RapidEye/E+ via Getty Images

Introduction

Superior Industries (NYSE:SUP), a leading manufacturer of aluminum wheels, operates within a highly competitive and mature industry. To navigate this challenging landscape, the company has strategically located production facilities in Mexico and Poland, benefiting from lower labor costs. However, profitability remains a concern due to a significant debt burden, dependence on a limited customer base, and low industry growth. Furthermore, the company doesn’t offer any investment opportunity in the short term or the long term, so in my opinion, it is a ‘Hold.’

Business Overview and Competitive Landscape

Superior Industries designs and manufactures aluminum wheels. It sells to OEMs in Europe and North America and the aftermarket in Europe. Superior produces its wheels in Mexico and Poland to take advantage of lower labor costs compared to the United States and Germany.

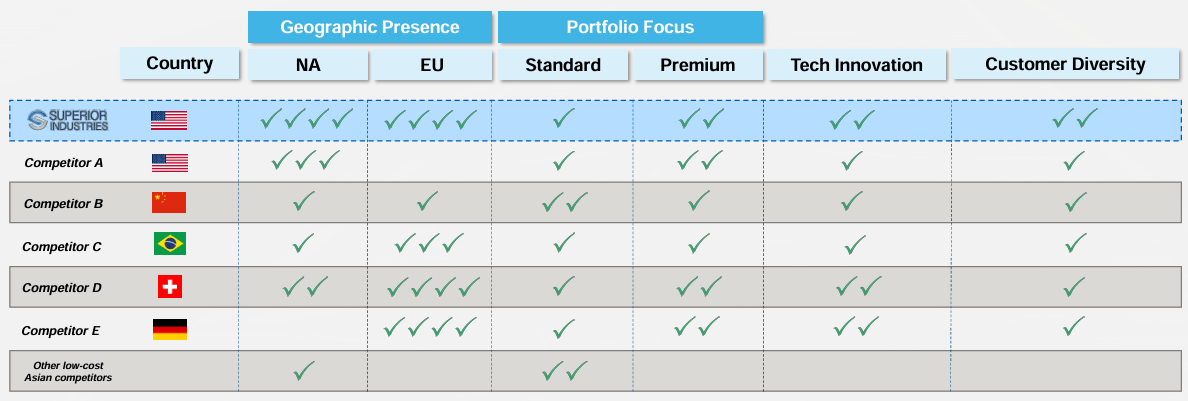

Lower labor costs are crucial as the industry is highly competitive (as noted in Superior’s low returns and slow industry growth), and the presence of low-cost Asian producers is a constant threat. In this sense, other competitors have expanded their operations in low-cost countries like Morocco (Hands Corporation), India (Enkei), and Mexico (Maxion).

Moreover, competition seems to be significantly similar to Superior Industries, as its investor presentation shows.

Investor Presentation

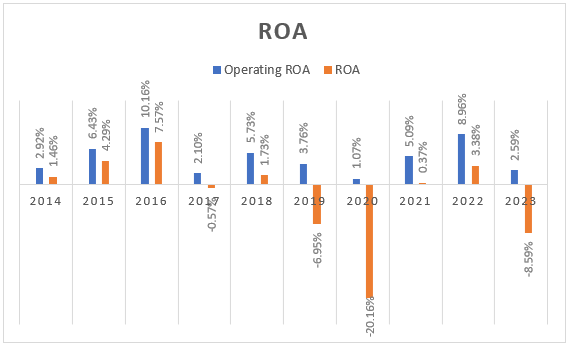

Thus, companies must keep innovating while keeping costs as low as possible to compete in a mature industry. I think this is a perfect combination for low returns over the long term, and Superior Industries’ historical performance demonstrates it.

10K Reports

*Operating ROA= (Operating Profit excluding Impairment / Assets Average)

Consequently, given that other companies can keep up with Superior Industries’ innovative pace and produce in low-cost countries, there is little room for outperforming competitors or improving margins, in my opinion.

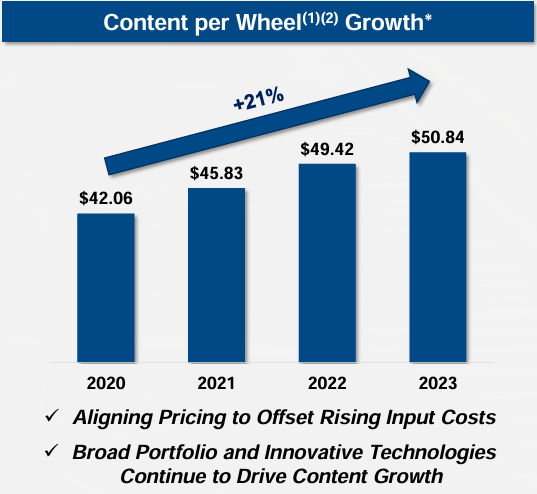

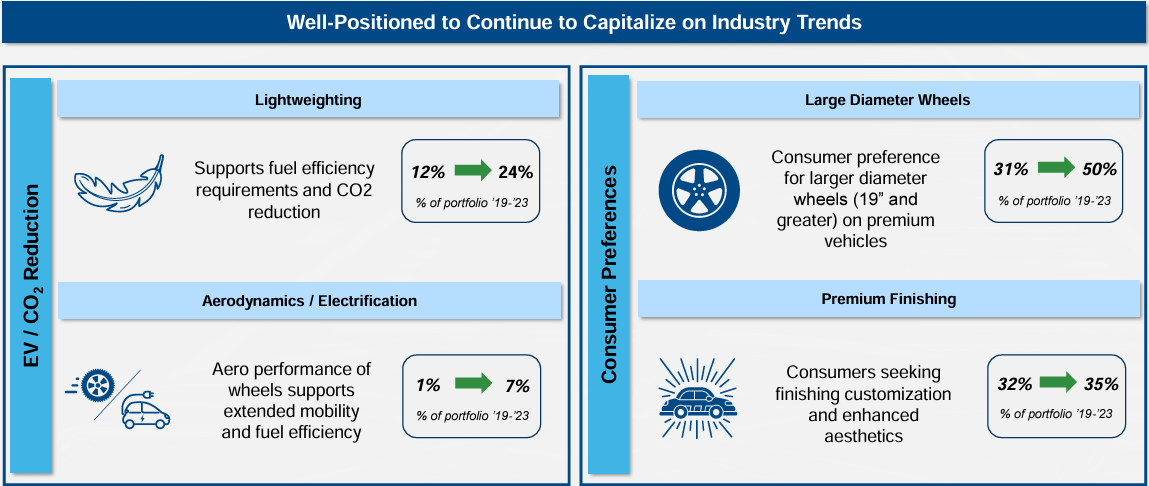

Nevertheless, I don’t think that all competitors are as innovative as Superior Industries (especially the smaller ones), as the company has been able to increase the price of its wheels by approximately 21% thanks to the introduction of successful products, such as lightweighting wheels, large diameter wheels, aerodynamic wheels, and premium finishing. These new wheels increased as a portion of Superior’s revenue in the four years.

Investor Presentation Investor Presentation

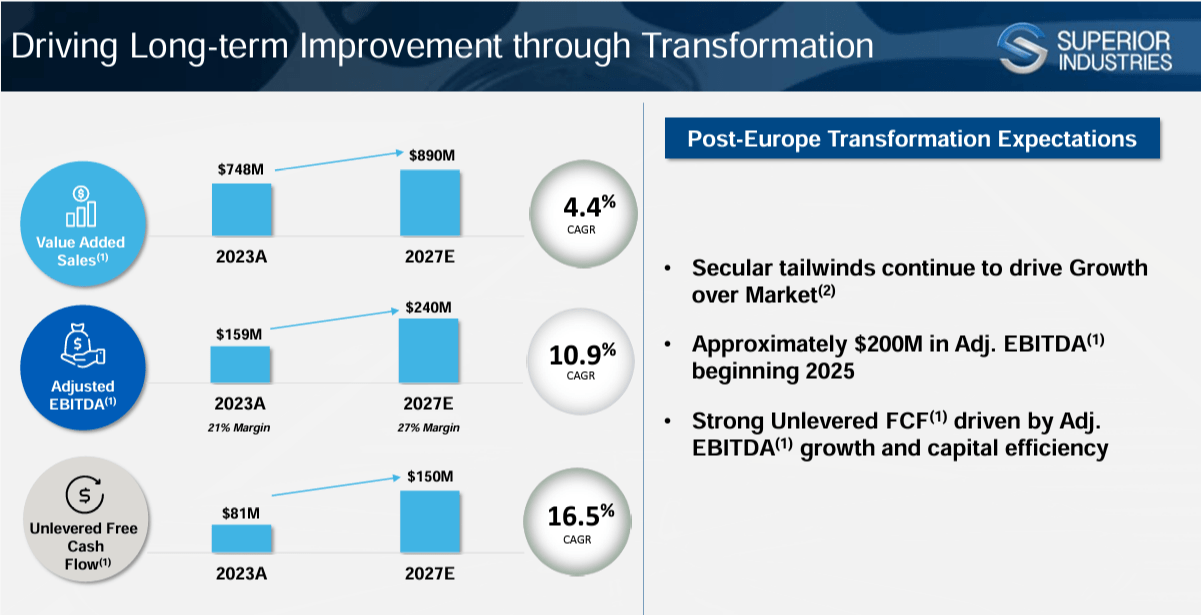

Finally, the company halted its operations in Germany in August 2023 so that it could concentrate its production in Poland to improve margins in Europe by 500 bps. Thus, the company will be able to lower its costs through better utilization of its Poland manufacturing facility, lower labor costs, and lower SG&A expenses. On this basis, the management expects to outperform the market by 4.1%, as the market is expected to grow only 0.3% annually, while management believes Superior Industries can grow approximately by 4.4% annually. Meanwhile, unlevered free cash flow is estimated to grow at a CAGR of 16.5% thanks to increasing revenue, lower capital expenditures, and margin expansions.

Investor Presentation

Bad Acquisition and Worrisome Debt

In 2017, Superior Industries acquired Uniwheels AG, the third-largest European aluminum wheel provider at the time of the acquisition. The acquisition cost around $715 million, recognizing a goodwill of $286 million. The benefits behind the acquisition were more diversified revenue (crucial as Superior depended on GM and Ford for 68% of its sales in 2017), possible synergies of $15 million, a larger scale, and technology sharing.

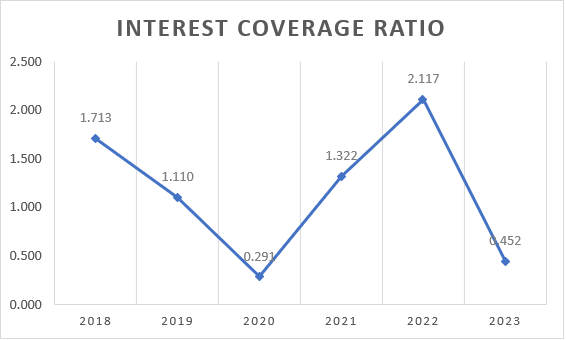

Nevertheless, the transaction resulted in a costly acquisition and sequentially impairment expenses in 2019 and 2020. Moreover, Superior Industries has a long-term debt of $605 million as of March 2024 due to the acquisition. In this regard, $375.6 million of debt comes from the Loan Term Facility, which has a variable interest rate. In 1Q24, the weighted average interest rate of the Facility was 13.3%, which is substantially higher than the 2025 Senior Notes interest rate of 6%. In this sense, the company has to pay back or rollover $238 million from these Notes in 2025; the company currently has $191 million in cash, so I don’t think the company won’t meet its obligations; nonetheless, its financial position is vulnerable with interest coverage ratio (excluding deconsolidation losses and impairments) of 0.452 in 2023.

10K Reports

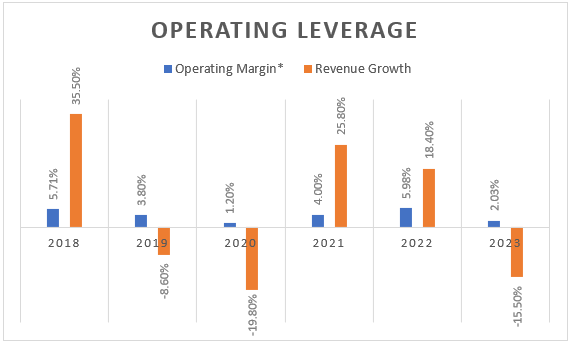

Furthermore, as noted in the graph below, the company relies on operating leverage to be profitable. When revenue falls, the operating margin shrinks significantly more than the change in sales and vice versa. This risk is significant in an uncertain macroeconomic environment with higher interest rates. If sales decrease, the operating margin will fall significantly more, affecting the company’s capacity to face its debt obligations in the following years.

10K Reports and QuickFS

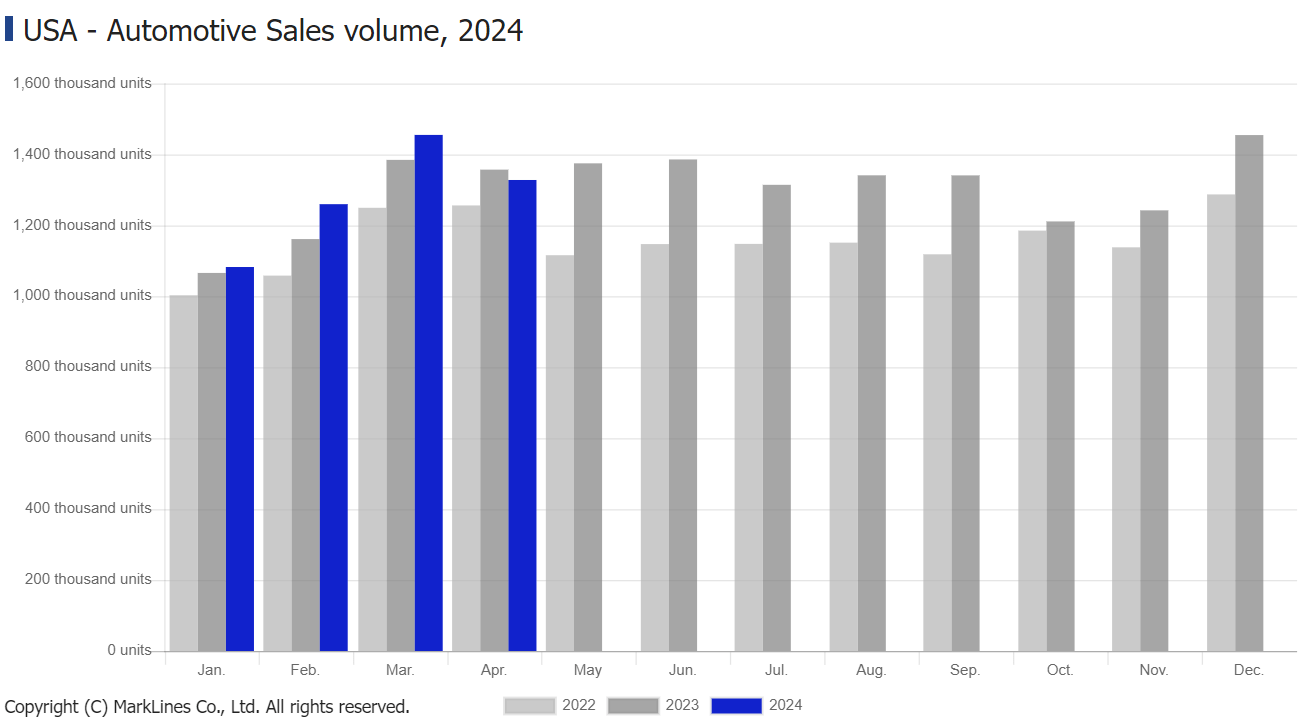

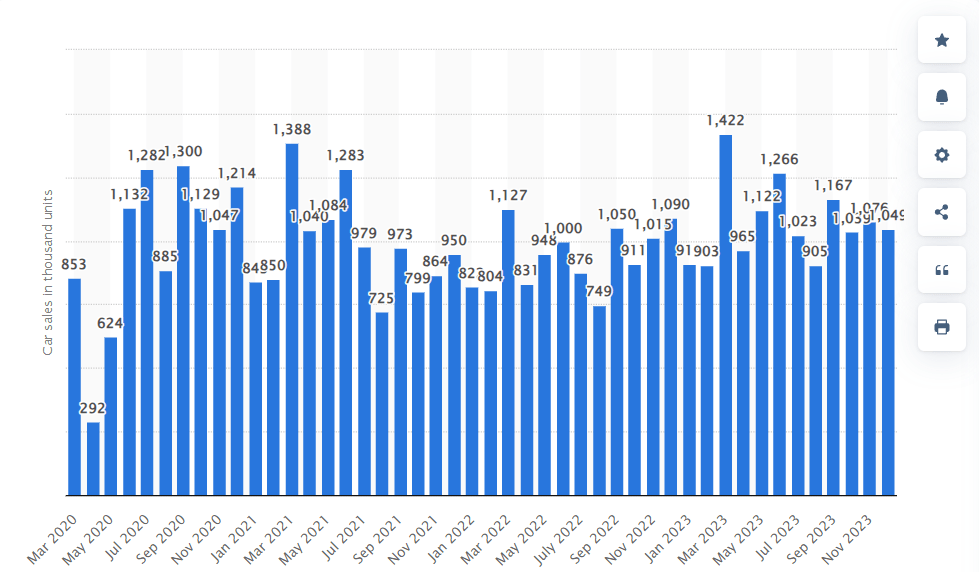

Nevertheless, the number of passenger cars sold in the US continues to rise, and there is a similar upward trend in Europe. Therefore, there is no sign that the market is decreasing yet.

MarkLines Statista

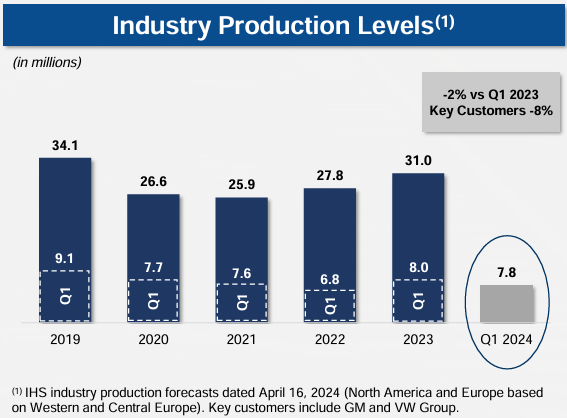

In this sense, management expects flat revenue growth in 2024, mainly due to the restructuring of European operations, which has already decreased its sales by 4% in 1Q24 and to a slightly weak first quarter in the industry compared to 2023.

Investor Presentation

In addition, Superior Industries expects to generate between $110 to $130 million in unlevered free cash flow with reduced capital expenditure of $50 million thanks to the deconsolidation of the Germany facility. Expecting similar interest expenses in 2024, the company will use approximately half of its unlevered free cash flow to pay interest on debt, while the other half will be available to pay back the debt.

Paying back the debt is critical as the company can barely meet its interest expenses, and it’s already paying over 13% of interest rates, while the Notes have an interest rate of 6%. Therefore, debt rollover will carry a higher interest rate, making it unsustainable for Superior Industries. Another debt payment solution is leasing back agreements for its manufacturing facilities, allowing the company to refinance its debt with a lower interest rate than other forms of debt like senior bonds.

Additionally, the company has issued redeemable and convertible preferred stocks, which bear a dividend yield of 9% that can be paid in cash or in kind, increasing the dilutive effects for common shareholders.

Risks

Competition

Superior Industries’ return on assets has been low in the last ten years and very volatile due to operating leverage, impairment losses, and tough competition. Moreover, the market is mature and has very low expected growth; thus, companies in this industry compete fiercely on price and innovation, forcing companies to migrate to low-labor-cost countries to remain competitive. Owing to its low returns, it’s clear that Superior Industries lacks a significant competitive advantage that sets it apart.

Debt

Even if the company won’t default on its 2025 debt, it can barely meet its interest expenses with its EBIT, raising concerns about its solvency. As a result, the company is paying a high-interest rate on its variable-interest debt. If the company doesn’t decrease its debt burden, it may threaten its existence as a going concern.

Cyclicality

The Superior Industries market depends on the automotive industry, which tends to be susceptible to the business cycle. This, alongside a reliance on operating leverage, makes profits highly volatile in the following years, especially in a high-interest environment.

Customer Concentration

After the acquisition of Uniwheels, the company could diversify its revenue among a larger number of customers. For instance, before the acquisition, the top three customers accounted for 82% of sales (2016); after the acquisition, the top three customers accounted for 42% (2017). Nevertheless, in 2023, that percentage rose to 52% of total sales. Hence, the company still heavily relies on a few customers to generate most of its sales, leaving it in a vulnerable position in negotiations and susceptible to disruption in its customers’ operations.

Valuation

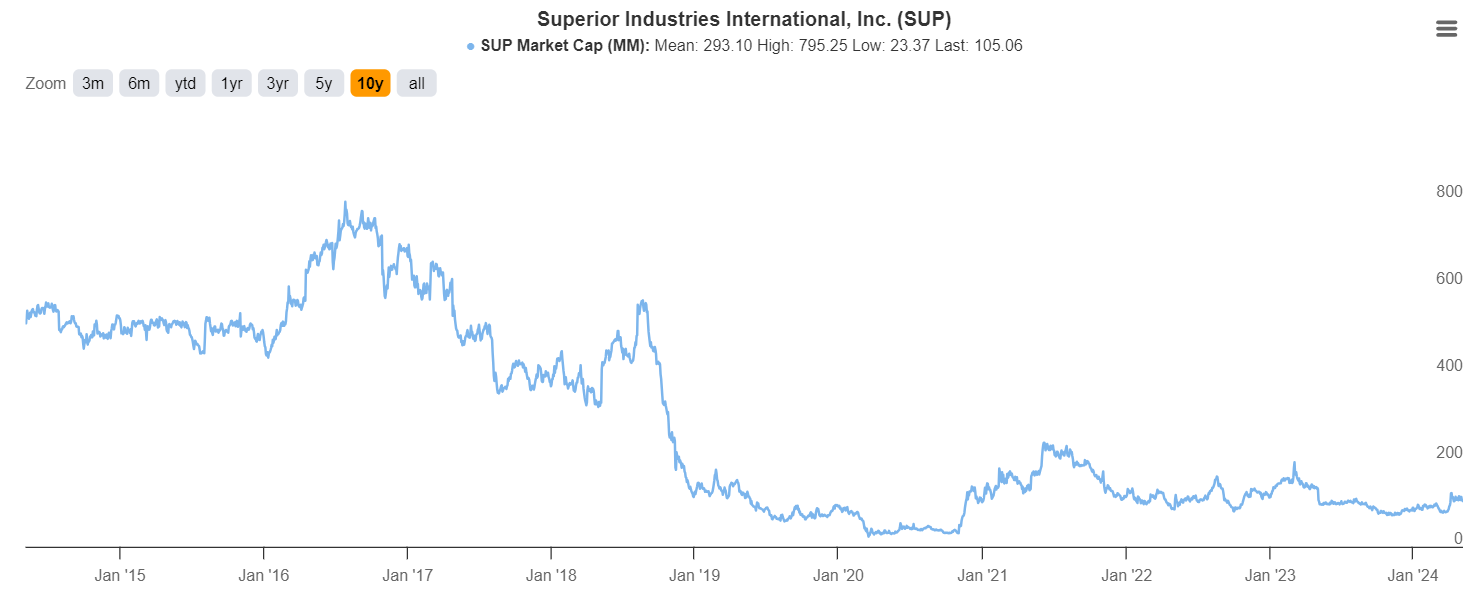

Since the acquisition in 2017, Superior’s market capitalization has decreased from $800 million to just $105 million, which tells us how devastating the acquisition was for the company.

TIKR

If we take the midpoint of management guidance, the company is currently trading at an FWD EV/Unlevered FCF of 6.47. Comparing this valuation with its historical TTM EV/Unlevered FCF in the last four years, the company seems relatively fair valued at its current multiples, as it has traded at a multiple range of 5 to 8.5. Therefore, it’s unlikely investors will earn any return from various expansions. Furthermore, the expected unlevered FCF will depend on whether management’s assumptions are met.

Nonetheless, if we compare Superior Industries with some of its public peers, Iochpe-Maxion, Enkei Wheels (India), and Hands Corporation, the company seems to be undervalued, as the industry median EV/Unlevered FCF is 10.31. For instance, Iochpe-Maxion has an EV/Unlevered FCF of 2.64, Enkei Wheels of 119.21 (due to large capital expenditures), and Hands Corporation of 10.31. Consequently, even if the company seems to be fairly valued compared to its historical multiples, it’s relatively undervalued if compared to its public peers. On this basis, Superior Industries may have some upside potential if the company reaches its industry EV/UFCF. Nonetheless, this metric has been volatile among the companies in the industry, so taking a less volatile multiple as P/S, we find that SUP is close to its peers as the company has a current P/S of 0.08, very similar to Maxion (0.12) and Hands Corporation (0.08).

Conclusion

From my perspective, I don’t see any investment opportunity in the short term, as the company will still suffer from high debt, a low revenue growth rate, and no multiple expansion opportunities. Furthermore, the low returns, as a product of fierce competition, lack of competitive advantages, and slow market growth, don’t make the company appealing to long-term investors. Consequently, I think the company is a ‘Hold.’