metamorworks

Following the failure of a number of outstanding banks within the U.S. and the compelled rescue of Credit score Suisse within the first quarter, monetary sectors remained largely resilient in 2023. This upheaval, triggered by issues round banks’ unrealized losses, was extra pronounced than anticipated within the U.S., prompting sizeable assist measures from the Federal Reserve to comprise dangers and restore depositor confidence in small-to-medium sized banks there. These adverse results had been largely contained to the U.S.

The tight financial coverage surroundings yielded a tightening of some monetary circumstances as anticipated, however the accompanying slowdown in lending and rise in non-performing loans (‘NPLS’) was comparatively delicate in most international locations. Current tendencies level to more practical tightening of banking circumstances in 2024 because the lagged influence of upper rates of interest, the rapidly waning advantages of COVID-19 pandemic-related assist measures, and slowing financial development weigh on debt servicing capability. The similar elements that supported stability in 2023 stay in power for 2024, though some tail dangers exist to our comparatively modest outlook for asset high quality deterioration in 2024.

1. Nominal credit score development charges will stay resilient, though ghost deleveraging will proceed in most international locations, performing as a drag on development.

Lending will proceed to develop in nominal phrases in most areas pushed by still-high ranges of inflation, though in a extra contained trend than in 2022 and 2023. We’re forecasting that two-thirds of our lined economies will report decrease credit score development in 2024 in contrast with 2023 estimations owing to increased rates of interest and slowing financial exercise. It will lengthen “ghost deleveraging” in rising markets — a development noticed over the previous decade the place credit score expands in nominal phrases, however beneath its long-term development as measured by the credit-to-GDP hole. This cautious stance from banks will weigh on financial development, constraining each company funding and family spending. Such credit score tightening already has affected a major proportion of nations in all areas, though it has been extra prevalent in economies in Jap Europe, Latin America, and Sub-Saharan Africa. We anticipate this development to proceed in 2024.

2. Credit score dangers will stay elevated, leading to a continued rise of NPL ratios.

Slowing worldwide financial development and extended increased rates of interest will weigh on debtors’ mortgage reimbursement capability, resulting in increased impairment in 2024, proven by rising NPL ratios. We forecast the vast majority of economies below our protection to register increased NPL ratios in 2024 than in 2023. This enhance is predicted to stay comparatively delicate. For households, a key asset high quality danger is that present mounted fee mortgage loans will have to be refinanced at far increased charges in lots of international locations. That is predominantly prone to happen in Europe. Actual property sector danger can also be a priority in Asia, significantly in China and Vietnam, the place giant financial institution publicity to the sector and falling actual property costs will put strain on banks’ asset high quality. For corporates, increased funding prices on each financial institution loans and capital markets financing will place elevated strain on their reimbursement capability, which is prone to set off the next stage of bankruptcies. For the US and different developed economies, the falling costs of economic actual property, decrease rental earnings, and better rates of interest stay a key tail danger to asset high quality.

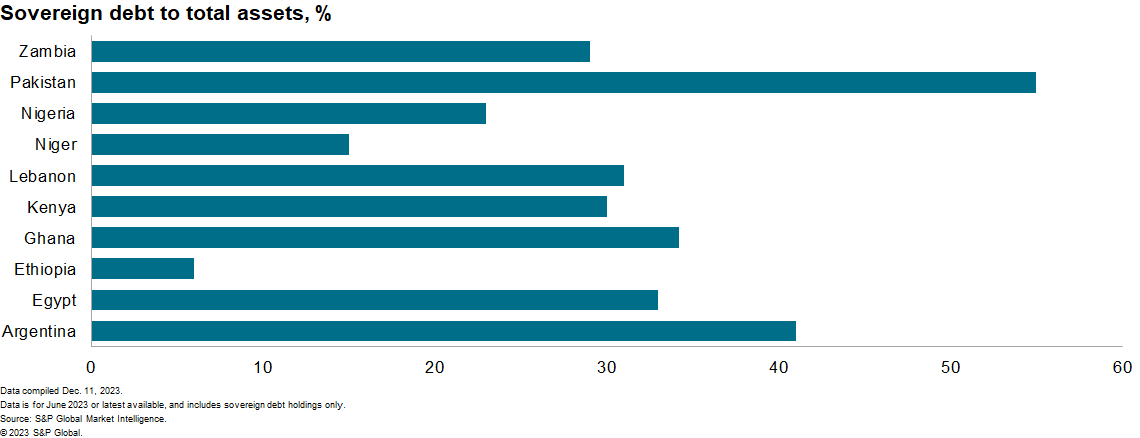

3. Sovereign debt issues will stay elevated in debt-stressed economies as home banks stay the first supply of funding for rising and frontier markets largely locked out of worldwide capital markets.

Given increased shares of public debt following the COVID-19 pandemic and restricted entry to worldwide capital, banks in rising markets will face elevated strain to lend to their home governments, growing bank-sovereign linkages. This will increase banking sector vulnerability to sovereign debt misery and arrears accumulation. This danger stays a robust concern for 2024, due to elevated sovereign debt unsustainability in a number of rising market international locations. Between 2020 and 2023, Zambia, Chad, Lebanon, Ghana, and Sri Lanka defaulted on their exterior debt. In January 2023, Ghana notably concluded a home debt restructuring (DDEP) that considerably impacted banks’ profitability and capital ratios given banks’ giant holdings of sovereign debt.

4. International forex shortages will stay pronounced in some jurisdictions.

International forex (‘FX’) shortages are prone to be extra pronounced in 2024 in particular jurisdictions — together with Lebanon, Egypt, Tunisia, Algeria, and lots of international locations in Sub-Saharan Africa (‘SSA’) — reflecting increased debt service prices in rising and growing international locations, weakening native alternate charges towards main buying and selling currencies, and insufficient international reserves. Larger rates of interest and capital flight from rising economies may also negatively influence the price and availability of foreign-currency funding for banks. This might trigger difficulties for banks to roll over foreign-currency debt and create international alternate asset and legal responsibility mismatches that might have adversarial impacts on banks’ capital ratios and profitability. The continued international forex scarcity is prone to power central banks to mandate banks to institute withdrawal limits to protect their international forex holdings to fulfill FX-denominated obligations as they turn out to be due. Dangers to the banking sector are higher the place international forex denominated lending is a bigger share of the full and the place reliance on international funding is largest.

5. Capital preservation is gaining renewed focus for regulators given asset high quality issues.

Capital preservation has been a key space of focus for authorities in current months and we anticipate this to proceed in 2024. Though capital positions seem strong, regulators are involved about future asset high quality deterioration and are prone to take steps to bolster monetary soundness. The US is reportedly contemplating increased capital necessities for banks in 2024. We anticipate EU regulators to problem banks on mortgage loss provisioning practices following their identification of inconsistent anticipated credit score loss estimation practices in late 2023. Regulators are prone to retain heightened capital-based measures, such because the countercyclical capital buffer, even within the absence of credit score booms. Restrictions on dividend funds are also prone to be prolonged in some jurisdictions. Preventative borrower-based macroprudential measures, resembling imposing increased danger weightings for actual property loans, are prone to be thought-about by regulators looking for to deal with recognized systemic dangers and vulnerabilities pre-emptively.

6. Asset worth corrections stay a vulnerability, though eventual financial coverage loosening ought to cut back banks’ unrealized losses.

Following the failure of Silicon Valley Financial institution in March 2023, bond worth declines later within the yr (October 2023) renewed issues over expanded pending unrealized losses on banks’ holdings of debt. Unrealized losses on financial institution stability sheets outdoors the US didn’t generate monetary stress comparable with that within the US in early 2023. Nonetheless, they’ve had a pro-cyclical impact on financial coverage, curbing banks’ willingness to increase new credit score and inspiring tighter lending requirements whereas sources are tied up in debt securities valued at a loss. As financial coverage pivots in direction of an easing section of the financial cycle in 2024, bond worth restoration over the approaching 12 months ought to cut back these losses. This could most profit banks in Latin America, rising Europe, and different growing economies that raised coverage charges earlier and extra rapidly and have managed to decrease inflation sooner than in superior economies. Banks within the eurozone are prone to see unrealized losses persisting no less than till the second half of the yr given later forecasted financial coverage pivots. Even the place coverage charges are declining, implementation of plans to scale back central financial institution stability sheets after their speedy development through the pandemic will worsen the provision/demand stability in debt markets. Such coverage motion represents an efficient tightening motion and is prone to sluggish or delay bond worth restoration and the reversal of unrealized losses.

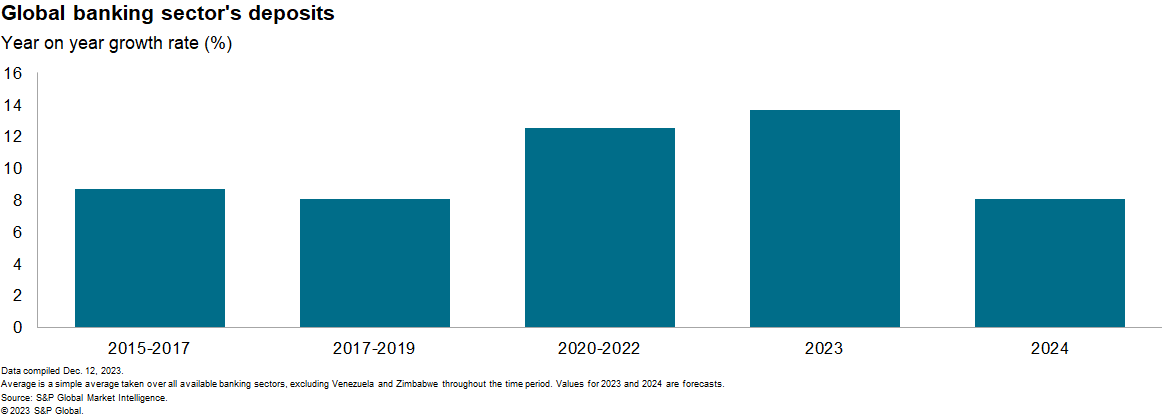

7. Slowing deposit development will enhance financial institution funding prices, hurting profitability.

Deposit development is forecast to sluggish in 2024 in two-thirds of the banking sectors below our protection. It will enhance banks’ funding prices as a mix of tighter monetary circumstances and weak financial efficiency will dampen non-financial sector stability sheet development. The speedy deposit development charges skilled by the pandemic, as households constructed up saving buffers, are unlikely to proceed. As a substitute, we challenge annual world (excluding Venezuela and Zimbabwe) deposit development to sluggish to single digits in 2024 versus about 13% between 2020 and 2022. Consequently, banks shall be compelled to supply increased deposit charges to stem deposit withdrawals and to mirror the probability of higher competitors for deposits from their home friends. The place banks search recourse to wholesale markets, prior financial coverage normalization would require banks to situation debt at traditionally increased ranges and in tighter markets, additional squeezing their liquidity and profitability.

8. Merger and acquisition (M&A) exercise is probably going as bigger financial institution teams search to increase in core markets and smaller banks exit given the difficult surroundings.

M&A exercise has largely stalled in lots of rising markets because the begin of the pandemic as heightened uncertainty within the world economic system lowered the urge for food for financial institution purchases. We anticipate market sentiment will change. Improved current profitability and monetary sector resilience ought to encourage bigger financial institution teams to renew cross-border enlargement, consolidating their market share in core markets. Smaller and weaker banks experiencing increased funding prices reflecting elevated competitors for deposits, with lagging technological capabilities and in some sectors increased taxes, shall be foremost prone to endure consolidation, notably in rising Europe and probably in Sub-Saharan Africa, the place many banking sectors have numerous small banks.

9. Industrial banks will stay below strain from fast-growing fintech corporations.

Excluding Nubank in Brazil and Tinkoff in Russia, fintech banks have achieved most of their development through deposit mobilization. They haven’t but considerably expanded into credit score disbursement, as their enterprise fashions are normally primarily based on holding short-term protected property relatively than lending. Most fintech corporations will proceed this strategy by 2024. We anticipate fintech development to proceed accelerating, significantly of their function as deposit collectors for retail clients and SMEs and as a cost channel. Over time, as fintech acquires a extra related function, we do anticipate them to start out conducting conventional lending, though that is unlikely to occur in most economies till no less than 2025. For the few international locations with extra strong improvement of the fintech sector and the place these operations are actually nearer to these of typical industrial banks, we anticipate regulators to tighten supervision. Growth of a transparent regulatory framework ought to help the most important fintech corporations to increase their industrial lending actions. Smaller establishments will face increased prices, growing strain to consolidate or merge into bigger banking teams (or exit the sector).

10. Additional developments with central financial institution digital currencies (CBDCs) is predicted.

Given sizeable ongoing funding into blockchain know-how by governments, banks, and different personal sector entities, it’s possible that important additional advances shall be made in 2024, each in direction of wider use of CBDCs and personal sector use of latest applied sciences. Consequently, banking sectors are more and more uncovered to being undercut in a number of conventional product areas (resembling international alternate, securities settlement, and cross-border funds) by lower-cost state initiatives or sizeable personal sector early movers providing cheaper and near-instant cross-border and home cost and settlement preparations. Progress is probably going in 2024, notably in markets like mainland China and India, with the latter having introduced plans to introduce a CBDC inside 2024. In most world banking techniques, an expanded authorities presence through CBDCs is extra possible solely in 2025 or past, given intensive pilot testing and the necessity for legislative initiatives previous to implementation.

Editor’s Be aware: The abstract bullets for this text had been chosen by Searching for Alpha editors.