SOPA Photographs/LightRocket through Getty Photographs![]()

I’ve kicked off this 12 months of investing by together with Alphabet, the guardian firm of Google (NASDAQ:GOOGL) (NASDAQ:GOOG), in my Top 3 Picks for 2024.

I’m satisfied that 2024 is the 12 months Google will profit from additional ad-spending restoration, a contested presidential election within the US, and elevated effectivity and ad-targeting led by AI enhancements.

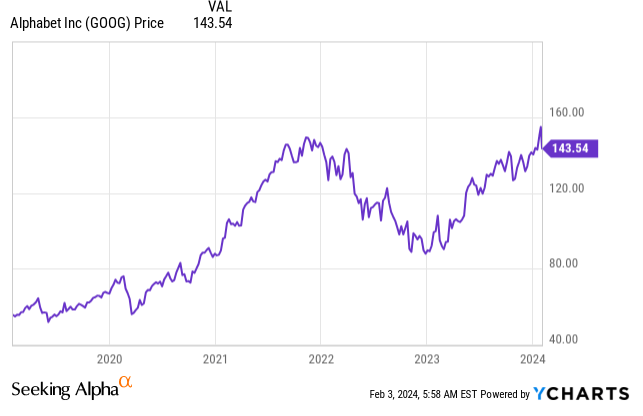

The corporate has simply reported Q4 and full-year 2023 earnings, and the outcomes got here in very positively, with a 13% income development in This autumn and EPS up 56% YoY. For the complete 12 months, income is up 10%, and EPS is up 27%.

These are nice outcomes, if I had been to guage; but, the inventory has dropped from its 52-week excessive of $154 right down to $143, or roughly an 8% pullback.

Worth Growth (Searching for Alpha)

With the year-end 2023 rally and a robust begin to 2024, the valuations of the Magnificent 7 have change into stretched, and nothing lower than stellar earnings would keep away from punishment.

That’s exactly what occurred. Google delivered good outcomes, however they weren’t stellar, as Google promoting dragged a bit on total income development, solely up by 11% to $65.5 billion, falling in need of expectations for $65.8 billion.

So, let’s study whether or not this presents a great shopping for alternative for what I imagine ought to be an incredible 12 months for promoting companies in 2024.

This autumn Earnings

We have been via this example earlier than, do you recall?

Within the earlier quarter, Google posted sturdy Q3 earnings, however its inventory confronted a 15% drop from its peak of $142, plunging to $121. This downturn resulted within the firm shedding greater than $180 billion in market capitalization inside per week.

Throughout that interval, the decline within the inventory worth was primarily linked to Google’s Cloud unit, which did not develop as quickly as anticipated. It was the one phase that fell in need of Wall Avenue’s consensus expectations, regardless of a good 11.1% income development for the quarter.

Again then, I wrote an article titled “Why I’m aggressively buying the dip,” and since its publication, I’ve seen my funding return by over 11%.

As we speak, the narrative is strikingly related as soon as once more. Let’s guarantee we draw classes from the previous and seize the chance.

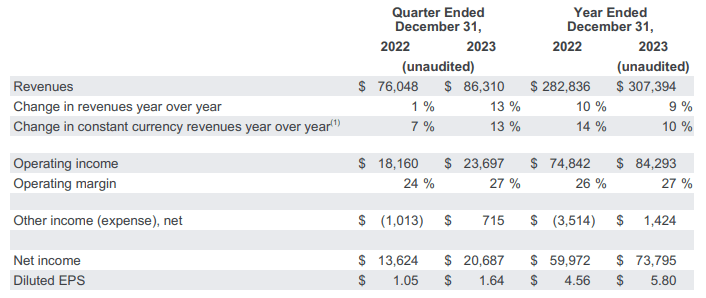

In its Q4 earnings report, Google has achieved a 13% enhance in total income to $86.3 billion.

This marks the corporate’s quickest development within the final six quarters.

Quarterly Progress (CNBC)

The income has surpassed Wall Avenue expectations of 12% development, and the working earnings has surged by 30% to $23.7 billion, with an working margin of 27%, marking a 300 foundation factors enhance YoY.

Internet earnings has reached $20.7 billion, reflecting a 52% development YoY, and the EPS of $1.64 has exceeded analysts’ expectations by $0.04.

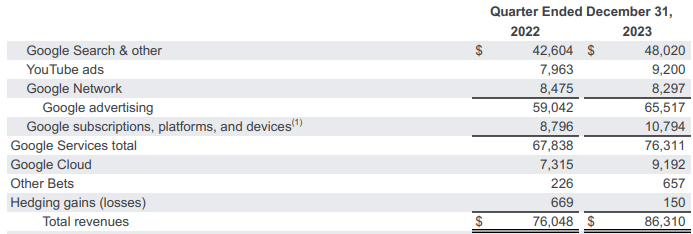

This autumn Earnings (GOOGL IR)

Within the broader context, Google’s efficiency in This autumn has been strong, significantly when in comparison with earlier quarters. That is confirmed by the just about solely double-digit development in every phase:

- Google Search & Different skilled development of 12.7%, reaching $48 billion.

- YouTube adverts exhibited even quicker development, hovering by 15.5% to $9.2 billion.

- The Google Community phase was the one space that confronted a decline, dropping by -2.1% to $8.3 billion, a development we’ve got noticed for a number of quarters.

- Google Cloud delivered development of 25.6% and generated $9.2 billion in income, surpassing the 22.4% development in Q3 and marking a reversal in slowing development.

This autumn Earnings by Section (GOOGL IR)

Now, one may ask, if the earnings had been so good and largely beat analysts’ expectations, alongside the reaccelerating development within the cloud unit, why did the inventory expertise a major 8% pullback because the report got here out?

The expectations going into the earnings had been fairly excessive; the valuation of the Magnificent 7 corporations has change into comparatively stretched. Something higher than stellar earnings and beating expectations can be punished, as we’ve got noticed with different shares.

| Firm: | 2022-2023 P/E | Present P/E | CY24E EPS Progress |

| Microsoft (MSFT) | 32.0x | 37.8x | 14% |

| Apple (AAPL) | 25.2x | 29.6x | 7% |

| Amazon (AMZN) | 51.9x | 57.2x | 40% |

| Tesla (TSLA) | 88.5x | 60.2x | 1% |

| Nvidia (NVDA) | 56.8x | 53.6x | 67% |

| Meta (META) | 20.8x | 31.0x | 33% |

Google’s blended P/E heading into the earnings was 26.2x, or one may say “priced to perfection,” marking a major enhance from the 23.2x its earnings we had been accustomed to between 2022 and the top of 2023.

With the valuation stretched, the corporate needed to ship, and Google did produce good outcomes. Nonetheless, Google’s whole promoting income barely impacted total income development, rising by solely 11% to $65.5 billion, falling in need of expectations for $65.8 billion, or even perhaps an overdelivery.

But, there have been highlights, reminiscent of the expansion in YouTube Adverts and Google’s Cloud unit, which carried out higher than expectations.

In the end, the 8% pullback will not be a response to poor outcomes; as an alternative, it signifies a normalization of expectations. In my view, we may even see extra of this throughout this earnings season as expectations are excessively stretched.

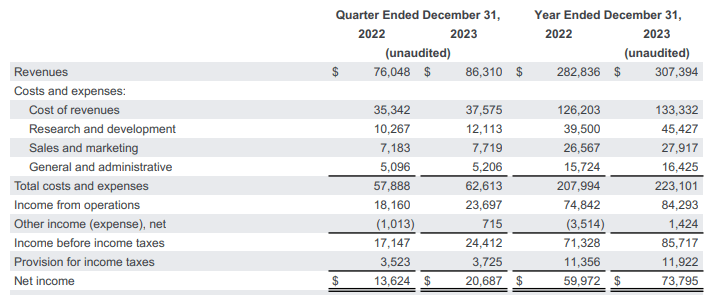

One factor I’m keeping track of heading into 2024 is Google’s elevated R&D spending, which got here in This autumn at $12.1 billion, displaying a 17.5% YoY enhance. This might pose a problem to the working margins.

This autumn Bills (GOOGL IR)

The corporate has additionally highlighted a rise in CapEx spending, reaching $11 billion in This autumn, because it strives to catch up within the AI race. This surge is predominantly fueled by investments in technical infrastructure, with servers being the most important element, adopted by knowledge facilities.

The elevation in CapEx throughout This autumn displays their anticipation of the extraordinary purposes of AI, aiming to ship advantages for customers, advertisers, builders, cloud enterprise prospects, and governments globally. It underscores their perception within the long-term development alternatives introduced by AI.

Waiting for 2024, Google anticipates that CapEx funding will notably exceed the figures from 2023. This development is predicted to be constant amongst most Magnificent 7 corporations as they place themselves on the forefront of innovation.

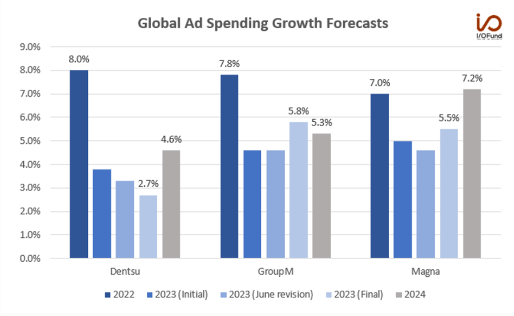

But, I’m optimistic about 2024, as advert spending development is broadly forecasted to speed up. The market appears to be cheering for a return to increased development in 2024, pushed by new synergies from generative AI promoting choices from Large Tech, and pockets of stronger development in digital and retail media advert spend.

Growth forecasts from Magna, Dentsu, and GroupM usually level to an acceleration subsequent 12 months, averaging round 5.7% between the three, in comparison with 4.7% in 2023.

International Advert Spending Forecast (Forbes)

As we look into 2024, a pivotal election 12 months within the US, it is clear that the stage is ready for intense political discussions amid the prevailing points within the nation. Firms targeted on promoting are more likely to achieve considerably from the surge in on-line campaigning. Meta is predicted to be among the many key beneficiaries on this situation.

Valuation

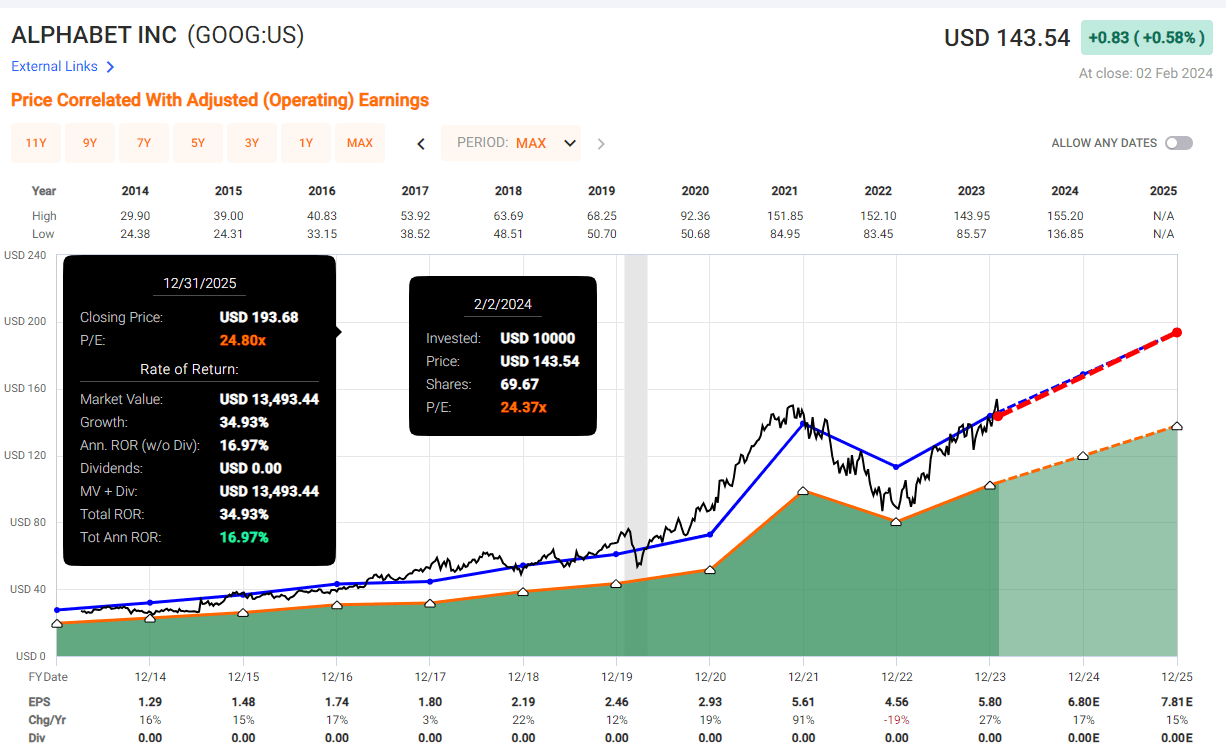

As you’ll be able to see from the desk above, Google is at present essentially the most reasonably priced among the many Magnificent 7 shares.

After the pullback, the inventory is trading at 24.3x its blended P/E ratio.

Since 2013, the typical valuation has stood at 24.8x its earnings, with a mean annual development fee of 17.7% in EPS over the identical interval.

Following a strong restoration in 2023, with a 27% enhance in EPS, the expansion will not be anticipated to decelerate:

- 2024: EPS of $6.80E, YoY development of 17%.

- 2025: EPS of $7.81, YoY development of 15%.

- 2026: EPS of $8.98E, YoY development of 15%.

The upward trajectory of this development signifies that the historic valuation of 24.8x offers an affordable estimate for the place the inventory is more likely to commerce sooner or later, given the anticipated sustained development.

This situation means that we are able to count on annual returns of roughly 17% till 2023, making it one of the crucial promising prospects among the many Magazine 7 shares.

Setting a short-term goal, I intention for the inventory to succeed in $170 by the top of 2024.

Whereas the inventory appears to be buying and selling at a good valuation, the continued development is predicted to drive capital appreciation. If Google had been to comply with in Meta’s footsteps and provoke its first-ever dividend, there may be potential for a 0.5-1% yield over the following couple of years, accompanied by substantial buyback exercise.

Valuation (Quick Graphs)

Takeaway

Google simply dropped 8% after reporting its This autumn earnings.

For my part, it is a justified dip as a result of, let’s face it, the inventory was a bit overpriced heading into the earnings, in comparison with what we have been used to up to now couple of years.

Now, the earnings report itself was good – a strong 13% income development, nothing mind-blowing although. However this is the twist: the drop in inventory worth is not an indication of doom and gloom for Google’s future. As an alternative, it is a actuality test, a recognition of extra normalized development ahead.

Apparently, as of now, Google’s inventory is the most affordable among the many Magnificent 7 corporations.

I am optimistic about Google’s future, particularly in 2024. I am betting on a dynamic 12 months forward, partly fueled by the anticipated intense US presidential election and a lift in advert spending.

Seizing the second, I’ve doubled down on my Google holdings after the earnings report. Google is now one in all my prime holdings, and I am setting my sights on a $170 goal by the top of the 12 months.