ucpage

Funding Rundown

Investing in a pool firm could seem fairly niched proper now, and I do are likely to agree with that. Hayward Holdings Inc (NYSE:HAYW) has been fairly risky over the past 12 months however finally displayed a rise of above 48% for the inventory value. Nevertheless, plainly revenues are fairly suspectable to decrease demand within the housing market and the market is kind of damaging on the corporate nonetheless going ahead because the quick curiosity is at 14% proper now. I don’t just like the valuation of the enterprise and assume we’re in for a correction very quickly, leading to a promote right here because the draw back quantities.

Firm Segments

HAYW is an organization dedicated to the design, manufacturing, and world advertising and marketing of a complete vary of pool tools and superior automation methods. Working in North America, Europe, and varied worldwide markets, the firm’s product portfolio encompasses an array of important pool tools corresponding to pumps, filters, robotic cleaners, in addition to fuel heaters, and warmth pumps. These choices cater to the various wants of pool homeowners, offering them with environment friendly and dependable options for pool upkeep and delight.

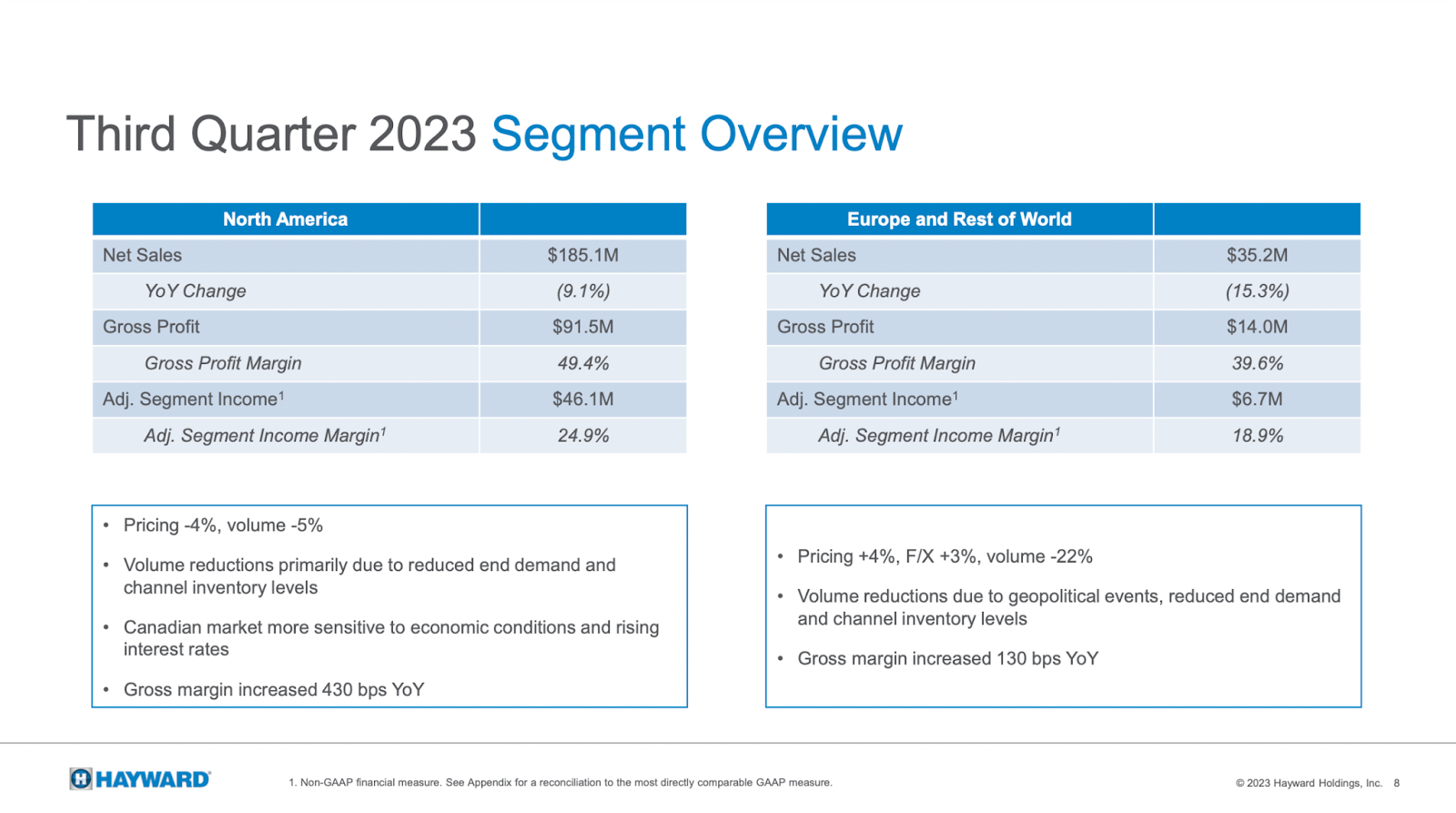

Section Outcomes (Investor Presentation)

The final report from the corporate showcased a decline within the volumes and gross sales for the enterprise. In each North America and in Europe and the remainder of the world the gross sales decline was within the double digits on a YoY foundation. This fairly clearly displays the influence that rising rates of interest are having on client demand, principally for the housing market. With much less available capital for patrons to spend, I feel that we cannot see a fast restoration within the quick time period, sadly.

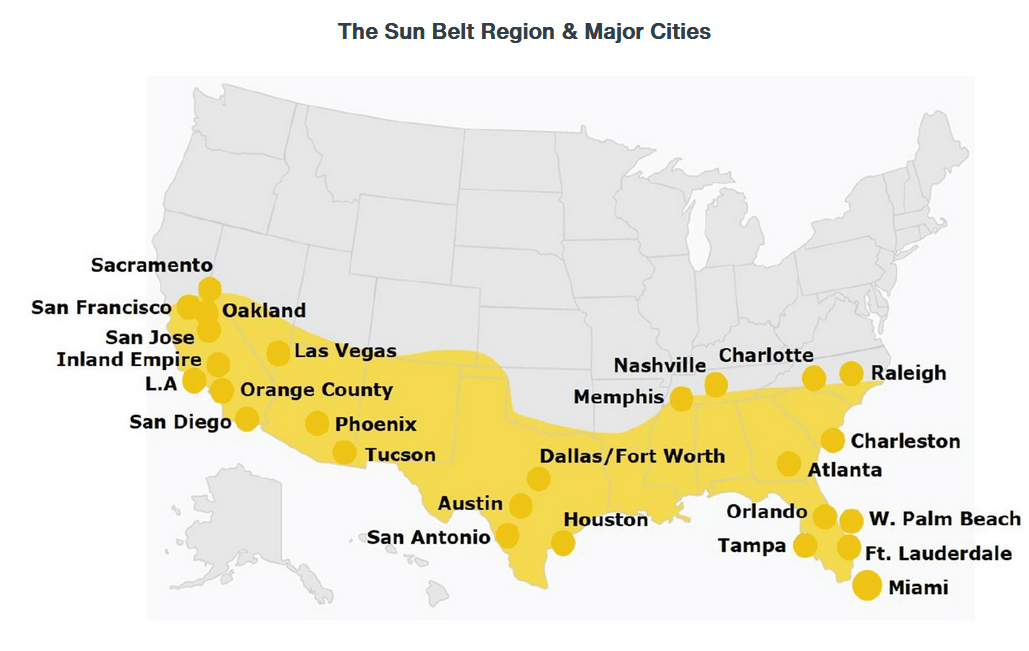

Market Overview (Investor Presentation)

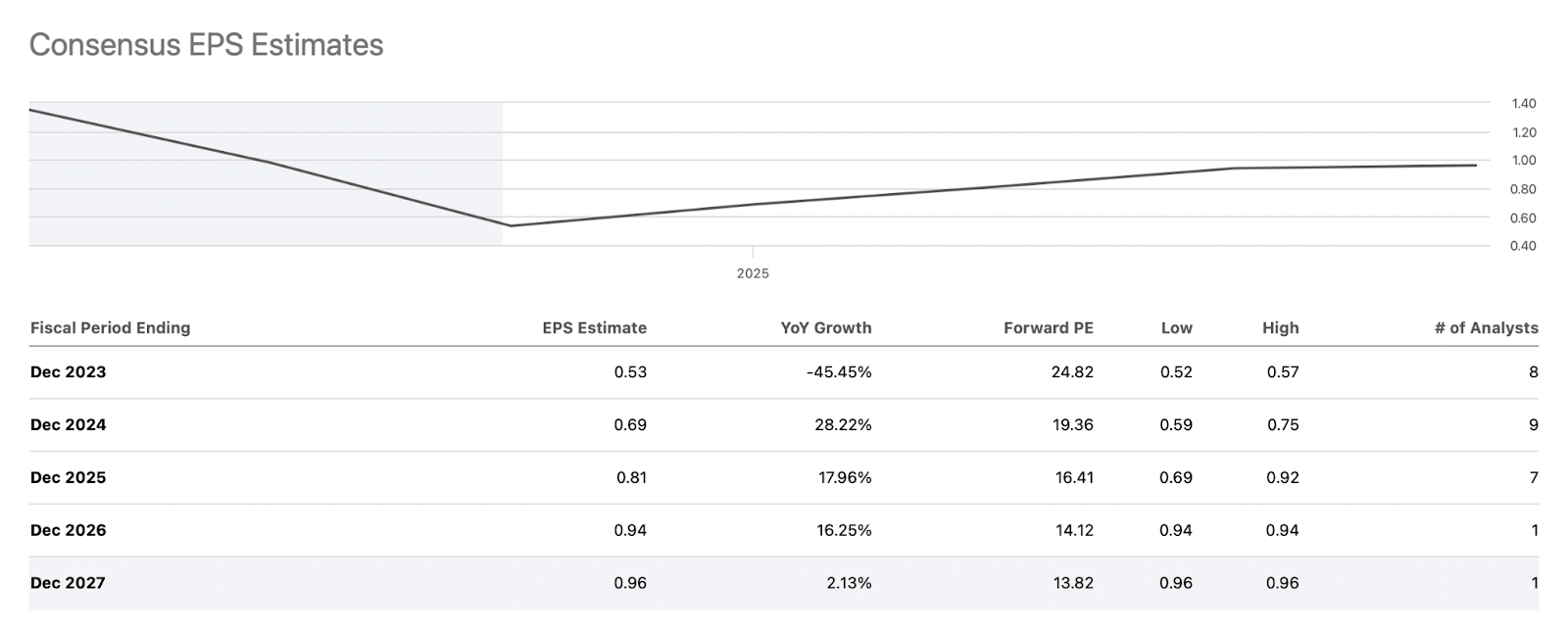

The corporate’s progress prospects are underpinned by a number of key elements, together with the Sunbelt migration pattern, the combination of linked sensible house applied sciences, and the emphasis on environmentally sustainable merchandise. As the worldwide population ages and life evolve, the demand for swimming pools is anticipated to rise considerably. In the US alone, the market contains roughly 5 million in-ground swimming pools, and on a world scale, this quantity expands to a considerable 25 million. This presents a considerable progress avenue as pool homeowners search to modernize and preserve their swimming pools with cutting-edge IoT-enabled applied sciences, creating sturdy alternatives for growth. Estimates for HAYW differ within the coming years, however plainly most are anticipating double-digit EPS progress not less than when the gross sales are nonetheless exhibiting YoY declines I’m fairly involved concerning the legitimacy of the estimates and the chance of them coming true I feel will get decrease every time the Fed will not be chopping charges.

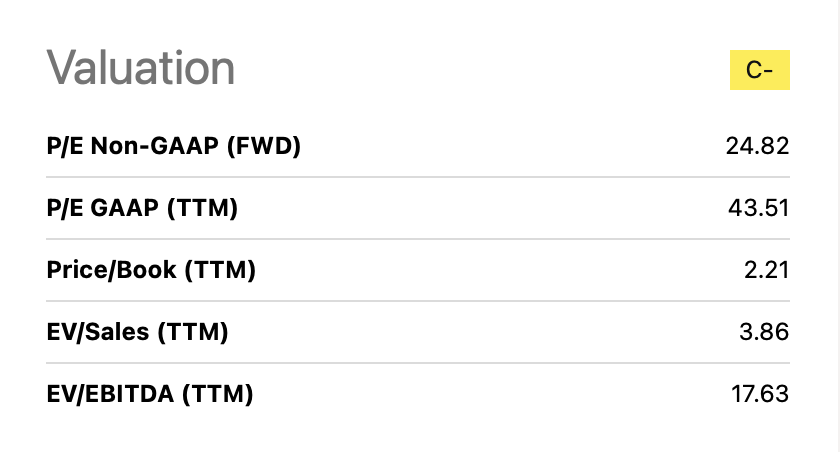

Worth Evaluation

Valuation (Looking for Alpha)

One of many key factors round my promote case with HAYW is that the valuation is correct not sustainable. The corporate is buying and selling at a really wealthy p/s of two.87 on an FWD foundation. Being within the industrial sector and extra particularly the constructing merchandise trade, I’d count on a p/s of round 1 – 1.5 as an alternative for a extra cheap stage. This premium will not be value paying, and with out even a dividend or sturdy buyback program, buyers are left with not quite a lot of worth proper now, sadly. With the final earnings report additionally showcasing a decline within the gross sales for the enterprise I do not assume this kind of premium is justified right here. There have been macroeconomic challenges like heightened rates of interest, and that’s true. However what can be true is that HAYW has failed in being resilient towards that and due to this fact lacks the assist to have a premium this excessive, I feel.

EPS Estimates (Looking for Alpha)

The earnings estimates are fairly optimistic for the corporate it appears the approaching years with the EPS rising at double digits into 2026. I nonetheless do not assume that HAYW is well worth the premium by 2026. Even when the rates of interest fall subsequent yr I feel the difficulties for HAYW might proceed. The corporate has closely diluted shareholders the previous couple of years, and maybe a bit harshly, and solely actually has a excessive debt place to indicate for it I feel. Gross sales have fallen from the file $1.4 billion in 2021 when the housing market was extraordinarily sizzling. The market is betting towards the inventory so I feel it should stay suppressed for so long as shares are being diluted nonetheless. I would not pay over 12x earnings for a housing-related firm like HAYW. Pool tools will not be in excessive demand if homes aren’t being constructed at an accelerated fee, and for the medium time period, I feel that would be the case sadly. The underside line has been proven to lack resilience as effectively and NI fell 49% last quarter. The chance for a big correction I feel warrants the promote right here.

Dangers

In latest quarters, HAYW has encountered a discount in gross sales quantity, primarily pushed by a decline within the demand for pool tools and associated automation methods. This decreased demand prompted its channel companions to cut back their stock ranges. It is value noting that the corporate’s income stream closely depends on a handful of key prospects, introducing a component of danger related to buyer focus.

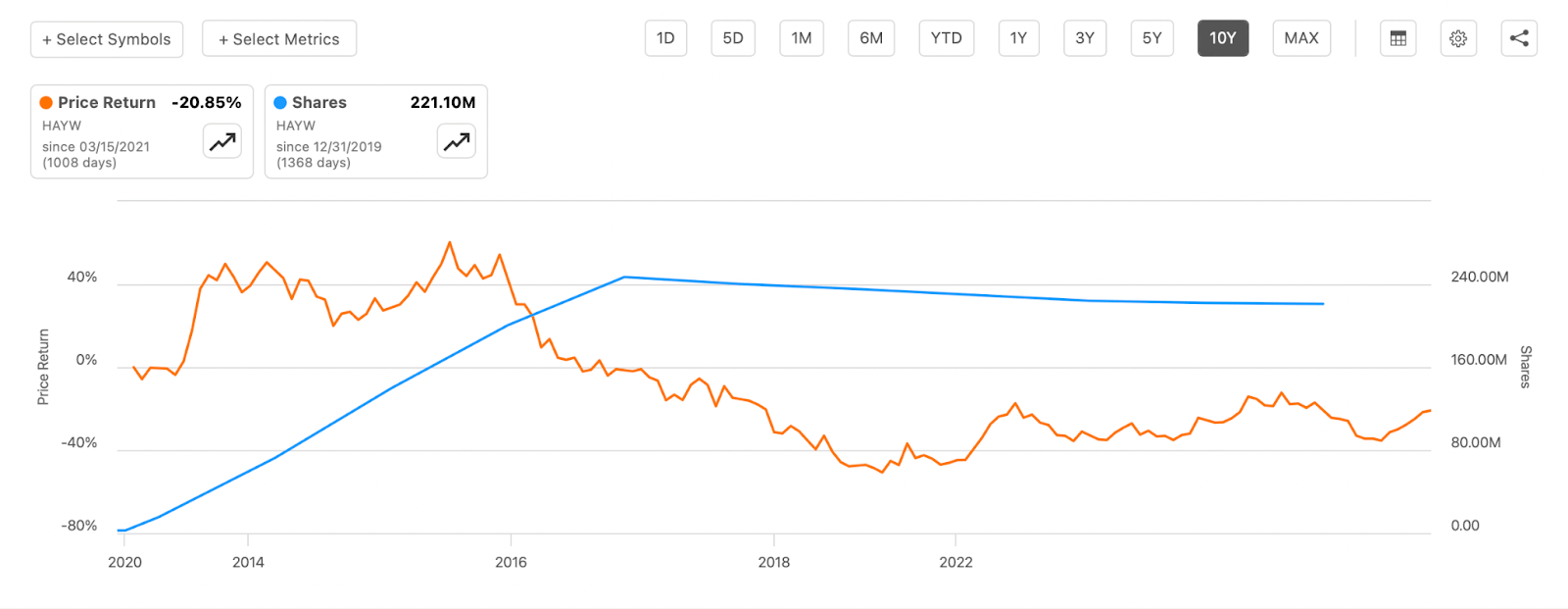

Share Dilution (Looking for Alpha)

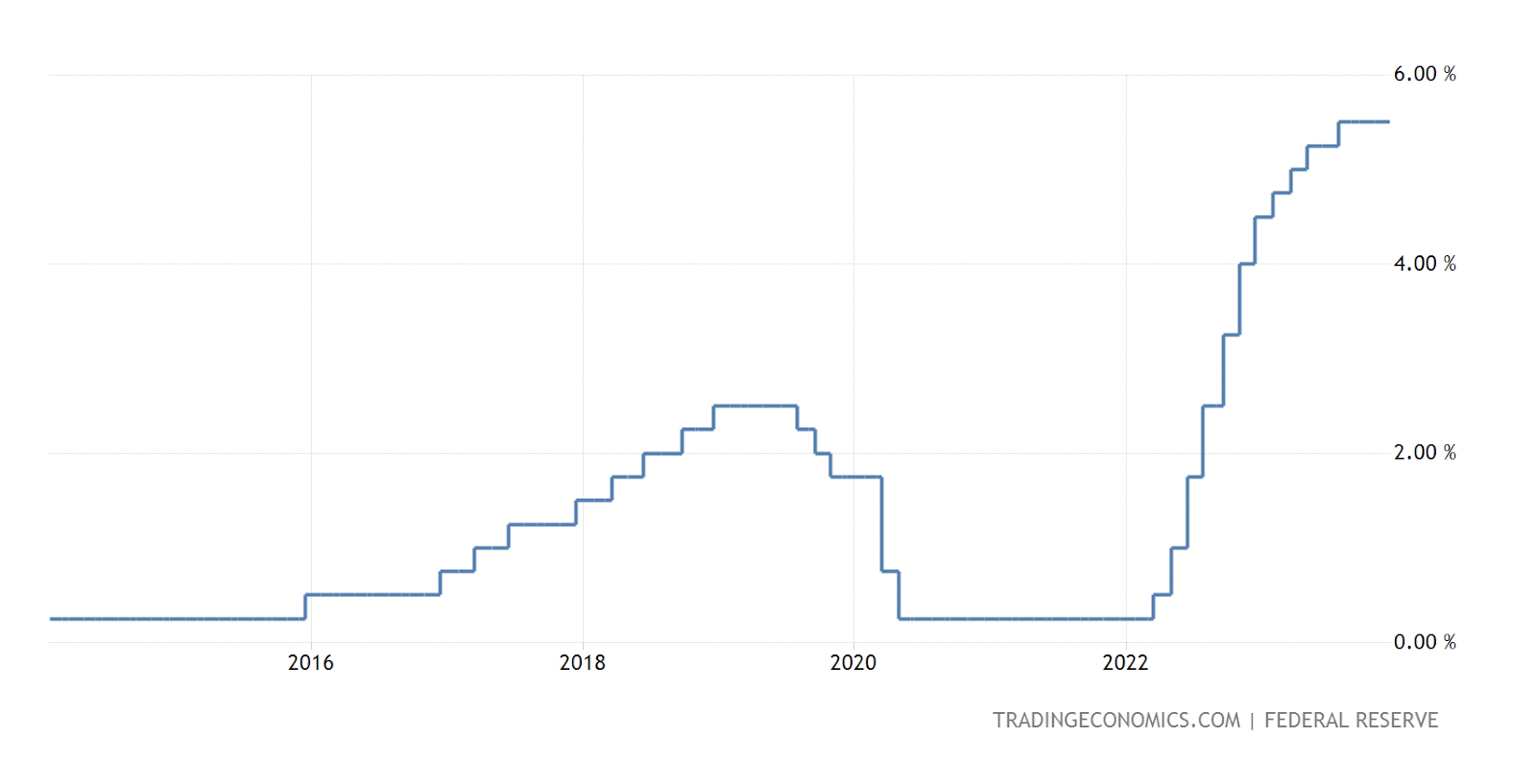

Over the previous yr, inflation and rising rates of interest have emerged as important financial considerations, casting a shadow of uncertainty over the economic system’s stability. Notably, the US rate of interest climbed, surpassing the 5% mark in June 2023. Elevated rates of interest can have hostile results on each client demand and borrowing prices, impacting varied sectors of the economic system.

US Curiosity Charges (Tradingeconomics)

Apart from this, I feel that the rise in brief curiosity for the corporate goes to weigh on the long run efficiency. The market is kind of damaging in the direction of it and betting towards the market can generally result in improbable returns, however generally additionally result in disastrous returns. I feel the chance of a correction is kind of substantial right here too, because the rise in latest months is main it to commerce above sector friends, even while posting decrease gross sales volumes. It could be due to the final quarter’s gross sales popping out forward of estimates, however trying on the greater image, it is nonetheless fairly damaging in my opinion.

Last Phrases

HAYW is an attention-grabbing firm because it roughly has its volumes pushed by the local weather of the housing market. A whole lot of development merchandise beginning results in extra demand for HAYW and in occasions of decrease rates of interest extra folks have capital available for making purchases and investments like a pool and heaters. We’ve got the previous couple of years seen a big double-digit decline in gross sales and I do count on this to proceed for the medium time period earlier than probably selecting up when charges go decrease. This leaves a lot of draw back dangers nonetheless and the dearth of investor optimistic practices is making the present state of affairs for HAYW a promote.