MicroStockHub/iStock via Getty Images

Market Environment

U.S. equities showed strength throughout the first quarter of 2024, aided by excitement surrounding artificial intelligence, encouraging economic data and investor expectations for rate cuts from the U.S. Federal Reserve this calendar year. As a result, U.S. market indexes reached new highs. In March, the Federal Reserve Open Market Committee held a meeting and chose to leave interest rates unchanged while it continues to monitor evolving economic data.

Portfolio Performance

The portfolio’s return was 10.31% (‘net’) for the reporting period. This compares to the Russell 1000® Value Index that returned 8.99% for the same period.

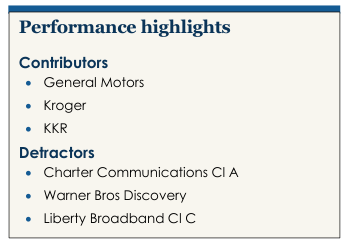

Top contributors:

- General Motors (GM) was a contributor during the quarter. The U.S.-headquartered consumer discretionary company’s stock price rose following fourth quarter results that were in line with consensus expectations along with 2024 guidance that was ahead of consensus expectations. Despite persistent fears over an imminent market downturn, demand and pricing have remained resilient. Notably, General Motors noted its planned investor day will be pushed back from March to an unnamed date later in the year as CEO Mary Barra wants to focus on showcasing accomplishments to investors as opposed to presenting plans in an effort to restore management’s credibility. Overall, we are pleased with General Motors’ results as we believe the company continues to be more resilient than expected. Further, we appreciate the significant cash flow that is being returned to shareholders. General Motors remains an attractive hold.

- Kroger (KR) was a contributor during the quarter. The U.S.-headquartered consumer staples company’s stock price rose following the release of fourth-quarter results that were modestly ahead of consensus expectations and favorable guidance for 2024. While the metrics do not appear particularly strong, the environment is still normalizing after exceptionally strong performance during Covid-19. Notably, Kroger reiterated its intention to fight the FTC’s lawsuit to block the Albertsons deal. We continue to believe in the long-term prospects of Kroger.

- KKR was a contributor during the quarter. The U.S.-headquartered financials firm’s stock price rose following the release of fourth-quarter results. Notably, private markets fundraising, carried interest revenue and capital markets fee generation saw their best results since mid-2022. We modestly increased our estimate of intrinsic value following the company’s fourth-quarter results and management’s commentary regarding the outlook and we look forward to investor day in April.

Top detractors:

- Charter Communications (CHTR) was a top detractor during the quarter. In February, the U.S.-headquartered communication services company’s stock price fell when the company reported that broadband subscribers declined 0.2% sequentially. We anticipate that broadband subscriber growth will remain challenging in the near term due to a heightened competitive environment and the likely wind-down of a government subsidy program. However, we expect these competitive forces will abate over the medium term and that Charter’s broadband subscriber base will return to normal growth. In the meantime, the company continues to grow earnings, invest in high-return capital projects and repurchase stock. We maintain our belief in the long-term prospects of Charter Communications.

- Warner Bros. Discovery (WBD) was a detractor during the quarter. The U.S.-headquartered communication services company’s stock price fell following the release of mixed fourth-quarter results with earnings metrics falling below consensus expectations, mainly driven by the studio segment. On the positive side, free cash flow came in above our expectations, which allowed for continued debt paydown, which we were glad to see. We continue to believe in the long-term prospects of Warner Bros. Discovery.

- Liberty Broadband (LBRDK) was a detractor during the quarter. The U.S.-headquartered communication services company’s stock price fell alongside the release of Charter Communications’ fourth-quarter results due to its investment in Charter. Overall, we believe full-year 2023 results for GCI Liberty were decent. Notably, GCI does not expect an impact from ACP rolling off. Instead, the company sees this as an opportunity to acquire mobile subscribers. Lastly, Broadband subscribers grew during 2023. We continue to believe in the long-term prospects of Liberty Broadband.

PORTFOLIO POSITIONING

We initiated the following position(s) during the period:

-

- Delta Air Lines (DAL) is a global airline company based in the U.S. In our view, the largest U.S. airlines emerged from the Covid-19 pandemic with arguably the strongest competitive position they have ever occupied and now command the vast majority of industry profits. We believe this is a result of a growing consumer preference toward premium travel experiences and the largest airlines responding by improving product segmentation. This compares to many low-cost carrier competitors that are in a weakened position as they have been disproportionately impacted by high cost inflation following Covid-19. We see Delta Air Lines as the leading and best positioned premium airline brand within the U.S. thanks to its long track record of industry-leading operational performance and investments in the customer experience. We also think the company’s geographically optimal hubs, high local market share, robust loyalty program and unique corporate culture all support healthy returns on capital. We believe Delta’s current valuation is compelling for a competitively advantaged and growing business.

- Deere & Company (DE) is a leading manufacturer of agricultural equipment with dominant market share positions in North America and Brazil. Despite its brand strength, technological capabilities and distribution advantages, the company’s stock price has recently come under pressure due to investor fears of a trough in the current agriculture business cycle. Longer term, world population and food demand are expected to increase annually with land and labor devoted to agriculture set to decline each year. As a technological leader, we believe Deere is well-positioned to benefit from this dynamic as farms will need to become more productive. We also like that the company’s management team has a strong track record of growing the business organically through cycles, continuously improving returns on invested capital and returning capital to shareholders. We were able to purchase shares in the company at a discount to our estimate of intrinsic value and to other high-quality industrials.

- Kenvue (KVUE) became the largest standalone consumer health company following its split-off from Johnson & Johnson in May of 2023. The company’s highly recognizable brands, such as Neutrogena, Listerine, Tylenol, and BandAid, have been market share leaders in their respective categories for generations. However, Kenvue’s first year as a public company was clouded by litigation and market share losses in certain categories. Kenvue trades at a substantial discount to the market and other consumer health and packaged goods companies. Furthermore, we see an opportunity for Kenvue to operate more efficiently as a standalone entity and re-invest cost savings into increased product development and marketing, which should help improve growth and ensure its brands remain at the forefront of their categories. We believe the market is reflecting an overly pessimistic view and were recently able to purchase shares at an attractive price for a leading consumer company.

We eliminated Amazon (AMZN), HCA Healthcare (HCA), Hilton Worldwide (HLT), Meta Platforms (META) and PHINIA (PHIN) from the portfolio.

OUTLOOK

While we keep a watchful eye on the macroeconomic environment, we remain focused on our bottom-up, fundamental analysis at the company level when constructing portfolios. We invest in businesses priced at substantial discounts to our estimate of intrinsic value, that we believe will grow per share value over time, and have management teams that think and act like owners. Our analysts are generalists who remain industry agnostic and focused on finding value, regardless of what is in favor at any given moment. We believe this positions our portfolios for sustainable, long-term success.

|

The specific securities identified and described in this report do not represent all the securities purchased, sold, or recommended to advisory clients. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time one receives this report or that securities sold have not been repurchased. It should not be assumed that any of the securities, transactions, or holdings discussed herein were or will prove to be profitable. The information, data, analyses, and opinions presented herein (including current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) are for informational purposes only and represent the investments and views of the portfolio managers and Harris Associates L.P. as of the date written and are subject to change without notice. This content is not a recommendation of or an offer to buy or sell a security and is not warranted to be correct, complete or accurate. Data is in terms of U.S. dollars unless otherwise indicated. Certain comments herein are based on current expectations and are considered “forward-looking statements”. These forward-looking statements reflect assumptions and analyses made by the portfolio managers and Harris Associates L.P. based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Actual future results are subject to a number of investment and other risks and may prove to be different from expectations. Readers are cautioned not to place undue reliance on the forward-looking statements. The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000® companies with lower price-to-book ratios and lower expected growth values. This index is unmanaged and investors cannot invest directly in this index. ©2024 Harris Associates L.P. All rights reserved. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.