JHVEPhoto

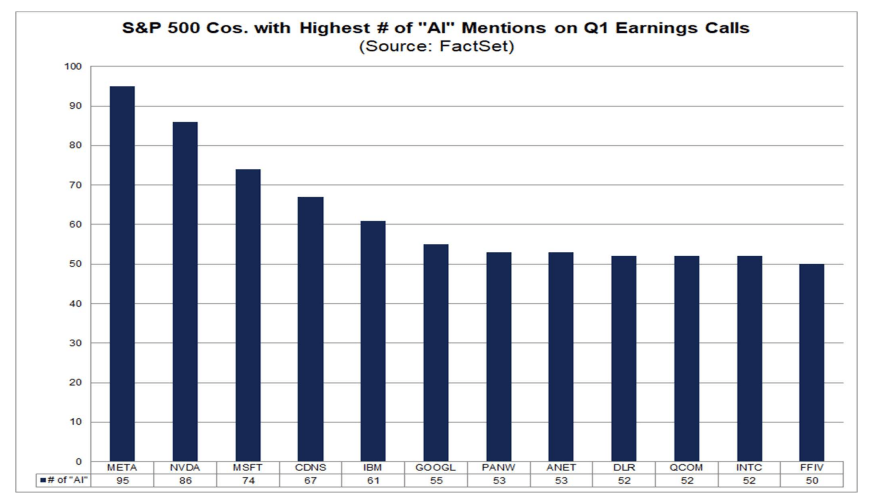

FactSet put out an interesting read last week on the state of corporate earnings and how AI has infiltrated the zeitgeist among executives, particularly for firms in the Information Technology sector. According to the report, a handful of S&P 500 firms mentioned “AI” at least 50 times in respective Q1 earnings calls. Coming in fifth position is International Business Machines Corporation (NYSE:IBM). AI is indeed a potential growth driver – and that’s seen in a few different partnerships detailed lately.

I am upgrading shares from a hold to a buy. I see the valuation premium has warranted today given strong free cash flow trends and the potential for EPS upside in the years ahead, though I do not see IBM as a tremendous bargain. What has turned more sanguine, though, is its momentum situation.

AI Mentioned Surge Across New & Old Tech

Factset

According to Bank of America Global Research, IBM is a leading provider of enterprise solutions, offering a broad portfolio of IT hardware, business, and IT services, and a full suite of software solutions. The company integrates its hardware products with its software and services offerings in order to provide high-value solutions. IBM is comprised of four major segments: Infrastructure, Consulting, Software, and Financing.

Back in April, IBM beat on the bottom line. Q1 non-GAAP EPS of $1.68 topped Wall Street’s consensus estimate of $1.59, though revenue of $14.46 billion, up 1.5% from year-ago levels, fell shy of expectations. The stock plunged 8% after the report, but later stabilized, holding its 200-day moving average, which I will detail later. While operating earnings were solid, the company had a generally soft start to 2024. Its Consulting unit was weak, while Software was strong. $1.9 billion of quarterly free cash flow was a solid print, and the management team maintained its target of $12 billion of free cash flow for FY 2024.

On the AI front, IBM was aggressive – last month, the firm said it planned to acquire HashiCorp, Inc. (HCP) for $6.4 billion to better its hybrid cloud and AI capabilities. With a defensive portfolio, high dividend yield, and nascent but intriguing AI exposure, I would not be surprised to see Big Blue catch a longer-term bid akin to what we have seen, for instance, in fellow legacy tech player Dell Technologies Inc. (DELL).

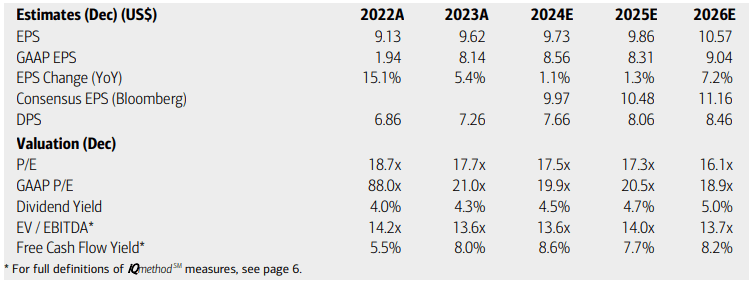

On valuation, analysts at BofA see earnings rising just 1% this year with continued modest profitability gains in the out year. By 2026, however, the firm is expected to grow EPS at a faster clip. The current Seeking Alpha consensus forecast shows steadier earnings growth, in the mid-single-digit range through 2026 while IBM’s top line is seen increasing in a 2% to 5% range.

Dividends, meanwhile, are forecast to rise above $8 annually by 2025, resulting in a high yield, potentially near 4%. Shares trade with a multiple that is about four turns cheaper than the broader market, but at a sizable premium to the company’s long-term average while its free cash flow yield is very high.

IBM: Earnings, Valuation, Dividend, Free Cash Flow Forecasts

BofA Global Research

With increasing free cash flow, a rising dividend, and EPS that could accelerate, the valuation picture has improved since last summer, in my view. If we apply an 18 multiple on $10.30 of normalized forward 12-month non-GAAP EPS, then shares should trade near $174. I assert that a P/E between IBM’s 5-year average and the broad market’s is warranted given the company’s improving growth and robust free cash flow trends.

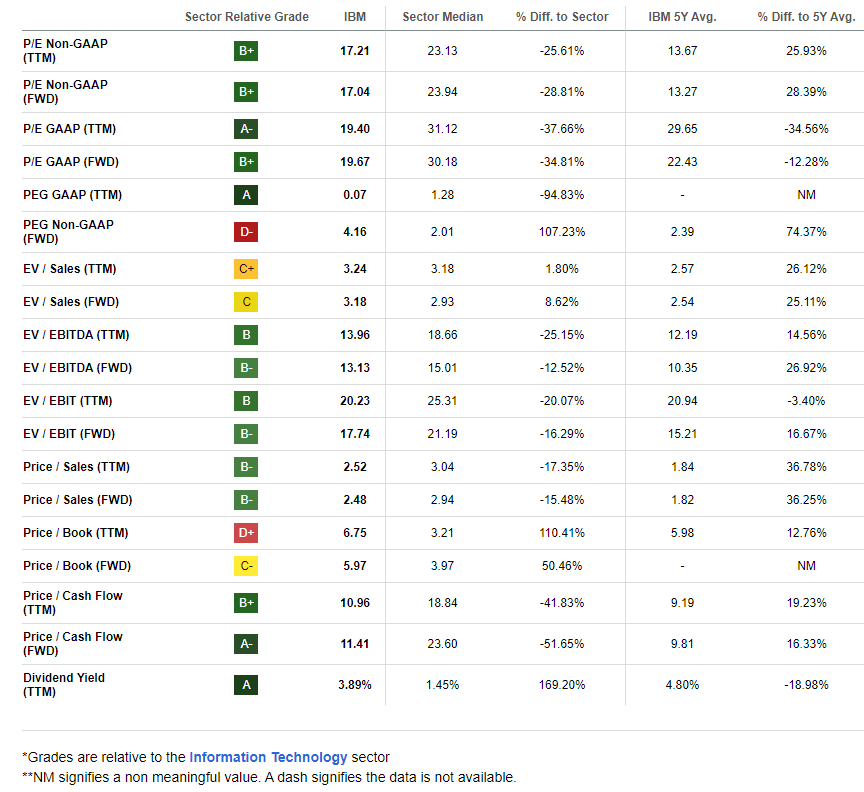

IBM: Attractive Nominal Valuation, High Dividend Yield

Seeking Alpha

Compared to its peers, IBM features an attractive valuation rating given the below-market multiple, though growth trends have been lackluster in recent quarters. But with top-notch profitability trends and much improved share-price momentum in the last three quarters, there’s reason for the bulls to get excited about Big Blue. Finally, sell-side earnings revisions have been weak in the last 90 days despite five consecutive bottom-line beats.

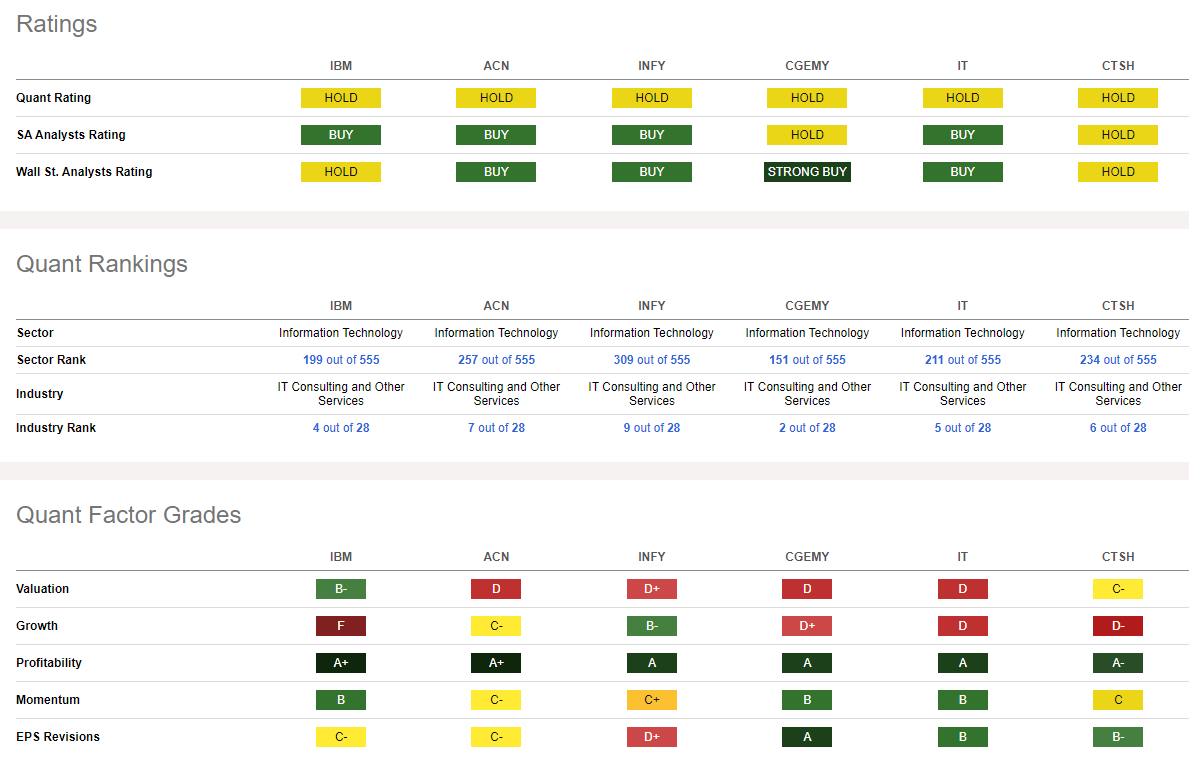

Competitor Analysis

Seeking Alpha

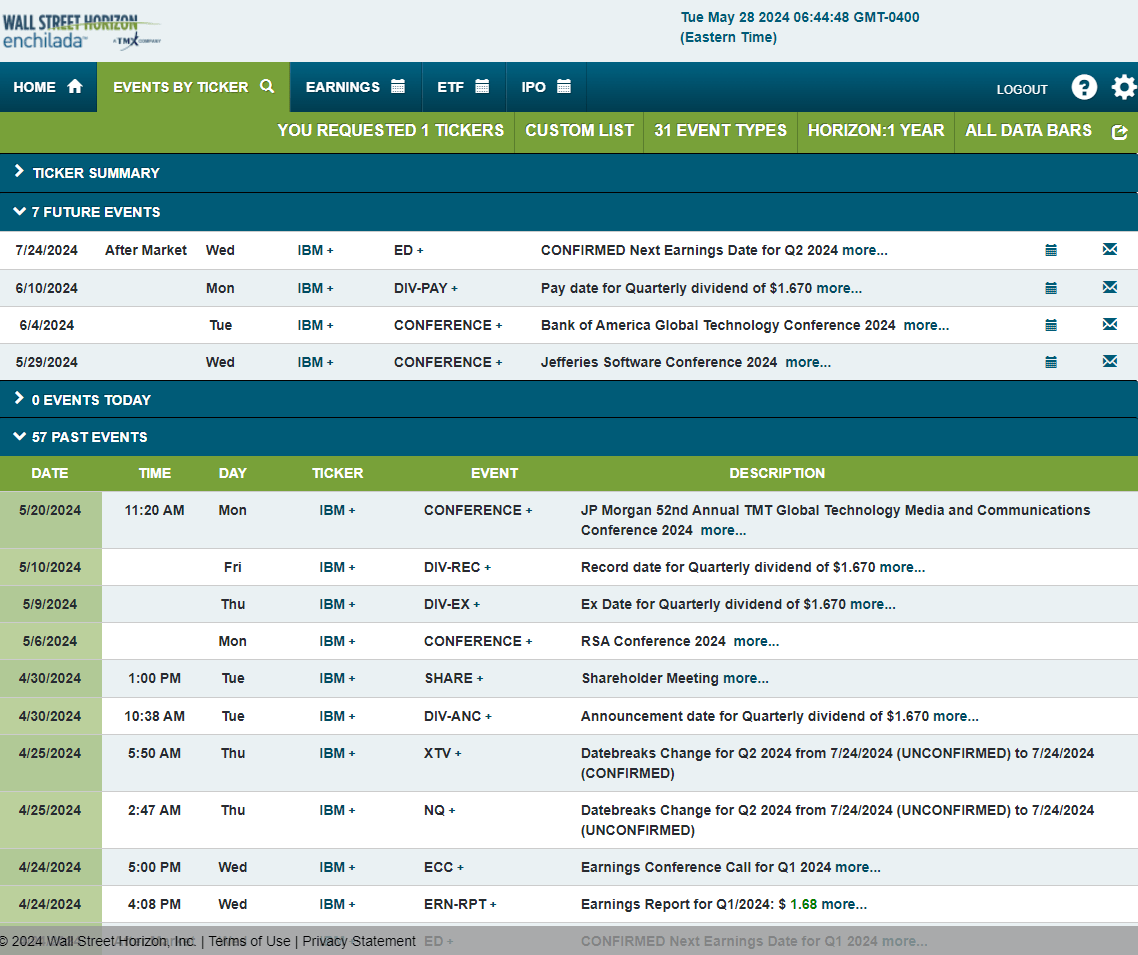

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q2 2024 earnings date of Wednesday, July 24. The company’s management team is also expected to present at a pair of industry conferences – one this week and the other in the first week of June. No other volatility catalysts are on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

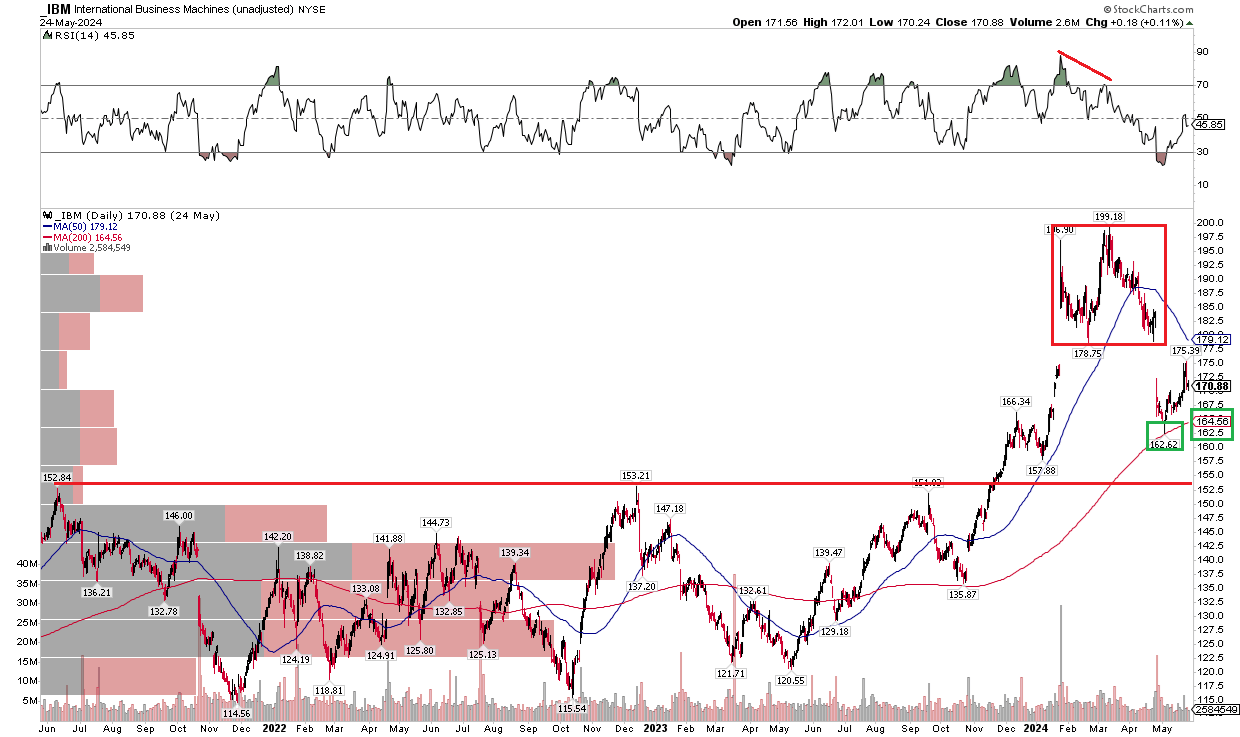

The Technical Take

While I do not see IBM as a steal of a deal in terms of valuation, the yield is compelling and its technical situation is much improved from last July. Notice in the graph below that shares broke out above a key resistance level which I pointed out last time. The $153 mark was finally busted through last December, and the stock was off to the races after that. IBM peaked at just under $200 after reaching nosebleed RSI levels. But then a bearish RSI momentum divergence took place, which turned out to be a harbinger of bearish price action. Shares drifted lower in advance of its Q1 earnings report in April, then gapped down after the profit update, with shares eventually tagging the long-term rising 200-day moving average.

But the bulls defended that spot, and the stock is now close to what I consider to be fair value. A bearish feature, however, is what appears to be an island reversal with comparable price gaps to the $180 level. I would like to see the stock rise through and hold above the earnings-related gap on improved RSI momentum. But with relatively few shares traded up to $200, there is not a whole lot of bearish overhead supply to be particularly worried about.

Overall, IBM’s above important support with a rising 200-day moving average despite some near-term technical risks.

IBM: Shares Break Out Above $153, Holding the 200dma

StockCharts.com

The Bottom Line

I am upgrading IBM from a hold to a buy. I see the stock close to fair value, but with its high dividend, robust free cash flow, and much-improved technical situation, shares look poised for higher prices.