sanjeri

Corbus Prescription drugs Holdings, Inc. (NASDAQ:CRBP) is a biotech inventory for buyers looking for to realize oncology publicity. Their flagship analysis undertaking is CRB-701, a Section 1 drug that targets Nectin-4-positive strong tumors. CRBP additionally has different analysis initiatives that might be profitable, however all of them are nonetheless of their levels and largely unproven.

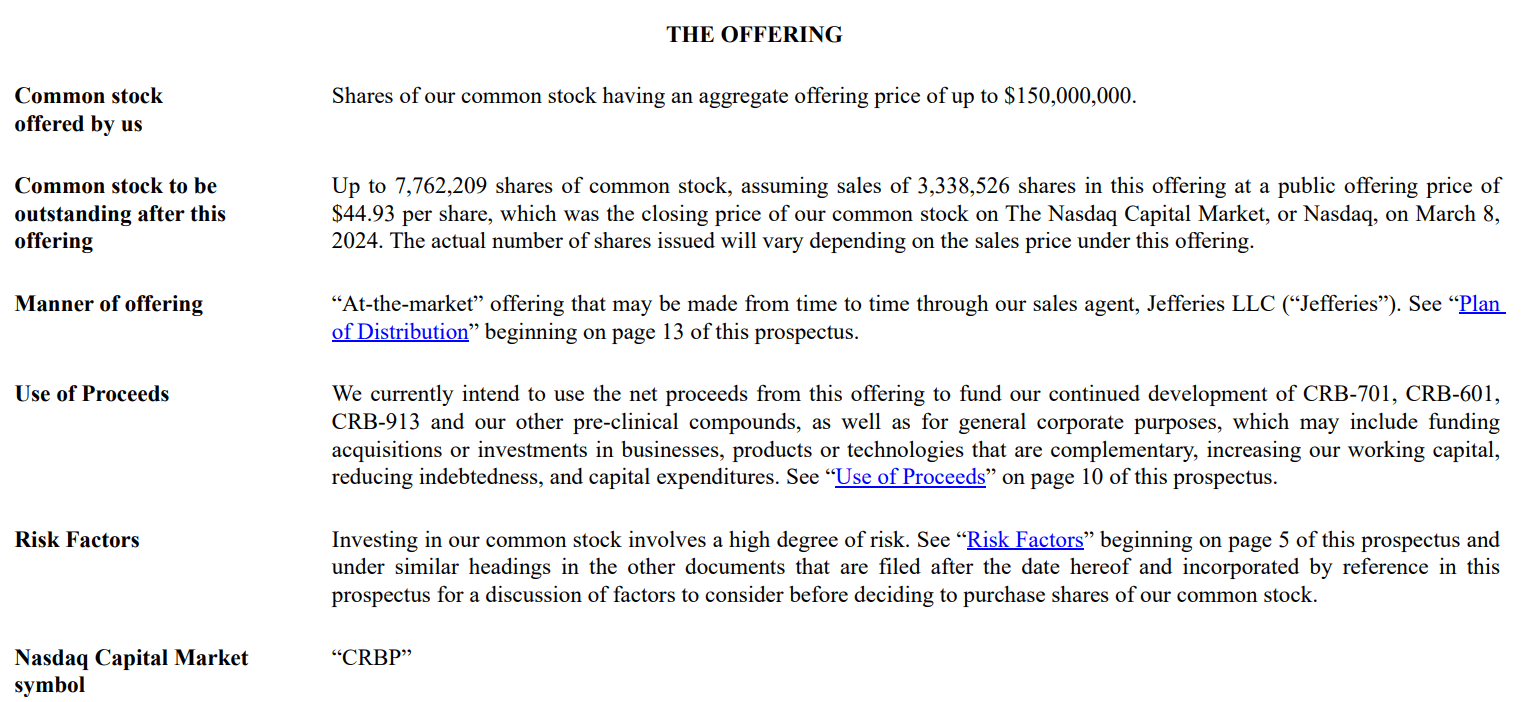

From a monetary perspective, CRBP is working low on funds, with lower than a yr of money runway. Nevertheless, the corporate lately filed with the SEC to boost as much as $300.0 million in further funds. This may doubtless trigger dilution for buyers and burden the balance sheet with extra debt.

Total, the underlying analysis is thrilling. Nonetheless, from an funding perspective, I believe Corbus Prescription drugs Holdings, Inc. inventory is a “Hold” till we get extra tangible medical trial knowledge corroborating its potential as a result of oncology has notably low odds of FDA approval.

A Guess On Oncology: Enterprise Overview

Corbus Prescription drugs is a clinical-stage biopharmaceutical firm situated in Norwood, Massachusetts. It was based in 2009 and is concentrated on precision oncology, weight problems, and associated circumstances. Immediately, CRBP is generally a guess on the corporate’s capacity to safe a profitable oncology area of interest, primarily by means of its flagship analysis IP, CRB-701. CRBP is on the pre-revenue stage, with no foreseeable income era sources for the close to time period. Furthermore, their newest 10-K report signifies that CRB-701 stays in Section 1 trials. This undertaking reveals promising early knowledge, however its early levels make CRBP an inherently speculative funding.

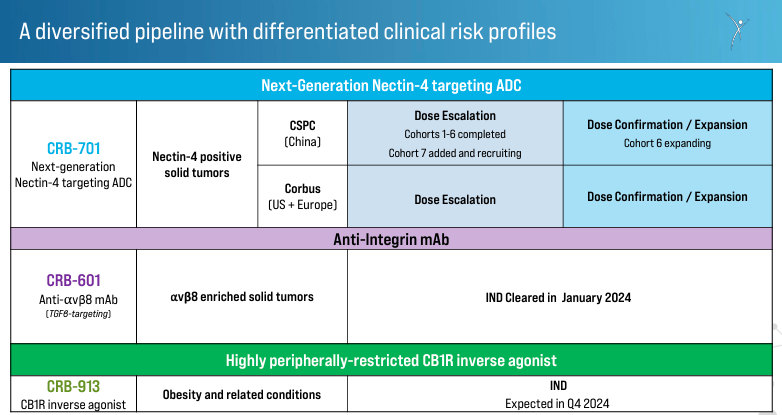

Supply: Company Presentation. March 28, 2024.

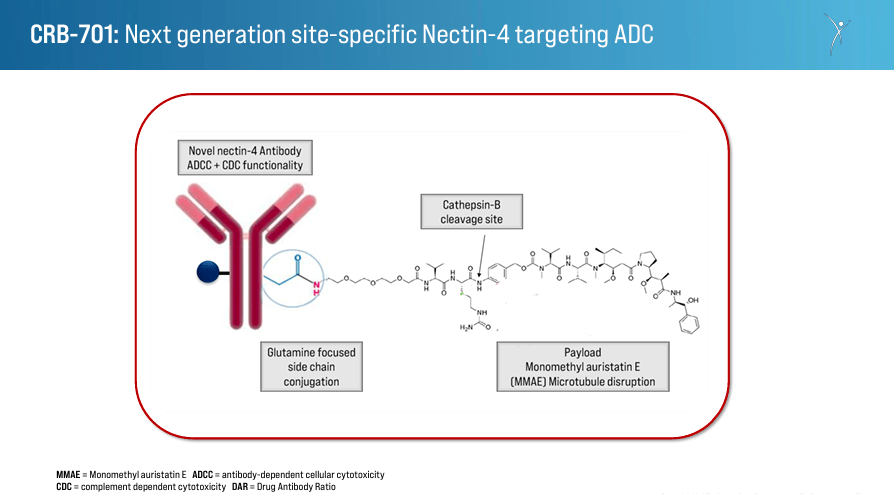

CRBP encompasses two approaches to most cancers remedies directed at completely different mechanisms of malign cell proliferation: 1) Subsequent-Technology Nectin-4 Antibody Drug Conjugate [ADC], and a pair of) Monoclonal Antibodies Concentrating on Integrins to Inhibit TGFβ Activation. The primary one makes use of an antibody-drug conjugate focusing on Nectin-4, a protein discovered on the most cancers cells’ surfaces. ADCs are extremely particular in delivering a cytotoxic agent to kill most cancers cells. By focusing on Nectin-4, this ADC reduces the affect in regular cells, diminishing unintended effects and eliminating most cancers cells. This remedy’s efficacy is enhanced in comparison with earlier ADCs, so it’s a promising differentiator for CRBP’s IP.

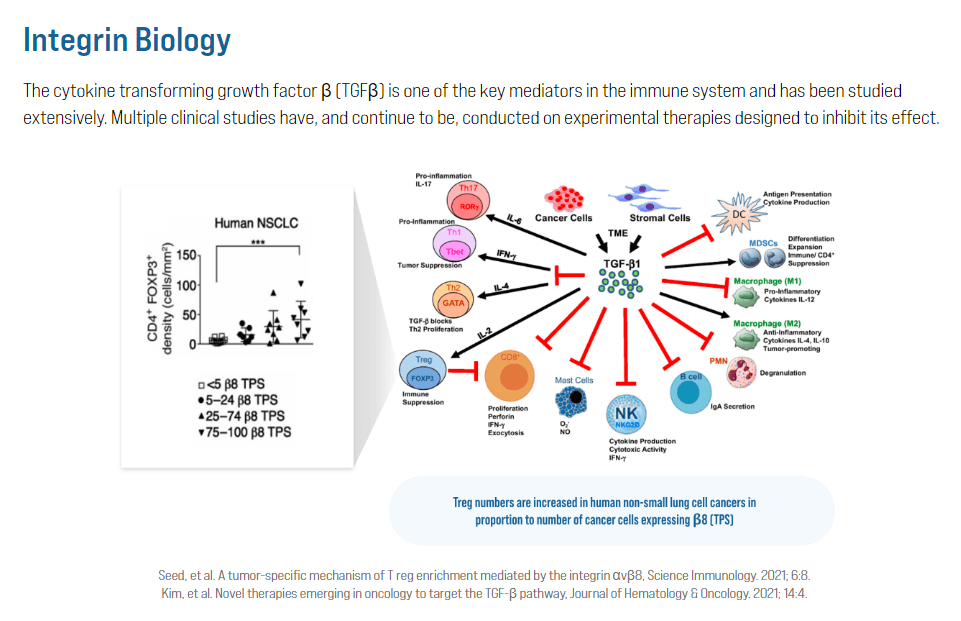

The second method with monoclonal antibodies blocks integrins that activate the Remodeling Progress Issue Beta [TGFβ]. This protein promotes tumor progress and suppresses immune response towards most cancers. By inhibiting integrins’ perform, these monoclonal antibodies forestall the activation of TGFβ, stopping most cancers development and enhancing the immune system towards the tumors.

Furthermore, CRBP’s improvement pipeline consists of the drug candidate CRB-701, which targets Nectin-4-positive strong tumors. Nectin-4 is usually overexpressed in varied varieties of strong tumors, together with bladder, breast, and pancreatic cancers. By particularly focusing on Nectin-4, CRB-701 has the potential to ship its cytotoxic payload on to most cancers cells whereas minimizing harm to wholesome cells. This implies fewer unintended effects and improved efficacy in comparison with conventional chemotherapy. Corbus developed this remedy for the U.S. and Europe, and it’s in section 1 of the medical trials. The primary affected person In [FPI] is scheduled for Q1 2024, with plans to enter Q2 2024 with dose escalation and Q3 2024 with dose affirmation/enlargement. CRBP collaborates with CSPC Pharmaceutical Group Restricted to develop and distribute this remedy in China, the place the drug is within the dose-escalation section.

It’s price noting that whereas CRB-701 is CRBP’s flagship product, the corporate additionally has CRB_601, which was accepted for medical trials in January 2024. It’s an anti-αvβ8 monoclonal antibody [mAb] focusing on TGFβ-signaling. The therapy is indicated for strong tumors with a excessive presence of the αvβ8 integrin.

Supply: Corbus Prescription drugs web site.

Moreover, CRBP’s product pipeline additionally consists of CRB-913, a peripherally restricted cannabinoid kind 1 receptor [CB1R] inverse agonist. This drug can bind to CB1R, which is said to vitality stability and metabolism, and acts outdoors the central nervous system to dam the exercise of the receptor that promotes urge for food. Thus, inhibiting this receptor induces weight reduction, helpful in circumstances like weight problems and associated problems. The Investigational New Drug [IND] software is anticipated in This fall 2024, which, if accepted, could be a big milestone for CRBP as it might additional validate its general IP portfolio.

From Setback to Revival: Corbus’s Pivot to Precision Oncology

However, in 2021, CRBP confronted a setback with Lenabasum for dermatomyositis, failing to fulfill its major endpoint in section 3. Consequently, Corbus’s inventory worth considerably dropped that yr. In response to this problem, the corporate modified its focus to precision oncology and weight problems remedies. That is a part of biotech investments, as not each drug will get FDA approval. Nevertheless, this specific setback is necessary to think about earlier than investing in CRBP, because it reveals that analysis progress isn’t assured, even when it reaches the ultimate FDA approval levels.

Supply: Company Presentation. March 28, 2024.

In distinction, CRBP’s newer CRB-701 drug candidate offered promising section 1 dose escalation research outcomes. That is basically a pivot from Lenabasum to a brand new IP, which appears to have been welcomed by the market to some extent. The shares rallied in early 2024 in response to this pivot, which has yielded favorable knowledge.

To this point, early medical trial knowledge from the research, offered on the 2024 ASCO GU symposium, confirmed a 43% goal response fee and a 71% illness management fee at therapeutically related doses for sufferers with Nectin-4 constructive tumors with out dose-limiting toxicities on the highest dose ranges examined. There have been no studies of peripheral neuropathy or pores and skin rash, frequent antagonistic results of comparable medication. Moreover, the drug had promising pharmacokinetic profiles, suggesting that it may very well be given much less steadily (each three weeks) and nonetheless keep efficient ranges within the bloodstream.

The constructive outcomes for CRB-701, which can provide advantages over present remedies, revived investor curiosity and market confidence in the way forward for CRBP.

Dilution & Too Early to Inform: Valuation Evaluation

From a valuation perspective, CRBP stays a comparatively small biotech firm, buying and selling at roughly $390.5 million market cap. Its stability sheet holds $20.9 million in money and equivalents towards $20.9 million in whole debt. This implies the corporate has the identical money and debt in the present day.

Furthermore, its cash flow assertion, I estimate its newest quarterly money burn was about $6.0 million, which annualized implies a yearly money burn of roughly $24.0 million. I obtained that determine by including the latest quarterly CFOs and Web CAPEX, then annualizing them. Thus, I calculate a money runway of roughly 0.87 years, which is regarding because it signifies that the corporate will want further financing within the close to time period.

Supply: CRBP, Kind S-3 Submitting.

Consequently, it’s unsurprising that the corporate recently filed with the SEC for capital elevating functions. CRBP seems to be to boost as much as $300.0 million in further funds by means of a mixture of fairness, most well-liked inventory, monetary derivatives, and debt. The funds will likely be primarily used for persevering with their analysis initiatives (ostensibly CRB-701 being the primary focus) and different normal company wants. The phrases are fairly normal and versatile for CRBP, which is frequent for this submitting kind. It basically permits the corporate to boost capital as wanted, and dilution would possibly happen if it’s carried out by means of fairness.

Nevertheless, most well-liked inventory and debt wouldn’t essentially be as dilutive instantly. I consider $300.0 million could be greater than sufficient to finance the corporate’s analysis efforts for the foreseeable future, as that may suggest roughly 12.5 years of money runway if raised absolutely in the present day.

However, for the reason that firm’s market cap stays comparatively small, a $300.0 million inventory increase would dilute present shareholders significantly. So, it’s a threat price contemplating earlier than investing within the shares. I doubt they’ll do it , and I anticipate them to make use of a mixture of fairness and debt.

Supply: American Council on Science and Well being.

Moreover, what buyers purchase in the present day is actually CRB-701, which is CRBP’s predominant worth driver. This analysis stays in Section 1, however it has acquired IND clearance from the FDA and began medical testing in Q1 2024. The FDA’s IND clearance is essential, because it reveals regulators really feel comfy with human testing for this drug. Though it’s nonetheless early, I consider this reveals a slight constructive angle in direction of CRB-701, which is an efficient omen general.

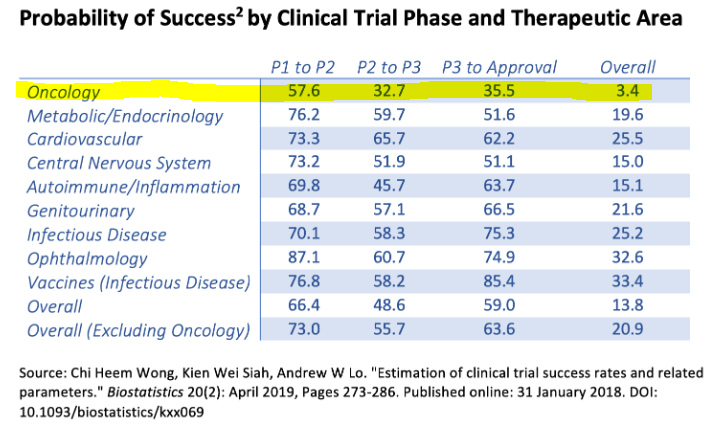

However, the highway to an eventual FDA approval is lengthy and unsure. For context, oncology medication often have a few 57.6% odds of constructing it by means of Section 1 into Section 2 trials. And general, the percentages of going from Section 1 to an eventual FDA approval are fairly slim, at simply 3.4%. For sensible functions, I believe it’s doubtless that CRBP will get to Section 2 with CRB-701, which may very well be a welcome catalyst for the inventory. But, past that, that is nonetheless extremely speculative.

Moreover, CRBP does have CRB-601 and CRB-913, that are each promising in their very own proper. Nevertheless, these analysis initiatives are simply of their starting levels. CRB-601 ought to begin the primary affected person enrollment in the summertime of 2024, a big milestone. CRB-913 is aiming for its IND submitting by late 2024 as effectively. Nevertheless, these initiatives are nonetheless largely experimental, and I wouldn’t contemplate them vital worth drivers but.

So, assuming that CRBP will doubtless dilute shareholders within the close to time period and its IP continues to be fairly undercooked, I believe it’s inappropriate to fee it a “Buy” simply but. I consider CRBP’s extremely speculative nature may repay ultimately, however it’s prudent to stay cautious till we get extra concrete trial knowledge outcomes. Therefore, I fee the inventory a “Hold” for now, however it’s a good addition to your watch record for the catalysts I’ve talked about.

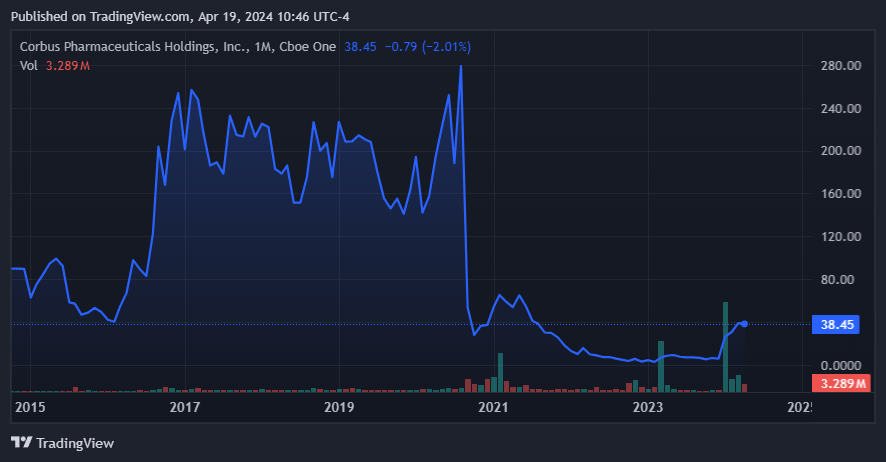

Supply: TradingView.

Undercooked: Conclusion

CRBP is a promising biotech within the oncology sector, notably with its flagship analysis undertaking, CRB-701. CRBP additionally has further initiatives in its pipeline, however they’re nonetheless within the very early levels. Furthermore, the corporate’s stability sheet wants to boost further funds to finance its analysis efforts, which can doubtless dilute shareholders and burden the stability sheet with debt.

So, on stability, I consider that the inventory’s risk-reward profile isn’t compelling sufficient to justify an funding. Nevertheless, I believe Corbus Prescription drugs Holdings, Inc. inventory is price watching sooner or later as a result of if its IP progresses as anticipated, the upside potential may very well be substantial. However for now, I believe it’s a “Hold.”