GoodLifeStudio

Elevator Pitch

Hyatt Hotels Corporation (NYSE:H) is assigned a Hold investment rating.

Earlier, I touched on Hyatt’s growth prospects and valuation metrics in my January 23, 2024 article. With this latest write-up, I review H’s Q1 2024 financial performance and the company’s recent asset monetization moves.

On the positive side of things, Hyatt continues to monetize its assets and generate divestiture proceeds that can finance future growth investments. On the negative side of things, H’s first quarter EBITDA and earnings fell short of expectations, as the company’s profitability was hurt by an increase in salaries for specific markets. As such, I have a mixed view of H that translates into a Hold rating.

Q1 EBITDA And EPS Missed The Market’s Expectations

On May 9, 2024 before trading hours, Hyatt published an announcement disclosing its financial results for the first quarter of the year. The company’s Q1 2024 non-GAAP adjusted EBITDA and normalized EPS came in below the consensus forecasts.

H’s normalized EBITDA decreased by -6% YoY from $268 million for Q1 2023 to $252 million in Q1 2024. Its non-GAAP adjusted EBITDA for the most recent quarter turned out to be -17% below the sell side’s consensus EBITDA estimate of $303 million as per S&P Capital IQ data. Hyatt’s Q1 2024 non-GAAP adjusted EPS of $0.71 also missed the analysts’ consensus bottom line forecast of $0.95 by -25%.

A difficult base for comparison and timing issues were factors affecting Hyatt’s latest quarterly results. At its Q1 2024 earnings call, Hyatt explained that its recent quarterly performance was hurt by “difficult comparisons versus 2023, including lapping the Super Bowl”, and “the timing of Easter compared to 2023” that “negatively impacted group and business travel.”

However, it is worth noting that H’s first quarter EBITDA and EPS were also affected by inflationary cost pressures. In addition, the company has a pretty conservative view of its full-year operating profitability outlook.

As per S&P Capital IQ data, Hyatt’s normalized EBITDA margin contracted by -130 basis points YoY to 14.7% in Q1 2024, which was -310 basis points lower than the consensus projection of 17.8%. The company acknowledged at its first quarter earnings briefing that “increased wages in certain markets” had an unfavorable impact on its recent quarterly EBITDA. It is reasonable to assume that inflationary pressures had led to higher salaries and lower operating earnings for H in Q1 2024.

Looking forward, Hyatt emphasized at the company’s Q1 results briefing that “our expectations continue to be that we will achieve flat to moderate expansion (my emphasis) EBITDA “margins for the full year.”

In summary, it comes as a disappointment that H recorded an EBITDA miss for Q1 2024 and the company doesn’t anticipate significant profitability improvement in FY 2024.

Recent Asset Monetization Initiatives Draw Attention

H has been actively monetizing some of the company’s assets in recent times. I view this as a positive development, as the proceeds received from asset monetization can be allocated to new growth investments.

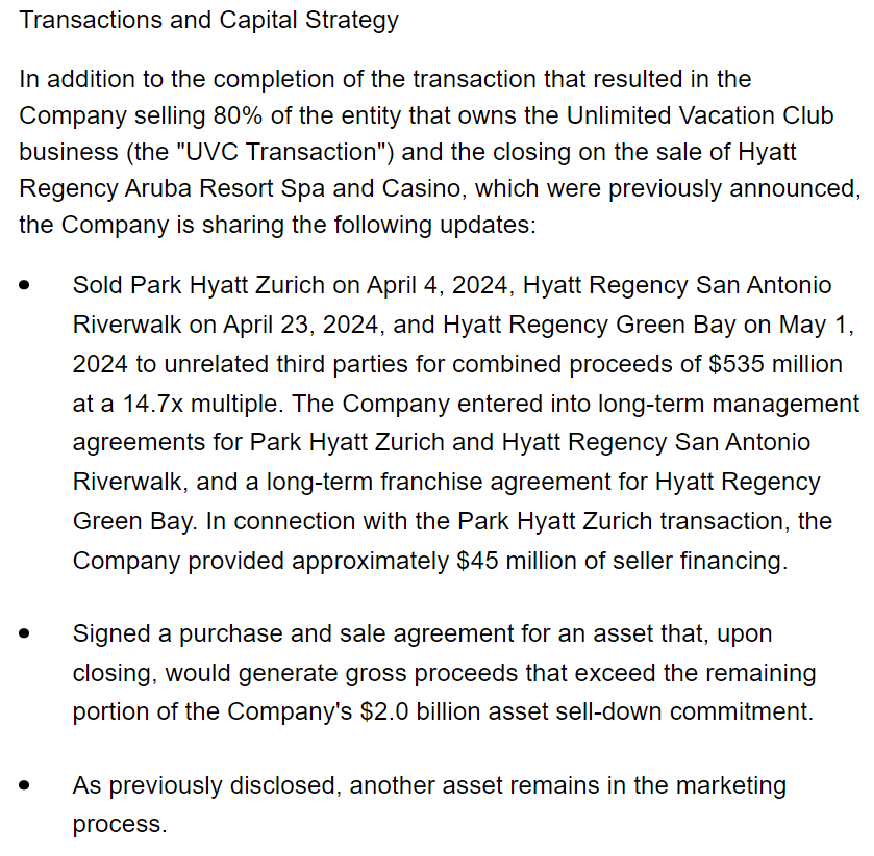

In its May 9, 2024 Q1 results announcement, Hyatt revealed that its equity interest in Juniper Hotels, an “unconsolidated hospitality ventures in India”, was reduced from 50.0% to 38.8% following Juniper’s public listing in February. H’s other recent asset monetization moves are detailed in the chart presented below.

Hyatt’s Recent Asset Monetization Initiatives

Hyatt’s Q1 2024 Earnings Release

According to the company’s management commentary at the recent earnings call, H had set a goal of achieving $2 billion worth of divestment proceeds between late-2021 and end-2024. As of early-May this year, Hyatt had already generated $1.5 billion from its asset monetization moves in the past few years. This means that the company is on track to meet its $2 billion divestiture target by the end of this year.

In its investor presentation, H highlighted that it has $800 million of cash and investments and $1.5 billion of “revolver capacity available.” Hyatt’s future financial position is expected to be strengthened by further asset monetization moves as mentioned above. In other words, the company has the financial capacity to invest for future growth.

Hyatt indicated at the company’s Q1 2024 analyst briefing that “our capital allocation strategy has not changed” and noted that “we’re still prioritizing investing in the business.” A potential area of new growth investments is China. In my late-January write-up, I cited H’s management comments and disclosures by other hospitality companies suggesting that China’s “branded hotel penetration rate” is pretty low vis-a-vis other developed markets.

In a nutshell, I like the fact that H continues to engage in asset monetization so as to free up excess capital for reinvestment.

Final Thoughts

H’s shares seem to be trading at a fair valuation based on a historical comparison. In the past two years, Hyatt has traded between 11.4 times and 17.8 times consensus next twelve months’ EV/EBITDA as per S&P Capital IQ data. This is equivalent to a mid-point EV/EBITDA metric of 14.6 times (sum of 11.4 and 17.8 divided by 2), which is close to Hyatt’s current EV/EBITDA multiple of 14.5 times.

There are positives (asset monetization progress) and negatives (earnings miss) associated with H’s recent disclosures. In addition, the stock appears to be reasonably valued as highlighted above. Therefore, I have left my existing Hold rating for Hyatt unchanged.