JulPo

Fundamental Thesis & Background

The aim of this text is to judge the VanEck Vectors Excessive Yield Municipal Index ETF (BATS:HYD) as an funding choice at its present market value. The fund’s objective is to “track the overall performance of the U.S.-dollar-denominated, high-yield, long-term, tax-exempt bond market”.

This has been an affordable performer in 2023, albeit not giving a lot in the best way of “alpha”. However I noticed this as an honest technique to attain for yield over the leveraged CEF choices – which is usually my most well-liked technique to play the muni sector. In regular years this permits me to seize a better revenue stream whereas nonetheless holding IG-rated bonds – as a result of the leverage amplifies the yield. However as my followers know, I used to be burned in 2022 on leverage and did not need to make the identical mistake this yr. This led me to passive, excessive yield muni choices like HYD, which have provided a modest optimistic achieve this calendar yr:

Fund Efficiency (In search of Alpha)

Given this actuality I figured it was time to reassess HYD to see if it nonetheless warranted holding in my portfolio within the new yr. I imagine it does, and I’ll give the explanation why within the following evaluate.

The Caveat: This Is For People With Excessive Tax Charges

To begin this evaluate I need to spotlight a key level. That is that prime yield munis are particularly engaging for individuals who earn some huge cash and/or are in a excessive tax bracket. It is because there are a bunch of the way to earn revenue on this market – whether or not in munis or company bonds, or based mostly on one’s tolerance for decrease rated debt. Within the case of HYD, traders are exposing themselves to bonds which can be typically not rated or rated beneath funding grade high quality. This brings on credit score threat that readers want to pay attention to, one thing that’s nearly a moot level within the IG-rated realm (IG-rated munis hardly ever default). The identical can’t be mentioned for top yield munis.

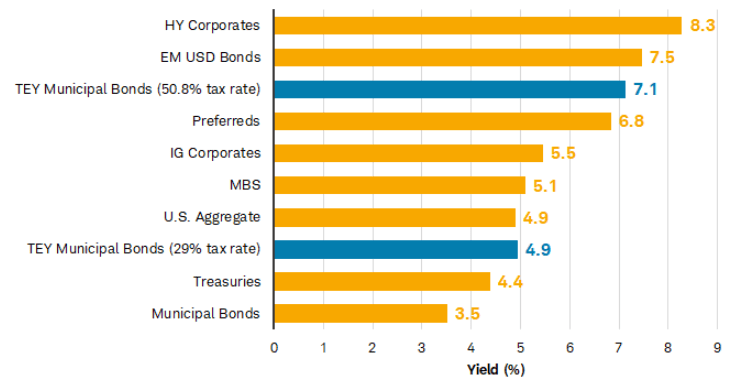

So, why would one need to tackle this threat? The reason being revenue – specifically after-tax revenue. Once we take a look at the fixed-income panorama proper now, we see that yields (and due to this fact revenue streams) are up throughout the board. Munis look engaging based mostly on their very own historic norms, however the identical might be mentioned for different sectors like treasuries and corporates. In actual fact, on the subject of munis, these in decrease tax brackets may very well be higher off reaching for yield elsewhere. However for these within the highest of brackets, muni’s tax-equivalent yields (TEY) are proper close to the highest of the revenue ladder:

Present Yields (By Sector) (S&P International)

What this reveals me is that traders can earn an equal yield in munis that they’d be getting in to rising market bonds or excessive yield corporates. Whereas there may be nothing inherently “wrong” with these choices, I personally want munis to those choices. On the very least, readers can diversify by this selection in the event that they have already got publicity to the opposite choices.

However once more, because the graphic clearly reveals, for sure traders in decrease tax brackets, the benefit of munis isn’t fairly as pronounced. So this actually depends upon every particular person’s circumstances and the way comfy they’re with different larger yielding sectors. For me, as a working skilled in a dual-income family, the advantages of muni’s tax benefits are clear. For my followers, this might be a giant benefit, or not, but when so I might counsel consideration of this sector.

Bonds To Profit From Declining Inflation

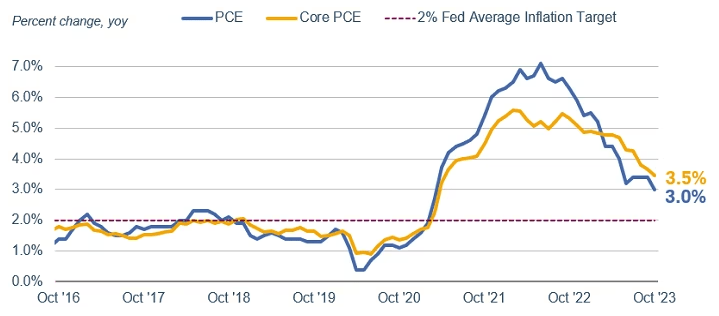

My subsequent level considers why bonds extra broadly are a great choice right here. The rationale is straightforward: inflation has been declining and that’s permitting central banks (such because the Fed) to carry off on extra rate of interest hikes. Since bonds transfer inversely with charges, the tip of a fee climbing path may be very favorable for bonds. Luckily, the sharpness within the decline in inflation (not less than domestically), suggests to me that the Fed has loads of help for taking a extra dovish strategy:

Inflation Figures (Charles Schwab)

The takeaway right here for me is that now could be positively a great time to start accumulating bonds or including to fixed-income positions. The development of decrease inflation has been constant sufficient now that I’m assured it is not going to immediately spike within the months forward. Bonds are hardly ever this engaging, from a historic yield perspective, so I imagine readers ought to be contemplating them in the intervening time. This goes for munis – and HYD by extension – in addition to a bunch of different choices which can be on the market.

HYD Is Not “Risk-Free”

It ought to be clear I see a powerful case for fixed-income, munis as a complete, and HYD as a technique to amplify one’s revenue stream. I see this as a sector that could be a sensible technique to tackle additional credit score threat as a result of defaults are typically uncommon. However this does not imply readers ought to blindly ignore the dangers. There are dangers with any funding, and HYD is not any exception.

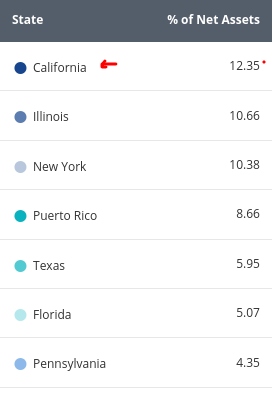

Chief amongst my considerations is the state publicity represented on this fund. The same old suspects high the checklist, with California because the state with the very best portfolio weighting, as proven beneath:

HYD’s State Publicity (VanEck)

That is particularly related contemplating the headlines hitting the market proper now. Simply over the previous week, California made some waves by the announcement that the state is dealing with an enormous price range deficit:

Current Headline – California Funds (AP Information)

This is because of a bunch of causes: a rise within the minimal wage for healthcare works, continued tax breaks for sure industries, a lack of Tech jobs (a lot of that are excessive paying), and a declining inventory market in 2022 that disproportionately hurts California’s tax revenues given the state’s over-reliance on taxing its wealthiest residents. All of this added as much as a backdrop that meant the state is planning to spend greater than it’s taking in. That is an all-too-common downside in our nation from many state governments and the nationwide authorities.

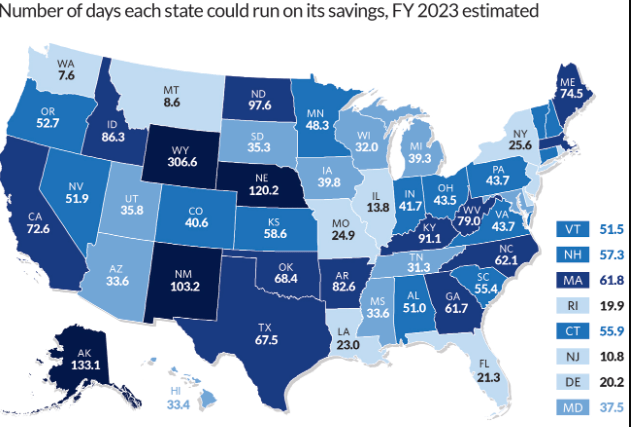

The excellent news is that California can survive this deficit within the short-term. That is because of the state having a big “rainy day” fund – which is basically money reserves. Many states throughout the nation noticed their balances explode as a result of federal stimulus from Covid-19. Whereas this was pretty widespread, California was (and is) in a stronger place than most, given what number of days it might operate simply on reserves alone:

Variety of Days State Might Perform On Financial savings (Pew Analysis)

The conclusion I’m drawing right here is to not be alarmist about current headlines. Is that this a threat? Undoubtedly – an one that’s elevated in comparison with the prior couple of years. However California was in good fiscal form getting in to this growth, so it stands to cause they’ve time to determine this out.

It could require some troublesome selections to be made down the road, and we most likely all have are personal opinions on whether or not the California legislature goes to have the ability to make these selections. However within the quick time period, this stays a “watch” merchandise and never one that’s large enough to maintain me out of a diversified fund like HYD.

Hospital Income Bonds An Alternative?

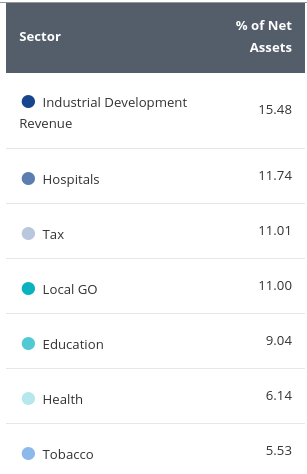

My last subject of dialogue considerations the sector publicity inside HYD. One space particularly that’s prone to increase eyebrows is the Hospital Income weighting:

HYD’s Prime Sector Weightings (VanEck)

At 12%, this does not expose traders to an enormous diploma of threat – however it’s nonetheless notable sufficient that traders will need to be bullish on this publicity earlier than shopping for this fund. This may occasionally look like an attention-grabbing spot to be lengthy given all the issues hospitals and healthcare suppliers had from the pandemic. However the worst of these days are behind us, so a forward-looking view is what is required now.

With that mindset, there are two components I see supporting the logic of holding these bonds going ahead. One, provide has been pretty tight in 2023. This helps to maintain the costs of those bonds excessive – all different issues being equal – as a result of the market has not been flooded with new points:

Hospital Muni Bond Issuance (By Yr) (Bloomberg)

That is supportive of resilient pricing for bonds that make up a major a part of HYD’s holdings.

A second cause is that even with all of the challenges within the excessive yield nook of the debt market, munis nonetheless have a tendency to carry up very properly. Now we have seen pandemics come and go earlier than and hospitals proceed to symbolize a necessary a part of a developed world life-style. Native, state, and federal governments proceed to speculate and help these healthcare methods, and I do not see that altering.

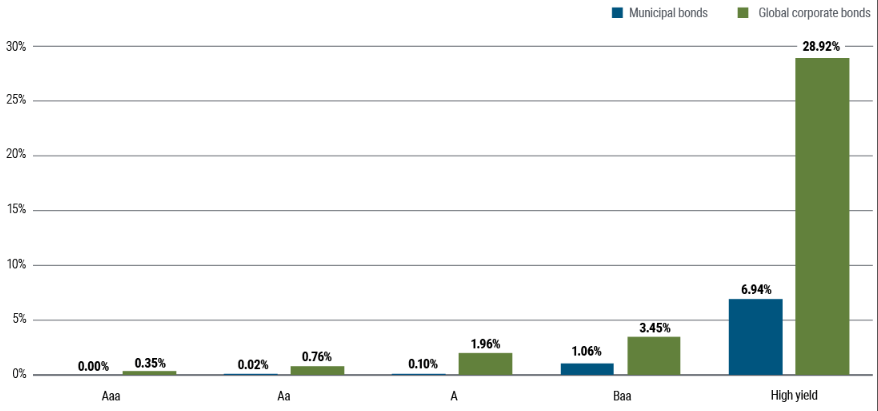

Because of this, defaults within the sector are typically uncommon. We all know this as a result of, collectively, excessive yield munis have a long-term common default fee beneath 7%. This compares extraordinarily favorably to the company bond sector:

Cumulative Default Charge (By Credit score Score) (Moody’s)

What I’m making an attempt to convey right here is that defaults for munis are comparatively low compared to company bonds whatever the sector and/or credit standing. I might nonetheless reiterate that traders want to watch this threat extra rigorously with HYD than with different muni choices. However the historic default charges, coupled with the low degree of provide for hospital-backed bonds, provides me consolation that it is a affordable place to tackle some threat.

Backside-line

Municipal bonds at present supply yields properly above what they’ve during the last decade, or extra. That is unlikely to final as averages have a manner of balancing out any short-term imbalance (which I see now within the fixed-income muni market). I’m waiting for the brand new yr with renewed optimism for muni bonds, however proceed to imagine passive ETFs and particular person points are one of the best wager for the sector, fairly than leveraged CEFs. The yield curve’s inversion presents a continued problem for funds that borrow to amplify the yield, so I believe taking place in credit score high quality is a greater play for the early phases of 2024.

In consequence, I might counsel traders in high-tax brackets particularly take a look at HYD. The fund is diversified by state and sector and gives a compelling tax-adjusted yield for these within the higher tax brackets. Additional, default charges for munis are decrease than for company bonds, even within the below-grade points. Subsequently, I really feel assured holding my “buy” score in place, and suggest to my followers that they offer this concept some thought going ahead.