Margarita-Young

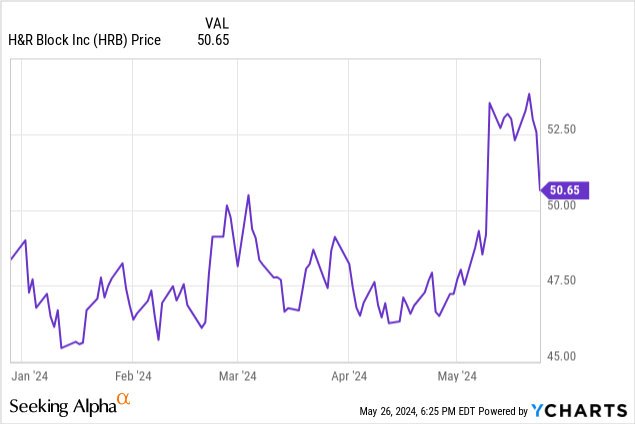

H&R Block (NYSE:HRB) just turned in an exceptionally strong, game changing Q3 quarter. Despite this, shares have recently given up much of the post-earnings gains, dropping 3.6% this Friday, seemingly following Intuit (INTU) lower after its Q4 Guidance disappointed. INTU, which trades at 36x earnings, is not even in the same valuation ballpark as HRB, but markets don’t always make sense, especially on a low volume Friday heading into a holiday weekend.

I think this recent dip is creating a buying opportunity, and shares rally into the end of the year.

Since my first buy call in September 2020, my view of the investment case in HRB has been straightforward. A stable business trading it a very cheap valuation and using its cash flow to pay dividends and repurchase shares. It was so cheap it didn’t need revenue growth to be a real winner. At the time, my concerns were:

- Expense control.

- Throwing good money after bad with another acquisition like Wave.

In the past 3.5 years, HRB has done a great job in controlling expenses, and they have not pursued another value destructive acquisition like Wave.

But now the business is showing pricing power in this inflationary environment, and we’re seeing revenue gains and the resulting operating leverage at work. This, plus continued share repurchases, could re-rate HRB higher than this 10-11x EPS ceiling it’s been rangebound in over the last few years.

Revenue Growth and Operating Leverage

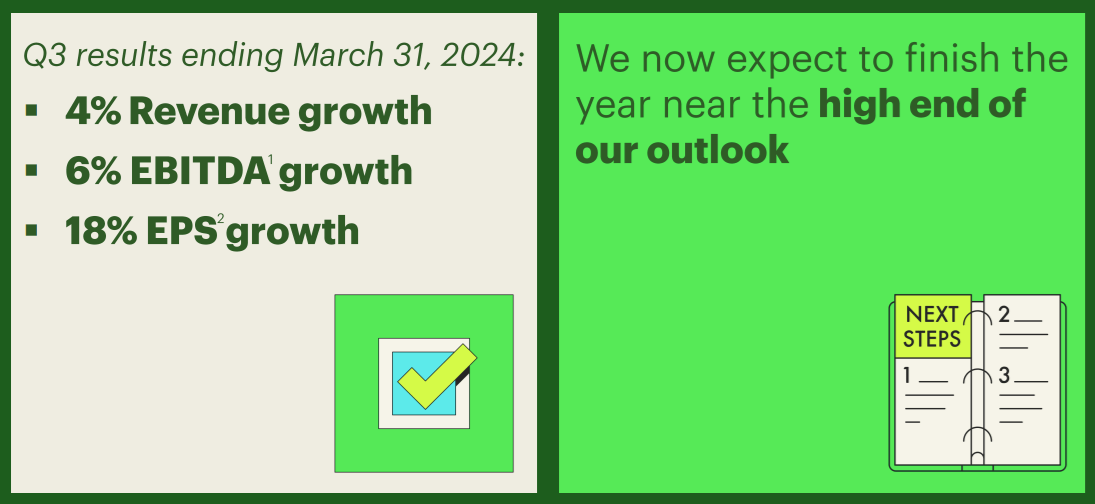

H&R Block delivered exceptional Q3 earnings, beating both top and bottom lines. Most importantly, after a few years of holding pricing steady, the company is taking price through low single digit inflationary type price increases. These increases are showing real operating leverage, where EBITDA growth is a multiple of revenue growth.

HRB Q3 Results (HRB Q3 Investor Presentation)

As far as “finishing near the high end”, I believe H&R Block will exceed the high end of the forecast when Q4 results are released, potentially coming in around $4.50/share.

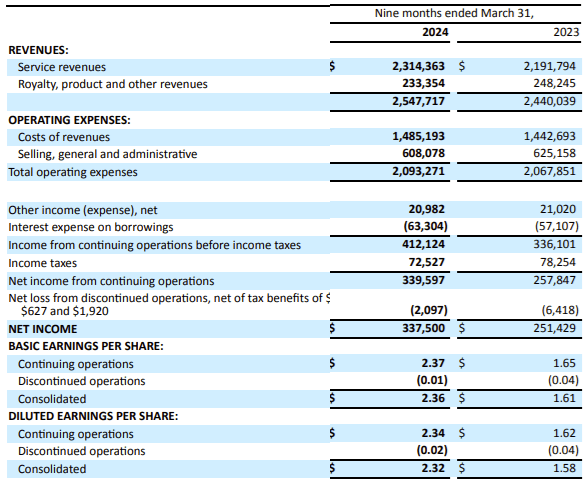

The key bullish piece of these earnings is how mild 4% revenue growth, driven by slightly higher pricing (7% increase in DIY, 4% in assisted), coupled with good expense control, is dropping more income to the bottom line. Earnings before taxes is up a whopping 23% year over year, which has translated into a 47% increase in EPS year over year (due to a favorable tax rate and lower share count.)

HRB FY24 Earnings (HRB Q3-24 10-Q)

I see no reason the 3-4% yearly increases will draw any negative reaction from customers. That feels mild compared to all of the other inflation in professional services and the broader economy. HRB could be entering a multiple year period where 3-4% topline growth turns into 10% net income growth, with share purchases driving another 5% EPS growth on top of that.

Expense Control

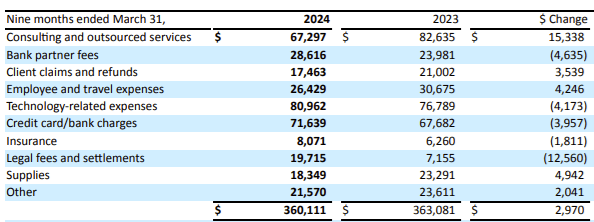

Credit to the H&R Block leadership team as they have done a fantastic job controlling expenses over the past 4 years. Expense control was my biggest concern when I made my investment in 2020. Their annualized spend on the below items is effectively on par with what they spent 4 years ago in nominal dollars, so in real terms, they’ve tightened spending a solid amount.

H&R Block Expenses (HRB Q3-24 10-Q)

I’m particularly happy with the job they’ve done, reducing the Consulting and outsourced service expenses. They spent $127 million on this in 2021 and are on track to spend closer to $90 million this year. My opinion on this is colored by my own professional experience, with the best run companies I’ve worked for and with having full time employees for most roles, while some of the worst and most inefficient companies I’ve worked for/with overly relying on consultants and 3rd party services for too many core business tasks.

Occupancy expenses are another area of spend they controlled very well, as well as Marketing. A $200 million marketing budget still seems high to me, but I’m happy this is flat to slight down year over year while achieving good revenue growth.

H&R Block Expenses (HRB Q3-24 10-Q)

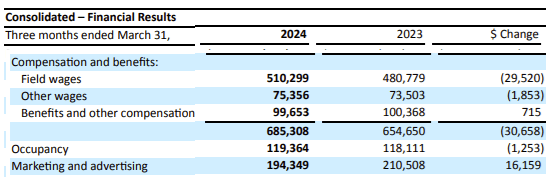

The only place where expenses have gone up significantly is in field wages, and that’s exactly where I would expect it to track with this competitive labor market. If I didn’t see this expense up at least 5%, I’d be worried they were sacrificing quality in their field teams.

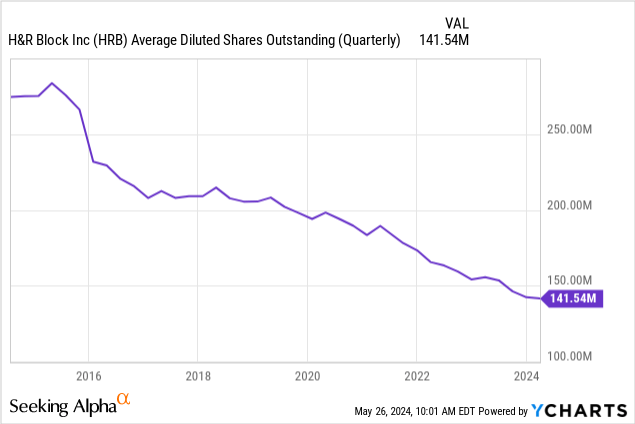

The incredible shrinking share count

In the past year, H&R Block executed some exceptionally well timed repurchases, buying the dip on itself and repurchasing $200 million at $31 in Q1 followed by another $132 million in Q2 around $40. They decreased the share count from 155.6 million down to 141.5 million in the past year.

H&R Block has repurchased nearly half the outstanding shares since 2016.

They will likely deploy another $300-400 million in the back half of this calendar year (their fiscal Q1 and Q2, where they execute most of these yearly purchases because of “narrow trading windows”.)

Conclusion

Markets and sentiment are funny sometimes.

In 2015, with the average S&P 500 firm trading around 15x earnings, HRB traded ~20x earnings ($33 share price got you $1.75 in diluted EPS.) Now, a decade later and despite returning nearly 100% of income to shareholders and repurchasing half the outstanding shares, it trades at half that multiple despite the broader market becoming significantly more expensive.

If HRB is able to show 15% EPS growth for the next few years through a combination of low-mid single digit revenue growth plus share repurchases, which I believe is very achievable, it deserves a higher multiple than 11x.

Starting at $4.50 for this year (my estimate) 15% EPS growth for the next 2 years yields ~$6 in earnings by 2026. At a 15x multiple, that’s a $90 stock.

H&R Block remains a compelling buy, and the 7% selloff over the last week provides a good entry point.