Anadolu/Anadolu by way of Getty Photographs

Since its IPO in 2004 folks have been saying Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL), then Google, has been overhyped, that search cannot proceed at this tempo, and that the market cap is simply too excessive. This complete time, Alphabet has been a transferring mountain persevering with to ship quarter after quarter and 2023 was no totally different. Within the wake of AI product roll-outs like ChatGPT and different AI instruments in late 2022, buyers continued to activate Alphabet’s Google Search cash maker. But full year 2023 outcomes demonstrated the negativity is unwarranted and Google Search continues to run. Couple that with the large tailwinds within the YouTube Premium house, there are a number of avenues for Alphabet’s advert enterprise to proceed its dominance. Then there’s Google’s cloud providing, GCP, which expanded revenues by over 26% and has sniffed out profitability for the first time this 12 months. Coupling all that income development with capital reinvestment in different bets companies and share buybacks lowering the float, it’s no marvel EPS grew 27% 12 months over 12 months. The inventory continues to development in the proper course.

Those that have been watching the inventory after earnings on January thirtieth know the inventory ended the week 7% decrease. The latest dip in inventory worth appears overdone and can present a gap for these searching for a 5-10-year maintain. Bringing it again to the shorter time period, Alphabet’s execution of the company technique underpins a $7.50 EPS estimate for 2025. Sustaining the present 25x worth to earnings (P/E) a number of into the longer term would elevate Alphabet’s inventory worth to $185-$190/share over the following two years. This transfer represents a 31% enhance within the inventory in comparison with at this time’s worth of $143. Sure, I just like the inventory.

Firm Overview

Alphabet is a global-spanning know-how conglomerate. The most important chunk of the corporate holds Google, the search engine enterprise the corporate was constructed upon. Right now, it holds different organizations that span totally different focuses from Google Workspace, internet hosting of content material creation, enterprise capital, and autonomous driving. The record of firms beneath Alphabet is lengthy, therefore the 26 letters within the alphabet. Just a few of the bigger well-known companies beneath Alphabet to notice are Android, YouTube, Nest, Fiber, Google Ventures, and Waymo.

A listing of Alphabet Subsidiary Firms (Google Search)

However is not Alphabet solely Google Search?

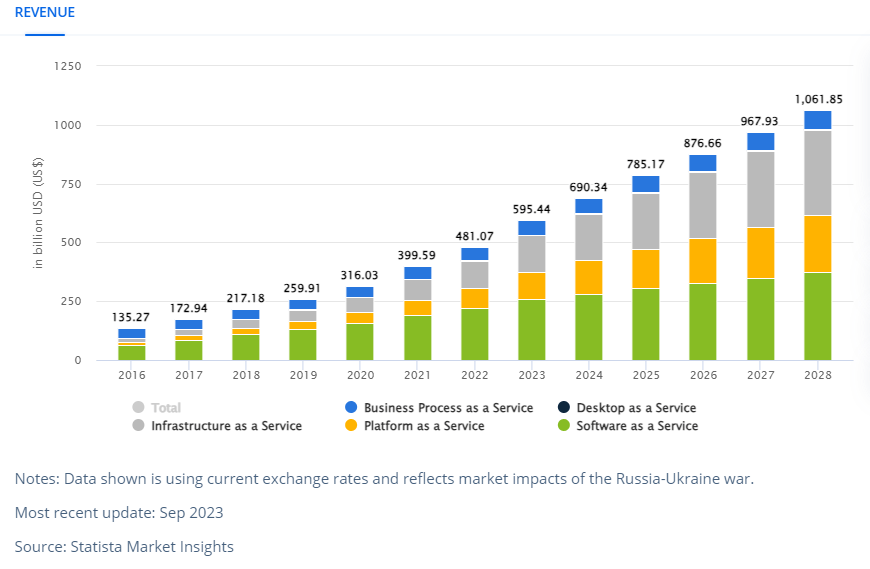

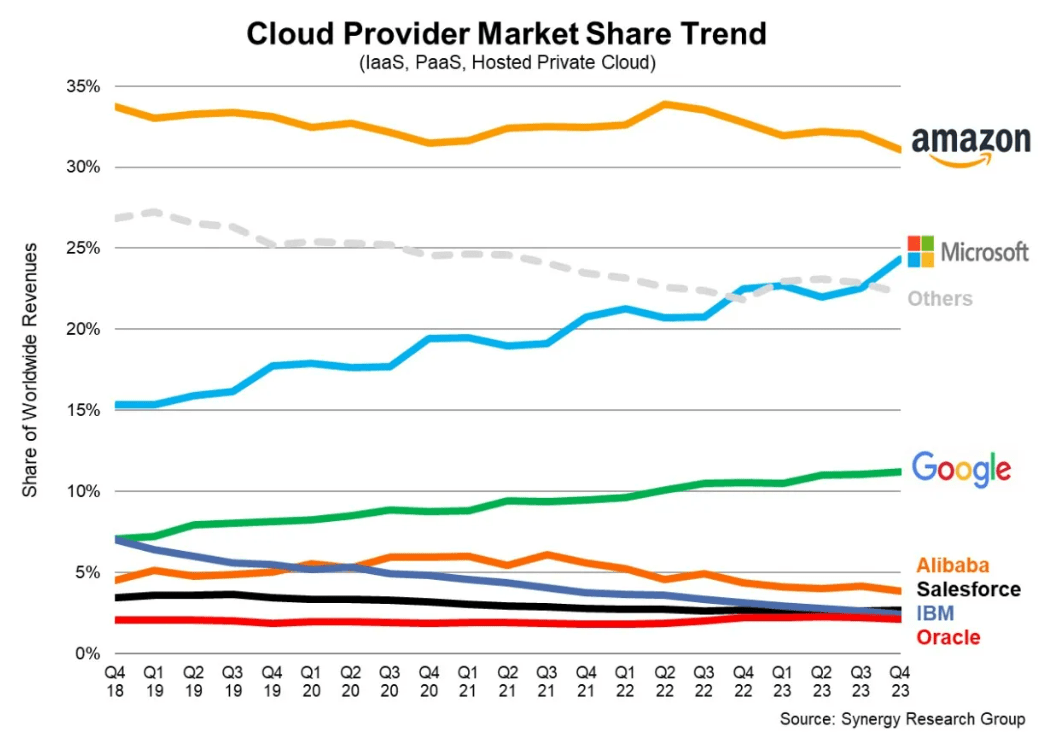

In the mean time, sure, 57% of the income from Alphabet is Google Search, however Alphabet’s Google Cloud Platform (GCP) continues to develop at a ridiculous tempo. Up to now 5 years, GCP has grown 150%, outgrowing the worldwide cloud market by 50% in that point.

Worldwide Cloud Progress (Statista)

Alphabet continues to steal market share from the smaller cloud suppliers and now has an 11% market share, up from 8% in 2019. Now some could also be saying that the cloud has run its course, it has been the money engine for Amazon (AMZN) and Microsoft (MSFT) for a decade now, and it’s achieved. Quite the opposite, the Cloud isn’t an merchandise to disregard – a number of sources be aware that the cloud will proceed to develop at a 15-20% CAGR into the 2030s. All of meaning, everything of cloud will develop from simply round $600bn in 2023 and can almost double within the coming 5 years.

Cloud Supplier Market Share (TechCrunch / Synergy Analysis)

If Alphabet continues to build up market share and double its cloud enterprise within the coming 4-5 years (15-20% CAGR), that might enhance income from $33bn in 2023 to just about $70bn in 2027/2028. Assuming GCP grows its margin from 5% in 2023 to nearer to 30% observed by AWS or 45% observed by Microsoft, then there’s a likelihood phase web earnings grows from lower than $2bn in 2023 to between $20bn and $30bn in 2028.

Sure, meaning Alphabet’s cloud enterprise may very well be price between $400bn-$750bn within the subsequent 5 years.

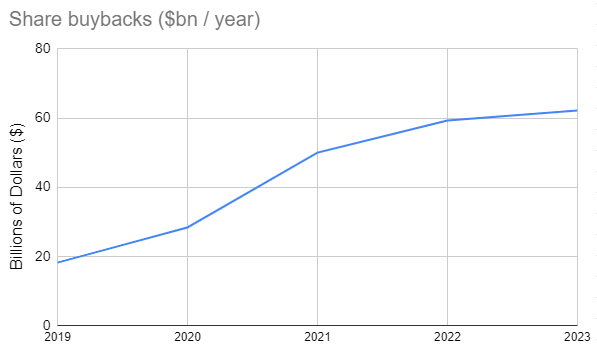

Share repurchases: Secondly, there’s prone to be EPS development over the approaching years because the board continues to authorize legendary share buybacks. Over the previous 5 years, Alphabet’s board has approved the acquisition of $218bn of shares equal to 2.2B shares, or virtually 15% of the float in that point. That 15% discount has been partly offset by share-based compensation to staff and administrators, leaving a complete float discount of simply over 9%.

The board typically proclaims upcoming share repurchase plans within the 1Q earnings launch (April). Final 12 months the board approved $70bn in share repurchases, to which the corporate bought 528m shares in 2023.

Alphabet Share Repurchases Over Time (Alphabet Earnings)

I anticipate subsequent 12 months to be no totally different, with money circulate from operations in 2023 of over $100bn and capex remaining lower than 30% of the ops money, buyback authorization in 2024 ought to run within the $70bn-$75bn vary shopping for again roughly 4% of the float.

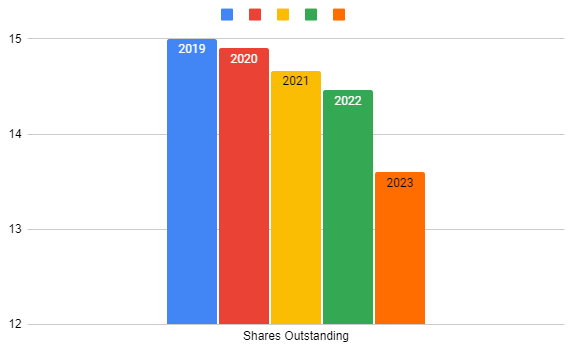

Over a 5-year interval, I anticipate that Alphabet will purchase again near 15-20% of the shares excellent. After share-based compensation, it will successfully cut back the float by 10-15%. This alone will increase EPS by 11-17.5% on prime of already stellar natural development.

Alphabet Shares Excellent Over Time (Alphabet Earnings)

There may be additionally one thing to be stated about YouTube Premium and its capacity to get into NFL Sunday Ticket, YouTube Music, and different options like downloading content material and watching movies offline. The service has grown to over 100M subscribers and rising… however I’ve not achieved the due diligence wanted to dive totally into it, so I’ll save this for a future article.

The Relaxation Of The Magazine 7

In relation to how Alphabet stacks up on a price-to-earnings a number of foundation in comparison with the remainder of the Magnificent 7, Alphabet and Apple (AAPL) are the one ones that appear fairly priced. That stated, I need to be aware that Nvidia (NVDA) is the one one of many Mag7 that has but to report earnings this season and thus may cut back its P/E a number of within the coming weeks.

I’m a agency believer that premium large-cap firms with moats deserve a 20-25x a number of on subsequent 12 months’s earnings as they’ll expertise money inflows related to mass ETF shopping for and can typically be thought of protected havens for capital.

Market Cap and FY 2023 Incomes of Magnificent 7 (Earnings from Respective Firms)

I might personally take into account P/Es north of 30x of subsequent 12 months’s earnings to be costly – nonetheless if the web earnings development of the corporate persists at 20% for the upcoming two years, 30x may be deemed low-cost. So with the persistent development Microsoft has seen and is predicting within the coming years, a P/E of 37x on a trailing twelve-month (TTM) foundation is nothing wild.

However then be aware Alphabet at 25x primarily based on 2023 earnings. I believe Alphabet’s EPS shall be $7.50 in 2025, which is up 30% from 2023.

$7.50 EPS would imply the inventory is presently valued at simply 19x 2025 earnings. In actuality, Alphabet may afford a 2023 P/E of 30-33x as EPS will develop from $5.80 in FY2023 to $7.50 in 2025 – warranting a worth carry of 30% between $185 and $190 per share.

Nevertheless, the popularity of dangers to Google search from AI chatbots and different LLMs shall be ever-present going ahead, presenting a drag on the longer term valuation of the inventory. Thus the inventory rising into $185-$190/share inside the subsequent two years is adequate for me as an investor.

Are There Different Alphabet Bulls On The Avenue or Looking for Alpha?

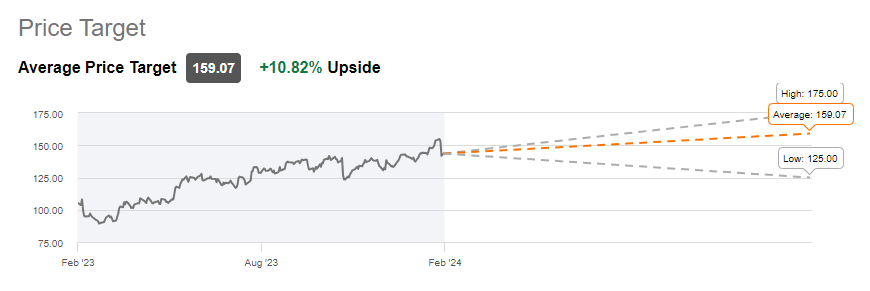

Avenue and Looking for Alpha analysts for Alphabet advocate the inventory as a strong purchase at present costs. My $185-190 worth goal over the following two years is on the excessive finish contemplating the $125 to $175 Avenue worth vary for the approaching 12 months. The common Avenue worth of $159 represents an 11% upside to at this time’s worth.

The $185-190 worth goal is a 30% upside to the inventory worth over the following two years or 14% per 12 months. Whereas the bullish Avenue analysts predict a rise of 11-22% within the coming 12 months.

Peer analysts on Looking for Alpha presently fee Alphabet a 3.9 out of 5, which alerts a purchase on the inventory. 4 SA analysts fee the inventory a powerful purchase, 9 ranking the inventory a purchase, and three ranking it a maintain. There’s a single vendor.

Wall Avenue analysts presently fee Alphabet a 4.3 out of 5, with 31 SA analysts fee the inventory a powerful purchase, 13 take into account it a purchase, 12 take into account it a maintain and there are not any sellers.

Quant presently charges Alphabet a 4.9 out of 5, a Sturdy Purchase.

One 12 months Value Goal (Looking for Alpha)

Main Dangers That Might Upend the Inventory

I see breaking apart of the corporate to keep away from monopoly legal guidelines and lack of Google Search income to be the biggest dangers to Alphabet’s future.

Alphabet break-up: The group continues to face regulatory hurdles and authorities anti-trust lawsuits throughout the globe main the corporate down a path of splitting up simply to take care of regular enterprise operations. A number of instances all through the previous decade, Google has been fined by the European Union for antitrust and misplaced. The EU claims Google is utilizing its dominance in search to throttle or deprioritize particular outcomes or embellish options that push down rival outcomes. The U.S. Justice Department can be working with the Legal professional Generals of California, Colorado, Connecticut and a number of other different states claiming that Alphabet, extra particularly, Google has monopolized digital promoting and is in violation of Part 1 and a pair of of the Sherman Act.

I’m beneath the agency perception that Google’s search dominance has been by means of its high quality product, beating out rivals through the years like Ask Jeeves, Yahoo, Bing, and plenty of different search engines like google and yahoo to reach on the prime. All of that stated, the intricacies of what’s really occurring with the search algorithms and throttling of particular outcomes are past my space of experience. All I do know is firms have been taken down by the federal government for much less and I might not be stunned in the event that they discover a option to break down Alphabet’s search enterprise.

Generative AI merchandise like ChatGPT, Bard, Bing, and DuckAssist all are altering how search is being achieved on the web. The concern that conventional merchandise like Google Search and website positioning fall by the wayside whereas generative AI improves search to supply a single hyperlink or choose few hyperlinks or paragraphs, leading to decrease advert income over time, may very well be a actuality. I see this being a short-term drawback, and similar to YouTube, the issue shall be solved with time and ingenuity.

Initially Meta’s (META) Instagram didn’t have advertisements. YouTube didn’t have advertisements. Fb didn’t have advertisements. Nevertheless, right here we’re in 2023, with these being the biggest advertisers on the planet. If there’s site visitors to a product like ChatGPT, Bard, or different, there shall be a most well-liked search circulate or ads – each will drive income.

Asking Bard’s AI chat immediate about black wafer cookies may instantly return outcomes particular to upsell Oreos or Kroger retailer model. After offering a response, Bard may merely ask in return if you need it so as to add Oreos to your purchasing record.

Or in case you ask about Denims it instantly begins referring to Levi’s.

There are methods across the conventional income stream that’s Google Search. It has simply not been constructed but.

Conclusion

The above demonstrates that Alphabet has defied the destructive sentiment of the market and customers over the previous twenty years by delivering robust efficiency and revolutionizing how the world operates. Regardless of the Avenue and plenty of retail investor’s issues in regards to the longevity of Google’s search enterprise, the corporate continued to develop handsomely whereas selecting up different income streams lately, like YouTube Premium. The Google Cloud Platform provides one other vertical to Alphabet’s arsenal. With GCP’s future development, it’s prone to be price between $400bn to $750bn within the subsequent 5 years.

All of this dominance in search, cloud, and leisure is a part of Alphabet’s strategic company strategy that contributes positively to the underside line. The share worth is then additional uplifted by plentiful share repurchases that proceed to get accepted by the board.

All of it will carry EPS from its $5.80 in 2023 to just about $7.50 in 2025. Mixed with a 25x P/E a number of, this helps a worth of $185-$190 within the subsequent two years – representing a 30% upside on at this time’s inventory worth. The latest worth motion put up This fall earnings ought to entice anyone who has been seeking to enter Alphabet and maintain it for the following 5-10 years. The inventory may dip into the $130 vary, however I might not get grasping. My bullish thesis on Alphabet is echoed by the Avenue and Looking for Alpha analysts, each sharing a “Buy” ranking.

All of the positives must be partly outweighed by the dangers of difficult regulatory environments throughout the globe presenting anti-trust lawsuits and the impression that generative AI could have on conventional search revenues. I’m assured Alphabet will navigate these waters properly however there could also be a drag on the valuation within the interim and the dangers, even when mitigated could all the time come to fruition.

I’m certain I missed loads on the constructive and destructive facet! Please share with me what makes you bullish or bearish on Alphabet under within the feedback.