Laser1987

Speculating on the outcome of mergers and acquisitions activities can be incredibly profitable. Much of the upside that comes with this comes from investing in a company before a deal is announced. This also is the stage of speculation that often carries the greatest uncertainty because there is no guarantee that a deal will be agreed upon. After a deal is announced, the difference between where shares of the company being acquired are trading at and the buyout price converge significantly. In many cases, this leaves little to no upside, besides a small gap that is essentially the time value of money and the probability that the deal will fall through.

Every so often, however, the market believes that the deal in question will collapse. And when that does occur, the gap between the price at which shares are trading and the price at which management agreed to sell the business can be vast. A great example of this can be seen by looking at Alaska Air Group (ALK) and Hawaiian Holdings (NASDAQ:HA). Back in early December of last year, I wrote an article discussing how the two companies agreed to a combination whereby Alaska Air Group will acquire Hawaiian Holdings in an all-cash deal valued at $18 per share.

If the market believed that this transaction was highly probable to occur, then realistically speaking, shares of Hawaiian Holdings would be trading at $17 or higher. However, as of this writing, they stand at only $12.64. This is a spread amounting to 42.4%, which is a massive amount of upside should the deal ultimately go through. We have had some positive developments on this front. But sadly, there does seem to be a lot more working against the transaction going through. For those investors who think that these concerns are overblown, now might be a fantastic time to buy into Hawaiian Holdings. But it’s important to know just how much risk is involved in this process.

A big spread

In the last article that I wrote detailing the acquisition of Hawaiian Holdings by Alaska Air Group, I talked about how shares of the former had surged in response to the news breaking. They ended up skyrocketing 192.6% because of the hefty premium offered up by Alaska Air Group. At the time, I called the transaction risky. This was because of the overall health of Hawaiian Holdings. But I also acknowledged that, should things go well, there could be some rather meaningful synergies created by this merger.

Alaska Airlines

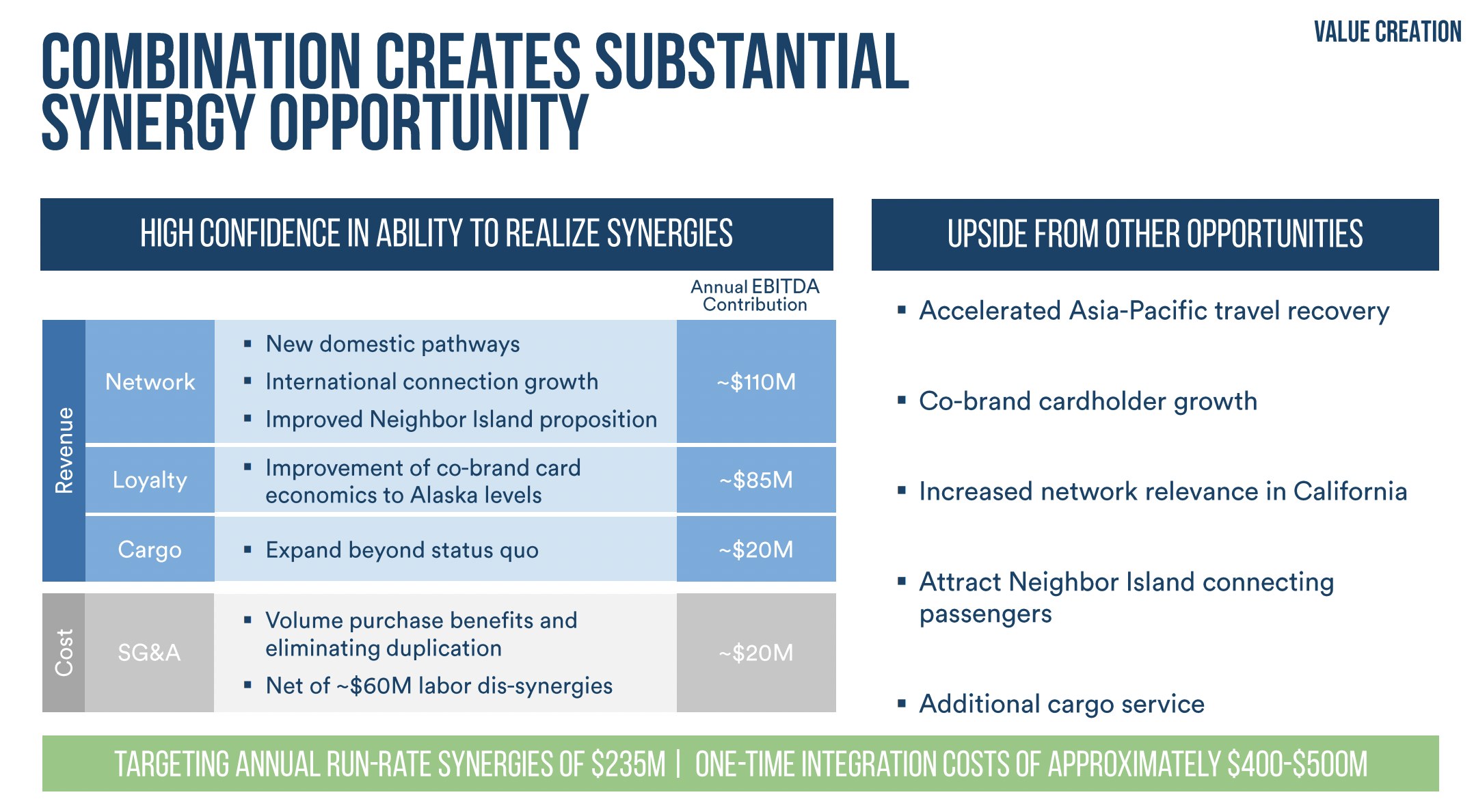

If everything goes according to plan, Alaska Air Group believes that there could be an increase in annual EBITDA to the combined business of about $235 million. Only about $20 million of this would come from cost cutting initiatives. The rest would come from increased revenue opportunities such as new domestic pathways that could be opened up, international connection growth, co-branding opportunities on the loyalty side of things, and even on the cargo side.

Bureau of Transportation Statistics

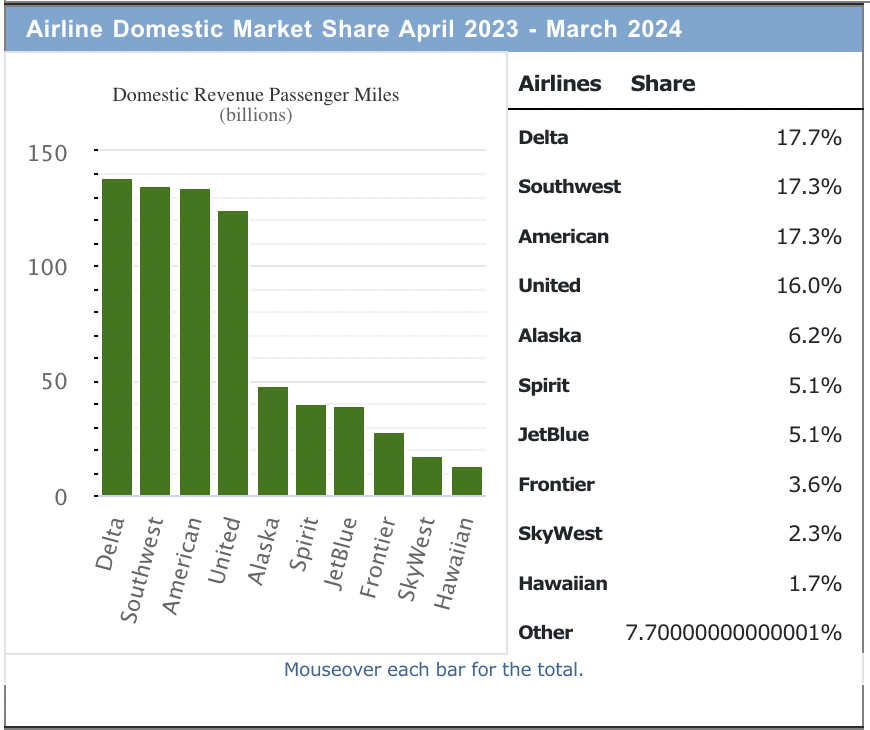

The combination of these two companies would undoubtedly create an industry giant. Already, Alaska Air Group is the fifth largest airline operator in the US, with a 6.2% market share. By comparison, Hawaiian Holdings is the 10th largest player with a 1.7% market share. Combined, the company would have 7.9% of the overall market. While this may not sound like much, they would have significant control over certain key markets. Combined, they would control about 51% of all air traffic to and from Hawaii. And they would also have about a 58% market share over flights heading into and out of Seattle, Washington.

One positive thing that is in favor of those who are bullish about this is that the management team at Hawaiian Holdings announced, on February 16th of this year, that shareholders of the company voted in favor of the merger. This means that the only thing holding the company up is the regulatory side. At that time, Hawaiian Holdings’ management team stated that they expect to complete the deal within 12 to 18 months following the announcement of the transaction on December 3rd of 2023. Clearly, the regulatory side of things will take some time.

Unfortunately, this is where the good news ends. In late March of this year, the two companies entered into a timing agreement with the US Department of Justice. According to this agreement, the companies agreed not to consummate the merger before 90 days following the date on which both firms certified ‘substantial compliance’ with what was then the latest request by the US Department of Justice for more information about the transaction. The purpose of the US Department of Justice at this point in time is to see whether or not this transaction would violate antitrust law by creating unfair competition and ultimately causing damage to consumers.

This is not the first time that there has been push back from regulatory agencies in this space in just the last year alone. In January of this year, a federal judge decided to block the proposed merger between Spirit Airlines (SAVE) and JetBlue Airways (JBLU). This decision was based on antitrust concerns, with the judge ultimately saying that the transaction, if completed, ‘would further consolidate an oligopoly by immediately doubling JetBlue’s stakeholder size in the industry’. Sure enough, that seems right. Both of the companies have a roughly 5.1% stake in air traffic in the US. Combined, that would place them at 10.2%. In response to this, the parties ultimately scuttled the deal. It is worth noting that the two firms did attempt to appease regulators. In September of last year, for instance, JetBlue even agreed to transfer all of Spirit Airlines’ operations at the Boston and Newark airports to another player and that they would also transfer some operations at Fort Lauderdale airport as part of the process. Unfortunately, that was not enough to get the job done.

With a combined market share of 7.9%, there is concern that the deal between Alaska Air Group and Hawaiian Holdings will be blocked as well. These concerns are further bolstered by news that the US Department of Justice is looking at this transaction in a way that is very similar to how it looked at the planned deal between JetBlue Airways and Spirit Airlines. This is not to say that a transaction will not be completed. This is because, in early May of this year, Hawaiian Holdings and Alaska Air Group announced that they have certified ‘substantial compliance’ with the US Department of Justice’s second request for additional information. This means that the 90 day window during which they agreed not to complete the deal will end in early August.

In my opinion, the best opportunities in the mergers and acquisitions space involve companies where, even if the deal does collapse, the firm that risks seeing its share price decline would still be undervalued at the buyout price. In those cases, I believe that the risk to reward ratio favors those who are along the stock. This is because, if the deal does get approved, you should see significant immediate upside. And if this does not come to pass, downside should be limited or even nonexistent.

Author – SEC EDGAR Data

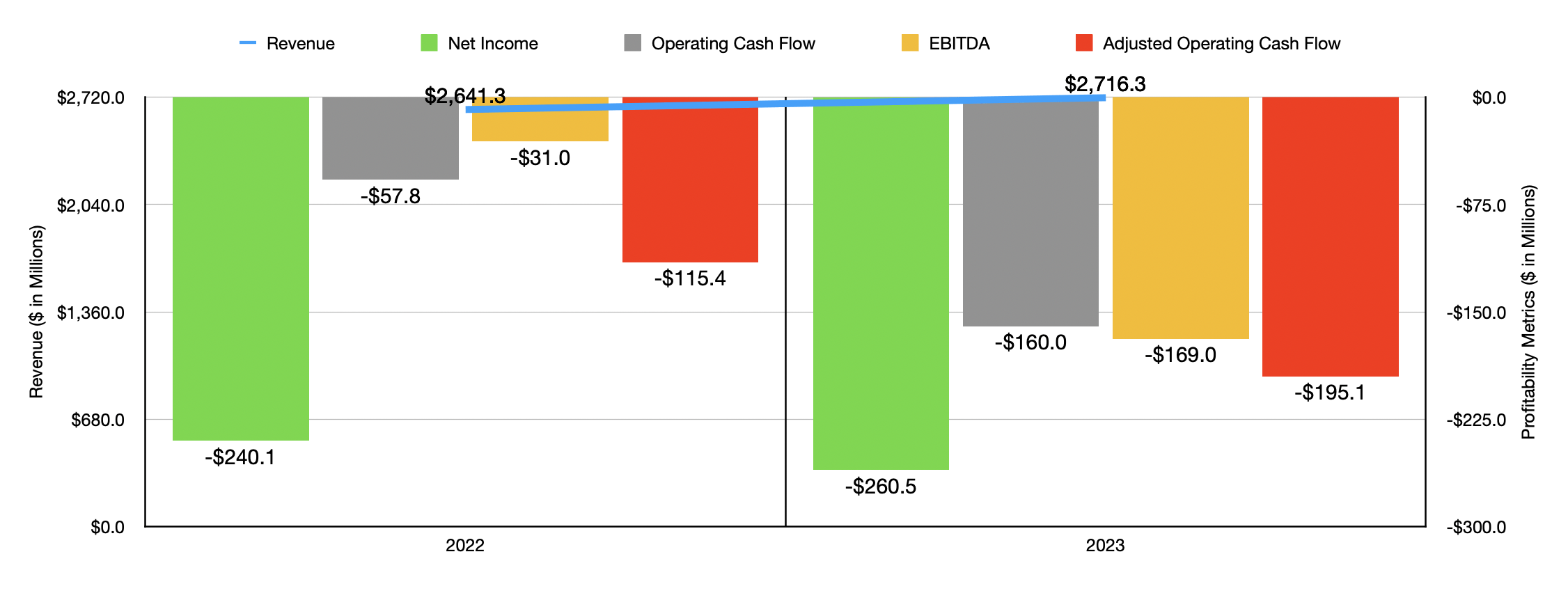

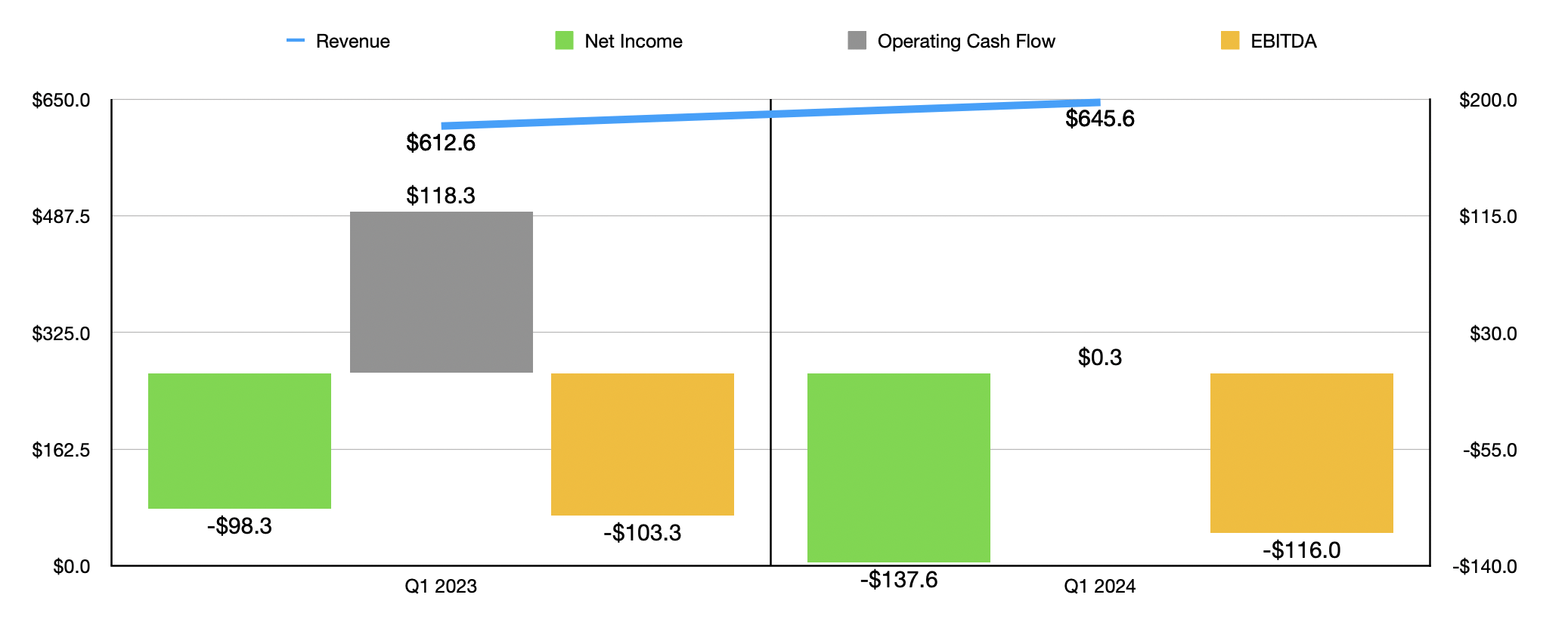

This is the mindset that I have regarding United States Steel (X), which is a company that I have 15.3% of my assets in at this moment. That makes it the second largest holding in my portfolio. I do not feel that way, however, when it comes to Hawaiian Holdings. In the chart above, you can see financial performance for the company covering the 2022 and 2023 fiscal years. Revenue for the firm increased nicely, but profits and cash flows worsened. In the first quarter of this year, as the chart below illustrates, this overall trend continued.

Author – SEC EDGAR Data

*Due to how cash flow is reported, adjusted operating cash flow cannot be calculated on a quarterly basis

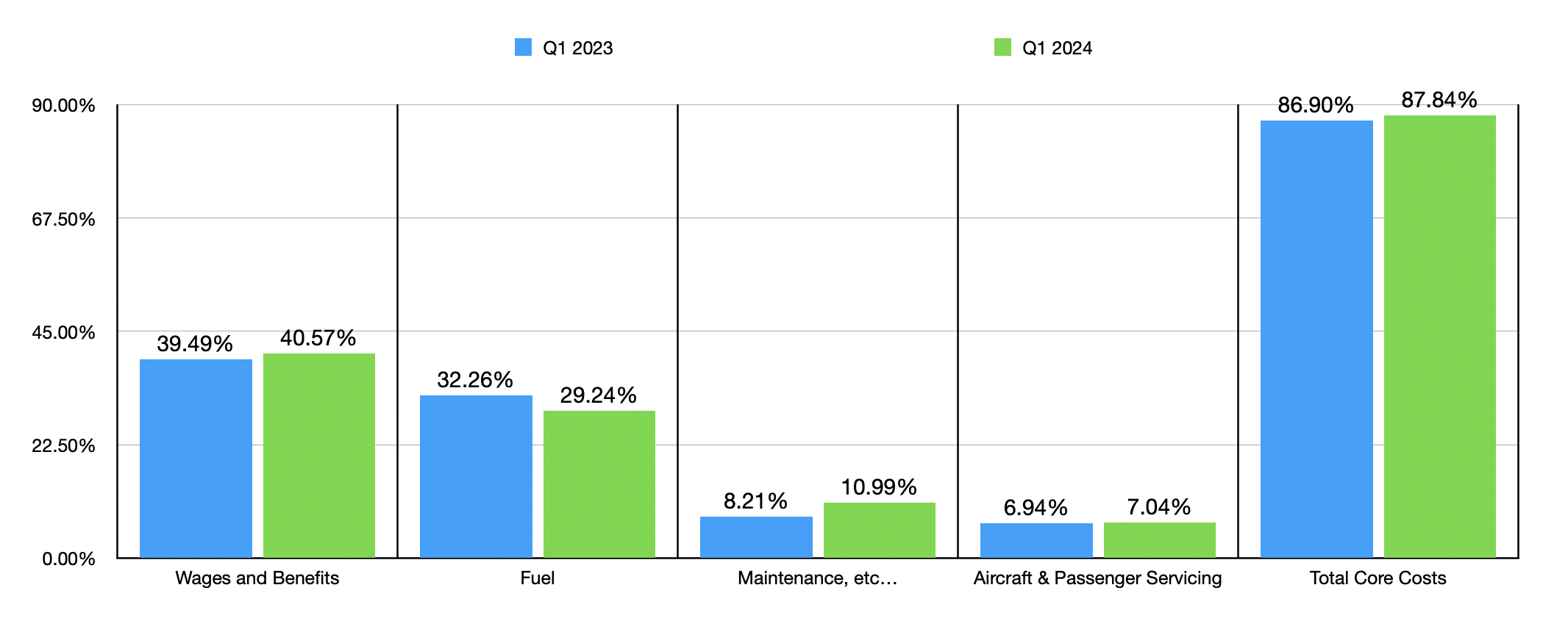

I do think it’s important to be flexible in cases like this. If there are cost items that are likely to be temporary, especially if they are one-time items, investors should give some leeway to matters. In the chart below, I decided to focus only on the most recent quarter for which data is available. This chart works at what I consider to be the core costs of Hawaiian Holdings. This consists of labor, fuel, maintenance costs, and aircraft and passenger servicing activities. These core costs for the business did manage to increase year over year from 86.90% of revenue to 87.89%. That’s a reduction of only $6.1 million on a year over year basis. When you have a company that is continuously losing money, every penny matters. But I would argue that this is not terribly material for the business.

Author – SEC EDGAR Data

Other factors that played an outsized role do seem to be things that are one time in nature. For instance, in the first quarter of this year alone, Hawaiian Holdings incurred $8.5 million in merger related costs. This would obviously disappear after the transaction is completed. There are multiple other factors that I could look at as well. For instance, the company saw a decline in interest income from $16.5 million to $10 million year over year. That was largely due to the fact that, in the first quarter of 2023, the company got a one-time tax refund of $4.7 million. So if anything, the prior years results were overstated if we factor out one-time events. In addition to this, there was an $11.1 million swing in other miscellaneous expenses. However, $10.2 million of that was attributable to a gain on a real estate transaction completed the prior year. So that’s another one-time event.

Hawaiian Holdings

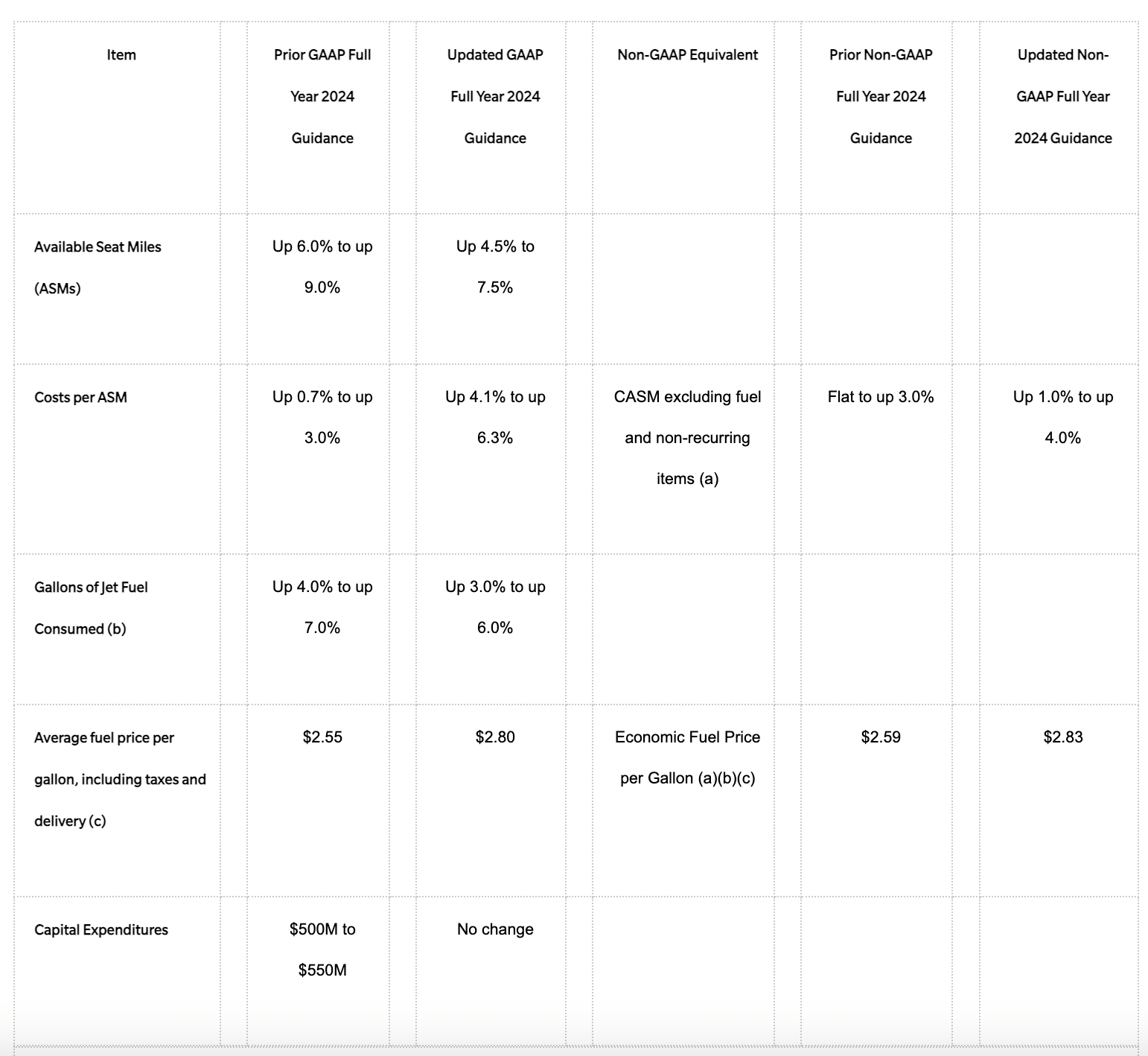

What this shows is that, instead of this year getting materially worse, last year was just exceptionally better. Or at least that was the case for the first quarter of the year. Either way, that doesn’t paint a particularly pleasant picture for the company. There are other concerns as well. When it comes to guidance for this year, management is now forecasting an increase in available seat miles of between 4.5% and 7.5%. Prior guidance called for this to be between 6% and 9%. In addition to this, driven largely by fuel costs, with average fuel prices expected to total $2.80 per gallon compared to what prior guidance estimated would be $2.55 per gallon, the cost per available seat mile is now anticipated to be between 4.1% and 6.3% above what it was last year. By comparison, prior guidance called for this to be up by between 0.7% and 3%.

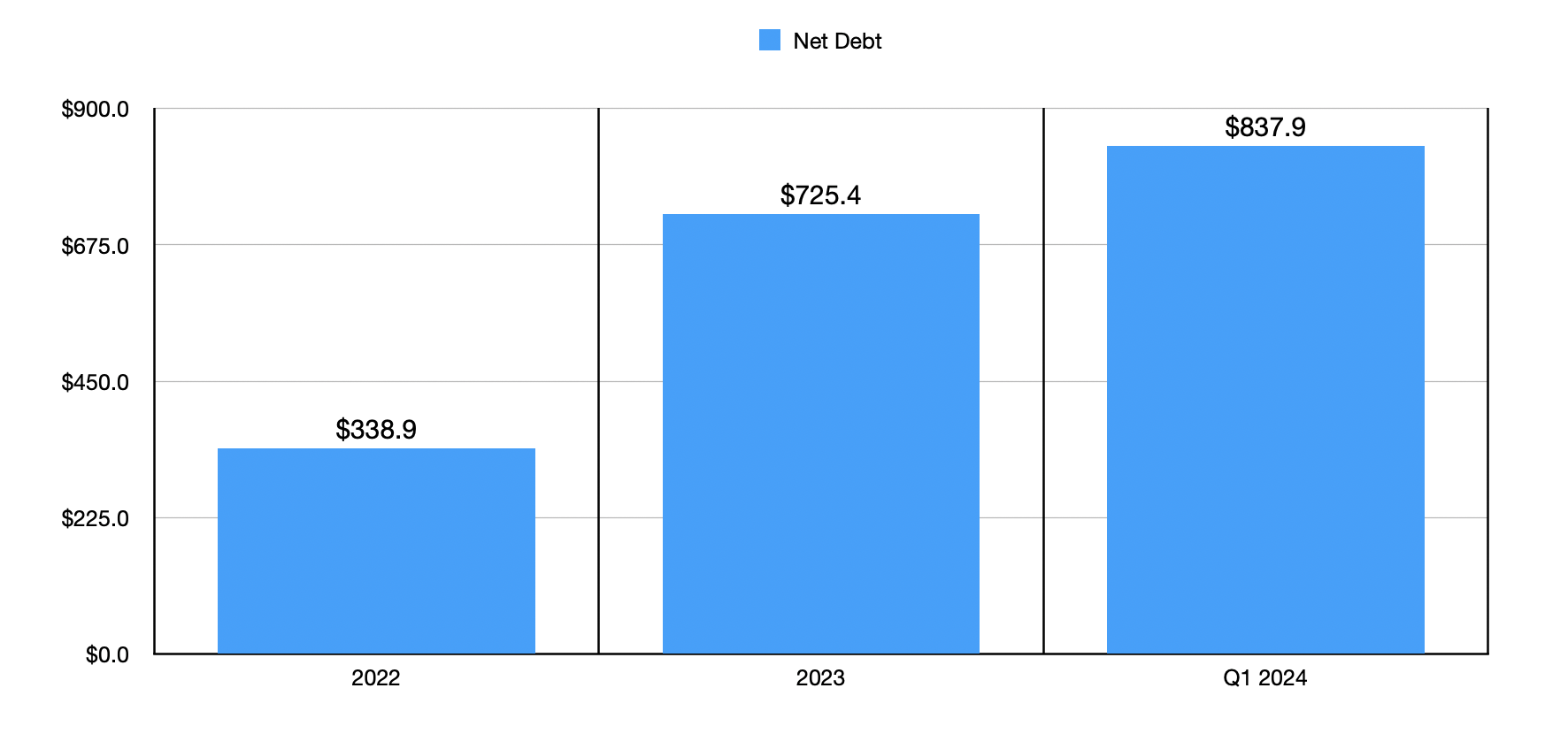

In addition to seeing costs increase and management scale back on growth initiatives, Hawaiian Holdings is also seeing its net debt grow. At the end of 2022, net debt was $338.9 million. That number ballooned to $725.4 million by the end of last year. In the first quarter of this year, it came in even higher at $837.9 million. Obviously, this makes the company higher risk and makes it less appealing to any suitor.

Author – SEC EDGAR Data

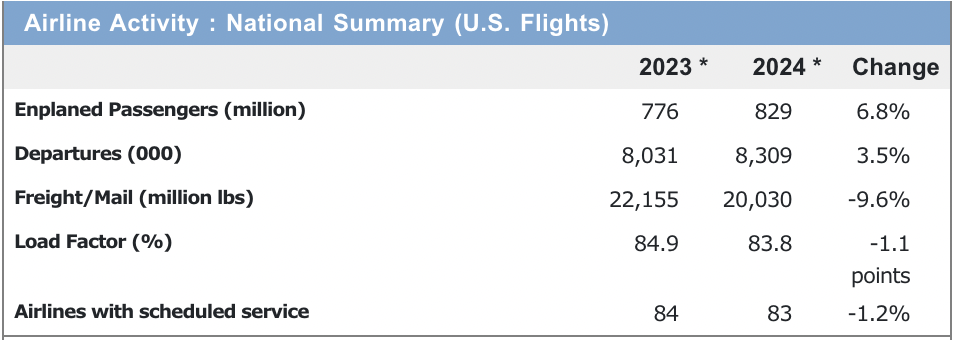

This is not to say that there aren’t some positive things regarding the industry. We only have data for the first two months of this calendar year. But during that time, enplanements in the US were up nicely year over year. In January, the 70.39 million recorded came in 8.6% above the 64.80 million reported in January of 2023. And in February, the 70.03 million was 4% above the 67.36 million reported the same time last year. Another source shows us that the total number of passengers in the trailing twelve months ending in March of this year came in at 829 million. That’s 6.8% higher than the 776 million seen one year earlier. As great as this is, however, there has been weakness from a fare perspective. Airline fares in the month of May were actually down 5.9% year over year. This came at a time when core inflation for the economy was up 3.4%. And in April, airline fares were down 5.8% at a time when core inflation was up 3.6%. To see airline fares dropping at a time when costs are rising and when fuel costs specifically are expected to be higher this year than previously forecasted, is not ideal.

Bureau of Transportation Statistics

Takeaway

The way I see things, the transaction between Hawaiian Holdings and Alaska Air Group will end in one of two ways. If the deal is completed as agreed upon, there could be significant upside for shareholders of Hawaiian Holdings. But on the regulatory front, that could be difficult or even impossible to achieve. The alternative would be that the deal collapses and shares of Hawaiian Holdings plummet. At present, if they were to fall back to where they were before the deal was announced, that would imply downside of 61.6%. In the event that the company looked solid and cheap as a standalone business, I would argue that this potential downside would not be an issue. But I don’t feel that way here. Instead, this looks like an extremely binary scenario and investors should tread cautiously because of it. Because of how worried I am about the regulatory side and the potential downside that investors could face, I personally am going to rate Hawaiian Holdings a ‘sell’.