LeoWolfert/iStock through Getty Photographs

Heidrick & Struggles (NASDAQ:HSII) is without doubt one of the most undervalued solidly performing firms I’ve ever seen. I do loads of deep worth investing so I routinely see overwhelmed down cash dropping firms I imagine are 30-50% undervalued. However Heidrick is not a struggling firm. Not even shut. It’s a financially sturdy, solidly worthwhile and rising firm. I imagine the disconnect is partially as a result of a latest downturn in its trade that’s prone to be quick lived.

Background

Heidrick & Struggles is an government recruiting firm primarily based in Chicago. Lately it has expanded into 2 adjoining segments, On Demand and consulting. On Demand is to position momentary or interim executives. Within the first 9 months of 2023, government recruiting revenues had been 66% within the Americas, 23% in Europe and 11% in Asia and the Pacific.

In 2021, Heidrick acquired Enterprise Expertise Group, LLC for $33 million to leap begin its new On Demand section. On February 1, 2023, Heidrick acquired Atreus Group GmbH so as to add to On Demand. Heidrick paid $33.5 million and estimated future funds between $9.0 million and $13.0 million.

CEO Krishnan Rajagopalan not too long ago notified the corporate he’ll resign efficient March 4, 2024. The corporate has employed Thomas Monahan to exchange him. Mr. Monahan was the previous CEO of DeVry College and CEB. Heidrick at present pays a dividend of $0.15 per quarter for a yield of two.1%.

Business

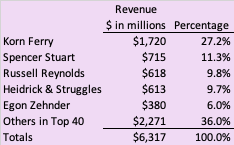

According to Hunt Scanlon the chief recruiting trade is kind of fragmented with the highest 40 companies representing $6.3 billion in annual gross sales. The highest 5 are listed beneath. Of the Prime 40, solely Korn Ferry (KFY) and Heidrick & Struggles are publicly traded.

Hunt Scanlon

The chief search trade struggled in 2020 throughout Covid lockdowns after which surged in 2021 and 2022 because the economic system, personal fairness, and enterprise capital boomed and corporations staffed again up after Covid lockdowns. In 2023 most main recruiting companies (not simply government recruiting) noticed revenues revert again to a extra regular degree.

A BDO survey launched in September 2023 confirmed 47% personal fairness CFOs and fund managers mentioned they’re understaffed in important management roles.

Based mostly on the above, the trade seems to be stabilizing, down from a surge in 2021, and 2022.

Monetary Outcomes

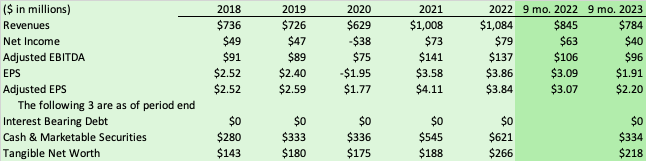

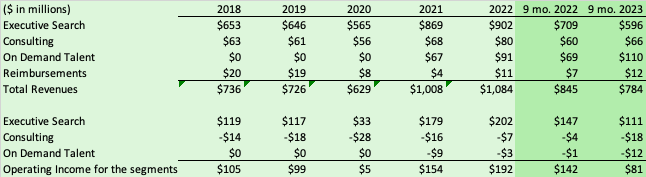

Monetary outcomes and steadiness sheet gadgets for the final 5 fiscal years and 2023 12 months so far are proven beneath. The final 2 columns evaluate the primary 3 quarters of 2023 to the identical interval in 2022.

SEC filings

Heidrick is extra conservative in what they name adjusted EPS than most different firms as they don’t add again amortization of intangibles. In the event that they did so, adjusted EPS for the 9 months ended September 30, 2023 can be $2.53.

Nearly all income development since 2020 was natural besides within the On Demand section which was principally via 2 acquisitions. The 12 months 2020 was Covid impacted. The next 2 years benefitted from a surge of demand as firms staffed up in a powerful economic system fueled by the huge fiscal stimulus, a powerful labor market, A giant enterprise capital and personal fairness surge and rehiring wanted after Covid.

The chart beneath breaks revenues and working earnings down by section.

SEC filings

Earnings are understated. Heidrick has been diversifying away from its legacy government recruiting. Within the first 9 months of 2023, 76% of revenues had been from government search. That’s down from 90% in 2020. Nonetheless, the two newer segments aren’t but worthwhile. The corporate is plowing in assets and funding in each and administration has acknowledged neither are to scale but.

If these two segments had been offered off, the corporate can be at about 47% extra worthwhile than it’s now. My calculation for that is as follows. Pretax web earnings was $64 million within the first 9 months of 2023. If the $30 million misplaced on the two newer segments is added again, that’s $94 million, or 47% greater.

Govt search revenues had been off 16% within the first 9 months of 2023. That is an trade state of affairs although the decline is greater than publicly traded rival, Korn Ferry, which was down 10%. As proven within the valuation part, Heidrick has had comparable total development to Korn Ferry over the previous 5 years.

The consulting section third quarter income grew 22% year-over-year to $23.3 million, partially as a result of a small acquisition. Natural development was 10%. Administration has acknowledged that losses there are primarily a perform of not being at scale but.

The entire On Demand section income development in 2023 was as a result of an acquisition. That section would have contracted by 16% with out that. The elevated loss in 2023 signifies the corporate acquired was dropping cash.

Complete consultants utilized in all 3 segments was 500 on September 30, 2023, up from 460 9 months earlier.

Trying Ahead

Heidrick had adjusted EPS of $2.20 within the first 9 months of 2023. The analyst’s estimate is $2.90 EPS for the total 12 months. That quantity is barely above the pre-Covid figures, however beneath 2022 and 2021. That is regardless of important income development since 2019. The analysts count on a return to EPS development in 2024 with a mean EPS estimate of $3.10. Administration is optimistic. In the newest convention name CEO Rajagopalan acknowledged “we are expecting to see strength in our markets in the short to medium term.” The corporate expects the On Demand EBITDA margins to remain round breakeven for now as they make investments and reposition. The 4Q income steerage of $240-260 million offered on the time of 3Q earnings was reconfirmed on January 23, 2024.

Stability Sheet

The steadiness sheet is powerful however the money and marketable securities degree requires some clarification. To start with, Heidrick had no curiosity bearing debt any of the final 6 years. Money and marketable securities are seasonal. It’s on the annual low on March 31 of every 12 months after which will increase the remainder of the 12 months together with a legal responsibility which is a compensation accrual. The reason being incentive pay is paid out every March. One of the best measure of money and marketable securities can be from March 31, 2023 when it was $205 million. That’s nonetheless fairly a big determine. To offer you an concept of the seasonality, money and marketable securities had been $622 million on December 31, 2022.

Catalysts and Strengths

Heidrick has a lot of catalysts and strengths however the greatest is solely valuation. This will likely be detailed extra within the valuation part the place it’s in comparison with friends.

1. EV/EBITDA Ratio of three.0 – The EV/EBITDA ratio is extraordinarily low. Adjusted EBITDA was $96 million within the first 9 months of 2023. This annualizes to $128 million. The market cap is at present $595 million. To get to enterprise worth the $205 million of money (on the low level) is deducted leaving an EV of $390 million. The EV to EBITDA ratio is 3.0. That’s nicely beneath the market averages of 11 to 16 per Investopedia and the bottom I’ve ever seen for a worthwhile firm with an excellent steadiness sheet and good prospects.

2. Robust Stability Sheet – The sturdy steadiness sheet mentioned above means extra flexibility than most publicly traded firms. The corporate can simply improve development with acquisitions, enhance the dividend or buyback inventory. The market they serve is fragmented and there are a lot of potential acquisition targets. The corporate pays a market common dividend however has achieved few inventory repurchases.

3. Sentiment – You’ll recall that for a lot of 2023, most economists had been predicting a recession inside a 12 months. This led to firms being extra cautious about hiring. Most economists are now not making that prediction. That is truly a giant one for me.

4. Company Development – Company development has continued strongly in recent times regardless of a drop off within the personal fairness and enterprise capital industries. These industries have been damage by the collapse of the IPO market attributable to too many overvalued IPOs in 2021 and 2022. The IPO market ought to ultimately return to regular ranges making a tailwind. In the meantime publicly traded and privately owned company development continues unabated that means extra want for executives.

5. Child Boomer Retirements – A lot of company executives are Child Boomers. That era is more and more reaching retirement age and can must be changed.

6. Heidrick Navigator – It is a new digital AI resolution for management assessments, teamwork, and group and tradition that may be delivered nearly. It’s at present in Beta testing however a primary contract was not too long ago introduced.

7. Earnings are Understated – The two smaller segments representing 24% of revenues are at present unprofitable however anticipated to offer future development and earnings. If they’re excluded, the corporate is 47% extra worthwhile than it’s exhibiting. Each may be offered or closed at any time in the event that they don’t work out. Additionally, when Heidrick calculates adjusted EPS, it doesn’t add again amortization from acquisitions like most different firms. Their Adjusted EPS was $2.20 for the primary 3 quarters of 2023. It was $2.52 if amortization is added again.

Considerations

I at all times listing my considerations and weaknesses when writing about an organization. Listed here are a few of the bigger ones.

1. Losses at Two Newer Segments – Each the consulting and On Demand segments are dropping cash and never anticipated to be worthwhile this 12 months. These segments trigger earnings to be considerably understated since they may promote or shut these segments at any time. They’re investments in future development and diversification.

2. European Publicity– Heidrick has extra European publicity than lots of its friends. About 22% of government search and the vast majority of On Demand is European. The European economic system is bouncing round breakeven at present and in higher years often grows extra slowly than the U.S. and Asia.

3. Cyclical– This trade is cyclical as not too long ago confirmed by the drop off within the recession 12 months of 2020, the surge in 2021 and 2022, and a newer drop off in 2023.

4. Insider Inventory Sale – The CFO offered 6000 shares 12/12/23. It ought to be famous he had been granted 17,580 shares in June, 2023. There have been no latest open market insider buys.

Valuation

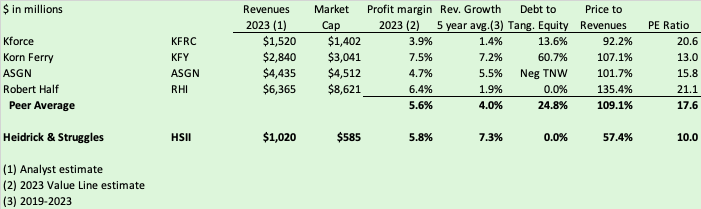

Heidrick has a really comparable peer in Korn Ferry. KFY has a really comparable footprint in that it additionally does consulting and on demand government search. Three different friends Kforce (KFRC), Robert Half (RHI) and ASGN (ASGN) fka On Project had been included as all of them give attention to recruiting professionals. I excluded blue collar recruiters equivalent to Kelly and TrueBlue which have a lot smaller revenue margins and well being care recruiters equivalent to Cross Nation and AMN since they focus on one trade.

SEC filings, Yahoo Finance & Worth Line

Whereas it isn’t proven above, all the above had income declines within the first 3 quarters of 2023. Over a 5 12 months interval, Heidrick has outgrown all however Korn Ferry, which had comparable development. Heidrick’s revenue margin is just like the peer. It could be greater if not for the cash dropping smaller segments. Heidrick has much less leverage than all however Robert Half. ASGN is kind of leveraged. General Heidrick has higher metrics than all however Korn Ferry, which has similarities however bigger.

Regardless of having higher metrics than its friends, Heidrick’s present market worth is nicely beneath them. It’s priced about half for the value to revenues ratio as Korn Ferry and the friends as a complete. Their PE ratio is 43% much less. As famous earlier, Heidrick has a ridiculously low EV/EBITDA ratio of three.0. The inventory worth to free money move ratio, it is usually very low. Free money move in 2023 YTD annualized (web earnings + depreciation and amortization plus or minus non-recurrings much less capex) is $79 million, just like $79 million in 2022. That leaves a inventory worth to free money move ratio of seven.5. The market common is often greater than double that.

Any approach you have a look at it Heidrick is buying and selling nicely beneath the market and its friends. But it is a traditionally solidly rising firm with comparable prospects to friends going ahead. Based mostly on the peer PE ratio and worth to revenues, it ought to be buying and selling 75% above its present degree of $29.56. That will convey it to $51.73. That will return it to the $50 it reached in September 2021.

Takeaway

There are actually catalysts right here, however the true story is excessive undervaluation. Heidrick has a historical past of stable development and a powerful steadiness sheet. But it trades for a 30-50% low cost to its friends. That low cost will get even bigger while you exclude its smaller cash dropping segments and the money on its steadiness sheet. I like to recommend a protracted place in Heidrick & Struggles with a one 12 months worth goal of $52.