been very generic.

GCT Staff (Firm 20-F)

Warehouse Staff (Culver Analysis)

Valuation

GCT inventory at the moment trades at 10.6x the 2024 consensus EBITDA of $119.9 million and seven.8x the 2025 consensus of $162.5 million.

It trades at a ahead P/E of 13x the 2024 consensus of $2.42 and 10.4x the 2025 consensus of $3.00.

Income development is anticipated to be 32.4% this 12 months, after which develop 31.5% in 2025.

Given its development price, GCT may simply be valued at double the place it trades at this time. That is in the event you imagine its numbers are correct.

Conclusion

For those who suppose GCT is legitimately going to develop income over 30% per 12 months over the following few years, the inventory is a transparent “Buy” at present valuations. The corporate has mentioned it’ll look to shore up its filings in 2024 with common 10-Qs and 10-Ks, the identical as a home filer, so there may very well be extra transparency, which may result in upside.

Nonetheless, when you have considerations in regards to the legitimacy of the corporate, then I’d keep away. In spite of everything, this can be a firm with a technology-sounding title that in actuality is promoting and fulfilling orders for Asian furnishings with only a few warehouse staff and little spending on gross sales & advertising (6% of income) in a horrible marketplace for residence furnishings gross sales. One in all its massive plans to drive development, in the meantime, is coming from the property of an organization it purchased out of chapter. Anecdotally, GTC’s B2B marketplace website is fairly primary and really gradual, so it’s not precisely leading edge.

GCT’s inventory has completely crushed any shorts because the Culper Analysis report. That doesn’t show its discovering are improper (or proper for that matter). Nonetheless, it does present the danger of being quick an optically low-cost title that on the floor is rising shortly.

Total, I’d keep distant from the inventory. On the very least, it ought to really feel gross margin stress from the rise in containership costs. As such, I price the inventory a “Sell.”