wildpixel

At first of the 12 months, the market was pricing in pretty excessive odds of as many as 5 rate of interest cuts by the Fed this 12 months, the primary one coming in March. Now, only a month later, March seems to be off the desk with the chances of a minimize down to only 23.5% immediately. Should still reveals a 55.1% probability of a minimize of 0.25% to 5-5.25% and June reveals a 52.4% probability of one other 0.25% minimize. The remainder of the 12 months reveals probabilities of additional cuts at lower than 50% and the top of the 12 months reveals the best odds (38%) that charges will probably be right down to 4 -4.25%. That might nonetheless be a complete of 5 cuts however the market’s confidence in that path has deteriorated considerably since January. Why? Effectively, the Fed has actually finished its finest to knock down the hypothesis however I feel the actual causes are extra elementary.

The post-COVID financial system has been a troublesome one to navigate as a result of nobody has ever skilled something prefer it. The companies and items sides of the financial system have been out of sync because the onset of COVID. Earlier than the financial system was absolutely re-opened, the products facet of the financial system boomed, whilst provide chain points brought on shortages and quickly rising costs. Because the financial system re-opened with the introduction of vaccines, companies began to broaden quickly as items consumption fell again. The pullback in items consumption was exacerbated on the manufacturing and wholesale degree by a build-up of inventories. Many items had been double- or triple-ordered to ensure shops had enough inventory and as soon as provide chains healed, all these further orders had been crammed. The consequence was a build-up of inventories that crammed warehouses. The manufacturing a part of the financial system needed to sluggish as these inventories had been labored down, and it did.

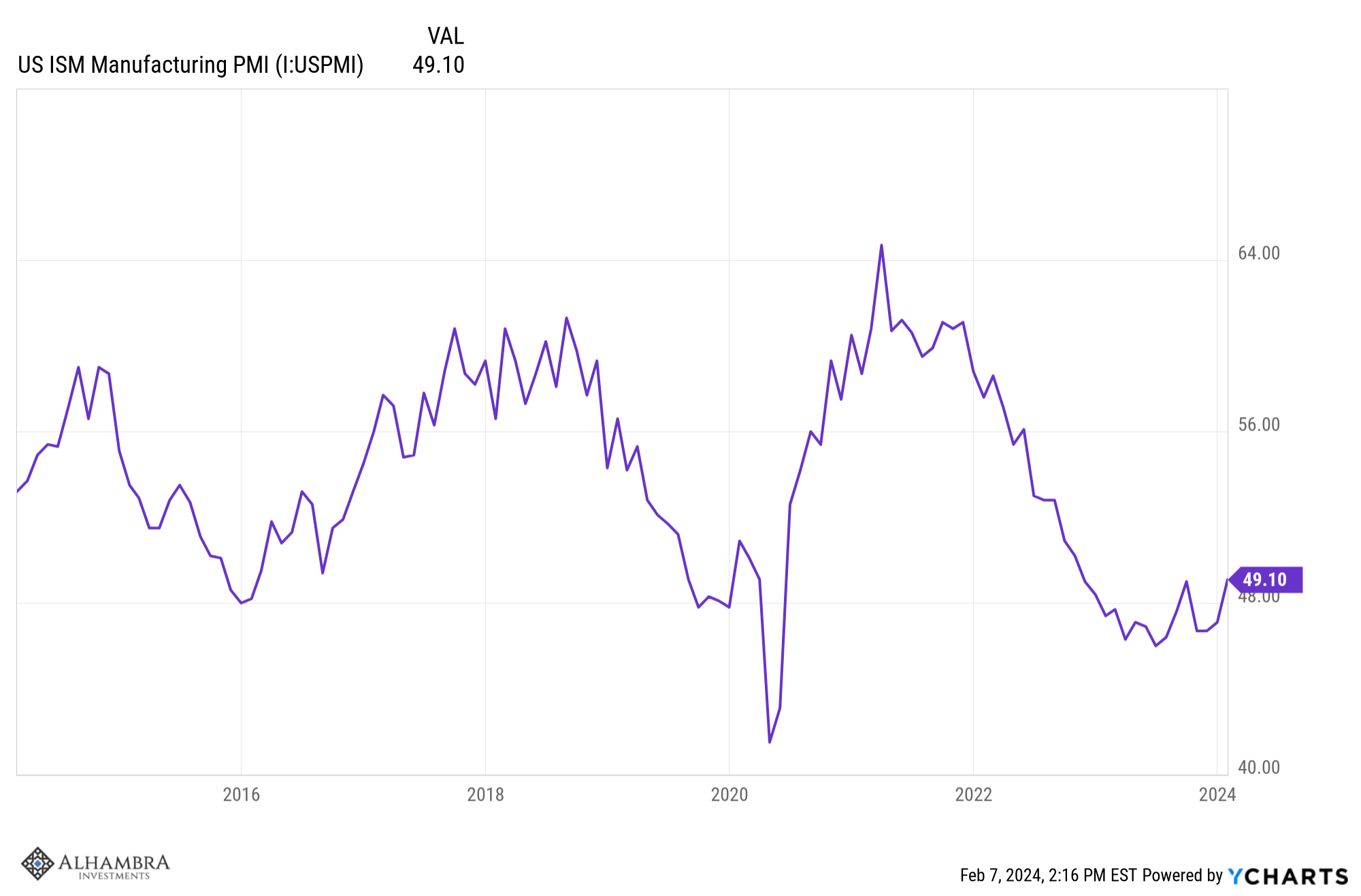

ISM manufacturing and different buying supervisor surveys have appeared recessionary for over a 12 months. On the identical time, the Fed was mountain climbing charges quickly and the yield curve inverted, a conventional omen of recession. The overwhelming consensus in the beginning of final 12 months was that recession was inevitable in 2023, which, in fact, turned out to be unsuitable. The expectations for fee cuts this 12 months had been/are based mostly on the identical indicators that failed final 12 months. Coming into this 12 months, the ISM manufacturing index had been under 50, indicating contraction, for 14 consecutive months, a situation that had by no means existed exterior recession. The brand new orders index was even worse, under 50 for 18 of the final 19 months and, once more, one thing that had by no means occurred, exterior of recession or in any other case.

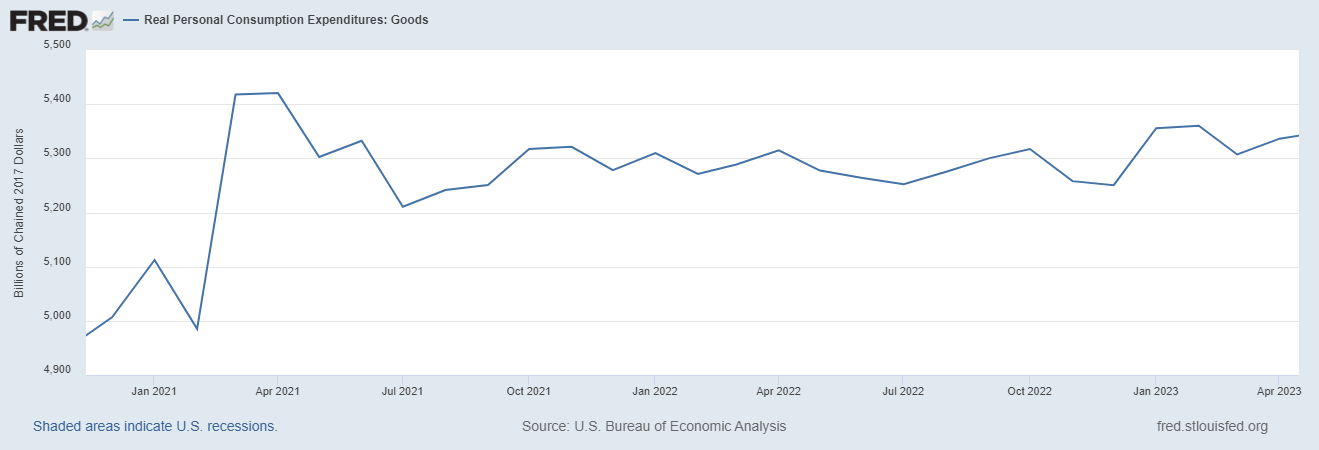

The ten-year/2-year Treasury yield curve inverted in July of 2022 and stays inverted immediately, though not as deeply as its nadir in July of 2023. The ten-year/3-month unfold adopted in October of 2022 and it appeared that recession was, certainly, inevitable. No such recession materialized as a result of the companies facet of the financial system continued to broaden and items consumption, whereas not rising because it had earlier, didn’t fall both. From June of 2021 to April of final 12 months, actual private consumption of products was primarily flat.

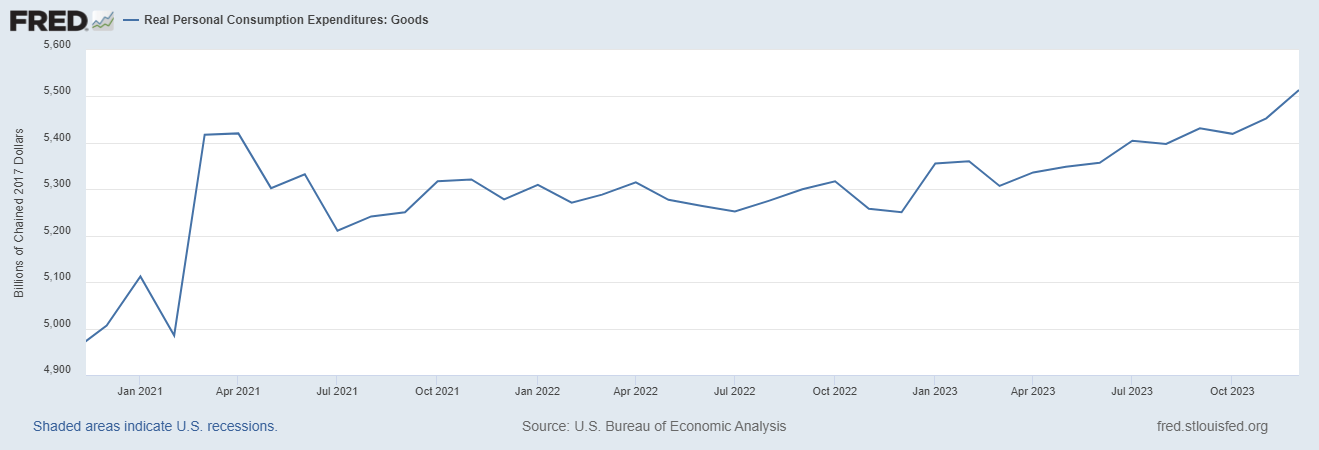

There have been a number of manufacturing-based indicators that turned unfavorable in ’22 and stayed there. The Convention Board’s Main Financial Indicators, that are skewed to manufacturing, have been signaling recession for almost two years. The S&P International Manufacturing PMI has been in contraction since late 2022 (with a few readings close to 50). However not too long ago, we’ve began to see some enchancment in these indicators, and I’m not shocked. Why? As a result of items consumption resumed its rise months in the past, and it was solely a matter of time earlier than manufacturing needed to choose as much as restock cabinets. Right here’s what the chart above appears to be like like for those who prolong it by the top of the 12 months:

What’s improved? The ISM Manufacturing index isn’t above 50 – but – however it rose to 49.1 in January and, extra importantly, the brand new orders index rose to 52.5. The S&P International PMI is again above 50 at 50.7 and almost 3 factors above the December studying. That’s the strongest enchancment since September of 2022. Even the Main Financial Indicators have improved; the contraction over the past 6 months was 2.9% versus 4.3% within the earlier 6 months.

On Wednesday, the newest piece of proof arrived within the type of the Logistics Managers’ Index. In case you aren’t aware of it – and most of the people aren’t – right here’s how they describe the survey on their website:

Logistics Metrics similar to transportation, warehousing, and stock are main financial indicators, and may level in the direction of potential actions within the general financial system. In our month-to-month survey, we collect the responses of over 100 professionals on the motion and path of eight key logistics metrics. These metrics are aggregated into the Logistics Managers’ Index, which is launched on the primary Tuesday of each month.

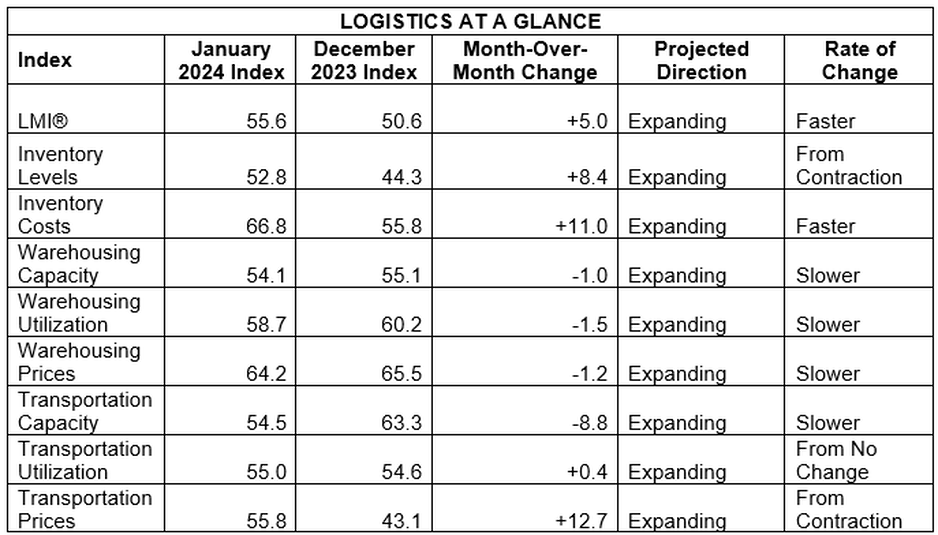

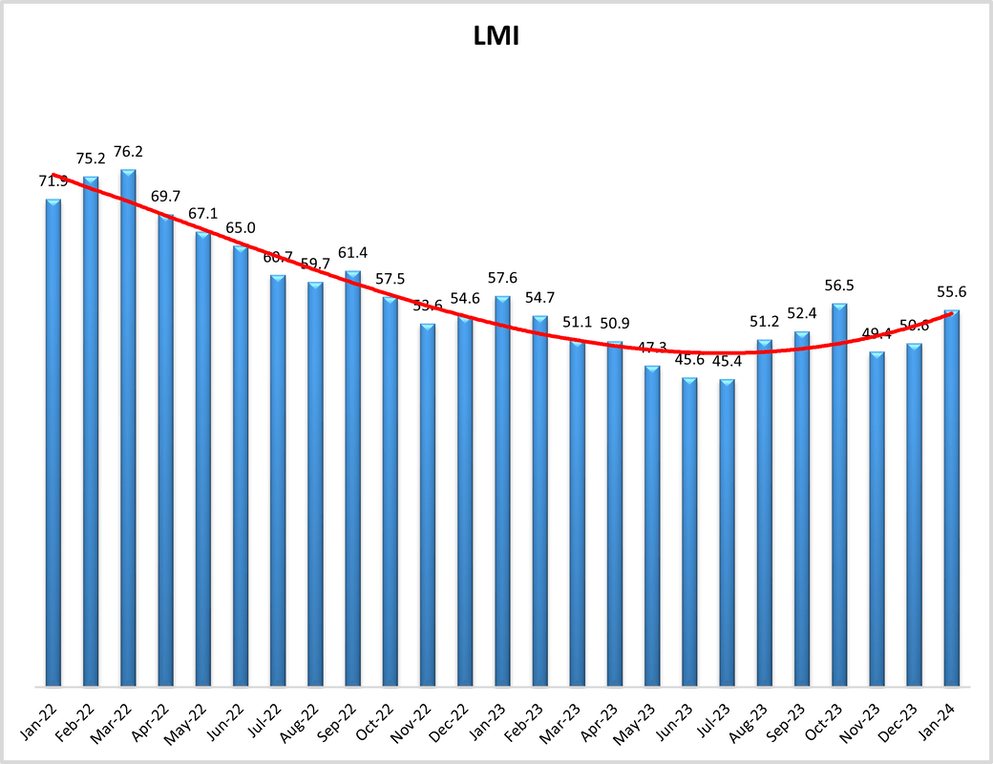

The index rose to 55.6 in January (it’s a diffusion index, so above 50 signifies enlargement). 5 of the final six readings have been above 50, and the index bottomed in July of final 12 months. Highlights from the commentary:

- For the primary time since September of 2019, each metric within the Logistics Managers’ Index is studying in enlargement territory.

- Probably the most important transfer is the long-awaited return of Transportation Costs (+12.7) to enlargement, its first look on the optimistic facet of the ledger since June of 2022 in the beginning of the freight recession.

- This progress is pushed by a rise within the restocking of inventories – particularly for retailers – after a busy vacation season as People are clearly feeling higher concerning the general financial system.

- Respondents had been requested to foretell motion within the general LMI and particular person metrics 12 months from now. The optimism respondents have been reporting on future circumstances all through the second half of 2023 have partially come to fruition in January, however respondents count on even future progress all through the remainder of 2024. Future predictions for the general index are 62.8 which is up (+3.9) from December’s future prediction of 59.9. This could exceed the all-time index common of 62.4 and would signify a wholesome fee of enlargement.

There are some variations within the report between upstream (producers) and downstream (retailers). Stock restocking isn’t aggressive, so this isn’t in anticipation of a surge of any form, simply regular restocking in a world that’s nonetheless largely “just in time”. However the pattern is fairly apparent:

I began writing about this months in the past in my weekly commentaries, and now we’re beginning to see it present up within the information. Sure, it’s survey-based and topic to all the traditional volatility related to such indicators. However surveys will be helpful anecdotal proof and are most helpful popping out of contractions, as we appear to be in at the moment.

If items consumption is rising once more and manufacturing has seen the worst for this slowdown, what does that say concerning the financial system and the prospect for fee cuts this 12 months? The Fed’s Abstract of Financial Projections, released in December, confirmed a median expectation by FOMC members for 3 fee cuts in 2024. In case you’ve been round lengthy sufficient (I feel I’m properly previous “enough”) you realize that’s going to be unsuitable; the one actual query is how. I feel most individuals simply assumed it’d be unsuitable by not anticipating sufficient fee cuts. What if the actual shock is that they’re anticipating too many?

Editor’s Word: The abstract bullets for this text had been chosen by In search of Alpha editors.