georgeclerk

Funding briefing

Selective alternatives throughout the industrials sector proceed to current us with a gorgeous threat reward profile in our opinion. Nearing the top of This autumn 2024 earnings season FactSet analysis estimates that the earnings development charge for the S&P 500 index is 1.5% to date. For the industrials sector, the blended earnings development charge has elevated to 1.4%, in keeping with the broad index.

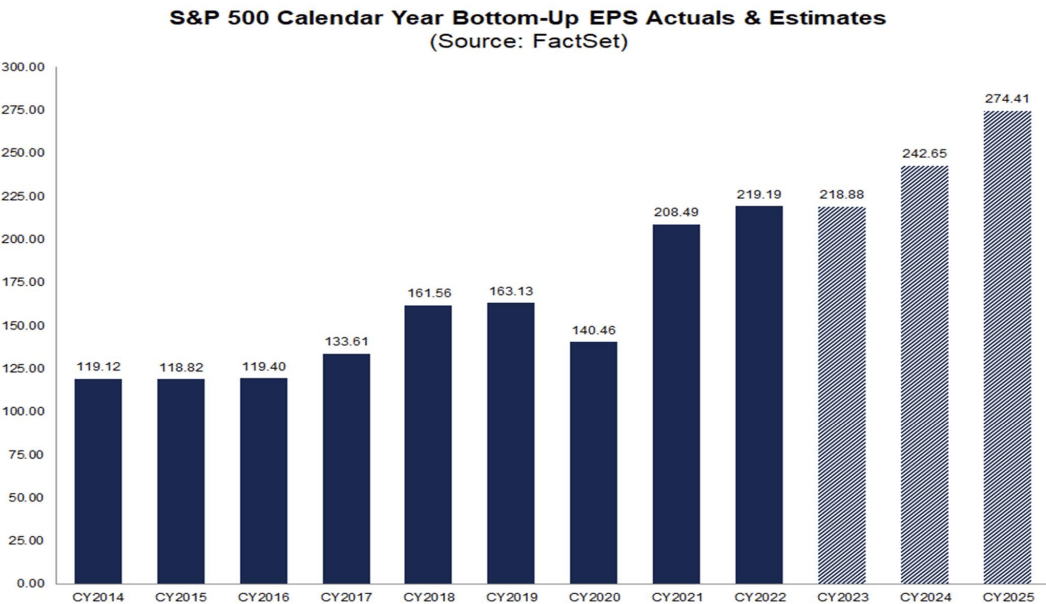

In the meantime, bottom-up EPS estimates for the index are calling for $242/share in CY’24, development to $274/share past this. Name this optimistic, nevertheless it a minimum of implies contribution from fundamentals this yr in our estimation.

Determine 1.

Supply: FactSet

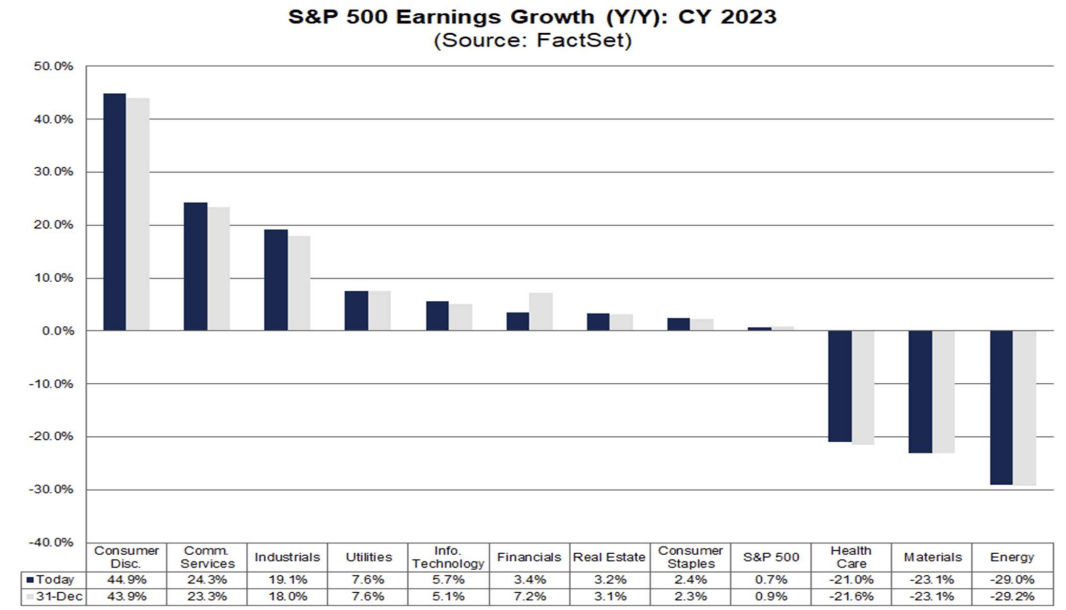

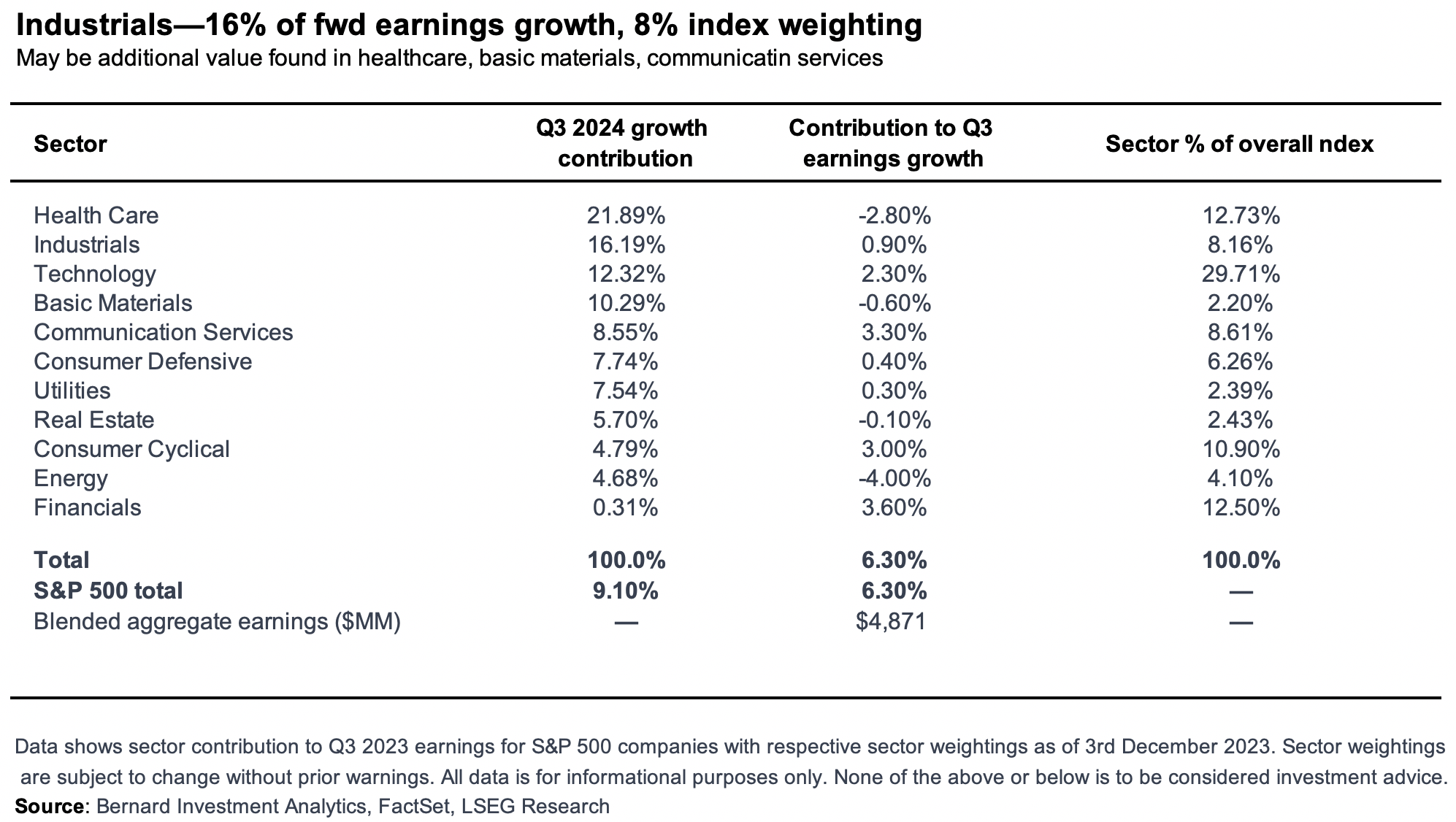

Turning again to the sector, the industrials group posted 19% YoY earnings development in FY’23 in line with FactSet, third within the pack from shopper discretionary and communication companies. I’d refer readers to our composite in Determine 3 that was posted on the finish of Q3 2023 earnings. Again then we had recognized the commercial sector held simply 8% notional worth of the market weighted index, however was projected to ship 16% of the forecasted earnings development over the approaching 12 months (avid readers of mine may have seen the graphic in Determine 3 fairly extensively). Level is that there continues to current compelling proof of threat unlock within the sector this yr.

Determine 2.

Supply: FactSet

Determine 3.

Our funding mandate permits us to purchase and promote the marketable securities of corporations which have enticing enterprise economics. With out making it too difficult, the easy course of is to examine any – if in any respect– corporations are rising at excessive charges of return, or are rising with little capital necessities, to gush free money move. Then, all that is wanted is a fast examine to see if the market is valuing this appropriately in line with our paradigms.

This course of to top-down safety choice has led us to the frequent inventory of Herc Holdings (NYSE:HRI). HRI is within the rental and tools provide enterprise, with differentiated choices in heavy automobile options, earthmoving and transport. It additionally gross sales numerous provides to rearrange contractors and has a footprint within the petrochemical and aerospace industries, together with adjoining industries in agriculture, morning, and the meals and beverage business.

We’ve got famous the next key drivers of funding return and a number of re-rating:

- Little working capital required to provide $3Bn in TTM gross sales and $700mm in pre-tax earnings.

- Promoting at 12x ahead earnings, 13x ahead EBIT, each steep reductions to the sector, and enticing in absolute phrases.

- Compounding earnings with little incremental capital funding, which means it will possibly throw off FCF to shareholders with out jeopardising development, and vice versa.

Conclusions derived from elements raised on this report are encouraging for these traders searching for long-term compounders who develop earnings with little volatility in multiples. We’re constructive on HRI and charge the corporate a purchase with preliminary worth targets of $164/share.

Transient commentary on upcoming earnings

The corporate is about to report its This autumn 2024 earnings subsequent week. For my part, the corporate is effectively positioned to ship a stable outcome. For one, administration are constructive on HRI’s development for the following 2 years (mentioned later). It’s calling for CAGR 10 – 14% annualized income development on this time. To me it is a bullish signal, however a excessive watermark for the corporate to beat come earnings time.

The second factor is the consensus estimates. Wall Avenue is eyeing 11% YoY development on the backside line, which is not an unreasonable quantity. A draw back shock from this quantity might be exceptional, nevertheless. We have seen the market react violently to earnings misses already this yr, so unlikely HRI can be completely different on this respect.

One should additionally think about the ‘established’ earnings of the corporate so far:

(1). 37% trailing gross margin,

(2). 21% trailing EBIT margin,

(3). Return on fairness of 31% during the last 12 months.

These are compelling numbers that sign earnings momentum in our view. Primarily based on these rudimentary insights, our posture is HRI is about to come back in with a robust set of numbers. Alas, the chance is that it surprises to the draw back, and traders must be effectively conscious of this.

Crucial funding findings

Primarily based on our evaluation, the next set of information factors kind the crux of the bull thesis:

(1). Brief-term and medium-term catalysts:

- Prime and backside line development forecasts

- Beginning valuations

(2). Lengthy-term catalysts:

- Capital allocation

- Development in earnings attributable to shareholders

Brief and mid-term catalysts

One catalyst that instantly stood out is a latest announcement by the corporate in November final yr, focusing on “organic rental revenue of 10% to 14% CAGR from 2024 through 2026, and established an organic adjusted EBITDA CAGR of 11% to 16% over the same period.”

If the corporate hit these sort of development charges, it could be c.4 share factors larger than its 5-year common revenue growth rate, and one other 3 share factors larger than its 5-year development in pretax earnings.

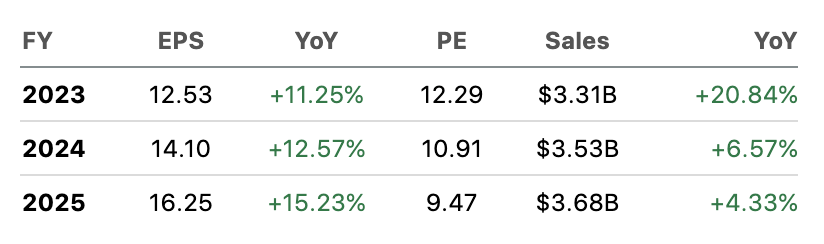

Administration’s view is supported by the truth that consensus estimates challenge a waterfall development schedule for HRI out to 2025. The median of analyst estimates expects 11% to fifteen% earnings development over the following 2 years together with single digit high line development of common throughout this era.

Determine 4.

Supply: In search of Alpha

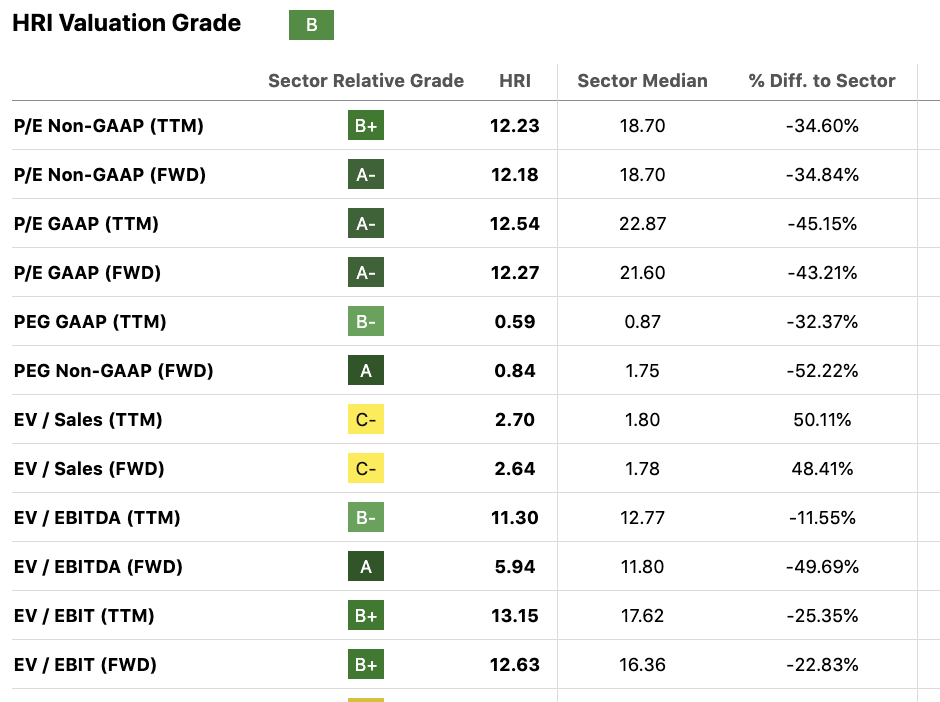

Equally as compelling for near-term returns is the beginning valuations at which the corporate might be purchased immediately. As seen in Determine 5, is at the moment trades at 12.2x forward earnings and round 12.6x ahead EBIT. These are steep reductions to the sector of greater than 30% and 22% respectively.

What’s essential right here is that beginning evaluations heavily decide the primary 12 months funding returns for any public funding safety. Shopping for shares at relative reductions– offered there may be the standard property underlying the enterprise–does present a statistical benefit particularly for close to time period beneficial properties to the fairness portfolio.

Have in mind we’re paying 12x for an organization that:

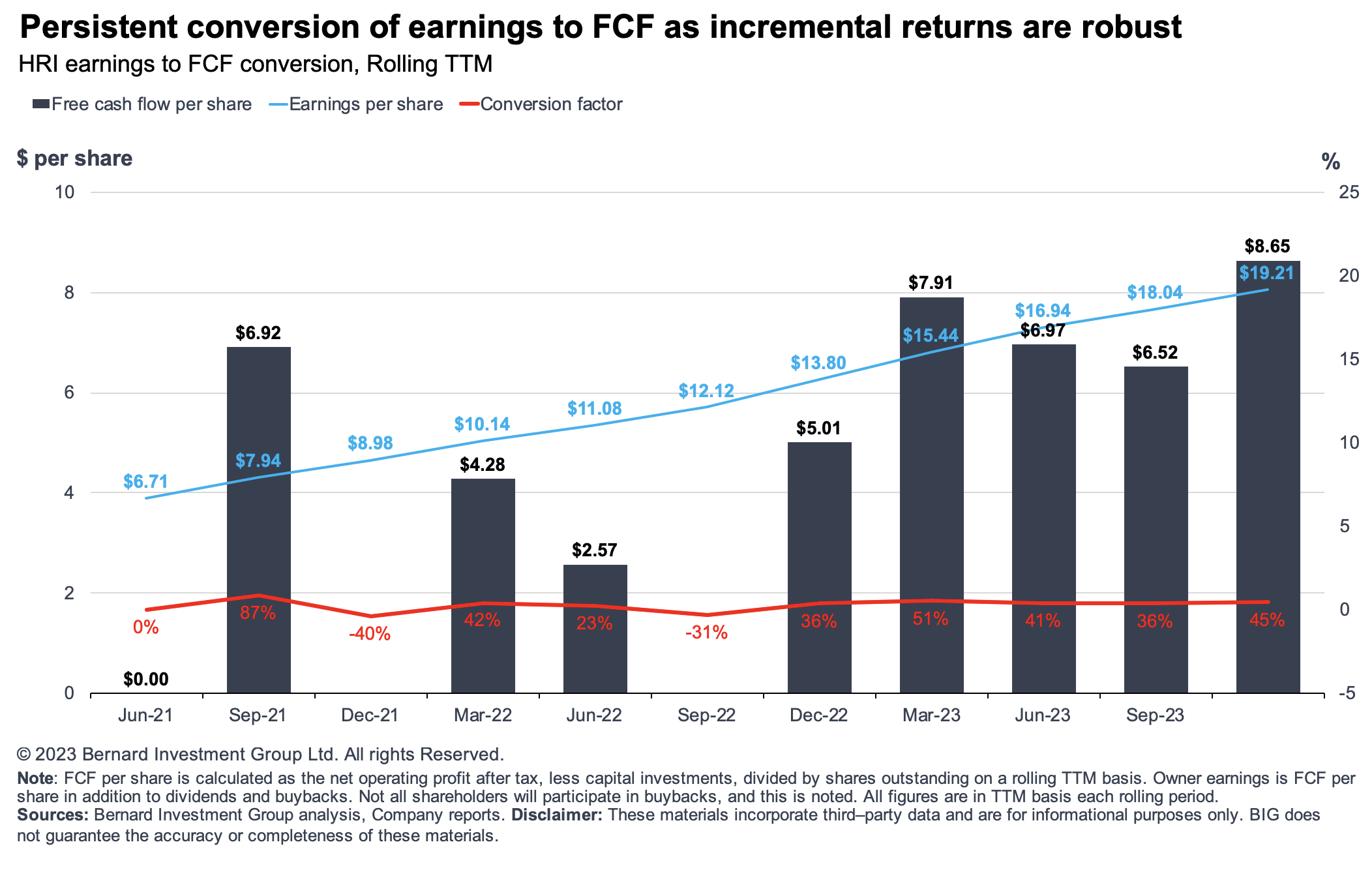

- Has grown free money move per share from $2.60 in Q2 2022 two $8.65 within the final interval on a rolling TTM foundation.

- Publish-tax earnings, measured right here as web of score revenue after tax, have additionally crept larger in close to linear trend. The corporate has grown its tax adjusted working earnings per share from $6.17 in 2021 as much as $11 on the identical time in 2022 $17 stress in 2023 and printed $18 per share in TTM NOPAT final interval (Determine 6).

Determine 5.

Supply: In search of Alpha

By the very best estimation these are usually not the hallmarks of an organization that must be closely discounted to a development sector. The corporate can also be methodically turning earnings into free money move on the charge of round 35 to 40% on common within the final 18 months, as seen in Determine 6.

Furthermore, as we’ll focus on later, it seems that development might be engendered on little or no allocation to working capital. Within the final three years gross sales, rising at a compound in charge of 6%, required $0.10 for each new $1 of gross sales, in comparison with $0.40 on the greenback for fastened capital. We imagine it is a constructive level and must be factored into the funding debate, as a result of it provides bullish tilt to the chance reward calculus for the brief time period funding horizon.

Determine 6. Be aware: The undated Final bar is the estimate for This autumn 2023.

Lengthy-term catalysts

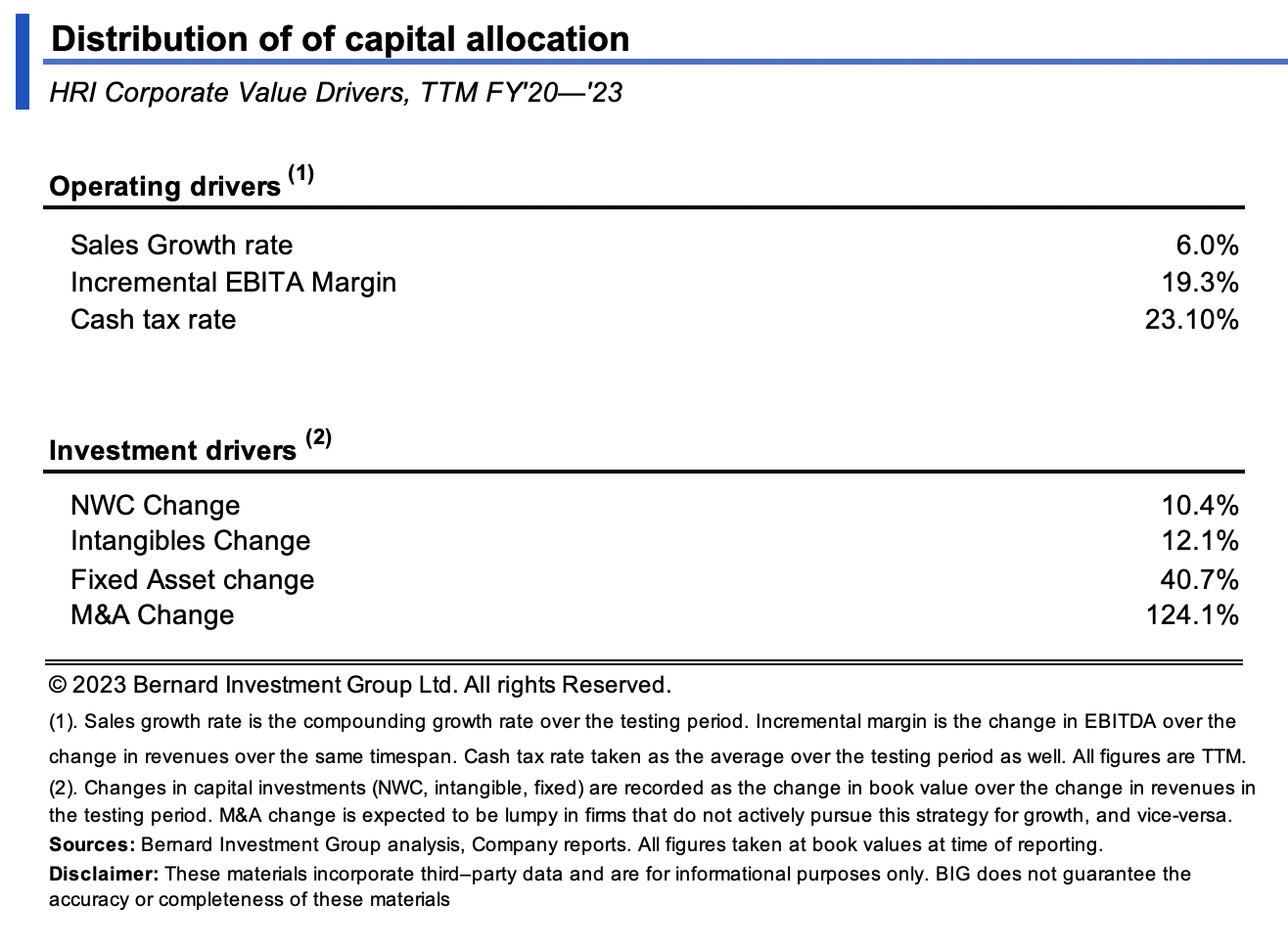

Lengthy-term catalyst might be grouped into two buckets, (i) capital allocation and (ii )enterprise returns. For the previous, the corporate’s distribution of incremental capital is listed in Determine 7. From the three years to Q3 2023, the corporate grew gross sales at a 6% compounding charge.

For capital allocation:

- As talked about earlier this development was engendered on little or no incremental working capital. The majority of the corporate’s money is tied up in its rental tools. Nonetheless these property produce a prolonged tail of returns whereby money is obtained upfront on the time of service supply. As a result of fee is made up entrance, this reduces the corporate’s money conversion cycle and there may be much less threat money being inefficiently tied up in working capital.

- For each new $1 in gross sales since 2020, this required simply $.10 funding in web working capital. The corporate additionally contributed $0.12 on the greenback to intangible property together with $1.24 per $1 in new gross sales two acquisitions and the change in rental tools which is booked on the stability sheet as such, however recorded because the change in M&A.

Ought to these tendencies proceed it suggests that each new one greenback of gross sales would require round $2.10 of investments to develop, dropping to round $0.80 when stripping out the adjustments to the rental tools on the asset aspect of the stability sheet. The important thing factors being that we imagine that firm can produce a greenback with $0.80 funding, thereby unlocking shareholder worth.

Determine 7.

For enterprise returns:

The scope for HRI to commerce larger of those multiples is bolstered by this development outlook and the financial worth that’s artistic to shareholders. Critically, findings present it’s compounding the speed of earnings produced on incremental capital, thereby rising post-tax earnings off every new $1 put it again to work within the enterprise. It’s right here the place we see long-term worth within the firm:

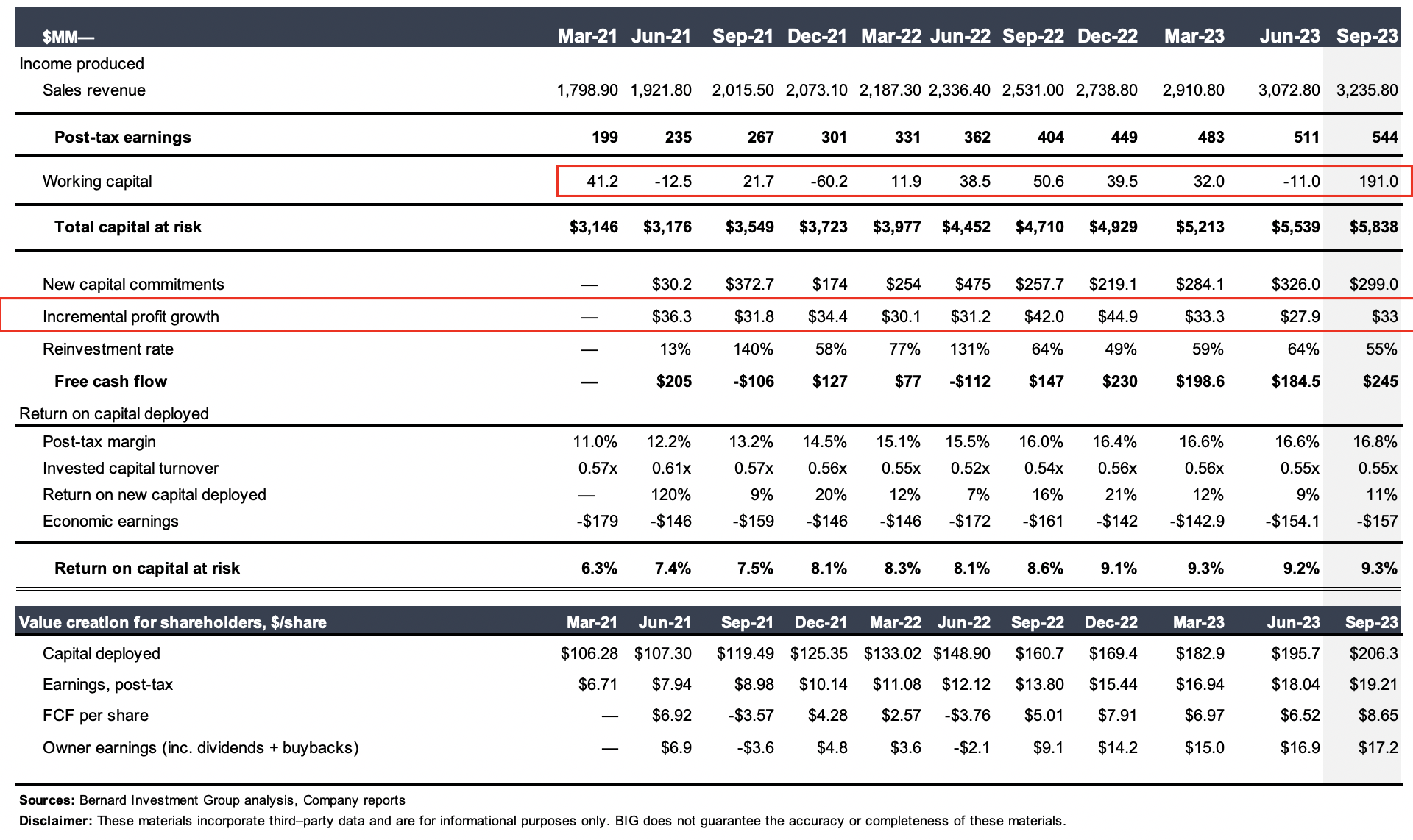

- As seen in determine 8, the corporate has round $206 per share of capital in danger invested in its enterprise property. On this, it produced $19.20 per share of web working revenue after-tax in Q3 ’23, a 9.3% return on funding. That is in keeping with its historic averages and even 300 foundation factors larger than what it clipped in Q1 2021.

- Nonetheless the incremental outcomes are what’s creating the momentum in our opinion, and what’s but to be totally appreciated by the market.

- The corporate has been efficiently reinvesting a big portion of its after-tax earnings to engender future development and keep its aggressive place. It has put >$250mm of capital to work every quarter at a minimal since 2021, indicating this stance.

- On these investments, the expansion ramp on its earnings has steepened, having elevated post-tax earnings per share from $6.70 in 2021 to $19.20 within the final report on a TTM foundation. It has achieved this on an funding of $106 per share, in any other case 12.5% incremental return on funding.

- By all measures, we imagine these returns – that are prone to mirror the corporate’s inventory worth returns – will proceed.

This lays the bedrock for an funding thesis shifting ahead. We’ve got right here firm that’s constantly compounding earnings on every steady use of capital. As a reminder capital is the lifeblood of any enterprise and is just the money that’s used for the acquisition of property or the technique of manufacturing.

Determine 8.

Valuation

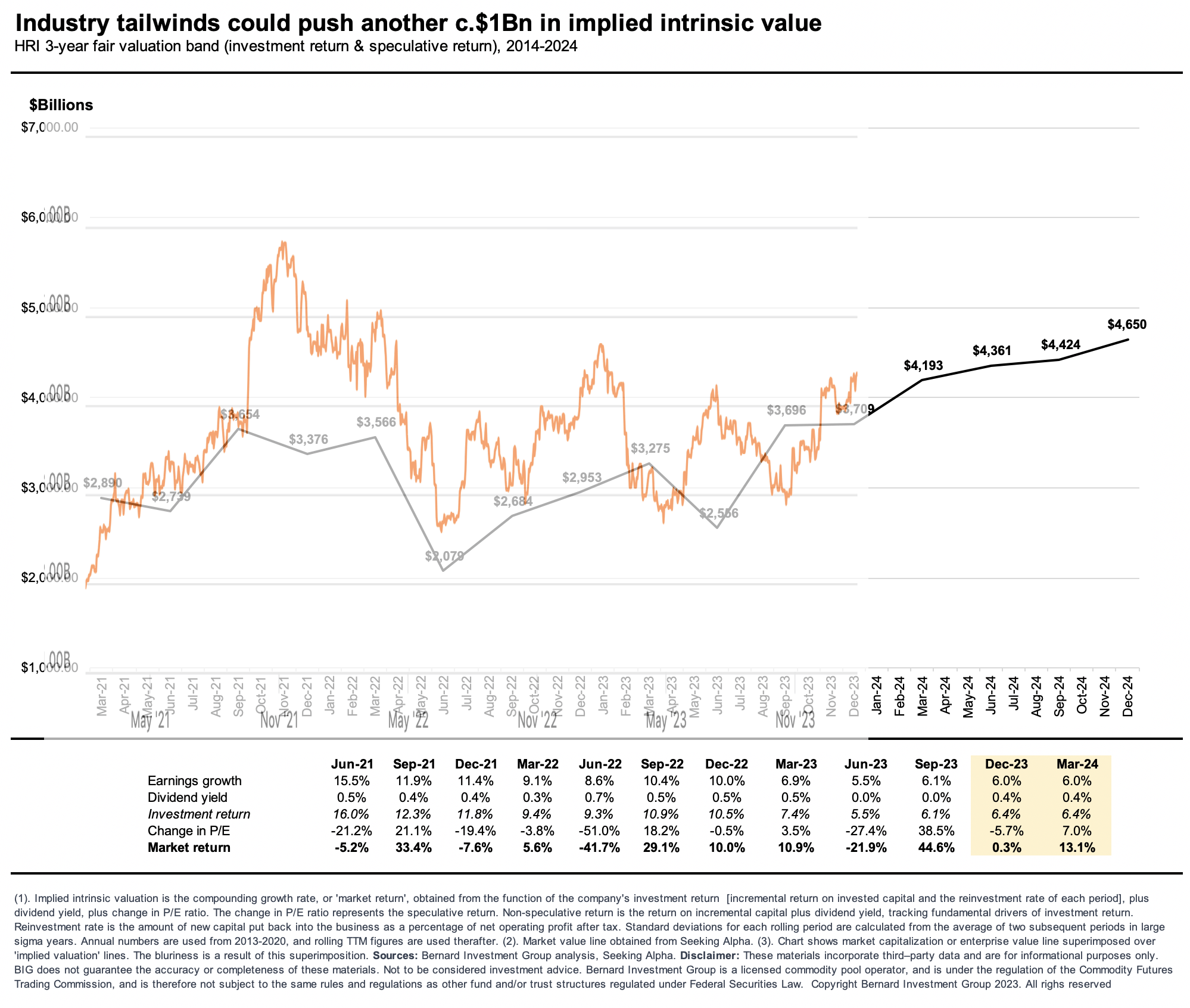

Financial worth is created by means of the returns generates on incremental investments, and the quantities it reinvests at these charges. A agency can compound its intrinsic worth at this perform (ROIC x reinvestment). However it’s not sufficient for the markets, which itself appears additionally to dividend yield and the speculative return, or the altering price-earnings a number of – how a lot traders are prepared to pay for $1 earnings. Mixed, these three issues for the markets return, all the overall shareholder return.

As seen in Determine 9, our mannequin has tracked the efficiency of HRI by compounding its implied intrinsic worth by its market return every rolling TTM interval. The info is proven within the desk beneath the graph. Ahead development assumptions name for five% – 6% earnings development over the approaching 12 months, with 1% dividend yield, together with 7% change within the implied P/E a number of, resulting in a 13% development in intrinsic worth.

This might place HRI at a market worth of $4.6Bn, in any other case $164/share or round 14x earnings if acknowledged by the market. Thus, paying 12.6x earnings implies the corporate is priced at truthful worth underneath our assumptions and subsequently is warranted as purchase by the very best estimation. We’re shopping for a superb stream of earnings that adjusts to 0.84x when factored for development.

Determine 9.

Dialogue abstract

After in depth evaluation of the funding info there may be plentiful help for allocating HRI to the fairness threat finances by our estimation. The corporate presents with sturdy economics and up to date worth actions which might be pushed by fundamentals, together with enticing beginning valuations of round 12.3x earnings.

The corporate’s development is engendered on comparatively little working capital necessities, with the majority of capital tied up in its rental tools, which produces a story of money flows. That is constructive in an asset-inflation setting.

This implies into might be allotted with nice effectivity to provide gross sales and earnings development. In our opinion, this positions the corporate effectively to proceed its development sample with out jeopardising the earnings attributable to its house owners, and/or it will possibly enhance earnings with out jeopardising its development sample. Internet-net charge purchase eyeing preliminary worth goal of $164/share.

The next dangers are related to the funding thesis and have to be understood earlier than progressing any additional as they stability the bullish outlook:(1). The projections for the industrials sector could not play out as we anticipated. This might have implications to our funding thesis and probably scale back the dimensions of the revenue pool for HRI.

(2). If the corporate doesn’t hit its projected earnings development charges this would scale back the scope for valuation enhance in our opinion. This can be a threat to the thesis.

(3). Consideration also needs to be given to the macroeconomic panorama. The inflation/charges axis nonetheless exists, regardless of latest constructive developments. The danger of rising actual charges may spill over into broad equities, thereby hurting the scope for HRI’s valuation to extend as effectively.

These dangers have to be acknowledged in full.