designer491

Horizon Know-how Finance (NASDAQ:HRZN) is a comparatively small-size BDC with a heavy give attention to VC-profile firm lending actions.

Based on HRZN’s investment policy, the next standards are utilized when contemplating new investments:

- Deal measurement as much as $50 million

- Deal time period based mostly on a 3-5 yr interval with a significant interest-only interval

- Precedence curiosity over fairness and unsecured debt

What comes instantly in thoughts when trying on the aforementioned investing standards is that plainly HRZN doesn’t comply with a conservative funding underwriting course of.

For instance, we don’t see a give attention to predictable money technology, non-cyclical industries, or every other side that may be related to prudent basic circumstances.

But, this shouldn’t be a serious shock both as the important thing goal section of HRZN lies in early-stage development firms, that are largely backed by VC gamers.

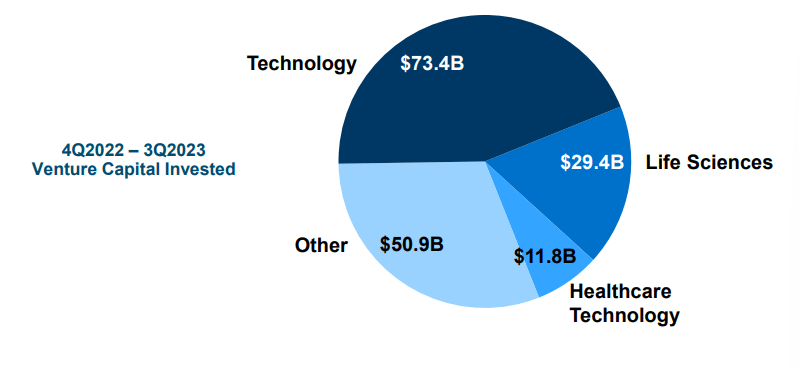

HRZN Investor Presentation

The present break up of HRZN’s portfolio illustrates this case fairly properly. Specifically, the lion’s share of HRZN’s AuM lies in inherently speculative sectors akin to life sciences, know-how, healthcare know-how, and many others. The speculative nature is additional boosted by the truth that the underlying firms are nonetheless within the early growth stage, oftentimes requiring money injections or loans to shut the gaps within the money technology till a brand new breakthrough is achieved.

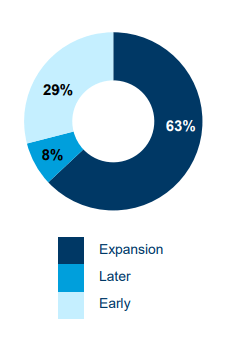

HRZN Investor Presentation

As of Q3, 2023, solely 8% of the companies that had obtained financing from HRZN have been categorised underneath “later stage” profile, the place usually you see some patterns of money movement neutrality.

Nearly one-third of the portfolio remains to be in a stage which requires important funding and the place there isn’t any certainty round whether or not the companies will handle to comprehend a profitable go-to-market technique. In different phrases, roughly one-third of HRZN’s portfolio is per definition speculative.

The remaining 63% of the publicity is constituted of companies which want capital to accommodate development. Right here it’s vital to notice that in most situations development is important to realize the advantages of economic system of scale in order that the fastened price base may very well be offset by a enough stage of top-line, thereby securing constructive underlying money flows. What this implies is that these firms embody a tiny margin of error, the place minor deviations from the projected development plan might result in an extra want for fairness injection or costlier debt financing to maintain the enterprise afloat till money movement (or margin) targets are achieved.

By way of exterior leverage, which is a vital a part of the enterprise for each BDC, HRZN carries a comparatively debt-saturated steadiness sheet. As of Q2, 2023, HRZN’s leverage profile landed at 1.2x, which may very well be categorised extra in the direction of the aggressive finish of the everyday BDC participant.

Because of the elevated threat exposures, HRZN has one of many highest debt portfolio yields within the {industry} (as per Rob Pomeroy, CEO, in the newest earnings call):

Our debt portfolio yield of 17.1% continues to validate structuring our investments with floating rates of interest in a rising rate of interest atmosphere, we once more generated one of many highest debt portfolio yields within the BDC {industry}.

Thesis

For my part, due to the extra riskiness that’s related to the character of companies to which HRZN supplies financing, this BDC just isn’t a lovely BDC to think about. The chance and reward ratio is off, the place the return potential doesn’t appear to justify the chance.

Let me clarify.

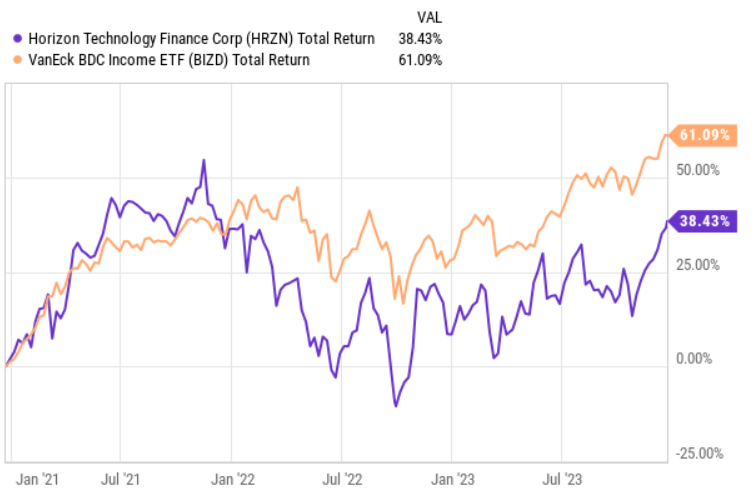

YCharts

First, HRZN has considerably lagged behind the general BDC house regardless that the market circumstances have been extraordinarily favorable for BDCs. So, even through the interval of robust industry-level tailwinds, the place extra “risk-on” BDCs ought to do higher relative to conservative ones, HRZN has underperformed.

Trying on the prevailing dividend yield of HRZN, we will additionally see that it’s slightly troublesome for the Fund to move by means of the ~17% yield to traders. Presently, HRZN yields simply 10%, which is even beneath the sector common (~11.5%).

A serious purpose for that is the subpar high quality of funding portfolio, the place, as elaborated above, a notable bias is shifted in the direction of slightly speculative and usually, money burning firms.

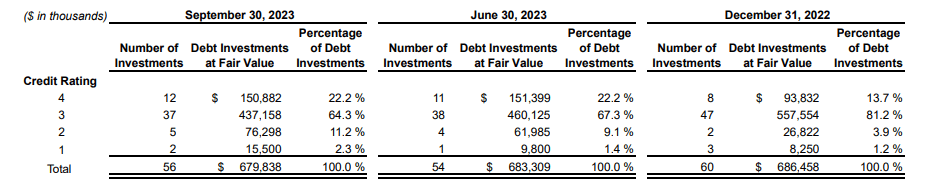

Third Quarter 2023 Monetary Outcomes

The desk above is an ideal instance of that.

HRZN’s portfolio high quality has been persistently deteriorating because the finish of 2022. As an example, whereas as of year-end 2022, HRZN had solely 5.1% of the investments labeled as in monetary difficulties with a terrific chance of capital impairment, now in Q3, 2023, the corresponding determine has elevated to 13.5%.

This isn’t solely materials within the charge of change phrases, but in addition within the context of the general portfolio.

Even Jerry Michaud, firm’s president, within the Q3, earnings name admitted the structural difficulties of HRZN investments:

VC exercise ranges stay underneath appreciable stress as VC investments in new portfolio firms made in 2021 and the primary half of 2022 are considerably overvalued within the present financial market. Consequently, the power of VC backed firms to lift new capital is difficult. Mixed with a just about closed IPO market and a muted M&A market, VC backed know-how and life science firms are discovering it more and more troublesome to lift a lot wanted capital to fund operations and development.

The underside line

All in all, HRZN is uncovered to some unfavourable threat elements past those, that are typical and already considerably excessive for traditional BDCs.

In HRZN’s case, there’s a large focus within the VC-profile firms, the place nearly all of them usually are not able to generate money flows in a sustainable method and thus depend on non-public exterior financing. Such a method works in a low rate of interest world and when the M&A and IPO markets are lively. Now, when the general financing circumstances have tightened, the prospects of many early-stage, cash-burning firms have considerably weakened, rendering their monetary prospects much more speculative.

Given the comparatively unattractive yield of HRZN (particularly within the context of the underlying threat stage) and a really unfavorable development within the portfolio high quality, I might keep away from investing in HRZN.