Michael M. Santiago

The JPMorgan Hedged Fairness Laddered Overlay ETF (NYSEARCA:HELO) is an ETF model of JPMorgan’s massively profitable Hedged Fairness Fund (JHEQX). It goals to enhance upon the JHEQX fund by using a discretionary laddered possibility technique as a substitute of following a hard and fast quarterly schedule.

Since HELO is managed by the identical administration workforce utilizing broadly related methods, I imagine the HELO ETF’s returns might be similar to JHEQX. Though JHEQX’s historic returns have been modest, the fund has been in a position to compress volatility, thus delivering higher threat adjusted returns to buyers.

I fee the HELO ETF a tentative purchase for conservative buyers who wish to be partly protected on the draw back and don’t thoughts giving up some upside returns.

Fund Overview

The JPMorgan Hedged Fairness Laddered Overlay ETF goals to offer buyers with publicity to a portfolio of U.S. giant cap shares with a laddered choices technique to guard draw back threat from falling markets. The aim of the HELO ETF is to seize the vast majority of the S&P 500 Index’s returns with decreased volatility and draw back.

The HELO ETF is newly launched with an inception date of September 28, 2023, so there may be not numerous working historical past. Nonetheless, the underlying technique employed by the HELO ETF has been utilized by JP Morgan for years in its Hedged Fairness mutual funds (JHEQX, JHQDX, JHQTX)

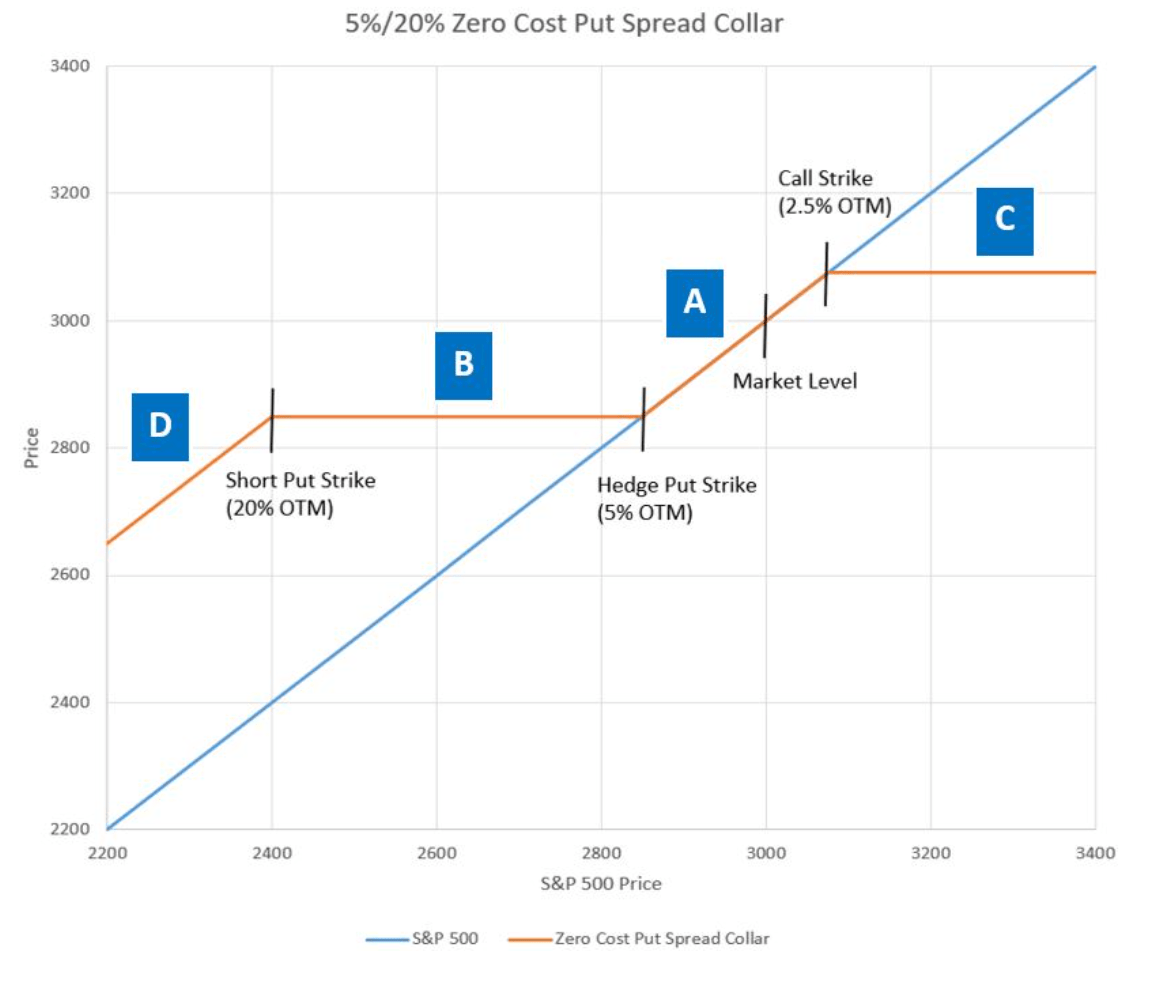

The fundamental technique for the JP Morgan Hedged Fairness funds is to put money into a portfolio U.S. giant cap shares, with the entire portfolio protected through a put spread collar utilizing SPX choices. Draw back is decreased through a put unfold that’s financed by promoting upside calls (Determine 1).

Determine 1 – Illustrative put unfold collar (swanglobalinvestments.com)

JP Morgan has been extraordinarily profitable with its Hedge Fairness technique, with the three aforementioned mutual funds hoovering up a mixed $24 billion in property and the HELO ETF seems to be aiming to duplicate this success within the ETF house. To this point, the HELO ETF has accrued over $100 million in property in 2 months of operation. The HELO ETF fees a 0.50% web expense ratio.

Laddered Choices Partly Deal with JHEQX Weak point

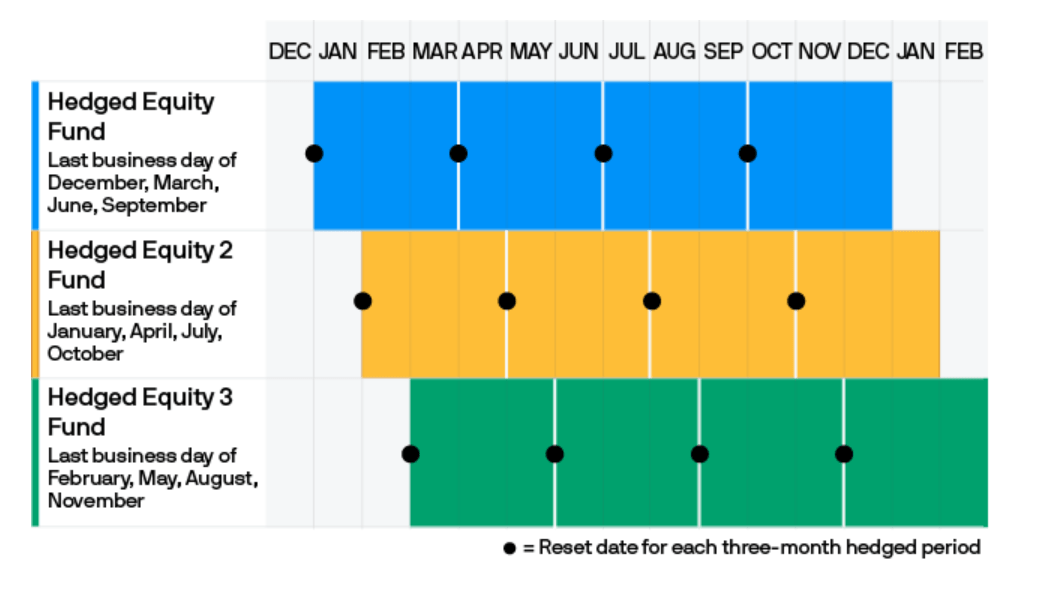

One criticism of JP Morgan’s success is that the JHEQX has turn out to be so giant that its quarterly hedging operations are actually closely anticipated by market contributors and front-run (Determine 2).

Determine 2 – JHEQX quarterly hedging schedule (am.jpmorgan.com)

The HELO ETF goals to enhance upon JHEQX by using a laddered possibility technique whereby the fund holds choices for a number of (usually, three) three-month durations (every interval is taken into account a “hedge window”), staggered a month aside. The fund supervisor additionally has discretion on how a lot publicity to allocate to every hedge window. HELO’s laddered possibility technique goals to reduce the market impression of the hedging operations by spreading it out month-to-month as a substitute of on a constant quarterly schedule.

Portfolio Holdings

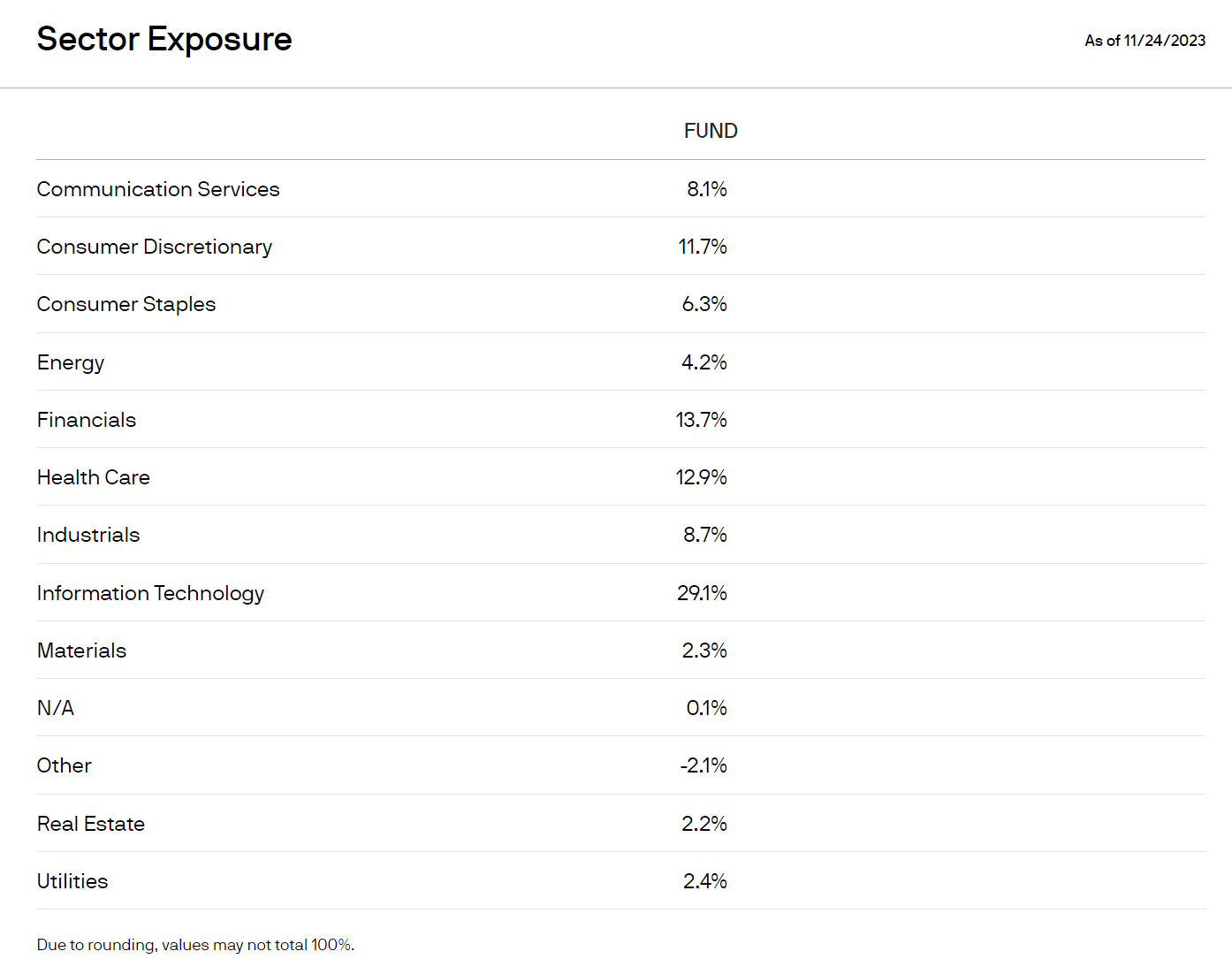

The HELO ETF has 163 positions and Determine 3 reveals the fund’s sector allocation. The HELO ETF’s largest sector allocations are Info Know-how (29.1%), Financials (13.7%), Well being Care (12.9%), Client Discretionary (11.7%), and Communication Companies (8.1%).

Determine 3 – HELO sector allocation (am.jpmorgan.com)

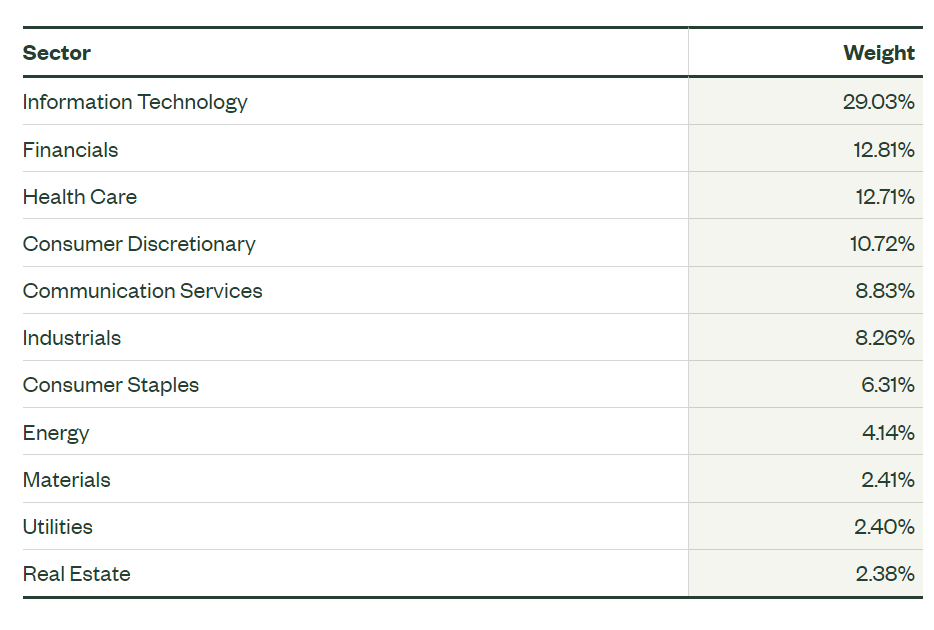

Determine 4 reveals the sector allocation of the SPDR S&P 500 ETF Belief (SPY) for comparability. HELO’s sector allocations are roughly much like SPY’s, with sector weights all inside 1% of SPY’s weights.

Determine 4 – SPY sector allocation (ssga.com)

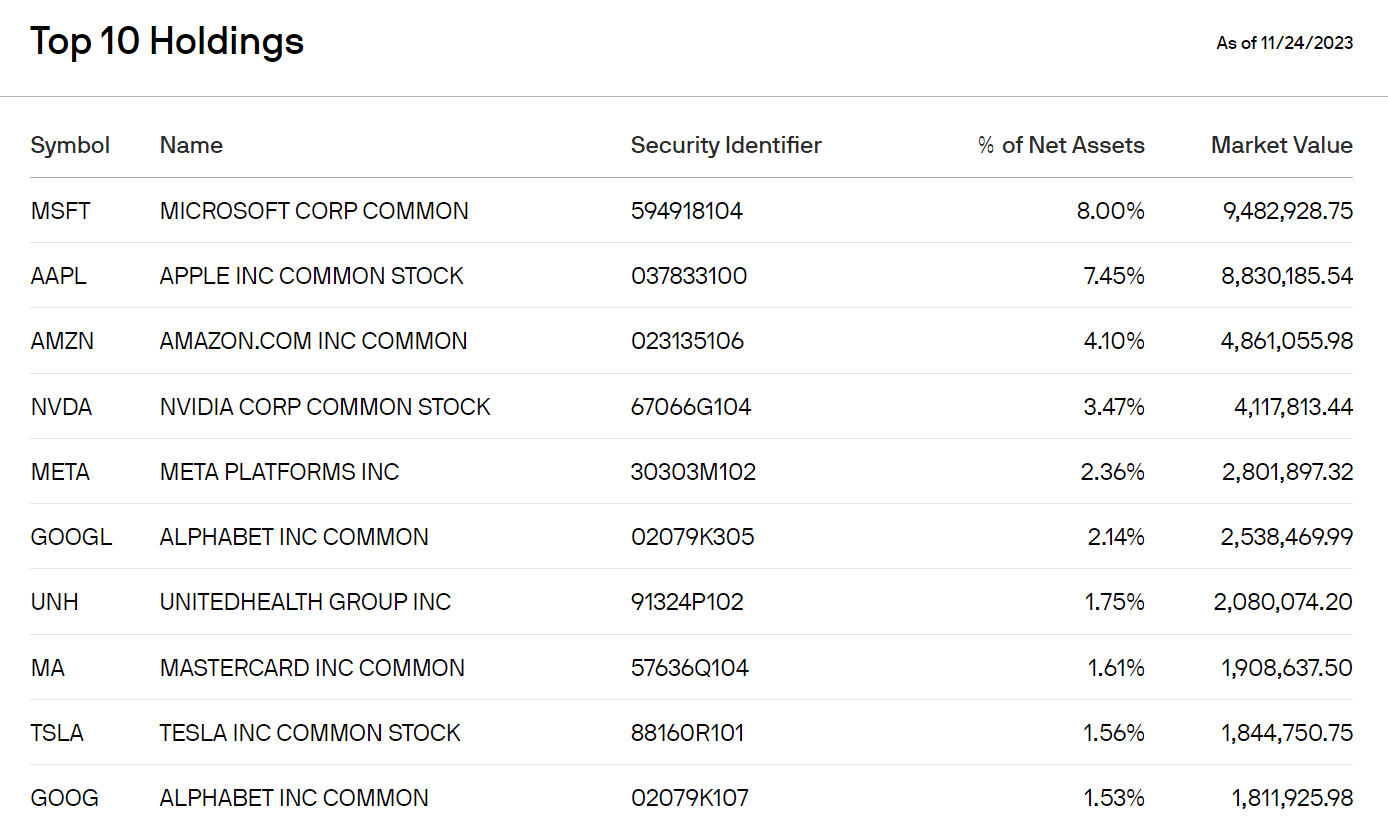

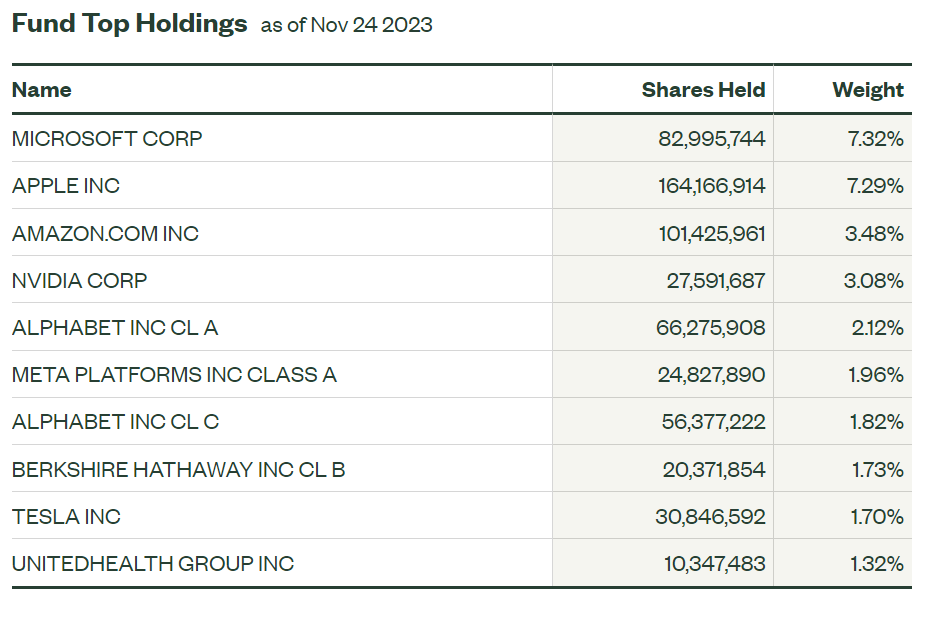

The highest 10 holdings for HELO (Determine 5) and SPY (Determine 6) are virtually similar, excluding HELO holding Mastercard as a prime 10 weight whereas SPY holds Berkshire Hathaway.

Determine 5 – HELO prime 10 holdings (am.jpmorgan.com) Determine 6 – SPY prime 10 holdings (ssga.com)

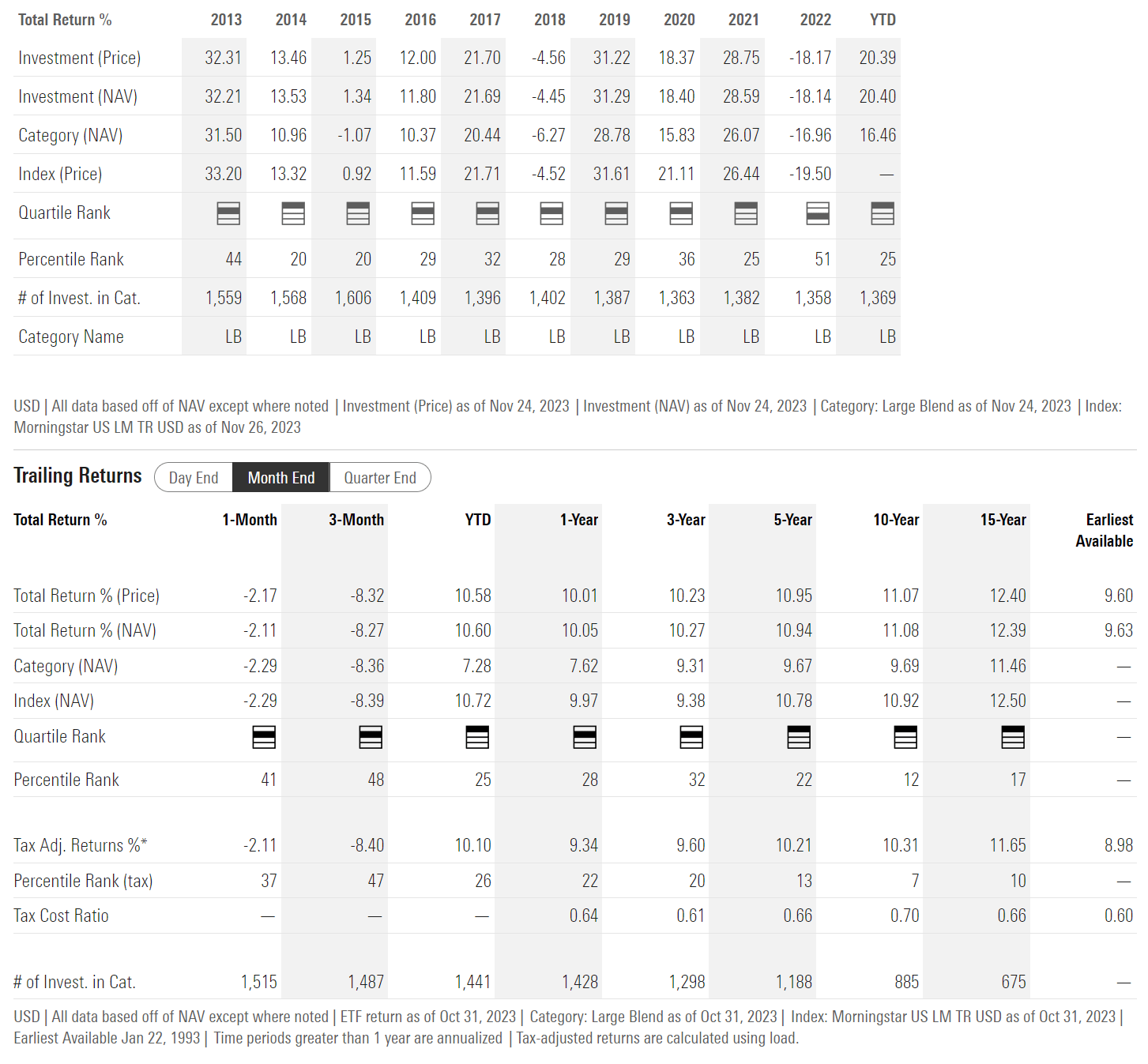

Returns

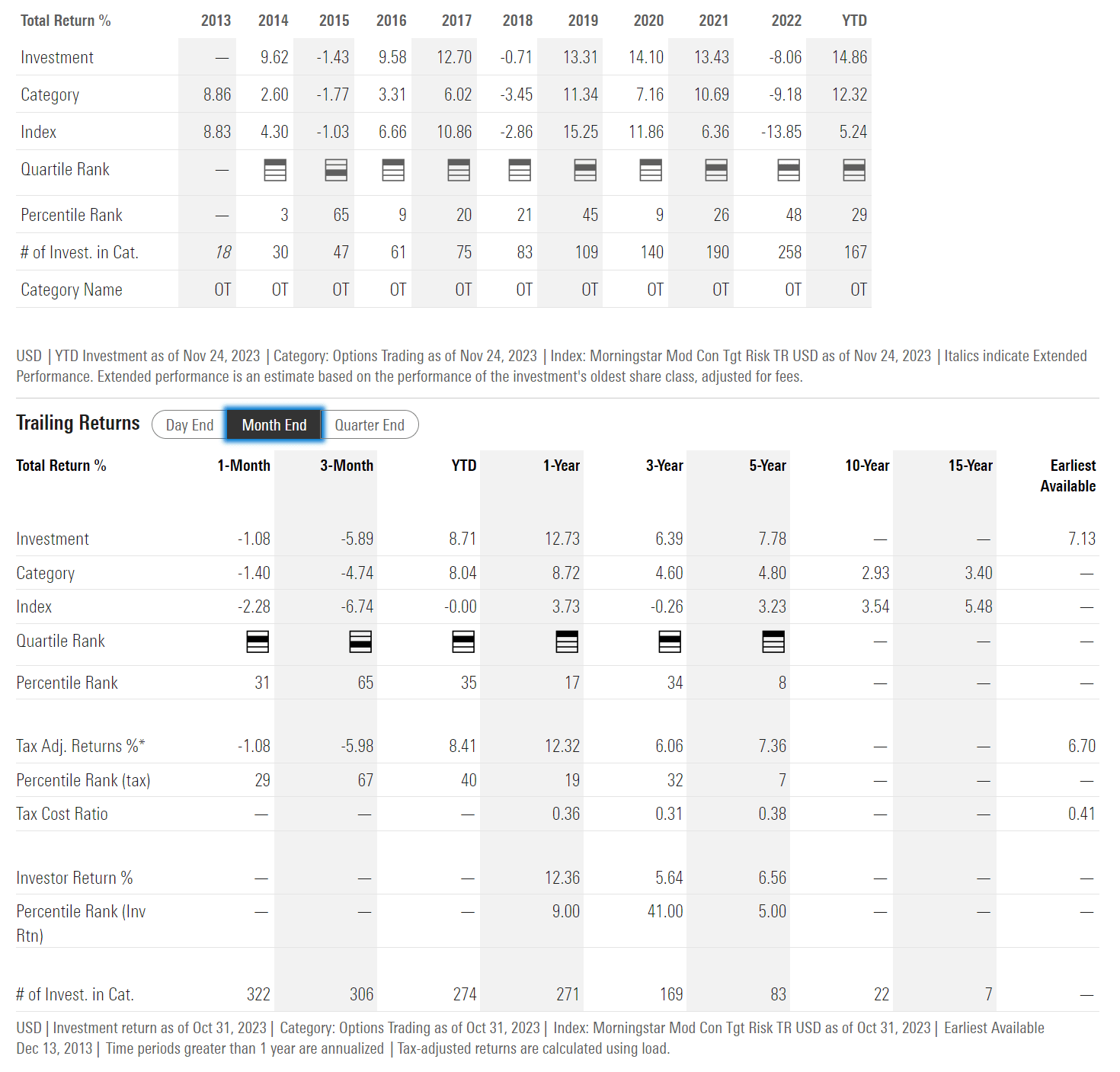

Because the HELO ETF has solely been in operation for lower than 2 months, there may be not numerous efficiency historical past to research. As an alternative, I imagine it might be informative to research the efficiency historical past of JHEQX to see what degree of returns can moderately be anticipated for HELO.

Traditionally, JHEQX has delivered 3 and 5-year common annual returns of 6.4% and seven.8% respectively to October 31, 2023 (Determine 7).

Determine 7 – JHEQX historic returns (morningstar.com)

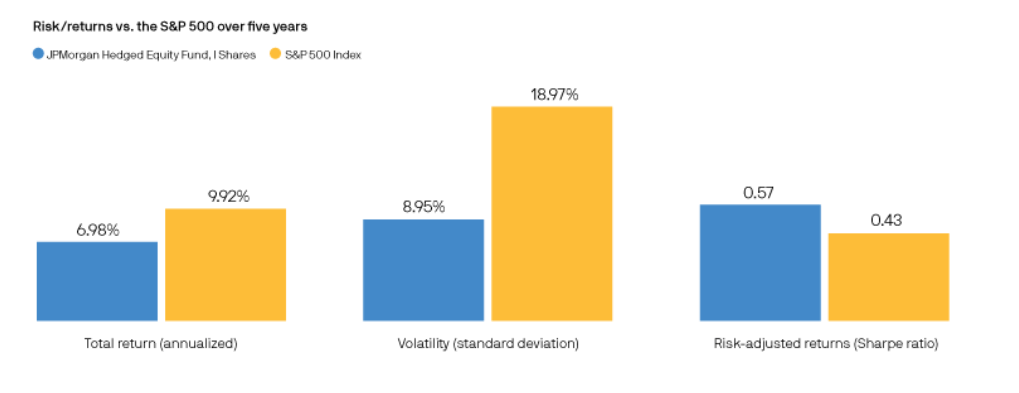

Whereas JHEQX’s absolute returns have been modest, what JPMorgan emphasizes is the low volatility of JHEQX’s returns. For instance, in response to the supervisor’s information, JHEQX has delivered 70% of the S&P 500’s returns for the previous 5 years (to September 30, 2023) with simply 47% of the danger (volatility), resulting in the next Sharpe Ratio (Determine 8).

Determine 8 – JHEQX has higher risk-adjusted returns than market (am.jpmorgan.com)

Hedged Fairness Offers Traders Peace Of Thoughts

A generally repeated axiom of investing is that “time in the market beats timing the market”. Regardless of decrease complete returns, JHEQX’s decrease volatility and drawdowns could also be helpful in the long term, because it provides buyers peace of thoughts and permits them to carry onto their fairness investments as a substitute of panic-selling throughout inevitable bear markets.

Dangers To Hedged Fairness Technique

Nonetheless, HELO/JHEQX’s put unfold collar technique just isn’t with out dangers. First, the promoting of calls to fund the put unfold implies that throughout sturdy bull markets, HELO/JHEQX’s technique will lag considerably. For instance, in the course of the sturdy bull market in 2021, JHEQX solely returned 13.4% whereas the SPY ETF returned 28.6% for an upside seize of lower than 50% (Determine 9).

Determine 9 – SPY historic returns (morningstar.com)

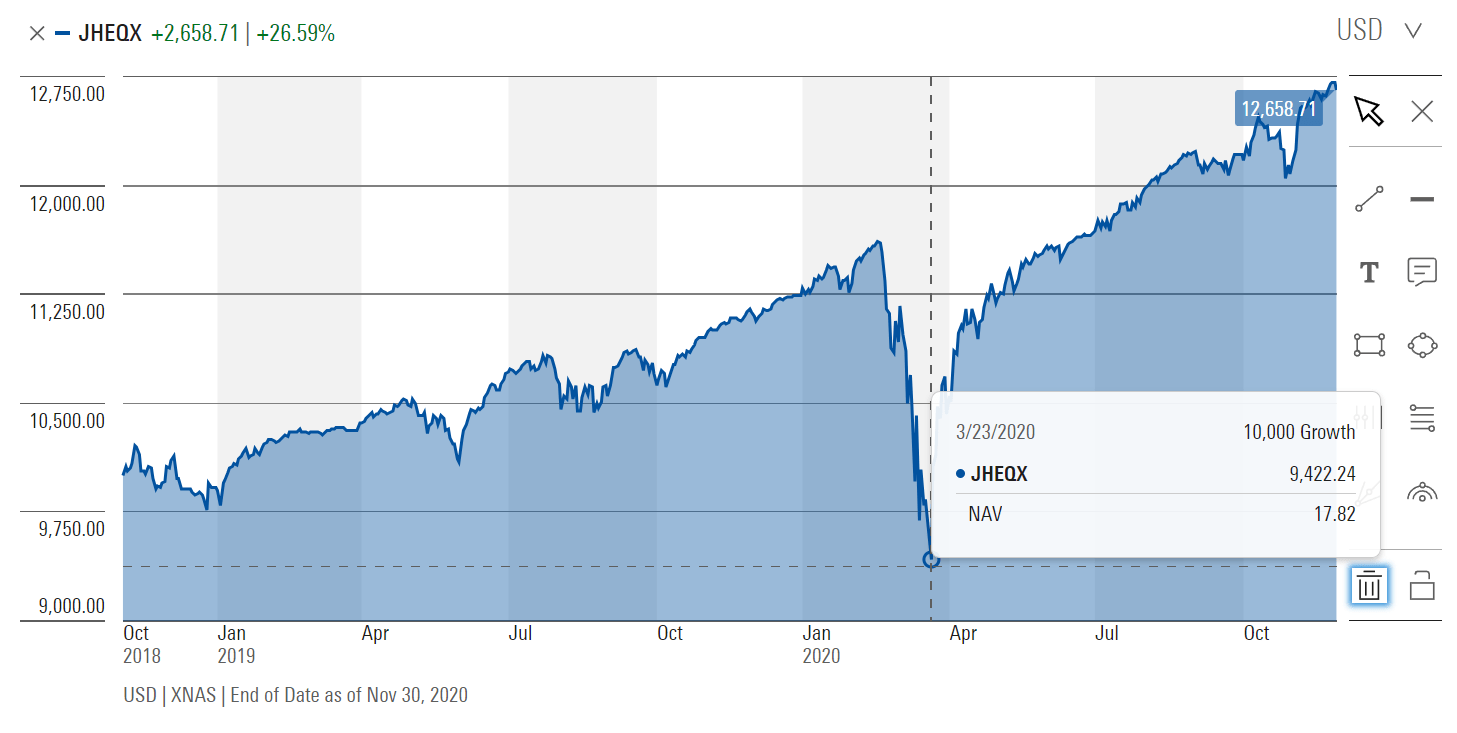

Secondly, HELO/JHEQX’s put unfold solely protects the portfolio from a 5 to twenty% drawdown throughout the “hedge window”. If markets crash like they did within the early days of the COVID pandemic, JHEQX’s NAV can nonetheless fall greater than 5%. From February 21, 2020 to March 23, 2020, JHEQX’s NAV fell by 18.8% in comparison with a 33% decline within the SPY ETF in the identical time-frame (Determine 10).

Determine 10 – HELO/JHEQX can nonetheless fall throughout market crashes (morningstar.com)

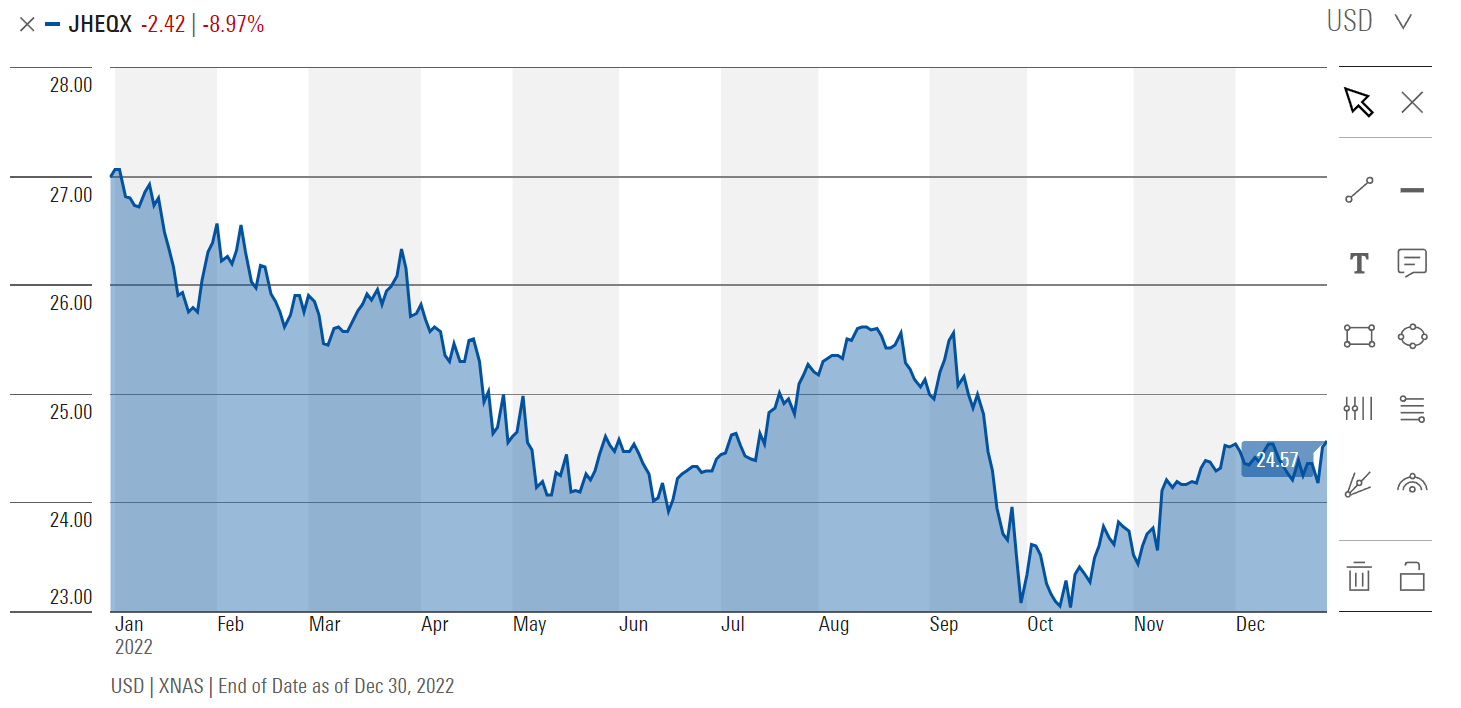

Moreover, if declines are protracted, like in 2022, HELO/JHEQX’s technique could cumulatively lose greater than 5%. On the nadir, the JHEQX NAV misplaced 14.4% in 2022, earlier than a year-end restoration decreased losses (Determine 11).

Determine 11 – HELO/JHEQX may also lose greater than 5% in protracted bear markets (morningstar.com)

Conclusion

The JPMorgan Hedged Fairness Laddered Overlay ETF goals to offer buyers with the vast majority of the S&P 500 Index’s returns whereas lowering volatility and draw back seize.

HELO seems to be an ETF model of JPMorgan’s a lot heralded Hedge Fairness mutual funds. Nonetheless, it improves upon the JHEQX fund by using a laddered possibility technique that minimizes the potential market impression of the hedging operations.

The HELO ETF’s aim is to offer buyers a smoother funding expertise by using a put unfold collar technique. Traditionally, the JHEQX mutual funds have been in a position to seize 70% of the S&P 500’s returns with solely 47% of the Index’s volatility for a greater Sharpe Ratio. For the reason that HELO ETF is managed by the identical funding workforce and employs related methods because the JHEQX, I count on returns might be related as effectively.

The draw back to the HELO ETF is it might lag considerably throughout sturdy bull markets, and it might nonetheless lose greater than 5% throughout market crashes or extended bear markets.

I imagine the HELO ETF could attraction to conservative buyers who wish to be considerably shielded from sharp market drawdowns.