Wirestock

SAS Institute Inc.

With inflation at or close to the best ranges in roughly 4 a long time, any rational investor needs to be asking “How well do U.S. Treasury yields forecast inflation?” Why? If Treasury yields are poor indicators of future inflation, then nobody can purchase bonds. On the opposite hand, if Treasury yields are fairly correct in predicting precise inflation, there isn’t any purpose to not purchase bonds as a part of a balanced fairness and fixed-income portfolio.

A associated query is one usually addressed by economists: how large is the “term premium” within the U.S. Treasury bond market? There are numerous forward-looking articles on that subject. It’s shocking that there are only a few evaluations of the historic outcomes evaluating rolling over short-term investments versus shopping for a fixed-rate bond. That calculation solutions each the inflation query and the time period premium query. If U.S. Treasury yields inaccurately mirror future inflation, then there needs to be many historic intervals the place the realized outcomes from rolling over short-term Treasury payments exceed the return that an investor holding the matched-maturity long-term bonds would have obtained.

On this be aware, we replace our semi-annual evaluation of realized and “in progress” time period premiums within the U.S. Treasury market by December 29, 2023. On each single buying and selling day since 1982, we evaluate the precise outcomes from rolling over 6-month Treasury payments in comparison with shopping for Treasury bonds with maturities of 1, 2, 3, 5, 7, 10, 20, and 30 years. As a result of rates of interest had been declining for a lot of this era however rising for a lot of the interval since February 2, 2022, we additionally report outcomes for investments which are “in progress” and whose ultimate end result remains to be unsure.

The magnitude of a “term premium” or danger premium in long-term U.S. Treasury yields is a serious focus of analysis by each teachers and economists within the Federal Reserve System. A recent paper by Canlin Li, Andrew Meldrum, and Marius Rodriguez summarizes two essential papers on this subject and evaluations their methodologies. Adrian, Crump, Mills and Moench (2014) summarize their time period premium findings as follows:

“The evolution of term premia has been of particular interest since the Federal Reserve began large-scale asset purchases. Over this time, short-term interest rates have been close to zero, and our estimates show that the term premium has been compressed and has at times even been negative.”

Estimates of the time period premium are a operate of the information used, the modeling method taken, and market expectations.

The main focus of this be aware is an easy one: the calculation of traditionally realized time period premiums and “in progress” time period premiums. From the angle of prudential regulation of economic establishments, Ramaswamy and Turner [2018] argue that rate of interest danger could be the set off for the subsequent monetary disaster, and the demise of Silicon Valley Financial institution on March 10, 2023, different U.S. banks confirms the accuracy of that forecast. The magnitude of the time period premium, each present and future, is a vital aspect in assessing the rate of interest danger of economic establishments.

A historic perspective on really realized time period premiums can be a probably essential contributor to market expectations, topic to the caveat acknowledged by Robert A. Jarrow, “History is just one draw from a Monte Carlo simulation.”[1]

We search to reply this query: “Which investment has provided the best total dollar return to investors, a U.S. Treasury bond maturing in X years or a money market fund that invests only in Treasury bills?” We deal with the reply to that query with respect to U.S. Treasury fixed-rate bonds with maturities of 1, 2, 3, 5, 7, 10, 20 and 30 years. We remind readers that what follows is an evaluation of historical past, not a forecast for the long run.

Methodology

We use the time collection of U.S. Treasury yields maintained by the U.S. Department of the Treasury and distributed by the Board of Governors of the Federal Reserve.[2] We assume that on every day for which knowledge is on the market, an investor invests $1000 within the U.S. Treasury bond and $1000 in 6-month Treasury payments. Each six months, the investor will obtain a coupon on the bond. We assume that money from the coupon cost is invested in 6-month Treasury payments and that this funding is rolled over in new 6-month Treasury payments till the underlying bond matures.[3] The funding within the “money fund” begins with an funding in 6-month Treasury payments and all money thrown off is reinvested in new 6-month Treasury payments till the underlying funding within the fixed-rate bond matures. Curiosity on the six-month payments is calculated on an precise/365-day foundation as a result of the U.S. Treasury knowledge collection for short-term charges is on an “investment” foundation.

The cost dates, 6-month invoice charges, and the worth of the “money fund” are given in a supplemental spreadsheet. The full greenback returns on 1, 2, 3, 5, 7, 10, 20, and 30-year Treasury bonds, each realized and “in progress,” are given in a second spreadsheet. Each spreadsheets can be found upon request from the creator.

Abstract Outcomes

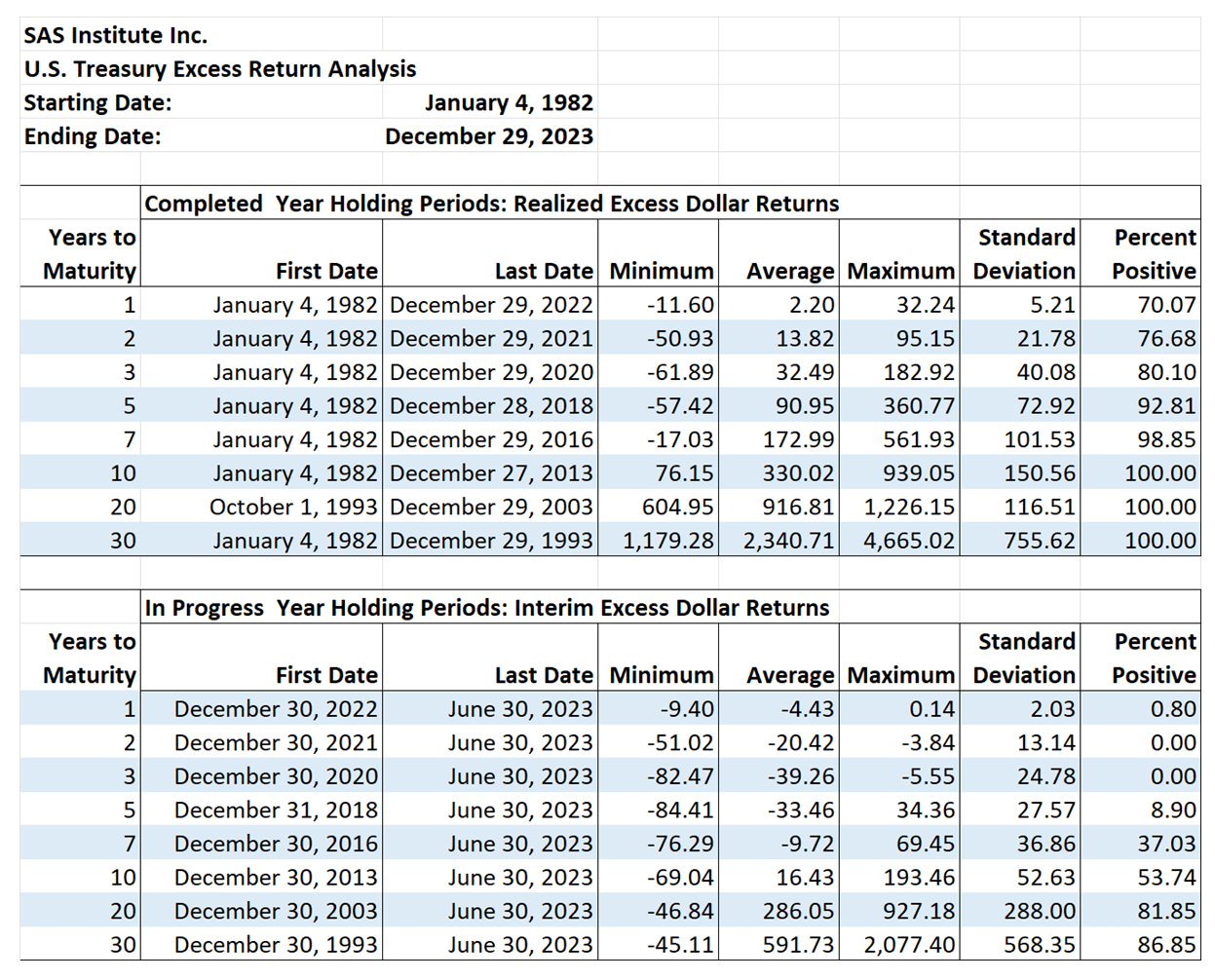

The outcomes of the time period premium evaluation are summarized within the following desk:

SAS Institute Inc.

The outcomes present that realized complete greenback extra returns have by no means been detrimental for maturities of 10, 20, and 30 years. This conclusion is unchanged because the prior replace by June 30, 2023. “Excess dollar return” is the ending greenback quantity of the “bond strategy” much less the ending greenback quantity of the “T-bill strategy.” For instance, on common, buyers shopping for a $1000 1-year fixed-rate bond earned $2.20 greater than buyers rolling over six-month Treasury payments. The utmost benefit was $32.24, and the worst end result was a loss: $-11.60.

Pending “in progress” extra returns mirror the sharpness of the current charge rise. On the shorter maturities, outcomes are dramatically completely different from the “in progress” outcomes of 18 months in the past. For 1-year and 2-year horizons, 0.80% and 0.00% of realized greenback extra returns have been optimistic. At three years, the outcomes are 80.10% (realized) and 0.00% (pending). At 5 years, the outcomes are 92.81% (realized) and eight.90% (pending). Even on the 7-year maturity, a minority of pending extra returns are optimistic: 37.03%. The statistics for different maturities are proven within the chart.

Graphical Evaluation Obtainable Upon Request from the Writer

Appendix A exhibits the evolution of complete greenback return (in purple) versus the 6-month T-bill cash fund complete greenback return (in blue) for accomplished 1, 2, 3, 5, 7, 10, 20 and 30-year phrases starting January 4, 1982. For many holding intervals, rates of interest have declined considerably over the funding intervals which have been accomplished. The graphs in Appendix A additionally embody the evolution of the preliminary six-month Treasury invoice yields (in gentle blue) and the related fixed-rate Treasury bond yields (in pink) on the origination dates.

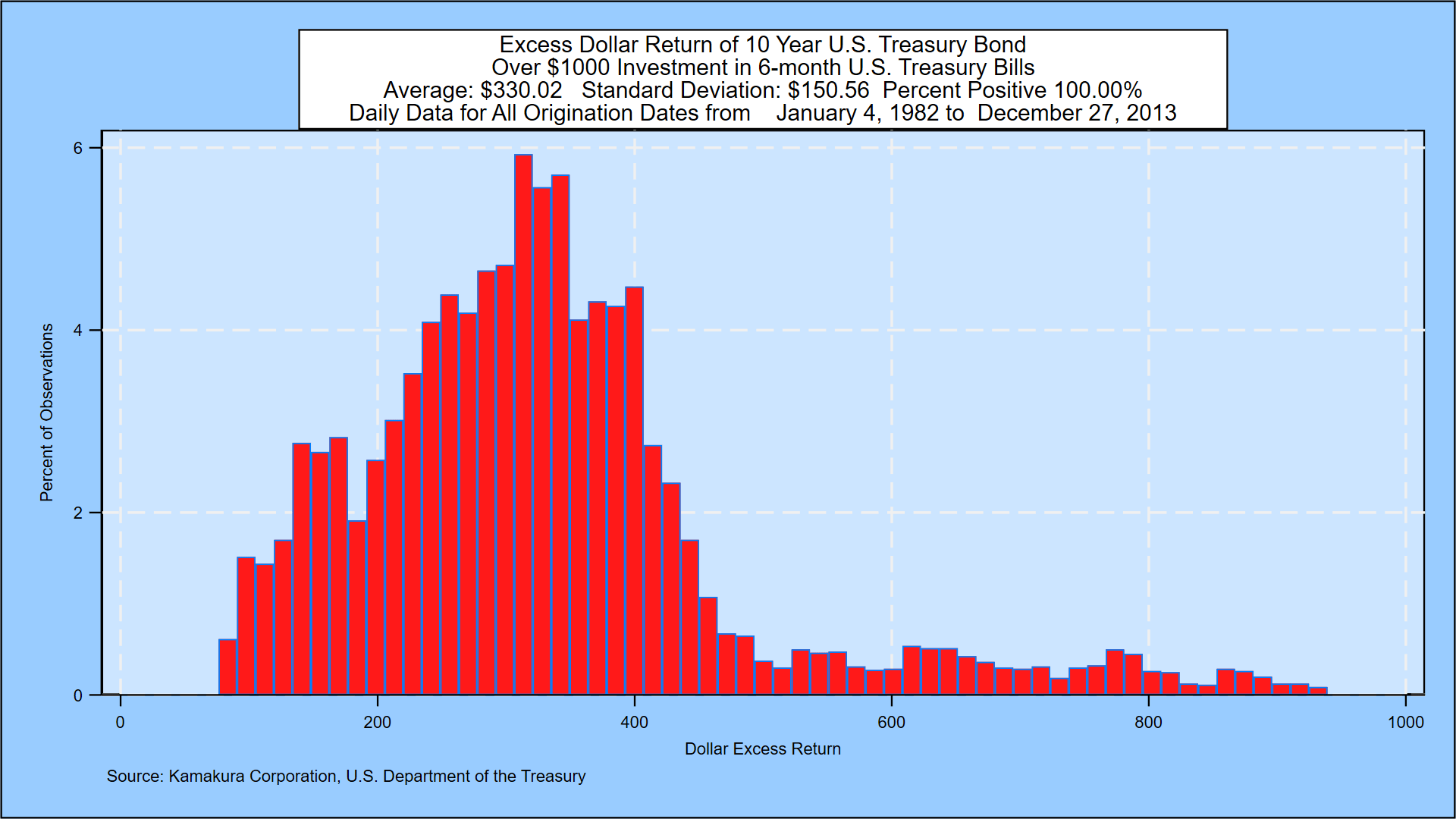

Appendix B exhibits the histogram of realized greenback extra returns for every of the 8 fixed-rate maturities. Appendix C reviews on the histograms of “in progress” pending greenback extra returns for every maturity. For these incomplete intervals, we outline the “pending excess return” because the identified greenback benefit of the fixed-rate Treasury bond over the 6-month T-bill funding as of the statement date. For instance, on August 26, 2022, the quantity of curiosity that will likely be paid on a 6-month Treasury invoice equal that matures in 6 months (not essentially 182 days) on February 26, 2023, is understood with certainty. We tally all the pending greenback time period premiums, all of which have a differing time to maturity, within the histograms in Appendix C.

One of many causes for the optimistic long-term premium outcomes is the big dimension of the “interest on interest” earned on the fastened coupon funds, that are assumed to be invested in 6-month Treasury payments. The very best complete realized greenback returns for all the accomplished fixed-rate intervals are proven in Appendix D. The bottom complete realized greenback returns for every of the fixed-rate holding intervals are proven in Appendix E.

Conclusions

The full greenback returns for the ten, 20 and 30-year Treasury bonds have exceeded the overall greenback returns for the 6-month T-bill cash fund on each accomplished holding interval for which knowledge is on the market. That is due partly to “interest on interest” earned on coupon funds rises when charges rise over the holding interval, and, not less than thus far, this has been sufficient to generate strictly optimistic extra returns for 30-year bonds. The current spike in short-term rates of interest, nonetheless, exhibits that the danger of “going long” just isn’t zero, particularly for maturities of 5 years and beneath. The following replace of this evaluation will likely be stuffed with extra drama.

With respect to the historic capability of Treasury yields to anticipate inflation, we conclude that the market’s forecast of future inflation has typically been fairly correct for very long-term holding intervals.

With respect to the historic extra returns versus the T-bill technique, the rewards for purchasing long-term bonds have all the time been optimistic for maturities of 10 years and over. For shorter maturities, the typical premium is optimistic in any respect maturities for accomplished holding intervals. For holding intervals in course of, the typical extra return is detrimental for maturities of seven years and beneath and optimistic for maturities of ten years and longer.

It goes with out saying that there isn’t any assure that the long run will likely be just like the previous. On the similar time, expectations for the long run needs to be set with the previous in thoughts.

The Appendices can be found in a supplemental PDF file upon request to the creator.

References

Adrian, T., R. Ok. Crump, B. Mills and E. Moench (2014), ‘Treasury Time period Premia: 1961-Current’, Liberty Road Economics, available here.

Adrian, T., R. Ok. Crump and E. Moench (2013), ‘Pricing the Time period Construction with Linear Regressions’, Journal of Monetary Economics 110(1), pp. 110-138.

Li, Canlin, Andrew Meldrum, and Marius Rodriguez (2017). “Robustness of long-maturity term premium estimates,” FEDS Notes. Washington: Board of Governors of the Federal Reserve System, April 3, 2017, available here.

Heath, David, Robert A. Jarrow and Andrew Morton (1992),” Bond Pricing and the Term Structure of Interest Rates: A New Methodology for Contingent Claim Valuation,” Econometrica, 60(1), pp. 77-105.

Kim, D. H. and J. H. Wright (2005), ‘An Arbitrage-Free Three-Issue Time period Construction Mannequin and the Latest Habits of Lengthy-Time period Yields and Distant-Horizon Ahead Charges’, Federal Reserve Board Finance and Economics Dialogue Collection 2005-33.

Ramaswamy, Srichander and Philip Turner, “A dangerous unknown: interest rate risk in the financial system,” Central Banking, February 7, 2018.

Footnotes

[1] Dialog with the creator, 2015.

[2] It is a completely different knowledge collection than was utilized by the papers reviewed by Li, Meldrum, and Rodriguez. The number of the U.S. Division of the Treasury collection was intentional, due to rate of interest smoothing high quality benefits that we focus on in a separate be aware.

[3] The “use of proceeds” of money thrown off from coupon funds was chosen for 2 essential causes. First, the everyday educational assumption that money generated is reinvested in the identical safety is an funding technique that’s troublesome, if not unattainable, to execute within the U.S. Treasury market as a result of a scarcity of liquidity in “off the run” points. Second, such an method preserves the valuation of the Treasury bond when utilizing the risk-neutral discounting methodology of Heath, Jarrow and Morton [1992].