Artwork Wager

Funding thesis

Our present funding thesis is:

- Hilton is a unbelievable enterprise, with all of the hallmarks of a staple in buyers’ portfolios. It’s low threat and has spectacular margins, with a robust runway for additional progress via new developments. We count on macroeconomic situations to weigh on the corporate within the close to time period however the broader trajectory seems optimistic.

- With distributions being the first worth driver, valuation is crucial in our view. With charges elevated, the money expectations for buyers are naturally far increased, which at the moment costs Hilton out in our view. The inventory is probably going barely undervalued, though we might counsel awaiting a transparent macro image and superior yield.

Firm description

Hilton Lodges Company (NYSE:HLT) is a worldwide hospitality firm with a various portfolio of 18 world-class manufacturers encompassing greater than 7,400 properties and over 1,000,000 rooms in 119 nations. Headquartered in McLean, Virginia, Hilton is famend for its dedication to offering distinctive visitor experiences and progressive choices.

Hilton

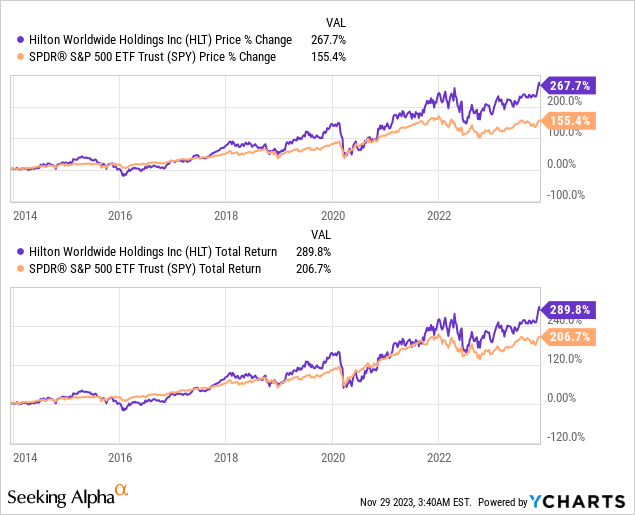

Share value

Hilton’s share value has been distinctive, returning over 250% to shareholders and noticeably outperforming the broader market. It is a reflection of its optimistic monetary efficiency and the event of its enterprise mannequin.

Monetary evaluation

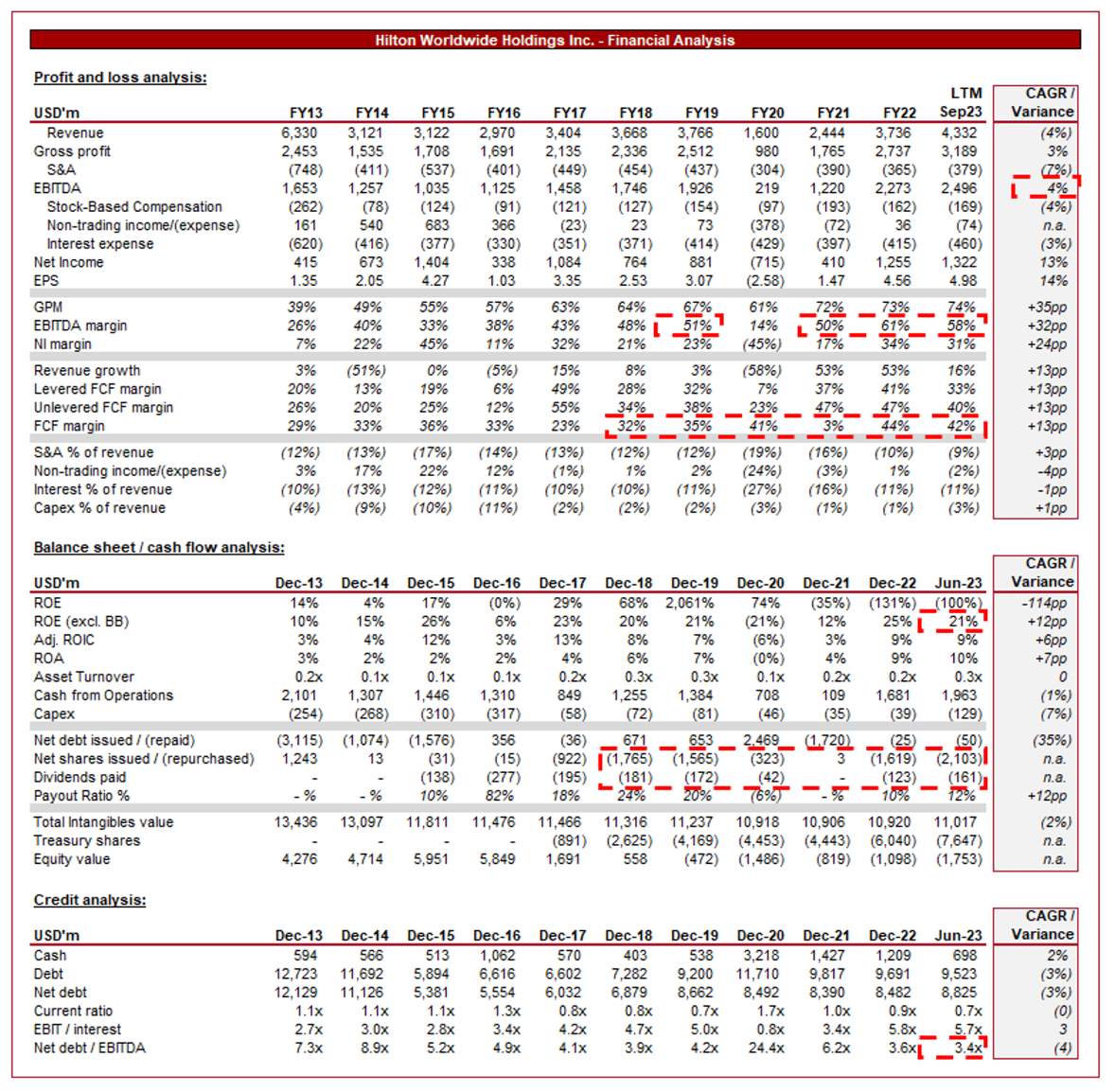

Hilton’s financials (Capital IQ)

Introduced above are Hilton’s monetary outcomes.

Income & Industrial Elements

Hilton’s income progress is deceiving, as the corporate has refranchised places, contributing to income and prices being exchanged for franchising charges. At the moment, ~80% of complete charges are franchising and licensing charges, with this income line rising at a CAGR of +10% since 2009.

Enterprise Mannequin

Hilton’s profitability progress (+14% EPS) has been propelled by a strategic shift in the direction of franchising. By franchising its manufacturers, Hilton can develop its world footprint quickly with out the necessity for important capital funding. Additional, this has de-risked the corporate, lowering its publicity to value inflation and demand cyclicality. Franchisees pay charges for utilizing Hilton’s model and profit from the corporate’s world reservation and distribution programs. That is the principal cause for its spectacular margin enchancment throughout the historic interval, as ~1% of RevPAR (“revenue per available room”) equates to ~1% of adj. EBITDA progress.

Along with franchising, Hilton enters into administration contracts. On this mannequin, Hilton manages inns on behalf of the property proprietor, incomes charges primarily based on the lodge’s efficiency. This enables Hilton to develop its model presence with out important possession stakes, once more permitting for de-risking.

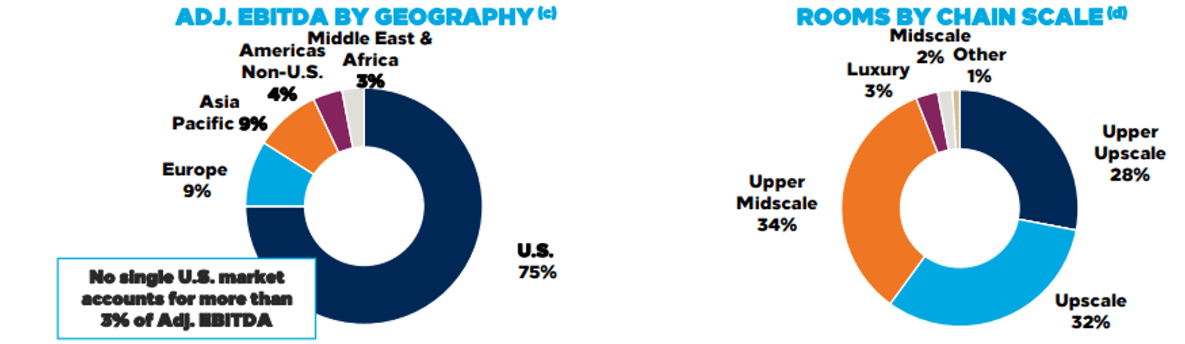

Hilton has a various portfolio of manufacturers catering to numerous market segments, from luxurious to budget-conscious vacationers. This diversification permits Hilton to seize a broad vary of shoppers and reply to totally different market calls for. This mentioned, the corporate is closely weighted towards the US and the upscale section (decrease with midscale, and better with higher upscale). This section is much less resilient than the luxurious section to cyclicality however has higher progress potential and runway for rooms as a result of bigger goal section.

Rooms (Hilton)

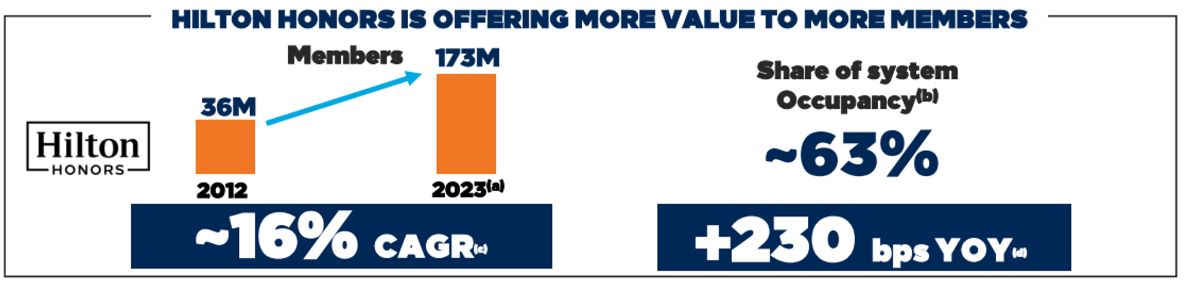

Hilton’s Hilton Honors loyalty program performs a vital function in buyer retention and attracting repeat enterprise,. This system provides members varied advantages, together with factors for stays, unique reductions, and entry to distinctive experiences. Loyalty packages profit from the community impact. If customers are simply capable of entry Hilton properties and have the scope and wish to take action repeatedly, it creates loyal clients. Conversely, if entry is restricted then psychologically, customers don’t see the worth proposition. Hilton advantages from its world presence and an unlimited vary of properties in varied classes.

Hilton

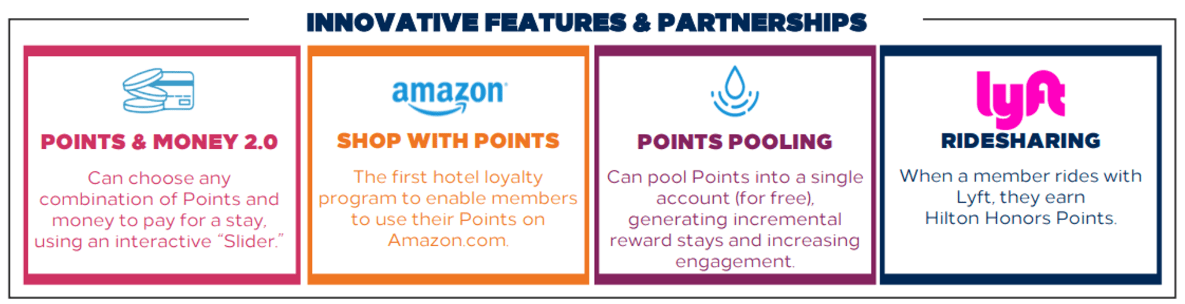

Hilton has invested in know-how and options to reinforce and differentiate the visitor expertise. Examples of resembling mirrored under, with the primary two choices specifically being genuinely helpful to its clients. This emphasis on incremental enhancements has the power to generate small however compounding model improvement.

Hilton

Hilton competes with the next friends (additionally represents alternate options for buyers):

- InterContinental Lodges Group (IHG): A worldwide participant with a deal with model differentiation and visitor loyalty.

- Accor (OTCPK:ACRFF): Recognized for its robust worldwide presence and various model choices.

- Marriott Worldwide (MAR): A significant competitor with a various portfolio of manufacturers, notably targeted on the higher-end section. We have now beforehand lined this inventory, score it a buy.

- Hyatt (H): Related profile to Marriott. We have now beforehand lined this inventory, score it a hold.

Margins

Margins (Capital IQ)

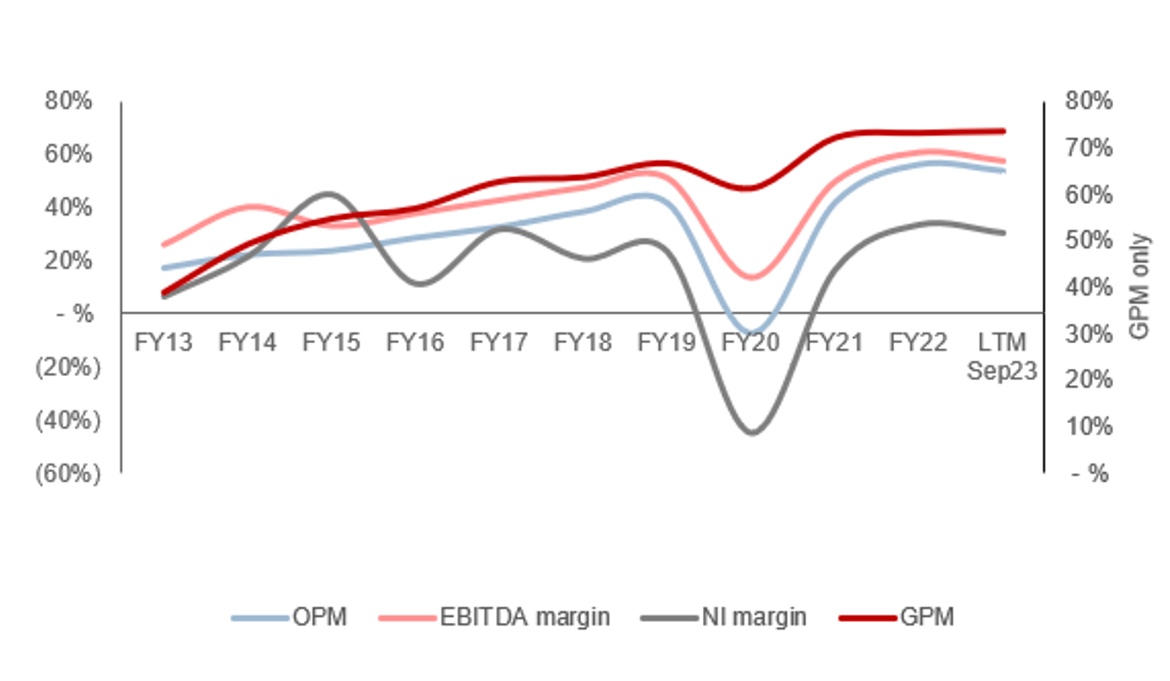

Hilton’s margins have meaningfully improved during the last decade and at the moment sits above its pre-pandemic degree, attributable to the shift to franchising. The corporate has externalized the price of operations whereas monetizing its model, contributing to an asset-light profitability profile.

With the corporate nonetheless ramping up most-pandemic, we see cheap scope for near-term margin appreciation, though this can be materially impacted by the present macroeconomic surroundings (mentioned intimately subsequent). If demand can stay strong, we imagine EBITDA-M can attain low the 60s, whereas a decline will possible go away the corporate at its present ranges. Inflationary situations have allowed Hilton to aggressively enhance margins, which might not have been potential in “normal” situations.

Quarterly outcomes

Hilton’s income progress continues to be robust, with top-line progress of +38.1%, +39.7%, +19.2%, and +14.0% in its final 4 quarters. Along with this, margins have barely softened, though stay materially above its pre-pandemic degree.

The robust progress is consultant of a continuation of its ramp-up post-pandemic, with journey progressively bettering following the top of lockdown restrictions and the vacation season throughout key Western geographies.

With progress falling to low single-digits in Q3’23, we suspect the enterprise is shortly approaching a normalized degree, notably as macroeconomic situations act as {a partially} offsetting issue. With elevated rates of interest and inflation, customers have skilled hovering dwelling prices, contributing to softening discretionary spending. This can possible proceed into most of FY24, because the outlook for a return to expansionary coverage stays unsure. We count on progress to say no to MSDs in FY24, though is extremely depending on the US’ financial efficiency.

Key takeaways from its most up-to-date quarter are:

- System-wide comparable RevPAR elevated by +6.8%, a powerful achievement in our view which displays the underlying demand for its companies at the moment. Importantly, customers are prepared to pay the elevated costs sufficiently to drive income ahead.

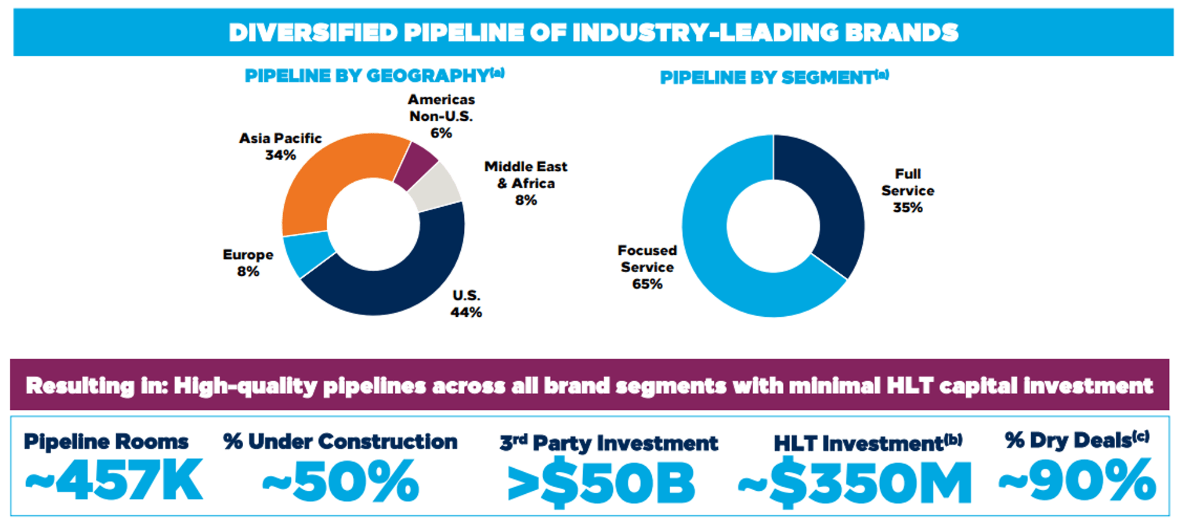

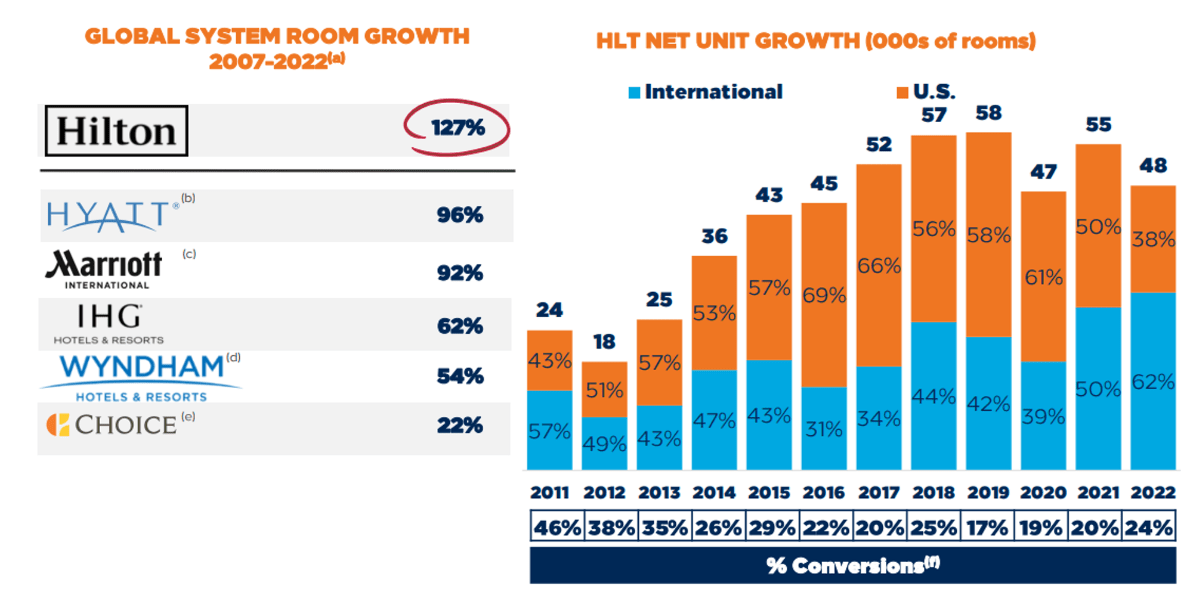

- 35.5k new rooms have been authorized for improvement, growing its pipeline to a file 473.3k, which is 10% of rooms in comparison with Sep22. It is a substantial pipeline relative to its current footprint and may permit the corporate to develop at MSD/HSDs within the coming years (Administration estimating 5-6% in FY24).

- Administration believes “an inflection point” has been reached, with a significant variety of new opinions anticipated going ahead. 14.3k extra rooms have been opened within the present quarter.

Pipeline (Hilton)

Stability sheet & Money Flows

Following the transition to a franchise/charge mannequin, Administration has been aggressive with capital allocation. Debt has been laddered up with profitability, at the moment sitting at 3.4x EBITDA. That is financially manageable attributable to its low-risk profitability profile, with curiosity protection of 5.7x.

Administration has utilized this money to distribute to shareholders, favoring share buybacks alongside small dividends. The money yield from that is spectacular, notably when contemplating the consistency of its profitability.

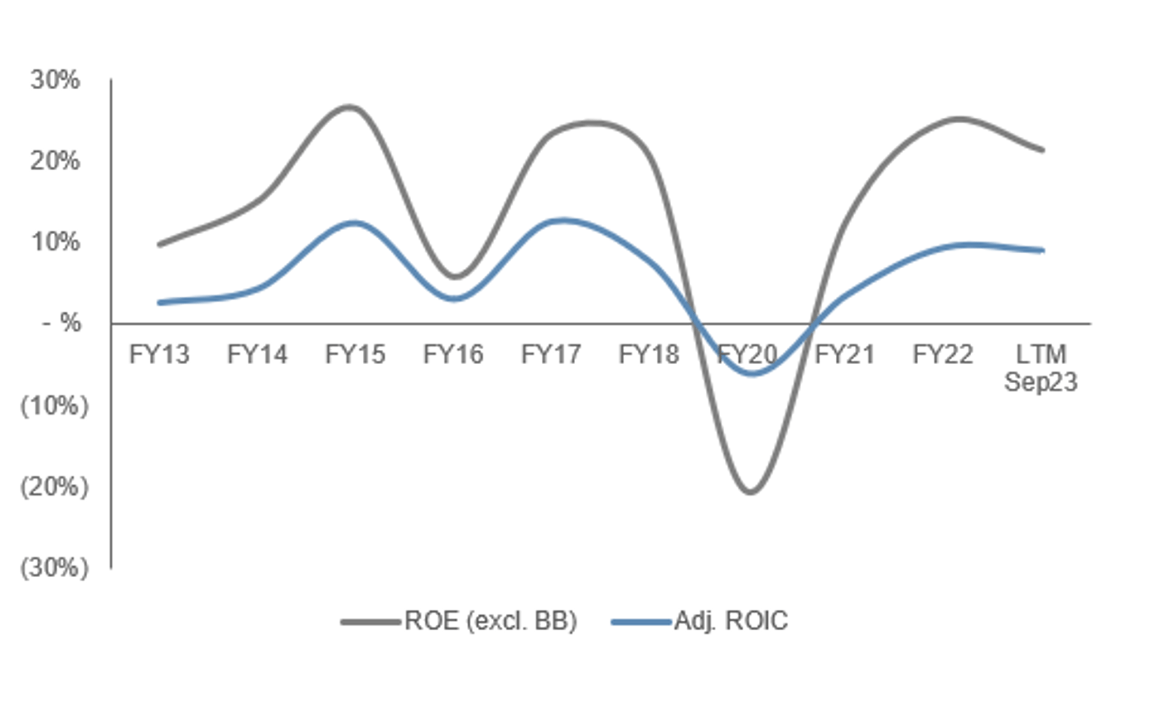

These symbolize an ROIC of ~9%, which we take into account to be a beautiful degree given the low cyclicality of the corporate.

Returns (Hilton)

Outlook

Outlook (Capital IQ)

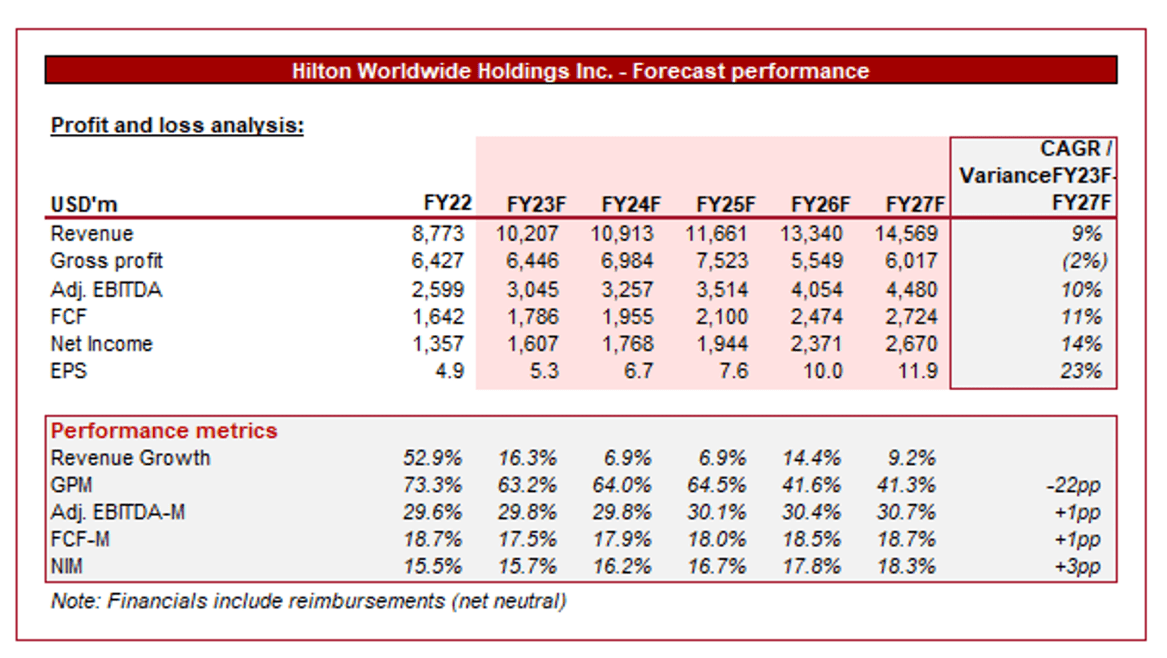

Introduced above is Wall Avenue’s consensus view on the approaching years.

Analysts are forecasting wholesome progress within the coming years, with a CAGR of +9% into FY27F. Along with this, margins are anticipated to sequentially enhance.

We take into account these assumptions to be cheap. With an aggressive pipeline of recent rooms, and future approvals, a robust progress trajectory is probably going. Additional, underpinning this can be financial improvement globally and rising incomes.

Trade evaluation

Lodges, Resorts and Cruise Traces Shares (In search of Alpha)

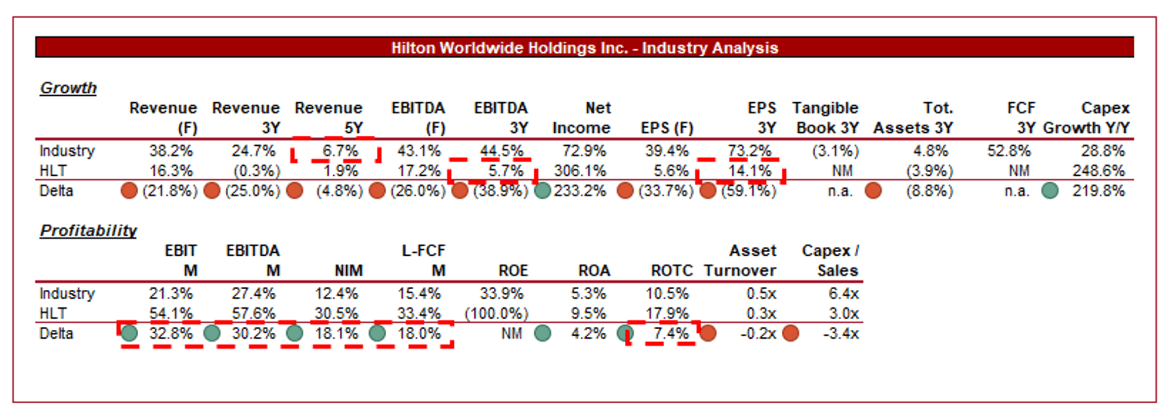

Introduced above is a comparability of Hilton’s progress and profitability to the common of its trade, as outlined by In search of Alpha (28 corporations).

Hilton performs exceptionally effectively relative to its discretionary friends. The peer group has been materially impacted from a progress perspective, contributing to messy monetary outcomes as many have bounced again from a decline in income. Importantly, its forecast income progress is superior to the 5Y income common of its friends, whereas its profitability progress has been robust and is primed to outperform. We count on this to be deliverable given the room progress achieved relative to its friends in recent times.

Hilton

Margins are the corporate’s key power, with its superior enterprise mannequin permitting for substantial returns. Solely three of its friends have a superior EBITDA-M, and just one has income in extra of $1b (Marriott).

Valuation

Valuation (Capital IQ)

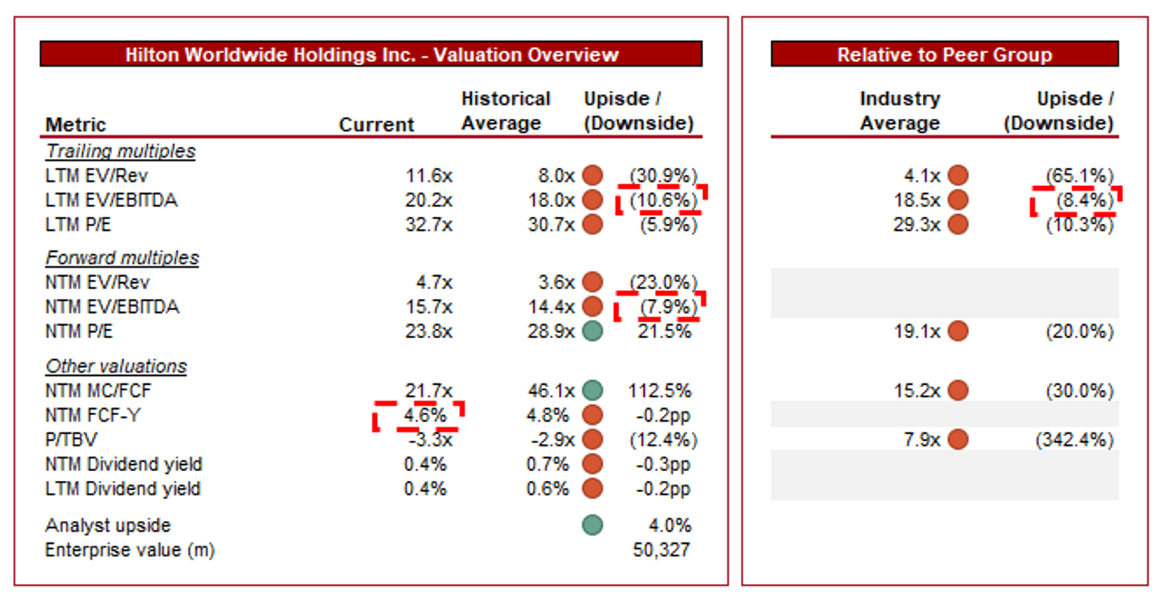

Hilton is at the moment buying and selling at 20x LTM EBITDA and 16x NTM EBITDA. It is a premium to its historic common.

Regardless of the numerous disruption in recent times and the macroeconomic outlook, we do imagine a premium is justifiable. The corporate is considerably extra worthwhile and fewer cyclical, positioned to be a money machine in perpetuity. At a ~10% low cost on an EBITDA foundation, we imagine there may be small upside with Hilton (Our truthful worth could be a premium of ~15-20%).

Additional, Hilton is buying and selling at a LTM EBITDA premium of ~9% and NTM P/E premium of ~20%. A premium is justifiable in our view, and noticeably so, owing to its spectacular margins and comparable progress on a normalized foundation. It’s positioned effectively to exceed its friends whereas broadly performing in step with the broader trade. We might counsel a premium of ~20-30%, which once more suggests upside of ~10%.

Based mostly on this, we imagine Hilton is barely undervalued however not materially so. We lean towards not sufficiently so for a purchase score, owing to its FCF yield of ~4.6%, which is under its historic common. We like to accumulate corporations at a money low cost ideally, except a noticeable acceleration is feasible (which isn’t the case right here). Additional, as this can be a money car in essentially the most simplistic sense, we might search a yield exceeding the RfR, which has noticeably elevated.

Key dangers with our thesis

The dangers to our present thesis are:

- [Upside] Financial downturn prevented and an early return to expansionary coverage (with out the re-emergence of inflation).

- [Downside] Financial downturns

- [Downside] Worth competitors if demand softens.

Ultimate ideas

Hilton is a high-quality enterprise following the transition to a franchise mannequin. It’s considerably de-risked from market elements, whereas boasting spectacular margins and a gentle progress trajectory. We count on its robust manufacturers, worldwide presence, spectacular pipeline, and incremental enhancements to its service to drive income progress of ~5-10%.

Given that is an funding motivated by money returns, entry valuation is crucial. At a FCF yield of ~5% following a share value growth in 2023, we don’t suppose the corporate is attractively priced any longer.