Sundry Photography

Investment summary

My recommendation for Hertz Global (NASDAQ:HTZ) is a sell rating. The main reason for my sell rating is the worry about additional charges incurred related to the remaining fleet of electric vehicles [EVs] sitting on HTZ balance sheet. While it is virtually impossible to accurately estimate the impact, I know from HTZ trading history that when it misses expectations, valuation takes a big hit. And I think these additional charges are likely to happen given that the prices of EVs are coming down.

Business Overview

HTZ offers car rental services to consumers across the globe under multiple brands, such as Hertz, Dollar Car Rental, Thrifty Car Rental, and Firefly Car Rental. While HTZ is a global company, most of its revenue comes from the US, representing ~79% of FY23 revenue and 63% of pre-tax income.

1Q24 results update

Released on April 25th, HTZ 1Q24 revenue came in at $2.08 billion, roughly in line with consensus estimates for $2.035 billion. However, the key highlight was the substantial miss in adj EBITDA that came in at -$567 million vs. consensus expectations for -$92 million. Consequently, adj EPS came in at -$1.28, which is also a lot worse than consensus expectation of -$0.45. Weakness was seen in both Americas and International. Revenue for the Americas segment saw ~$1.74 billion, led by higher rental days but softer pricing. America’s EBITDA represented the bulk of the group’s EBITDA negative performance, coming in at -$488 million. For the international segment, revenue saw $341 million (in line with consensus), with EBITDA coming in at -$27 million.

Visible earnings headwind ahead

I believe there is a very visible headwind in the near term that significantly dampens the EBITDA outlook. As noted above, EBITDA missed consensus expectations by a huge margin, and the culprit was the significant increase in vehicle depreciation (increased by $588 million), which translates to an increase of $339 (per unit basis) vs. 1Q23. The increase was driven by three key reasons. The first two reasons are understandable: (1) deterioration in estimated forward residual values at the expected time of disposal (probably hard to estimate with the price index falling); (2) disposition losses on ICE vehicles compared to gains in 1Q23 (this is a comp effect, so I think it is not a big problem). The third reason is the worrisome one: write-downs on the carrying value of EVs (electric vehicles) classified as held for sale. For comparative purposes, ~33% of the increase ($195 million) was related to EVs held for sale, and I expect more EV-related charges to incur in the coming quarters.

Recall that HTZ bought a lot of EVs in their EV strategy. So far, HTZ has already sold 30k EVs; the first batch of 20k EVs resulted in $81 million, and the second batch of 10k EVs resulted in a $114 million charge. Specifically, 10,000 vehicles have been sold out of the initial batch of 20,000, and the remaining 10,000 have had their carrying value reduced to their fair market value after deducting the expected cost to sell these vehicles. That led to a $41 million charge from the sold vehicles and a $40 million charge from the write-down for the rest. In the second batch of 10,000 vehicles, those were marked as being available for purchase when the decision was made, and they were later written down to their fair value minus the cost to sell them.

Collectively, this $195 million charge, along with the previous charge of $245 million (for the EV sales plan), summed up to a total of $440 million of charges booked in 4Q23 and 1Q24. I believe this strongly reflects the plummeting value of new and used Tesla EVs in the marketplace. With Tesla (TSLA) announcing further price cuts across the world, I believe the holding value of HTZ’s remaining 30k EVs is going to continue to deteriorate. Hence, I believe there is a risk of another write-down from the remaining 30k of EVs and also incurring losses when the vehicles are sold.

Top line outlook seems positive

The good news is that HTZ revenue per day [RPD] outlook is rather positive. While worldwide RPD fell 6% in 1Q24 compared to 1Q23, the decline in RPD has been narrowing, going from 10% in January to 3% in March, and this trend has continued into April. HTZ closure of 125 underperforming locations during the quarter should also enable it to reallocate fleets to areas that have better utilization. Longer term, management believes they can improve RPD into the low $60s by elevating customer experience (something that is hard for investors to verify). Therefore, until investors see more solid results, I think the market will remain neutral on how this will impact HTZ performance.

Valuation

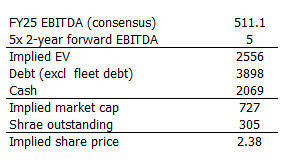

In the near term, I believe HTZ share price is going to be heavily impacted by management comments around the potential charges from the remaining 30k EVs. I am negative about this situation, but I believe it is virtually impossible to accurately model the potential charges. The way I would work around this situation to derive a value is by looking at HTZ historical forward EBITDA multiples. Since it emerged from bankruptcy, HTZ has typically traded within a tight valuation range of 5x to 7.8x two-year forward EBITDA multiple (I used 2 years because FY24 is expected to see negative EBITDA). If HTZ were to incur a large charge for the remaining 30k EV, at a higher magnitude than the $195 million since for the first 30k due to declining TSLA prices, HTZ is likely to report poor results again, and valuation could revert back to the low end of the range (this happened in 3Q23 when HTZ missed consensus EBITDA estimates by 10%). Assuming HTZ trades at 5x 2-year forward consensus EBITDA, this implies a share price a lot lower than today.

Redfox Capital Ideas

Risk

The same charges might not happen for the remaining 30k EVs, which means valuation is not going to see the same pressure I expected. Additionally, with RPD tracking positively into April, the topline could trend up further sequentially, driving EBITDA growth as increased utilization of previously non-performing fleets has a high incremental margin.

Conclusion

My view for HTZ is a sell rating due to the significant earnings headwind from potential write-downs on their remaining EVs. While HTZ’s revenue per day outlook seems positive, the uncertainty surrounding additional EV charges makes it difficult to accurately predict future earnings. The declining prices of EVs suggests further write-downs are likely, potentially causing the stock price to fall back to its historical low valuation range.