Nikada

Goldman Sachs BDC (NYSE:GSBD) is a comparatively large-scale BDC, which as of December 2023 ranks because the tenth largest BDC car when it comes to the market cap.

GSBD invests primarily in US mid-cap corporations (simply as most BDCs), with an EBITDA technology of between $5 million and $75 million. The EBITDA vary for this BDC is kind of huge implying fairly agnostic view on the scale of those mid-cap companies.

GSBD Investor Presentation

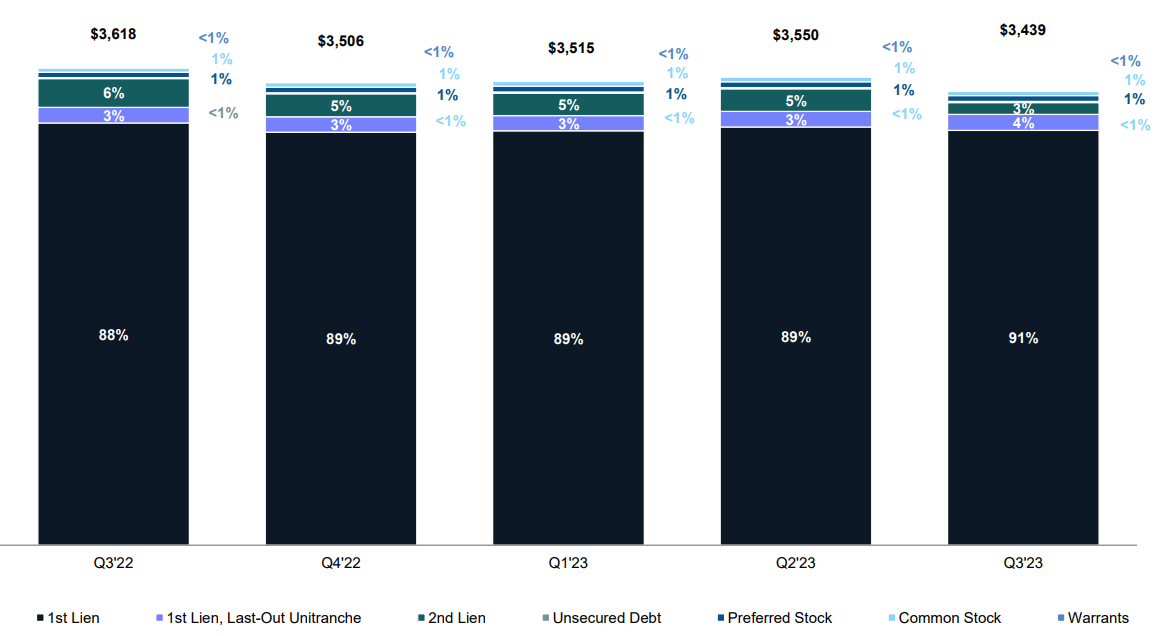

The publicity to the primary lien debt has been secure and appreciable already for some time, revolving round 90% territory. This type of portion in first lien could possibly be simply considered as one of many biggest ones in the whole BDC area because the common lies someplace between 70 – 80%.

GSBD Investor Presentation

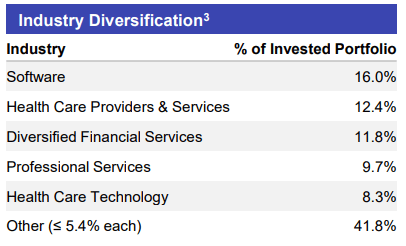

Along with the safeness that’s related to first lien constructions, GSBD carries a comparatively diversified portfolio, the place the businesses are properly distributed throughout numerous industries.

From Prime 3 industries, just one – i.e., software program – embodies inherently extra dangerous traits than a mean business, which are likely to have secure and simple enterprise fashions.

GSBD Investor Presentation

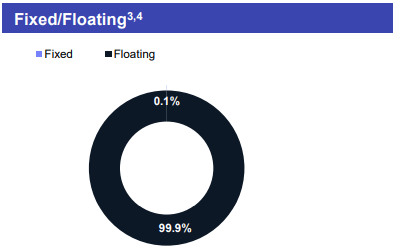

Furthermore, virtually the whole AuM base is comprised of floating devices, which have positively helped GSBD capitalize on the prevailing tailwinds related to excessive rate of interest surroundings. Plus, whereas rates of interest are seemingly set to normalize (i.e., go decrease) and thus there could possibly be some yield reductions in GSBD’s portfolio, in absolute phrases the yields ought to nonetheless stay at very stable ranges (except SOFR drops to zero).

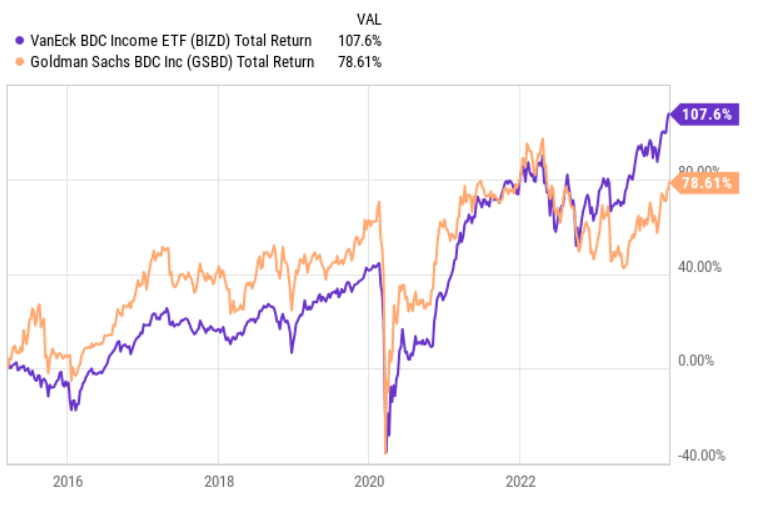

Ycharts

Nonetheless, if we take a look at the overall return chart above, we will discover very attention-grabbing dynamics:

- Within the pre COVID interval, as soon as the rates of interest had been extraordinarily accommodative, GSBD managed to constantly outperform the broader BDC index.

- Publish COVID, GSBD has struggled to ship alpha and actually as soon as the rates of interest began to surge, the Fund has considerably diverged from the remainder of BDC market.

I discover this fairly attention-grabbing given virtually 100% publicity to floating charge devices, which ought to theoretically enable GSBD to totally seize the present tailwinds warranting the alpha factor (as in lots of situations BDCs nonetheless carry fastened charge investments).

Thesis

Let me know clarify why that is the case and why I might not suggest proudly owning GSBD at this second.

In a nutshell, it’s the mixture of extreme leverage and relaxed requirements with respect to funding underwriting.

The standard of portfolio corporations has clearly deteriorated within the current quarters. For instance, the focus of GSBD corporations in third and fourth score buckets has elevated from 3.9% to 9% in simply 9-month interval.

GSBD Investor Presentation

Based on GSBD explanation, “rating 3” implies the next:

- Funding’s threat has elevated materially since origination or acquisition. Borrower could also be out of compliance with debt covenants; nonetheless, funds are usually no more than 120 days overdue.

“Rating 4” class is clearly even worse.

Trying on the portfolio traits beneath it shouldn’t be an enormous shock that we see worsening situations inside GSBD’s portfolio.

GSBD Investor Presentation

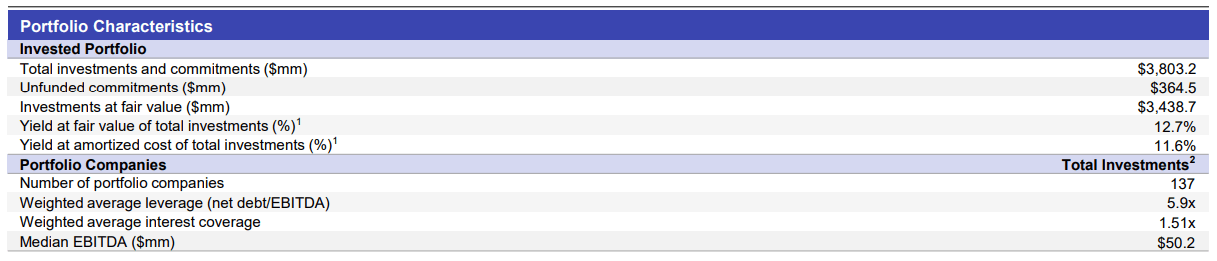

For instance, the truth that weighted common curiosity protection of all portfolio corporations stands at just one.51x signifies already there a big threat within the total construction. The online debt to EBITDA can be on the aggressive finish with 5.9x as of Q3, 2023.

I must also underscore that the standard in relation to the debt and protection metrics is just not getting higher both. The weighted common curiosity protection of the businesses at quarter finish dropped from 1.56x to 1.51x as indicated above.

Now, whereas the leverage of GSBD has certainly improved, the prevailing ranges are nonetheless skewed in direction of the aggressive finish with debt to fairness round 117%. That is barely above the sector average.

Given the low margin of security in portfolio corporations that’s related to very slender rate of interest protection ratios and excessive indebtedness, having aggressive leverage is just not optimum.

As a pure consequence of the aforementioned scenario, Tucker Greene – COO – commented on the rising quantity of non-accrual (as per the current earnings call):

And eventually, turning to asset high quality. As of September 30, 2023, two new positions had been positioned on non-accrual and one portfolio firm was faraway from non-accrual throughout Q3. Investments on non-accrual standing amounted to 2.3% and 4.2% of the overall funding portfolio at honest worth and amortized value respectively.

Within the context of total BDC area, 4.2% of non-accrual at amortized value may be very excessive.

GSBD Investor Presentation

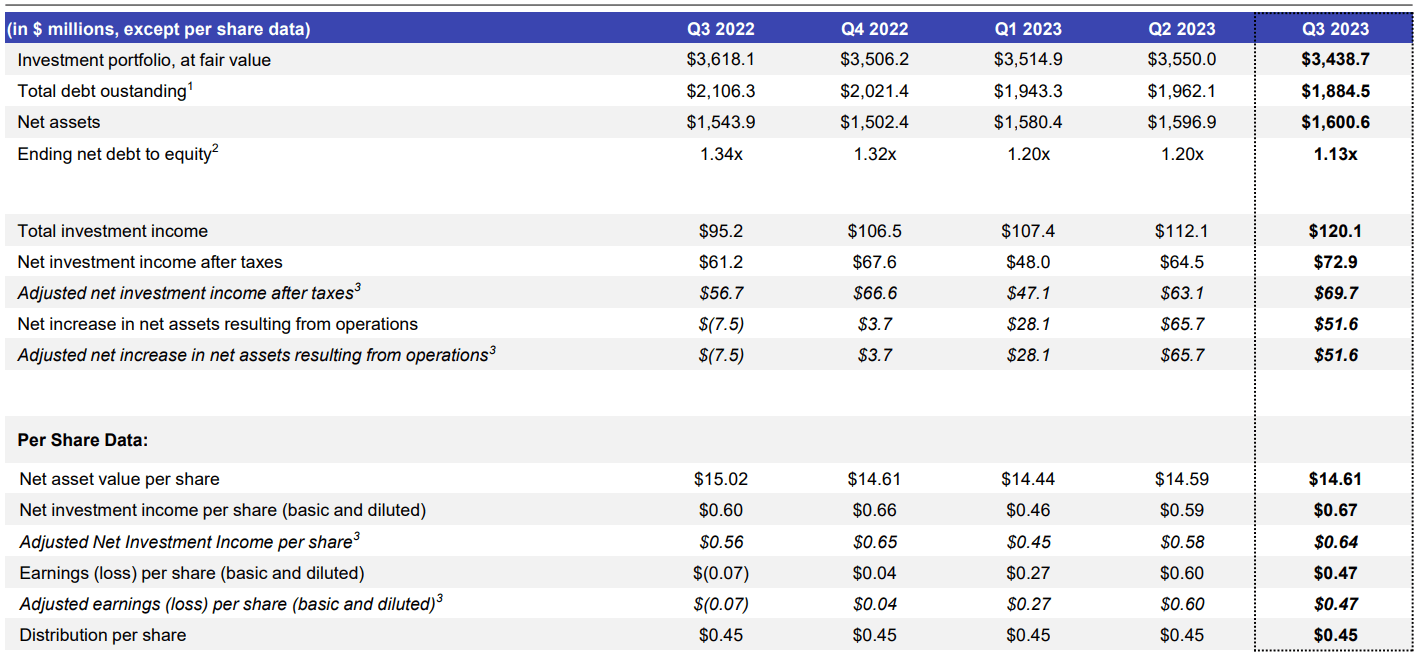

Lastly, to make the issues worse, GSBD has just lately skilled some struggles with the dividend protection (i.e., in Q1, 2023, when the adjusted NII barely coated the underlying dividend due to extra extreme write-downs). On an adjusted earnings per share foundation, the dividend protection seems much more pessimistic.

Whereas at the moment GSBD stays at a protected territory particularly based mostly on the Q3, 2023 knowledge, it is usually clear that as quickly as extra write-offs emerge, the sustainability of the dividend will grow to be questioned.

The underside line

GSBD has a sound portfolio construction when it comes to the large publicity to first lien and nice business diversification coupled with 100% floating investments, which make it simpler to profit from the excessive rate of interest surroundings.

However, the prevailing development in portfolio high quality, the place an rising quantity of investments are labeled below dangerous class and are written down make this BDC an unattractive funding. Extreme leverage and poor debt protection metrics of portfolio corporations might doubtlessly amplify these penalties within the state of affairs of contracting financial system.

The market appears to have already acknowledged this as since early 2022 GSBD is in a continuing destructive alpha territory. The truth that GSBD trades at a slight premium to NAV of 1.04x doesn’t make this story higher.