DSCimage/iStock by way of Getty Photographs

Introduction

Hudson Applied sciences (NASDAQ:HDSN) is the biggest participant within the U.S. refrigerant reclamation market and is strategically positioned to capitalize on the transformative modifications pushed by the AIM Act. With a 65% inventory improve since its 2023 low and a staggering 900% return over 5 years, Hudson could also be poised for much more development within the years forward. Hudson isn’t only a provide chain and inflation beneficiary or a COVID-era work-from-home story. Let’s discover Hudson’s market alternative and the way it may be capable of make the most of the regulation poised to shake up the trade.

Funding Thesis

The AIM Act is a long-term catalyst that can present Hudson with a possibility to speed up revenues and make the most of its working leverage because the reclamation market expands. Hudson already holds the biggest share of the U.S. refrigerant reclamation market; this positioning, mixed with its know-how benefit over rivals, a robust steadiness sheet, and a administration staff centered on the long-term alternative of the AIM Act supplies the chance for traders to realize market-beating returns, even after Hudson inventory has gained greater than 65% since its 2023 low.

The refrigerant reclamation market is in excessive development mode. A Dataintelo report in 2021 estimated a 10.5% CAGR from 2023 to 2031. Nevertheless, I consider that the AIM Act might greater than double that development fee, because it brings the start of a dramatic step down in HFC manufacturing beginning this yr. This supplies an unimaginable alternative for Hudson, which is completely positioned to profit. Similar to Hudson’s administration, I consider 2024 might mark an inflection level for the corporate’s enterprise.

Reclamation Market Is Set for Unprecedented Progress

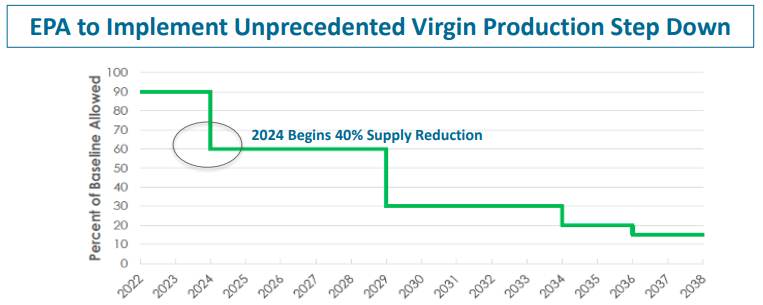

The refrigerant market is present process one other regulatory change with the AIM Act. The AIM Act mandates a gradual discount within the manufacturing and consumption of excessive GWP (excessive world warming potentials) refrigerants (HFCs) in the US, finally lowering HFC manufacturing by 85% in 2036 and past. The phase-down of upper GWP refrigerants will without end alter the provision and demand panorama.

Timeline of HFC Manufacturing Discount from AIM Act (HDSN Investor Presentation (Q3 2023))

Efficient January 1st of this yr, the quantity of HFCs allowed to be produced has now fallen to 60% of baseline. This marks a dramatic discount in virgin HFC manufacturing, growing the necessity for recycled and various refrigerants to fill the hole. As with all discount in a commodity market, it’s anticipated to drive refrigerant costs increased.

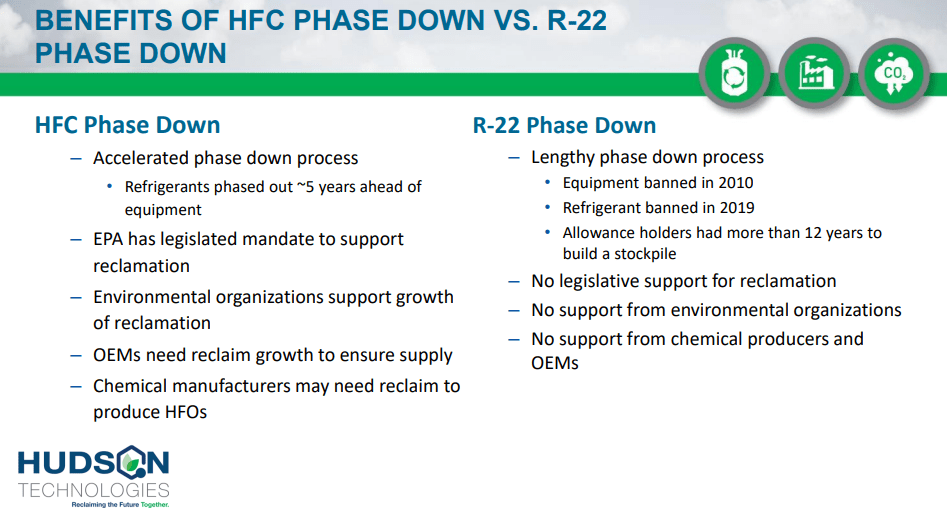

Not like previous phase-outs of refrigerants, the AIM Act is anticipated to make a extra significant change to HFC provide. When R-22 was phased out, the tools was the primary to go, permitting producers to stockpile R-22 earlier than the refrigerant was phased out. Costs fell when suppliers flooded the market with stockpiled R-22, and Hudson suffered. Nevertheless, this time, the HFC refrigerants are slated to be phased out first.

HFC step-down is anticipated to be extra impactful than previous step-downs (HDSN Investor Presentation (Q3 2023))

The precise impression the AIM Act could have on refrigerant manufacturing and reclamation markets will not be absolutely understood, however it’ll cut back the manufacturing of virgin refrigerants; Hudson’s administration anticipates a provide scarcity ensuing inside two years. Consequently, costs and the demand for reclamation, recycling, and re-use of current refrigerants will probably rise. Hudson is already positioned to make the most of this shift; 2024 might mark an inflection level for the corporate’s enterprise.

Hudson’s administration has talked about that these modifications might drive a 6x – 10x demand increase in reclamation. They didn’t specify what timeframe that 6x – 10x improve may happen over. This can be a essential a part of my thesis, however it’s tough to quantify the impression that it’s going to have available on the market for refrigerants. Nevertheless, we are able to estimate the rise in recycled refrigerants required to switch virgin refrigerants throughout this step-down.

Notice: These calculations exclude current virgin refrigerant inventories.

Quantifying The Influence of The AIM Act

Let’s use the whole refrigerant market as a baseline for demand development, then alter for the step-down in virgin HFC manufacturing and decide how a lot recycled refrigerants could also be wanted to fill the hole.

The North American refrigerant market is anticipated to grow at a 6.8% CAGR, however there might be a shift from new refrigerant manufacturing in the direction of recycled refrigerants. However how a lot development will the refrigerant reclamation market see in consequence? With out obtainable market measurement information for the North American reclamation market, we are able to use the worldwide market as a proxy after which make some changes for conservatism.

Primarily based on the estimated world reclamation market measurement of $1.29 billion and the whole world refrigerant market of $22.4 billion, the worldwide share of refrigerant recycling is 5.3%. If the recycled refrigerant market makes up 5.3% of the whole refrigerant market, we are able to use the step-down figures (“Baseline Virgin Production Levels”) from the AIM Act to estimate how a lot of a lower in HFC manufacturing ought to happen (“Virgin Refrigerants”) and the way a lot development might be wanted to account for a diminishing provide of virgin refrigerants (“Recycled Refrigerants”).

The phase-out of HFC manufacturing is anticipated to create important development potential within the reclamation and recycling market (Creator-generated desk)

We are able to see the potential for a 10-year CAGR of 39.9% for the refrigerant recycling market and a CAGR of 27.9% over the following fifteen years.

Nevertheless, the American market could differ from the worldwide market. As a result of Hudson is the biggest participant within the U.S. market, we must always think about the chance that refrigerant recycling already makes up a bigger share of the whole market. Let’s conservatively assume that it already makes up 10% of the market.

If we tweak these assumptions to make the present recycling market share 10%, we nonetheless see important development potential. (Creator-generated chart)

We are able to see that the reclamation market would nonetheless develop at an annual fee of 31.4% over the following ten years and 23% till 2039, a number of years after the step-down concludes.

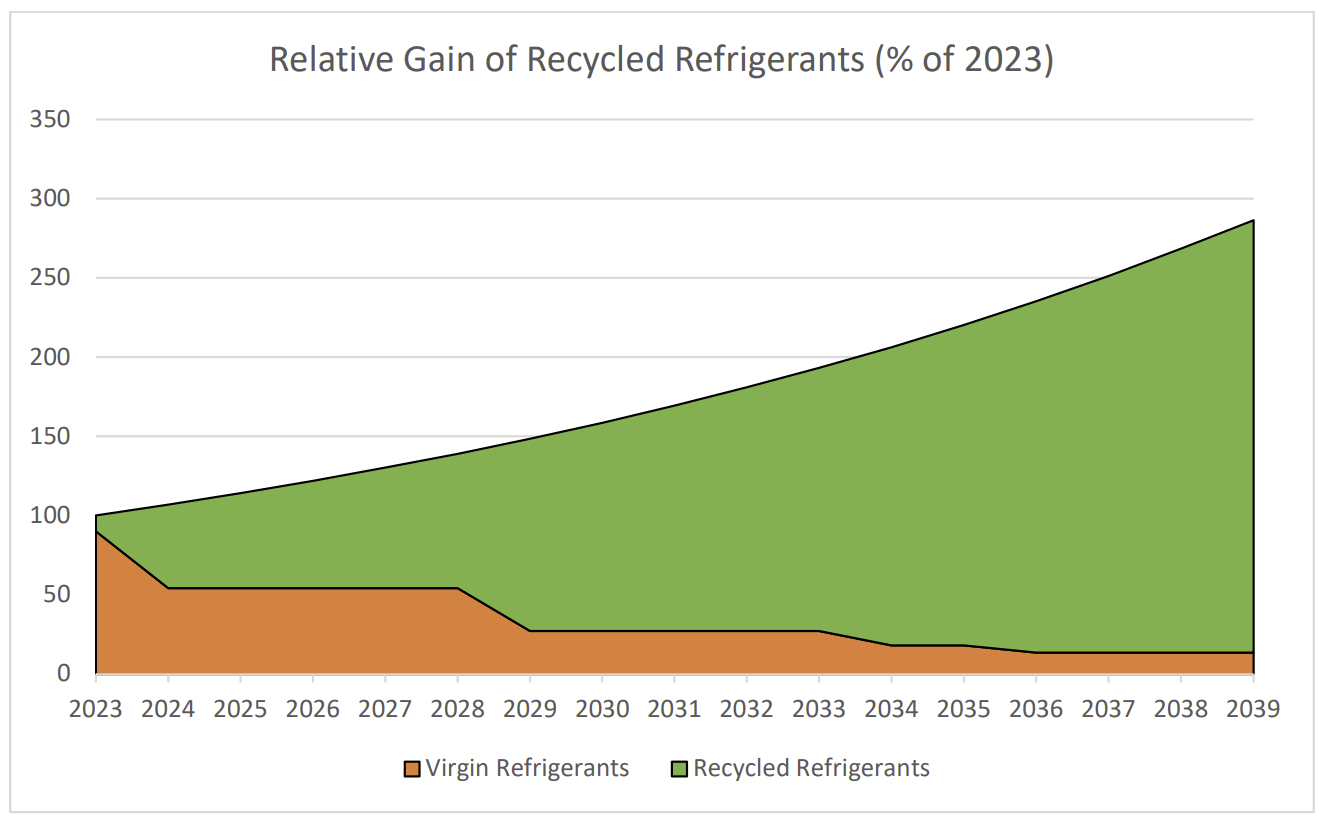

We are able to visualize the potential ahead development in recycled refrigerants.

Ahead Recycled Refrigerant Progress Potential (Creator-generated chart)

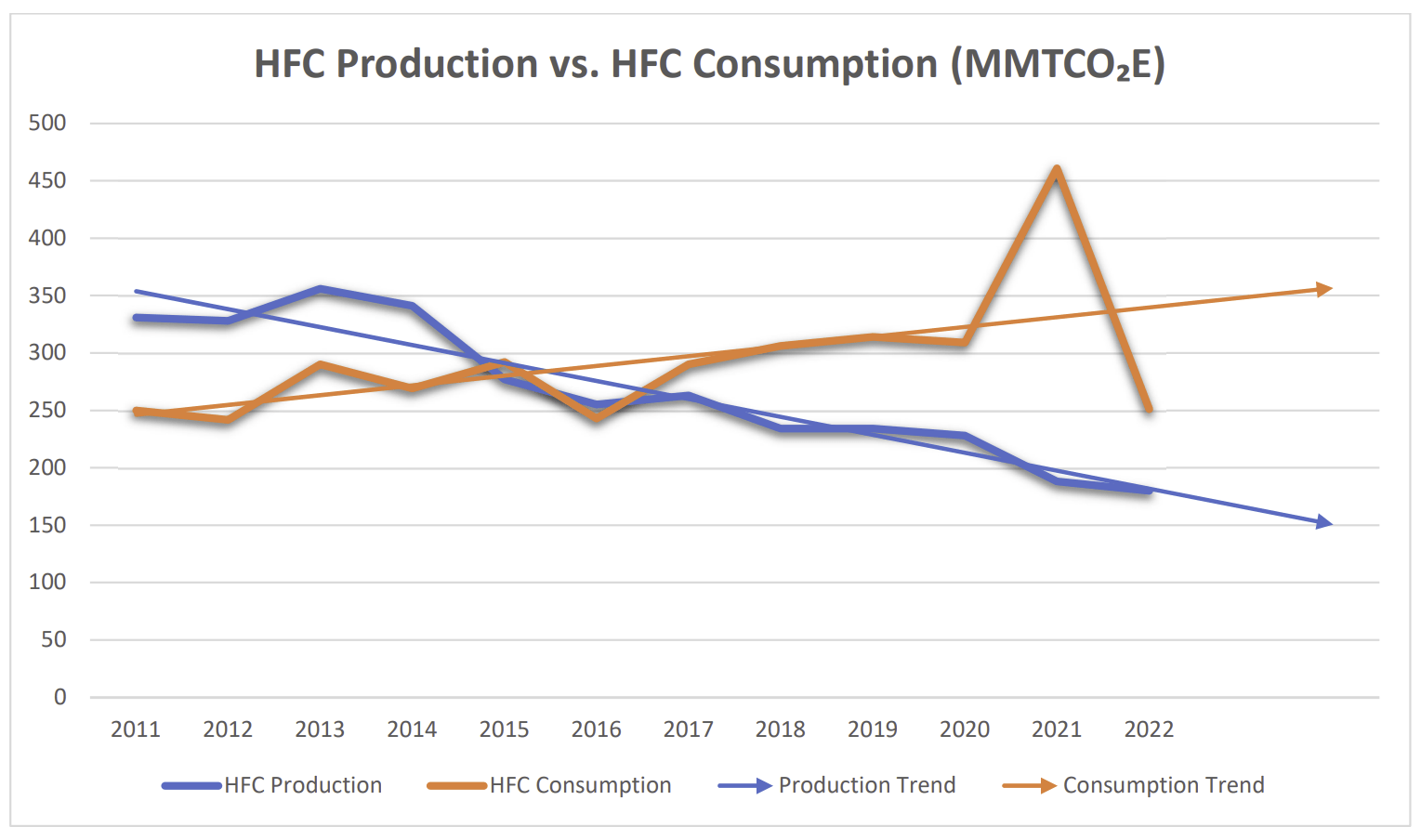

This development is on high of a development of decreased HFC manufacturing whereas consumption of HFCs has elevated.

HFC Manufacturing vs HFC Consumption (Creator-Generated w/ information from the EPA)

It’s vital to notice that these are tough assumptions that don’t embody present stockpiles of HFCs. I believe a extra cheap assumption is that the refrigerant recycling market will develop quicker than the ten.5% that was anticipated within the Dataintelo report. The outlook has modified since then, because the AIM Act has impacted the market. I can fairly see the reclamation market rising as a lot as 20% yearly, however I don’t anticipate it to develop at 40%.

Progress Assumptions

After I do my valuation work, I begin with figuring out the expansion assumptions wanted to help an organization’s present inventory worth utilizing a easy reverse discounted money movement mannequin. Then, I work backward to make sure the corporate’s fundamentals help this development.

HDSN is a small-cap development inventory; I need to see the potential for large returns earlier than I commit to purchasing and holding an organization in a cyclical trade with a unstable inventory worth. If I merely need market-like returns with some upside, I can extra safely play the HVAC trade by investing in bigger firms like Watsco (WSO), Lennox (LII), and/or Provider (CARR), and many others., and attempt to purchase them when the shares are comparatively low-cost. In investing in HDSN, I hope to attain market-smashing returns in a sector with secular tailwinds. Subsequently, I’m going to make use of 15.0% as my hurdle fee. I consider {that a} 2.5% terminal development fee is warranted, given the expansion potential within the reclamation market over the following 15-plus years.

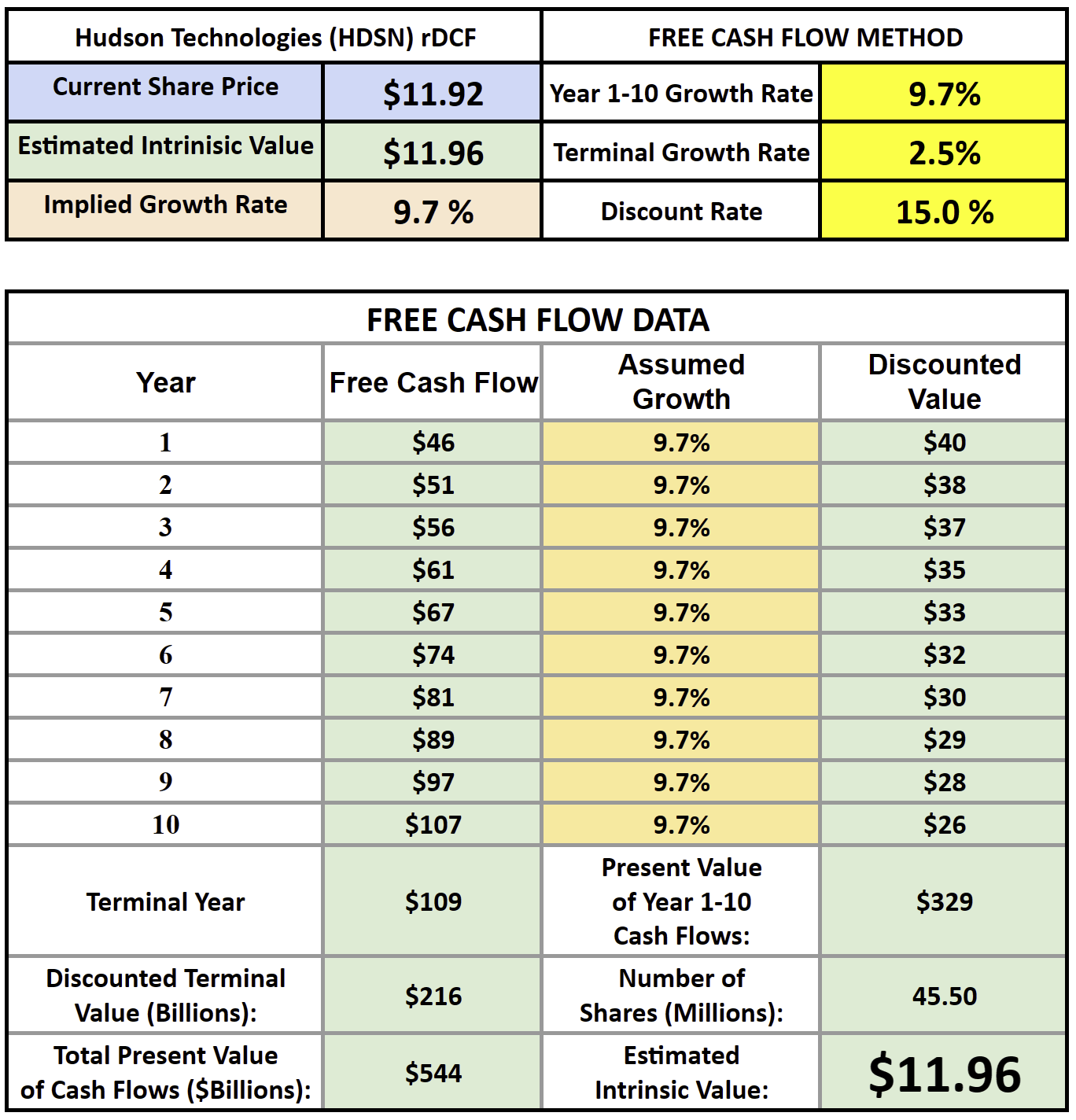

HDSN Reverse DCF – 9.7% FCF Progress Expectation (Inputs: Creator-generated, Calculator: www.BrianFeroldi.com)

Primarily based on Hudson’s TTM FCF of $42.2 million, the corporate would solely have to develop free money movement at 9.7% yearly over the following ten years.

Let’s dig deeper to make sure Hudson can obtain this development and hone in on a variety of assumptions for its development potential.

Income Progress and Working Leverage

As not too long ago because the Q3 earnings name, Hudson CEO, Brian Coleman has dedicated to reaching $400 million in income in 2025. That might symbolize a 17% CAGR based mostly on LTM income. This may be a decrease development fee than the final 8 years, as seen under, however an acceleration in development during the last twelve months of outcomes.

Hudson shows a substantial amount of working leverage and the corporate has improved its operational effectivity since buying Airgas Refrigerants in 2017. Since 2015, Hudson has skilled distinctive revenue development, with web earnings rising at twice the speed of revenues (36.6% Web Revenue vs. 18.2% Income).

HDSN has working leverage, as seen in its 2015-LTM financials. (www.FinChat.io)

Throughout the identical timeframe, income grew quicker than COGS and SG&A bills.

HDSN has grown revenues quicker than COGS and SG&A (www.FinChat.io)

Stability Sheet

Hudson borrowed over $155 million in 2017 to fund its acquisition of Airgas. This acquisition could have enabled Hudson to place itself to turn into the chief within the reclamation market, but it surely put its monetary well being in a extra precarious place. Hudson has since launched into a mission to de-leverage in recent times, absolutely paying off its long-term debt in Q3 of 2023, leaving it with a web debt/EBITDA ratio of 0.1, a debt/fairness ratio of 0.1, and a money movement/debt ratio of three.8. This places the corporate ready to climate any downturns available in the market.

Now that this debt is off the books, Hudson will save round $10 million in curiosity expense per yr, supporting web earnings and free money movement development.

Money Flows

Since turning constructive in 2014, Hudson’s free money movement has grown at a 53.6% CAGR, pushed by gross sales development, operational effectivity enhancements, and low capex necessities.

HDSN generates a wholesome development fee in FCF and OCF (www.FinChat.io)

With a stronger steadiness sheet, secular tailwinds, and the AIM Act accelerating development in a better margin a part of the enterprise, free money movement ought to proceed to develop quicker than income.

How Hudson Achieved Sustainable Progress

One of many largest dangers in investing in an organization that has seen 900% returns in a span of 5 years, however solely 2.5% yearly since its IPO, is the chance that latest development will not be sustainable. Hudson is tied to a cyclical trade, although it additionally supplies companies which are extra recurring in nature. It might even be cheap for some to query the sustainability of this development, given the work-from-home tailwinds granted by the pandemic.

Airgas Acquisition

Hudson’s spectacular development in recent times has extra to do with its acquisition of Airgas Refrigerants in late 2017, which allowed the corporate to increase its footprint within the U.S., increase its product choices, and improve its gross sales and distribution capabilities. The corporate’s acquisition thesis was that the elevated scale would permit it to higher serve prospects and place the corporate to make the most of reclamation development as HCFCs have been phased out. On the time, administration was nicely conscious of a future HFC phase-out interval that we’re at the moment coming into. The acquisition helped Hudson turn into extra environment friendly. Administration has said that it’s chargeable for as a lot as half of Hudson’s income base, positioning the corporate as the biggest participant within the reclamation market.

For the reason that Airgas acquisition, Hudson has dramatically elevated its operational effectivity. Its COGS during the last 12 months is sort of the identical as in FY 2018, regardless of growing gross sales by 75%. A few of this is because of accounting guidelines that require mark-to-market stock changes upon acquisition, however the longer-term development confirms this. Since 2013, Hudson’s revenues have grown at 17.9% yearly, however COGS has solely elevated by 12%, exhibiting that Hudson holds some pricing energy. SG&A bills have additionally grown slower than revenues (14.7% vs 17.9%).

Aggressive Benefits

With its proprietary ZugiBeast, Hudson holds a robust place within the reclamation market. The ZugiBeast is an in-line refrigerant reclamation unit that may be put in in giant cooling techniques, permitting it to service cooling techniques on-site. ZugiBeast operates up to 10x faster than different tools, each on-line and offline, permitting prospects to attenuate downtime and improve the effectivity of their techniques. Hudson additionally owns 2 of the 4 AHRI-certified laboratories within the U.S. and has three state-of-the-art reclamation amenities. This offers them a big footprint and unmatched experience within the trade. Holding the biggest share of the reclamation market offers the corporate scale benefits, permitting it to kind strategic partnerships with Lennox Worldwide and AprilAire.

Again to Valuation

If Hudson can merely preserve market share in an increasing reclamation market, and proceed to capitalize on its main place, it ought to be capable of maintain wholesome development for the foreseeable future. Given administration’s targets to succeed in $400m in 2025, I believe an affordable base assumption is that Hudson can develop normalized free money movement at 18% over the following 5 years. Even lowering this development fee for years 6-10 would offer nice returns.

Hudson Applied sciences Discounted Money Circulate (Inputs: Creator generated, Calculator: www.BrianFeroldi.com)

Utilizing the identical 15.0% hurdle fee, 2.5% terminal fee because the reverse DCF carried out earlier, and factoring in these development assumptions, Hudson inventory is at the moment undervalued within the base, bear, and bull circumstances. A weighted common honest worth for Hudson Applied sciences is $18.71. Primarily based on these assumptions, HDSN is undervalued by nearly 57%.

Dangers

Hudson Applied sciences is in a cyclical trade, and the value of refrigerants can have outsized impacts on revenues. Any over-supply to the market can be a danger to revenues and significantly to the underside line, contemplating the working deleveraging impact that will happen. This occurred within the late 2010s and almost broke the corporate, forcing it to interrupt debt covenants and default. Given the energy of its steadiness sheet, its larger foothold within the reclamation market, and the constructive impression anticipated by the AIM Act, I don’t see this taking place this time.

One other danger to Hudson, like most investments, is a recession. If this occurs, we might see a discount within the development of the put in base of HVAC techniques all through the U.S. I anticipate that Hudson is well-positioned to outlive a recession and poised to carry out nicely with out one.

Volatility is one other danger. I usually don’t think about high-beta shares dangerous investments, however for somebody unwilling to abdomen giant down drafts in inventory costs, this may not be the suitable inventory to put money into. I’ve sufficient confidence within the thesis, that I have a tendency so as to add to my place when the inventory is crushed down.

Conclusion

Hudson already controls 35% of the U.S. refrigerant reclamation market, has robust relationships with prospects, and has created new partnerships with giant gamers within the HVACR trade in recent times. Its proprietary know-how offers it a bonus over most, if not all, of its rivals. The corporate ought to see a direct and long-lasting profit from the AIM Act.

In my estimation, the AIM Act can probably develop the refrigerant reclamation market by as a lot as 20% per yr. The vary of potential outcomes is huge and unsure, offering traders with increased confidence on this potential development to get forward of Hudson’s potential inflection level and obtain beneficiant funding returns if the thesis performs out.

Hudson’s reclamation companies present a gross margin of roughly 50%, considerably increased than its web refrigerant companies. Because the AIM Act continues to scale back HFC manufacturing, I anticipate to see HDSN obtain its $400m income goal in 2025 and I consider the corporate has the potential to maintain gross margins above its goal of 35%.

HDSN could also be an awesome funding alternative for affected person, long-term traders prepared to abdomen volatility.