coldsnowstorm

By Nassira Abbas, deputy division chief, World Markets Monitoring and Evaluation Division, Financial and Capital Markets Division; and Corrado Macchiarelli, Economist (Mid-Profession Program), Cash and Capital Markets Division, IMF

Potential dwelling patrons face excessive costs and elevated borrowing prices, whereas owners chorus from itemizing their properties.

As international central banks raised rates of interest to tame inflation, home prices have cooled relative to the beginning of the mountaineering cycle. Nevertheless, regardless of the sensitivity of the residential market to greater coverage charges, costs are nonetheless above historic averages.

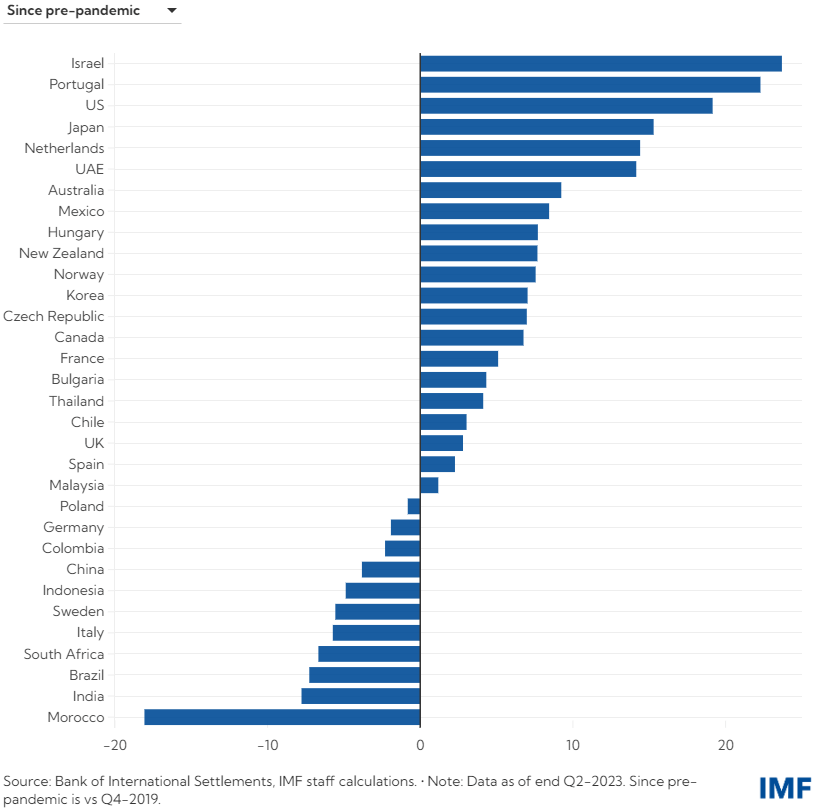

Dwelling costs in superior economies, together with most European Union international locations, in addition to Africa and the Center East are 10 p.c to 25 p.c greater than pre-pandemic ranges.

Rising rates of interest have handed swiftly to residential mortgage markets, impeding affordability for present and potential dwelling patrons.

Moreover, scarce dwelling provide is limiting purchases in some areas. In all, housing affordability is extra stretched amid still-elevated dwelling costs and better rates of interest.

Actuality test

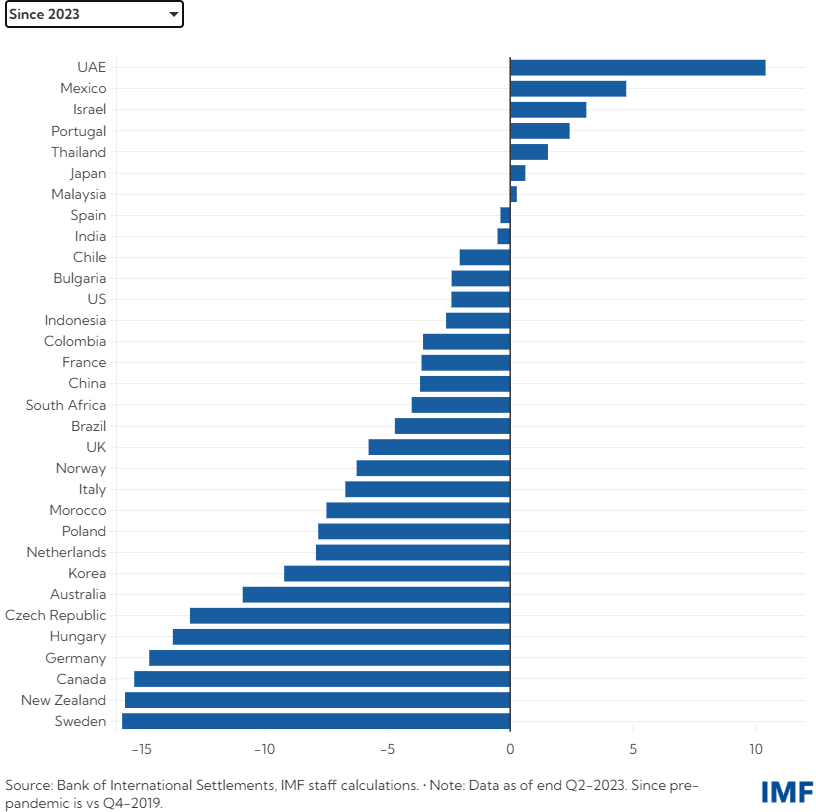

Dwelling costs are cooling, however a pointy downward correction stays unlikely in superior economies.

Change in actual home costs, p.c

Within the first half of 2023, mortgage charges in superior economies climbed by greater than 2 share factors in comparison with the earlier 12 months.

Throughout this era, international locations like Australia, Canada and New Zealand witnessed substantial declines in actual home costs, doubtless as a consequence of a excessive share of adjustable-rate mortgages and residential costs which have been stretched since earlier than the pandemic.

Comparatively, dwelling costs have fallen greater than 15 p.c in some superior economies, whereas the drop in rising economies was much less important. However, on internet, actual home costs might want to hold cooling from the 2021 and 2022 highs to achieve pre-pandemic ranges.

Larger borrowing prices are prone to see the biggest influence on family debt service ratios – a measure of debtors’ mortgage compensation skill – in international locations the place housing markets stay overvalued and common lifespans for mortgage loans are shorter, in line with our newest Global Financial Stability Report.

Approvals and compensation

As an illustration, for some superior economies equivalent to Norway, Sweden, Denmark, and the Netherlands with pre-existing double-digit households’ debt service ratios, debtors’ debt servicing prices may enhance by as much as 1.8 share factors given the surge in rates of interest.

That may have penalties for mortgage approvals and borrower compensation capabilities. However debtors are additionally much less indebted, and underwriting requirements have been strengthened for the reason that international monetary disaster, tempering the chance of a surge in mortgage defaults.

This may increasingly have additionally restricted cases of pressured promoting or foreclosures of houses, serving to to help dwelling costs.

In the USA, the Federal Reserve’s rate of interest hikes introduced huge adjustments to the mortgage mortgage market, with the typical charge on a 30-year fastened mortgage not too long ago reaching a two-decade excessive of seven.8 p.c.

For potential patrons, entry prices are placing homeownership additional out of attain, because the required down funds have additionally change into a prohibitive issue as a result of financial savings have shrunk for the reason that pandemic.

Current owners, deterred from buying new properties as a consequence of bigger month-to-month mortgage funds, keep put, inflicting a discount in provide of current houses.

This phenomenon, generally known as “lock-in” impact, is especially evident in the USA, the place long-tenured fixed-rate mortgages are hottest.

With common 30-year mortgage charges at the moment at 6.6 p.c, round 3 share factors above pandemic lows, mortgage originations stay 18 p.c beneath final 12 months’s ranges whereas refinancing purposes elevated 8.5 p.c over the 12 months as mortgage charges continued to ease.

Charges and refinancing

The 30-year fixed-rate mortgages accounted for 90 p.c of latest US dwelling loans on the finish of final 12 months, in line with ICE Mortgage Expertise.

Nearly two-fifths of all US mortgages have been originated in 2020 or 2021, ICE information present, because the low rates of interest through the pandemic allowed many People to refinance their dwelling loans.

Larger rates of interest additionally increase rental prices. Many individuals want to lease as a substitute of shopping for, given median home costs have been gradual to regulate.

On this context, the mix of upper charges and still-scarce housing provide creates a vicious circle that complicates central banks’ struggle in opposition to inflation.

US month-to-month dwelling costs continued to rise in October in contrast with a 12 months in the past, with shelter contributing to one-third of the change of client costs in November.

If the Fed begins charge cuts this 12 months, as policymakers and market members venture, mortgage charges will proceed to regulate, and pent-up housing demand could possibly be unleashed.

A sudden enhance, as the results of speedy charge cuts, may offset any enhancements in housing provide, inflicting costs to rebound.

Editor’s Word: The abstract bullets for this text have been chosen by Searching for Alpha editors.