skynesher/E+ through Getty Pictures

Abstract

My last coverage of Hayward Holdings Inc. (NYSE:HAYW) was in January 2023, and I really helpful a maintain ranking as I noticed seen headwinds that would influence its FY23 efficiency. Opposite to my fear, the inventory has executed very well since my preliminary value of ~$9, touching close to $14 in the present day. This submit is to supply an replace on my ideas on the enterprise and inventory. I’m upgrading my ranking from maintain to purchase as I’m anticipating FY24 to be the beginning of the restoration progress cycle. Accelerating progress ought to lead to excessive incremental margins that lead to margin enlargement.

Funding thesis

Within the latest results, HAYW reported 4Q23 income of $279 million, which is barely above the road estimates of $272 million. In North America, income grew 10% to $238 million, pushed primarily by pricing and pulled-forward demand, leading to robust quantity progress. As for Europe and ROW, efficiency didn’t fare as effectively; gross sales declined by 4% to $40.3 million, regardless of a 4% profit from pricing contributions and FX tailwinds. Gross margin did very effectively, coming in at a report of 49.2%, up 140 bps sequentially. The higher-than-expected gross revenue efficiency led to robust adj. EBITDA progress of 42% to $76 million, coming in barely above the road estimate of $74 million.

After ready for your entire FY23, 4Q23 has lastly proven optimistic progress, a really optimistic sign that implies a turnaround is across the nook. Administration additionally gave a really optimistic FY24 information that additional reinforces my bullish view. In FY24, HAYW expects income to develop between 2 and seven%, which suggests a income vary of $1.01 to $1.06 billion. This can be a very encouraging information, as (1) it alerts optimistic progress momentum persevering with into FY24; (2) 4Q23 efficiency has not seen a slowdown coming into FY24 as administration laid out this information in late February (29 Feb), which principally gave administration 2 months of 1Q24 information. Furthermore, this progress goes to see quantity tailwinds from:

- Normalization of stock channels;

- Robust early purchase applications, and energy within the US restore and change market; and

- Potential rebound of bigger initiatives in North America when charges get lower

The final level is one specific level to notice, as I feel it’d trigger an acceleration in quantity demand, provided that administration is already noticing a gradual enchancment within the macro setting in North America.

This outlook displays continued resiliency within the North American nondiscretionary aftermarket, with the extra discretionary parts of the market, new development, transform and improve impacted by the financial and rate of interest setting, notably in non-US markets. 4Q23 earnings results call

The improved progress outlook additionally meant that HAYW ought to see margin enchancment, and FY24 steerage definitely factors to this. They guided for gross margin enlargement to ~50%, pushed primarily by volumes and pricing in North America, which is anticipated to go above 50% sooner or later. This bodes effectively for the adj. EBITDA outlook within the coming years.

General, I feel we’re within the very early innings of the restoration cycle, and the tone across the robust early purchase program and report margins successfully confirmed this. What obtained me extra optimistic about this progress cycle is that HAYW has gone by means of its price discount program, and based mostly on the feedback that administration supplied through the name (consult with under), it seems that administration has pushed by means of some structural enhancements within the enterprise, and we might see stronger incremental margins because the enterprise progress recovers within the coming years. And if the macro state of affairs seems higher than anticipated, EBITDA might doubtlessly outperform steerage.

Yeah, so we have now progressively constructed our G&A workforce, our basic and administrative workforce up during the last three years, and so we’ll proceed to leverage on that. We’ve got made some discrete investments into G&A particularly round our enterprise intelligence capabilities. We have constructed up not too long ago a workforce in that regard. And we search for nice leverage on that funding over the following couple of years. However we actually do have a chance to carry that G&A base now, given the place we exited out of ’23, perhaps simply barely overinflation. So that might be an ideal alternative for margin leverage as we go ahead. After which clearly within the manufacturing price house, we have now a very good quantity of latent capability that we are able to proceed to faucet into, in addition to persevering with to execute on lean manufacturing methods to scale back price. 4Q23 earnings outcomes name

Though some traders are nervous concerning the American shopper provided that we aren’t fully out of the woods but, regardless, I feel a restoration could be very prone to occur this or subsequent yr. Hopefully will probably be this yr if the Fed cuts charges; if not, as charges proceed to carry larger, inflation ought to ultimately come down, particularly because the housing state of affairs within the US will get higher over time.

Valuation

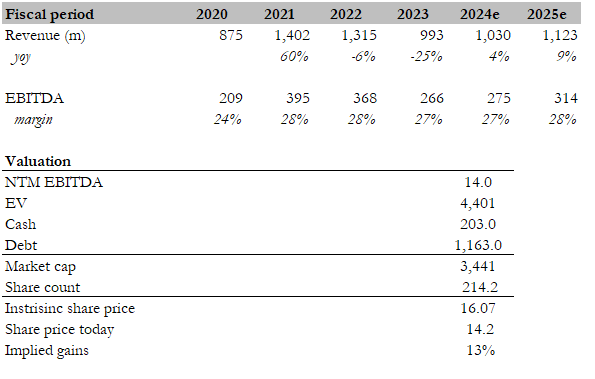

Personal calculation

My goal value for HAYW based mostly on my mannequin is ~$16. My mannequin assumptions are that progress and margin will are available on the midpoint of administration steerage, rising 4% in FY24 and reaching 27% adj. EBITDA margin. Because the macro setting improves by means of FY24/25, I count on progress to speed up to 9%, which is what consensus is anticipating. I take advantage of consensus estimates as a result of they are typically fairly correct. The truth is, over the previous few years, consensus income estimates have a tendency to come back under precise reported figures, which implies our 9% is definitely a conservative estimate. On EBITDA margins, I count on HAYW to the touch the excessive finish of the steerage due to the amount enchancment and potential mounted price leverage that administration has alluded to. This margin enlargement energy ought to be extra obvious in FY25 when progress accelerates to 9%. Evaluating HAYW progress and margin outlook towards friends like Leslie’s and Lowe’s Cos, I count on multiples to proceed staying at this premium. For reference, Leslie is anticipated to develop at a low to mid-single-digit share and has a 15% EBITDA margin. Lowe’s progress is anticipated to be flat, whereas the EBITDA margin is 15% as effectively.

Threat

My expectation is that the macro setting recovers by FY25 (within the worst-case state of affairs). Nevertheless, if we go right into a full recession-something like GFC-the HAYW progress cycle might be pushed out to a number of years later. This may put plenty of stress on demand, and I count on the market will take a really conservative method to the inventory and keep on the sideline.

Conclusion

In conclusion, my ranking for HAYW has been upgraded from a maintain to purchase ranking as I see optimistic indicators of a progress cycle from the robust 4Q23 outcomes with income exceeding expectations and report gross margins, and FY24 steerage which suggests optimistic progress momentum with potential upside from quantity tailwinds. I’m additionally optimistic on HAYW’s capacity to generate larger incremental margins from the cost-reduction efforts. The important thing threat is a full-blown recession delaying the expansion cycle and impacting demand.