Klaus Vedfelt

ETF Overview

iShares International Dividend Growth ETF (BATS:IGRO) owns a portfolio of international dividend growth stocks. About half of the fund’s portfolio are concentrated in Canada, Japan, and Switzerland. IGRO’s fund price has an inverse correlation to the U.S. treasury rate. Its fund price can also be impacted by currency exchange rates of different countries and can cause more volatility. IGRO also has a lower exposure to technology sector than its U.S. fund peer. This can limit its long-term return. Hence, we think investors may want to seek alternatives elsewhere.

YCharts

Fund Analysis

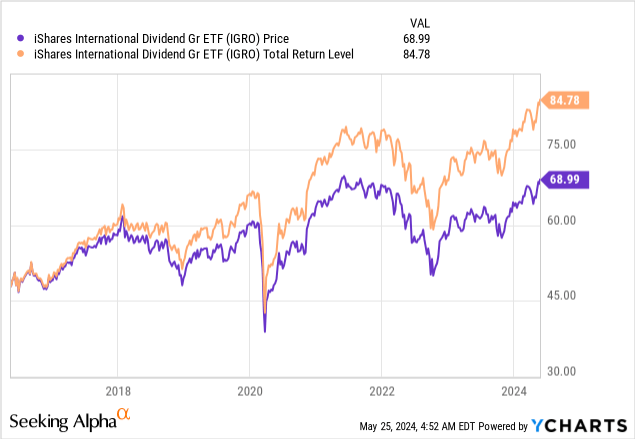

IGRO has finally near the peak of late 2021 again

Like many other funds, IGRO had a rough ride in the first 10 months of 2022. The fund has declined by about 26.5% during this time period, slightly higher than the S&P 500 index’s 24.8%. Fortunately, the fund has since recovered nearly all of its loss, and registered a return of 38.5% as of May 24, 2024. This return was good, but still lower than the S&P 500 index’s 48.1%.

Portfolio construction methodology

Let us now visit IGRO’s portfolio construction methodology. The portfolio is constructed by selecting stocks from the Morningstar Global Markets ex-US Index that meets the following criteria: (1) at least 5-years of uninterrupted annual dividend growth, and (2) a payout ratio of less than 75%. The selection method is sound in three ways. First, it focuses on dividend growth. Although the methodology of selecting stocks that have grown their dividends in the past 5-years does not necessarily ensure future growth, it ensures some level of consistency. Second, limiting the selection of stocks to those that have less than 75% of the payout ratio reduces the chance of any dividend cut. Third, this payout ratio below 75% also leaves some room for future dividend growth, especially in an economic recession.

YCharts

A portfolio of international dividend growth stocks

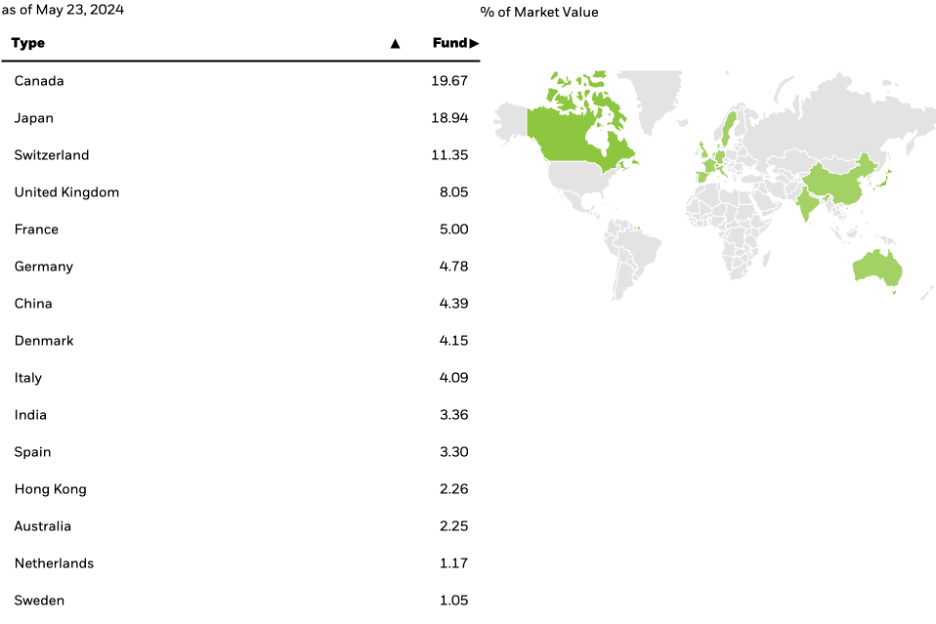

IGRO’s selection methodology has resulted in a portfolio of about 440 stocks from about 15 countries/regions. As can be seen from the chart, stocks from Canada, Japan and Switzerland represents about half of its portfolio.

iShares

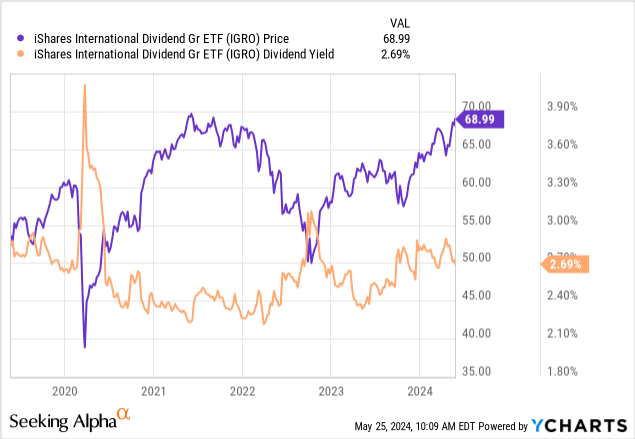

Given that these stocks are dividend growth stocks, not high dividend stocks, IGRO’s dividend yield has not been very impressive in the past. In fact, its dividend yield in the past 5 years has usually been in the range of 2.2% and 3.0% except in the initial breakout of the COVID-19 in 2020. Its current yield of 2.7% is slightly higher than its U.S. peer fund, iShares Core Dividend Growth ETF (DGRO), whose yield was about 2.4%.

YCharts

IGRO’s price performance can be impacted by Federal Reserve’s rate policy

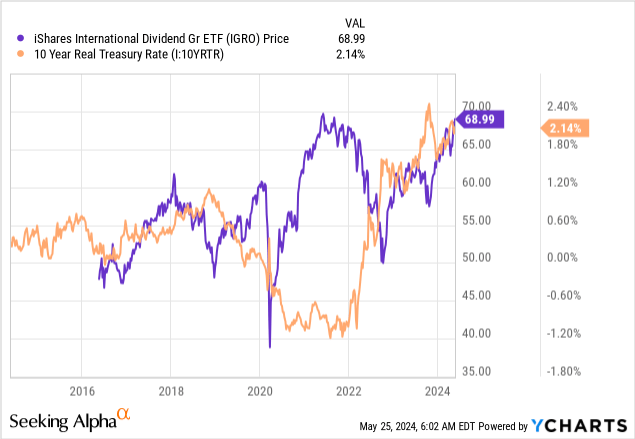

Given that IGRO’s portfolio include only international stocks, its fund price can be impacted by currency rates of different countries. In general, a strong U.S. dollar will typically compress its fund price and vice versa. The strength of the U.S. dollar is typically impacted by the U.S. treasury rate. As can be seen from the chart below, IGRO’s fund price typically has an inverse correlation to the U.S. treasury rate. When the Federal Reserve cut the rate in 2020, it impacted the treasury rate and IGRO’s fund price experienced a strong rally. On the other hand, when the Federal Reserve aggressively hiked the rate in 2022, IGRO’s fund price declined sharply.

YCharts

Looking forward, we are likely already at the peak or near the peak of this rate hike cycle. However, given the fact that the battle against inflation is far from over, and inflation has the tendency to become a self-fulfilling prophecy, the Federal Reserve may need to keep the rate elevated for a lengthy period of time. Therefore, in our opinion, it is unlikely that the Federal Reserve will lower the rate any time soon. Hence, we do not expect any tailwind from the Federal Reserve to happen in the near-term.

IGRO can decline more than its U.S. peers

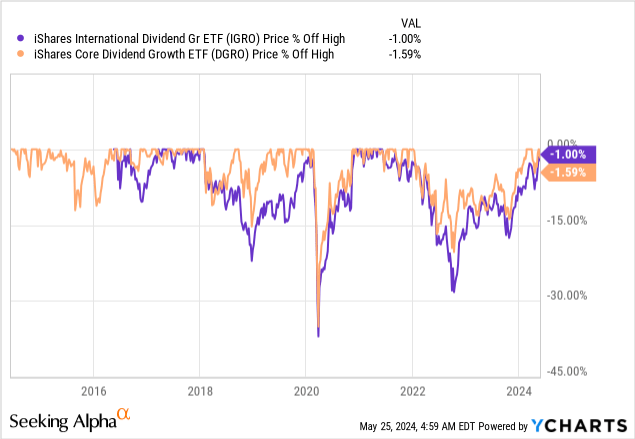

Since IGRO’s fund price can be impacted by currency exchange rate, its fund price can be more volatile than its U.S. peer fund, DGRO. In fact, IGRO’s 5-year average beta of 0.92 is higher than DGRO’s 0.83. For reader’s information, beta is a measure of the fund’s volatility in relation to the overall market. Not only does IGRO have higher volatility, it tends to decline much more than DGRO in a bear market. As can be seen from the chart below, IGRO’s fund price has a much higher degree of decline in the initial outbreak of COVID-19 in 2020, and during the bear’s market in 2022 than DGRO.

YCharts

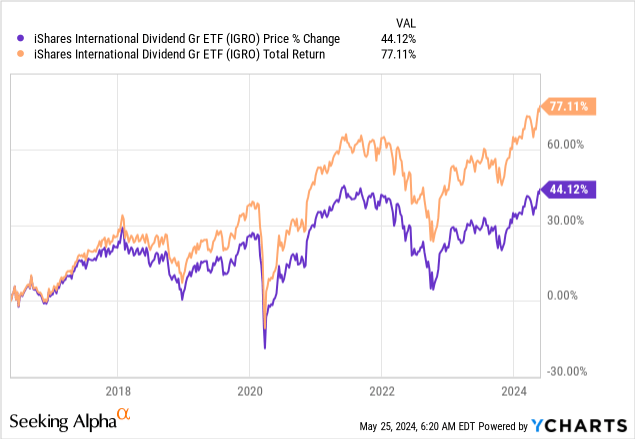

Not attractive relative to its U.S. peer

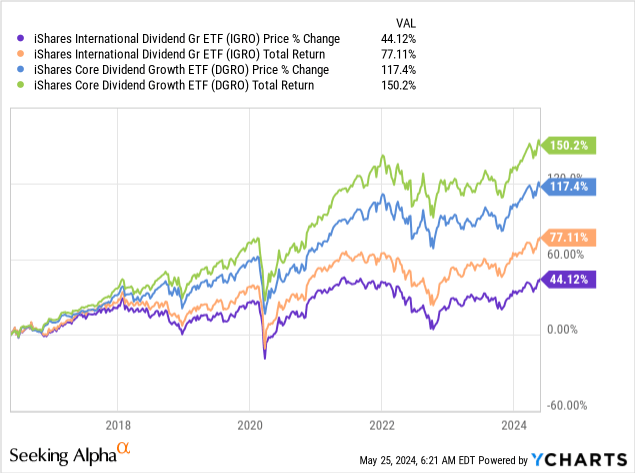

Besides higher declines in the past, it has a much lower return than DGRO in the past. As can be seen from the chart below, it has delivered a total return and price return of 77.1% and 44.1% respectively since its inception in May 2016. This is much lower than DGRO’s total return and price return of 150.2% and 117.4% respectively.

YCharts

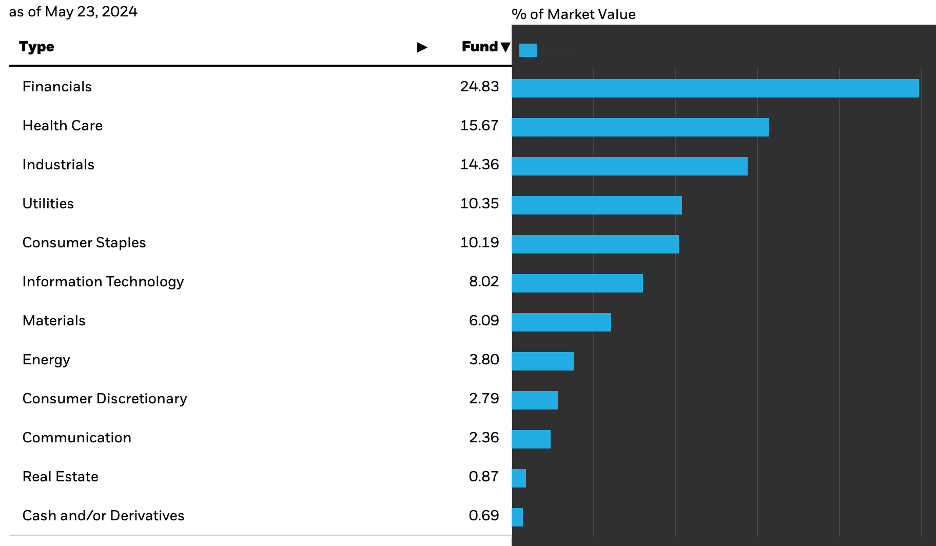

There are two reasons why we think IGRO underperformed DGRO. First, IGRO’s exposure to growth sectors such as technology sector is quite limited. As can be seen from the chart below, technology sector only represents about 8.0% of its total portfolio. In contrast, this sector represents about 17.0% of DGRO’s portfolio.

iShares

Another reason we think IGRO trailed its U.S. peer fund, DGRO, is because most stocks in IGRO’s portfolio are not multinational enterprises. The majority of them only concentrate in one or a few markets. This is quite different than DGRO’s portfolio. Although stocks in DGRO’s portfolio are U.S. stocks, the majority of them are multinational enterprises. In other words, these U.S. stocks have businesses in most major markets in the world. This is evident in the top holdings of DGRO’s portfolio. For example, Microsoft (MSFT) and Apple (AAPL), DGRO’s top two holdings, are much more “international” than most, if not all of the stocks in IGRO’s portfolio. Hence, these U.S. dividend growth stocks have better growth potential than IGRO’s international dividend growth stocks.

Investor Takeaway

Our analysis shows that IGRO may not be the best place to invest as it does not provide better return than its U.S. peer fund, and it can decline more in a bear market too. Therefore, we think investors should seek other funds instead.

Additional Disclosure: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.