fotostorm

Thesis

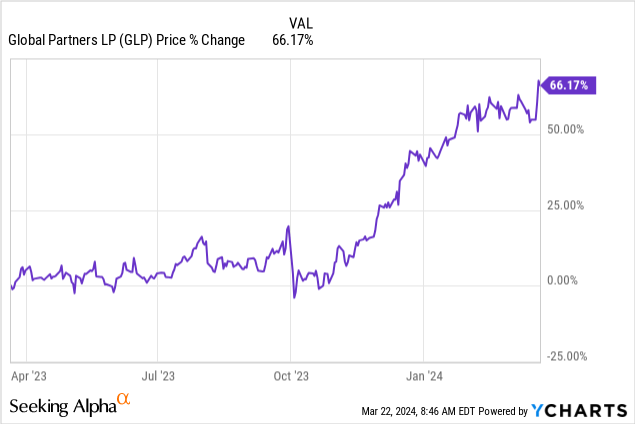

International Companions (GLP) is a U.S. Grasp Restricted Partnership (‘MLP’) which features as an proprietor, provider and operator of gasoline stations and comfort shops. The MLP has seen its widespread shares rocket upwards prior to now 12 months, on the again of higher than anticipated profitability and growth plans:

As an MLP, the corporate runs a considerable amount of debt, structured as revolving credit score strains, debentures and most popular shares. The corporate presently has two collection of most popular shares excellent, with the Collection A set to be retired on April 15, 2024. We lined GLP.PR.A in a separate article here, the place we outlined why we had been anticipating the debt to be known as.

For a retail investor who missed the rally within the widespread shares, there is just one collection of most popular shares excellent now, specifically Collection B (NYSE:GLP.PR.B). On this article we’re going to take a look on the construction of the popular shares, their analytics, and the explanations for which we discover them engaging from each an organization perspective in addition to a macro perspective.

MLP most popular shares – what you need to look out for

MLPs or Grasp Restricted Partnerships, signify corporates that do not pay federal earnings tax, however fairly see their income and losses handed by means of to traders, who then pay taxes on their share of the earnings. This ‘cross by means of’ mannequin applies for companies that generate a gradual, predictable stream of earnings. Thus many MLPs are concerned within the vitality sector, proudly owning belongings like pipelines, storage tanks, and even oil and fuel properties.

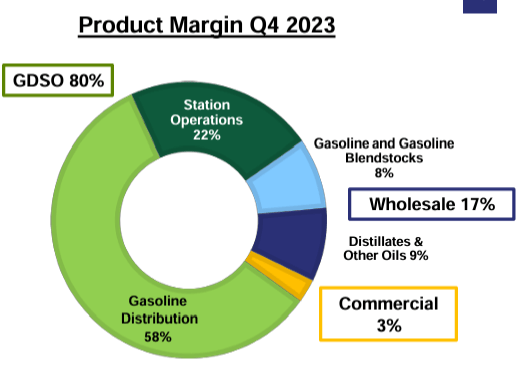

GLP is among the largest operators of gasoline stations and comfort shops within the U.S. Northeast, and derives most of its product margin from gasoline distribution:

Product Margin (Firm Presentation)

The MLP mannequin depends on a gradual stream of cash-flow and on comparatively excessive ranges of debt. Previous to the Covid disaster many MLPs had been working debt/EBITDA ratios in extra of 4x, however these figures have come down after lots of the corporates experiencing potential chapter situations.

Most well-liked shares are categorized as fairness on the steadiness sheet when they’re perpetual, and thus are usually not included within the debt/EBITDA ratio. GLP had points two collection of most popular shares, particularly as a result of they’d not have an effect on debt/EBITDA.

The corporate nevertheless has skilled progress, with a rise in EBITDA figures, which has moved its debt ratio to a really conservative stage:

Leverage Ratio (Firm Presentation)

When investing in MLP most popular shares, an investor must be conscious of 1 massive threat issue, specifically Chapter 11 restructuring/chapter. Outdoors of a chapter continuing, most popular shares may be seen akin to lengthy length debentures.

Many MLPs skilled misery through the Covid disaster as a result of the income figures decreased, however extra importantly as a result of the debt on the steadiness sheet was not structured correctly, with many close to time period maturities. Firms used to like close to time period maturities as a result of the price of funds was low-cost. They realized there’s a enterprise price to that in Covid.

New debt issued used to retire most popular shares

GLP is conscious about sensible steadiness sheet administration, and has $400M of seven.00% senior notes due 2027 excellent, and $350M 6.875% senior notes due 2029. Along with the above time period debt with maturities above 3 years, the corporate lately issued in January 2024 $450 million of 8.250% senior unsecured notes due in 2032:

The corporate mentioned that it intends to make use of the online proceeds from the providing to repay a portion of the borrowings excellent beneath its credit score settlement and for common company functions.

Whereas a few of the proceeds had been used to repay quantities excellent beneath the credit score facility, a portion of the debenture money was used to retire the GLP.PR.A most popular shares, given their present yield in extra of 10%.

Please observe the attractiveness of the debenture yield, with the corporate with the ability to subject 8 12 months debt at Treasuries+3%. The rationale for this issuance is the retirement of costly funding on the again of a low leverage ratio.

Given its conservative steadiness sheet administration, elevated progress and lengthy dated debenture maturity profile, we don’t count on GLP to subject most popular shares in right now’s surroundings, leaving simply GLP.PR.B excellent.

State of the steadiness sheet

Retail traders have entry to the GLP steadiness sheet and earnings assertion through the In search of Alpha platform within the Financials Tab. If one seems to be on the historic development for the online debt on the GLP steadiness sheet they may discover a relentless determine of roughly $1.5 billion:

Web Debt (In search of Alpha)

The above are annual figures, they usually have remained pretty fixed. What has modified although is EBITDA, which has grown considerably:

EBITDA (In search of Alpha)

Whereas the debt determine has stayed pretty fixed, EBITDA has grown by 40%, thus making the debt protection ratios for the corporate way more engaging, and decreasing the necessity for most popular share utilization within the capital construction.

How does GLP.PR.B examine to different most popular shares

Not like ETFs or CEFs with related mandates, particular person corporates are usually not fungible, particularly within the area of interest MLP house. We’re not conscious of one other gasoline distributor MLP that may have most popular shares excellent, thus GLP is a reasonably distinctive firm which must be assessed by itself threat and rewards. Using transportation MLPs as a comparability wouldn’t be right since pipeline firms have a unique income stream mannequin when in comparison with GLP.

At what level we might be much less serious about shopping for GLP.PR.B

As described within the yield analytics part under we count on a 3 12 months tenor for the popular shares, which presently values them from a yield perspective at T+4.5%. Given excessive yield spreads are at 300 bps, the unfold pick-up is 150 bps towards common excessive yield collateral. The unfold is justified given the capital construction allocation and waterfall of funds in case of a chapter. A selection under 100 bps can be thought of too tight for us, so we might not purchase GLP.PR.B at present yields under 8.5% within the present unfold surroundings.

Ahead-looking expectations for the corporate

The corporate has confirmed to be a savvy operator through its EBITDA growth, on the again of a relentless debt utilization. This progress has been absolutely mirrored in its widespread fairness, as illustrated through its 66% acquire prior to now 12 months.

For most popular fairness holders the corporate progress is just not that essential since there isn’t a upside with a name value at $25/share. Nonetheless, because the article describes the solvency of the entity is what issues. With a debt maturity profile layered out sooner or later (the primary debenture matures in 2027), there’s nothing from a steadiness sheet perspective that may represent a trip-wire within the close to future.

Profitability will probably be monitored through web earnings figures in addition to debt service protection ratios and free money circulation working figures to make sure ample protection of debt service.

Enticing yield for the Collection B most popular shares

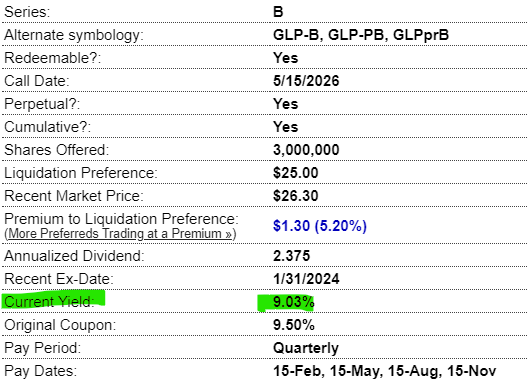

The Collection B are fastened price cumulative most popular items issued at 9.5% coupon however with a 9% present yield:

Yield (PreferredStockChannel)

The collection are properly set-up for the present macro surroundings the place price hikes are behind us, with the Fed now discussing when price cuts will start precisely in 2024. Mounted price debt will profit because the Fed lowers Fed Funds.

It’s attention-grabbing to notice how properly the market perceives GLP, given the very slim unfold of round 100 bps between the 2032 debt and the popular shares. The broader this unfold the upper the perceived riskiness of an issuer. Why? As a result of in a Chapter 11 restructuring debt holders are set for a really excessive restoration for asset wealthy firms like GLP, whereas most popular fairness could be very prone to get fully worn out.

Whereas widespread fairness embeds progress prospects, and now we have seen GLP widespread shares rally exhausting, the popular fairness acts like debt for wholesome firms. In right now’s macro surroundings selecting up 9% yielding most popular shares with an estimated length of three years is a horny threat/reward proposal. Whereas the primary name date is barely 2 years away, we don’t suppose GLP will name the collection straight away, ready for decrease threat free charges, thus we’re including a 1 12 months tenor to the preliminary name date.

Conclusion

GLP is an MLP that operates gasoline stations and comfort shops within the U.S. Northeast. The corporate has skilled EBITDA progress, which has lowered its debt ratios and has boosted its widespread shares. The corporate is a really sensible steadiness sheet supervisor, having termed out its debt, with the most recent issuance coming in January 2024. A part of the proceeds from the most recent debentures will probably be used to retire the Collection A most popular shares on April 15, 2024. Retail traders having missed the widespread shares rally can have a look at the one remaining collection of most popular shares, specifically GLP.PR.B. The shares yield 9% and have a 2026 first name date, with our base case expectation for an precise 2027 retirement/name. Underneath the present steadiness sheet construction we see no threat that may put GLP right into a Chapter 11 restructuring till the anticipated GLP.PR.B redemption, thus making the remaining most popular shares a really engaging threat/reward proposal in right now’s macro cycle the place price cuts are anticipated.