Eoneren/iStock via Getty Images

Pareto upgrades are a key technique for improving yield on invested capital over time. This article will discuss what Pareto upgrades are, how to use them, and highlight real examples of how we improved yield on invested capital from 8.53% to 11.33% in under 2 years. We conclude with actionable opportunities available today.

What is a Pareto upgrade?

Pareto superiority is an economic concept in which one choice is better in at least one parameter while being at least equal in every other parameter. You get to upgrade in one area without sacrificing in any other area.

This is generally not the case with most stock trades. If one is debating whether to buy Exxon Mobil (XOM) or Microsoft (MSFT), they may choose Microsoft for its higher expected growth, but in so doing, miss out on the better value of Exxon. Even if you can find a stock that is both better value and higher growth, it would likely be a different economic exposure resulting in an entirely different set of risks.

These sorts of stock selection considerations are an essential part of portfolio management, but they are always a tradeoff. You get A or B.

With Pareto upgrades what I am talking about is replacing A with something that is strictly better than A.

Real Pareto Upgrade Examples

Different preferred issues from the same issuer are often a source of Pareto upgrades. They are usually pari-passu with the same risks and same underlying economic exposure. However, fluctuations in market price will often make one issue better than another via higher yield or more upside to par.

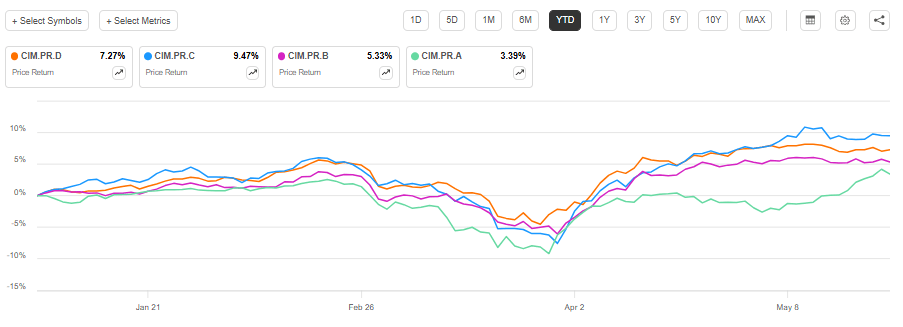

Note the disparate trading between the pari-passu preferreds of Chimera (CIM).

SA

We crunch the numbers continuously and in early April, CIM-C was the better issue while presently CIM-A is the better issue.

Each time a different issue stands out as superior in terms of YTM and upside to par, there is an opportunity to flip from the expensive issue to the relatively cheaper issue. In so doing, one can clip a few basis points of excess yield.

Pareto upgrades are also present in different classes of stock from the same issuer

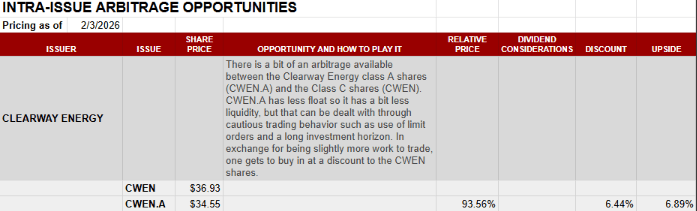

Back in February we wrote about how Clearway Energy (CWEN) A shares (CWEN.A) was much better positioned than CWEN.

“At the current large spread the A shares look far better in my opinion. I think the gap in price between the issues will close over time.”

Here was the pricing at that time:

SA

I consider CWEN.A to have been a Pareto upgrade over CWEN because they both provide the investor with the same claim to the same company, yet the A shares traded substantially cheaper.

On March 9th, Clearway Energy consolidated to a single share class.

The Board has approved a proposal to amend and restate the Company’s certificate of incorporation (the “Charter Amendment”) that would convert each share of the Company’s Class A common stock, par value $0.01 per share (the “Class A common stock”), into one share of the Company’s Class C common stock, par value $0.01 per share (the “Class C common stock”).

This crystallized the arbitrage into immediate realization of the spread.

A similar opportunity exists today with Lennar class B shares (LEN-B) looking much better than Lennar (LEN).

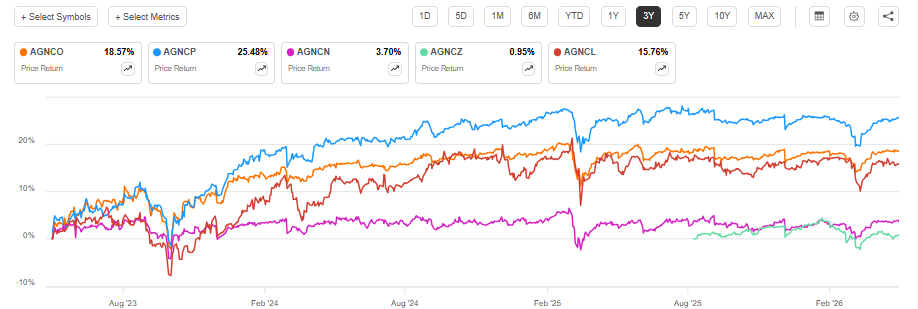

Pareto upgrades with AGNC preferreds

The AGNC Investment Corp (AGNC) preferreds are not quite the same as each other because there are significant differences in their floating rate schedules and terms, but the substantial differences in trading behavior between them have created plenty of opportunities in which one issue was clearly better than the others.

SA

In flipping between the AGNC preferreds as they fluctuate in relative opportunity one could repeatedly clip basis points of excess yield.

Cumulative impact of Pareto upgrades

Many investors don’t bother with Pareto upgrades because it feels like such a small gain, but the cumulative effect of doing it repeatedly adds up to something very powerful for yield on invested capital.

These issues trade erratically intra-day with as much as a few percentage points of difference between the bid and ask. This means that one can capture small Pareto upgrades within the same issuer many times. We have traded between the AGNC preferreds dozens of times.

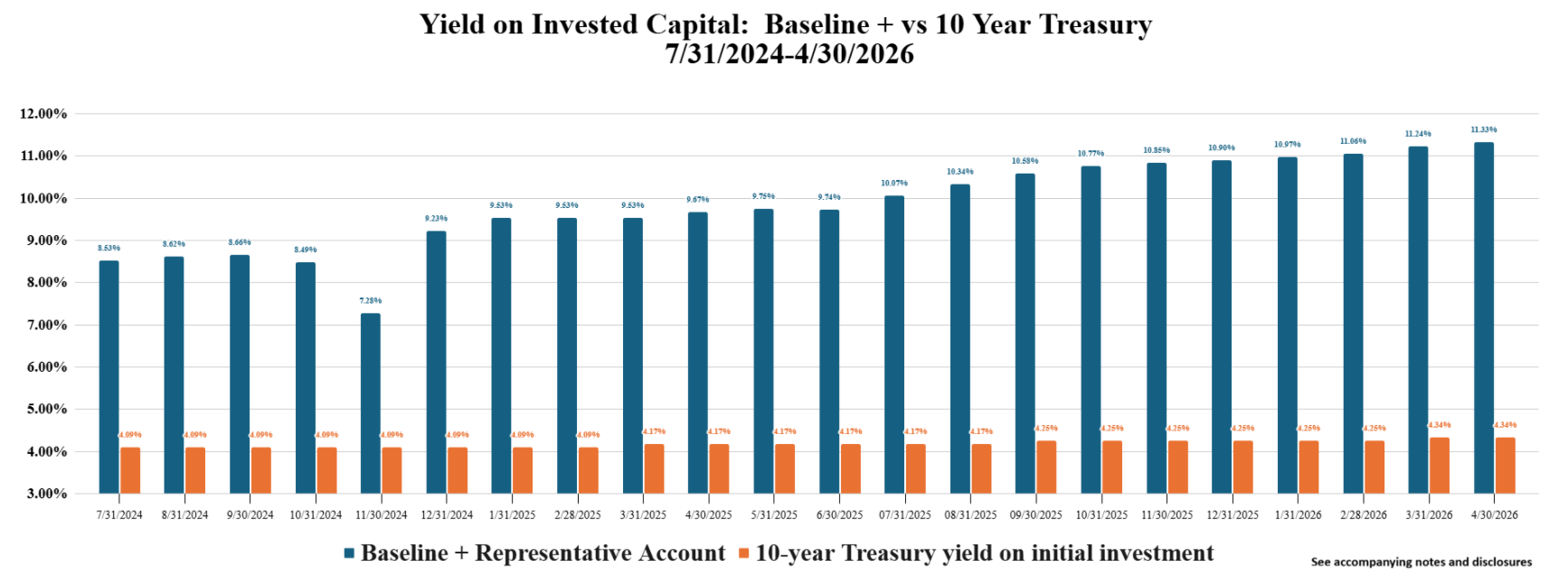

Each time one gets a Pareto upgrade it stacks multiplicatively. The individual trades might only add 5 basis points to yield on invested capital, but after doing it again and again, yield on invested capital starts to materially outpace what one would get from simple dividend reinvestment. To illustrate this point, we can look at the actual data from our Baseline + accounts. Yield on invested capital rose from 8.53% in July of 2024 to 11.33% as of the end of April 2026.

2MC

A significant portion of the rise in yield on invested capital came from repeated Pareto upgrades.

In comparison, investing in a 10-year treasury with just interest reinvestment would have taken yield on invested capital from 4.09% to 4.34% over that same timeframe.

Current Pareto upgrade opportunity

So as to make this less theoretical and more actionable, let us examine a Pareto upgrade that exists today.

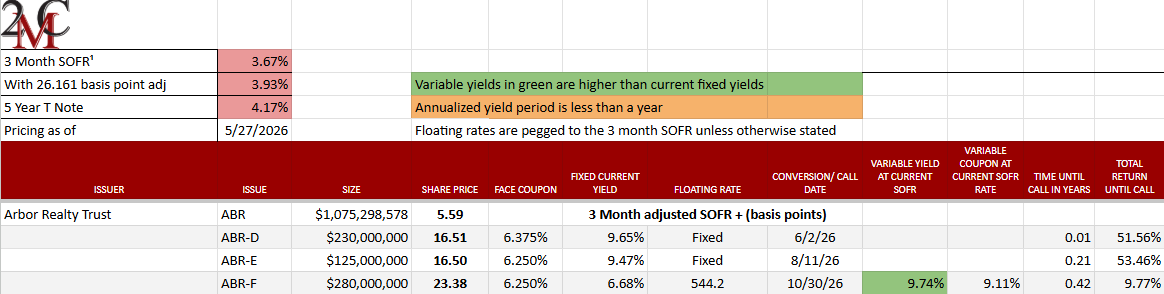

Arbor Realty (ABR) has multiple preferred issues with slightly different terms. ABR-F floats in October while ABR-D and ABR-E are fixed rate.

Portfolio Income Solutions

At the exact pricing of the time of the screenshot, ABR-D is clearly better than ABR-E. Its yield of 9.65% is 18 basis points higher than the 9.47% of ABR-E. They are trading at $16.51 and $16.50, respectively, so the upside to par is essentially identical.

Thus, anyone who currently owns ABR-E could upgrade to ABR-D and get an extra 18 basis points of yield without any extra incremental risk.

While not a Pareto upgrade due to the difference between fixed and floating, I would also argue that ABR-D is substantially better than ABR-F. The yield of D is quite similar to the yield at which ABR-F will float, but the delta in upside to par is massive.

The takeaway

Opportunities to execute Pareto upgrades are ubiquitous yet the majority of market participants do not bother to look at such a granular level for what appears to be a small gain. Do not underestimate the compounding effect of these small gains.