marcoventuriniautieri/E+ via Getty Images

The last time I reviewed Information Services Corporation’s (TSX:ISV:CA, OTCPK:IRMTF) was in January, when I noted that the company’s Q3/2023 financial performance was notably weak due to increased interest expenses from $150 million in debts taken on to finance the renewal of the Saskatchewan land registry contract. At the time, company management was guiding to better future earnings as the company had instituted price increases in its land registry services that will flow through to future results.

So far, the company’s results are playing out just like how management is guiding, with Q1/24 revenues increasing by 15% YoY and adj. EBITDA surging by 34% YoY.

Despite a strong share performance, ISV’s valuation multiple has gotten cheaper as adj. EBITDA has grown faster than the share price. I continue to rate ISV a buy and look forward to future updates from the company as it embarks on an ambitious plan to double the company’s size over the coming 5 years.

(Author’s note, financial figures in this article are in Canadian dollars)

Brief Company Overview

Since Information Services Corp. (“ISV”) is not a well-covered company, I believe readers may benefit from a brief recap of the company’s business.

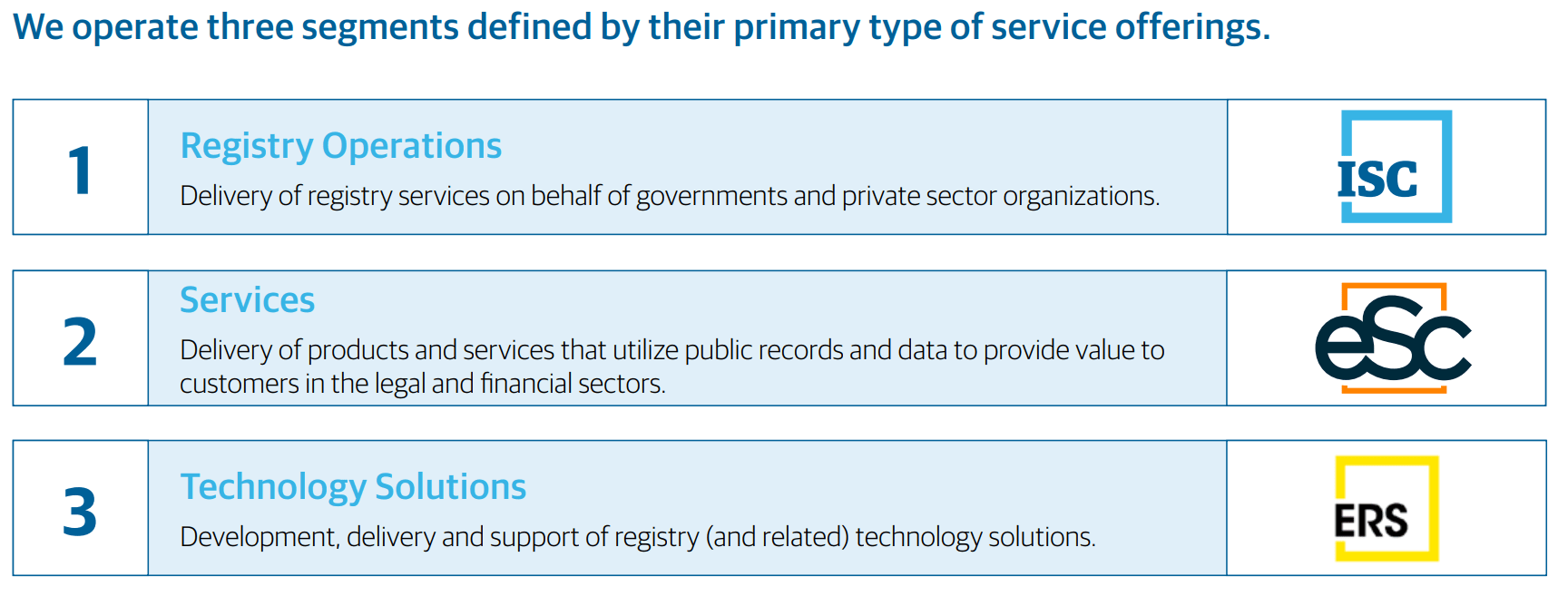

ISV primarily provides registry and information management services to governments and private entities. The company is structured into 3 business segments: Registry Operations provide registry services on behalf of governments and private sector organizations; Services deliver products and services using public records and data to customers in the legal and financial sectors; and Technology Solutions develop, deliver, and support registry and related services (Figure 1).

Figure 1 – ISV business segments (ISV investor presentation)

For more details on the business segments, investors are encouraged to read ISV’s annual reports or refer to my initiation article.

Adjusted Performance Improved As Management Has Guided

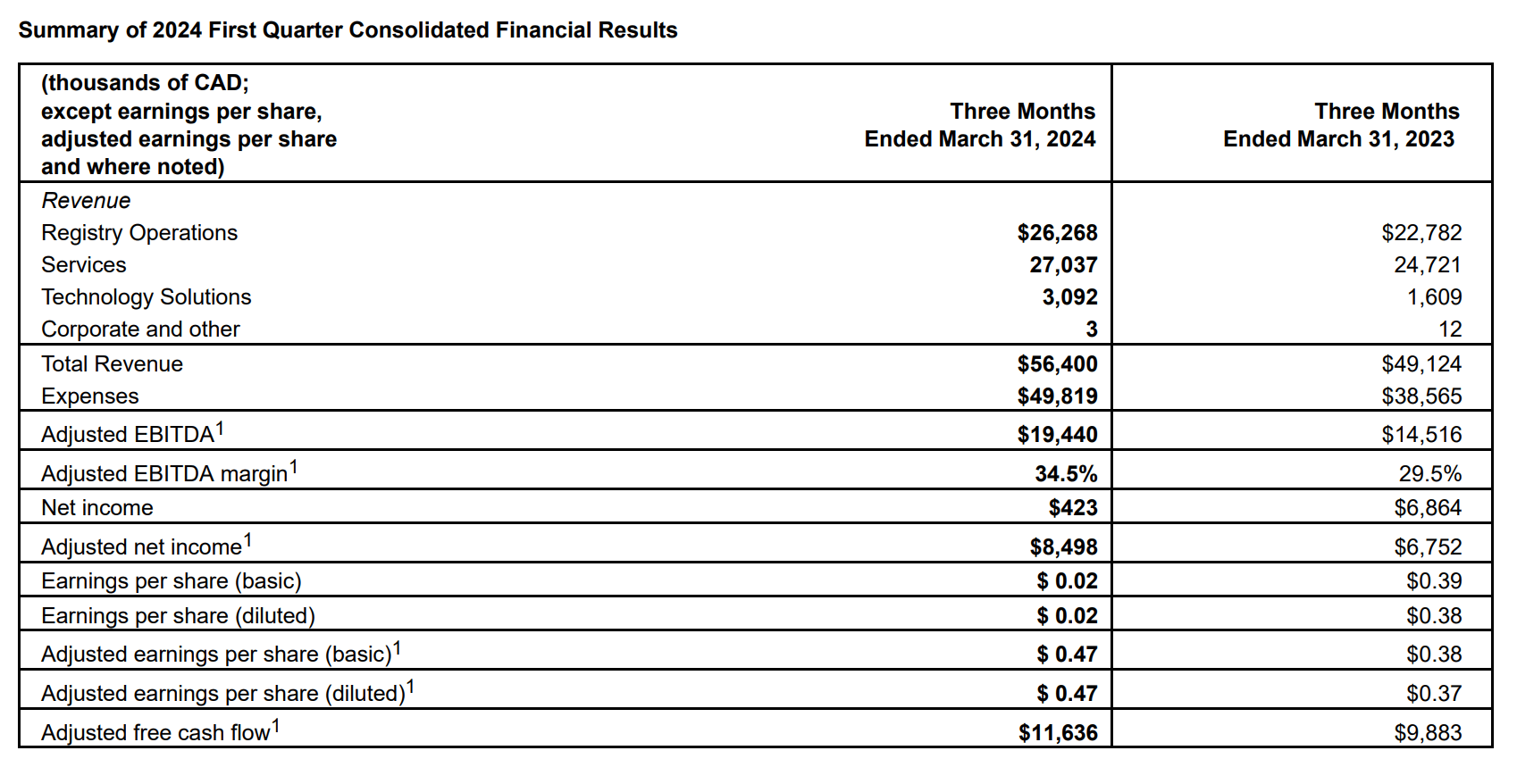

So far, ISV has been keeping its promise with a strong start to 2024. For Q1/2024, ISV recorded revenues of $56.4 million, a 14.9% YoY increase while adj. EBITDA soared higher by 33.8% YoY to $19.4 million (Figure 2).

Figure 2 – ISV Q1/24 financial summary (company reports)

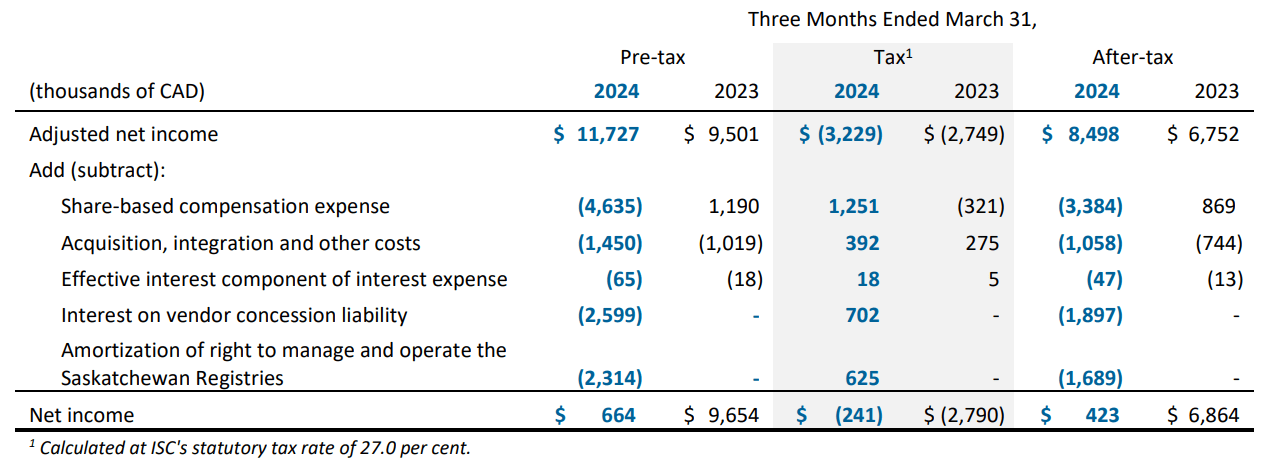

Adjusted net income was $8.5 million compared to $6.8 million in the prior year’s Q1, reflecting strong operating results offset by higher interest expenses.

But Beware Heavy Adjustments

Readers should note that the financial figures quoted above are adjusted for share-based compensation, acquisition expenses, interest on vendor concessions and the amortization of the right to manage the Saskatchewan contract (Figure 3).

Figure 3 – Adjustments to net income (company reports)

Without these adjustments, net income was $0.4 million compared to $6.9 million YoY.

Readers should note that I have a fairly dim view of adjusted financials as I believe share-based compensation is a real expense borne by shareholders and acquisition expenses should not be excluded for serial acquirers.

However, in ISV’s case, I do agree that the interest on vendor concessions and amortization of the right to manage the Saskatchewan contract should be backed out for a fair YoY comparison.

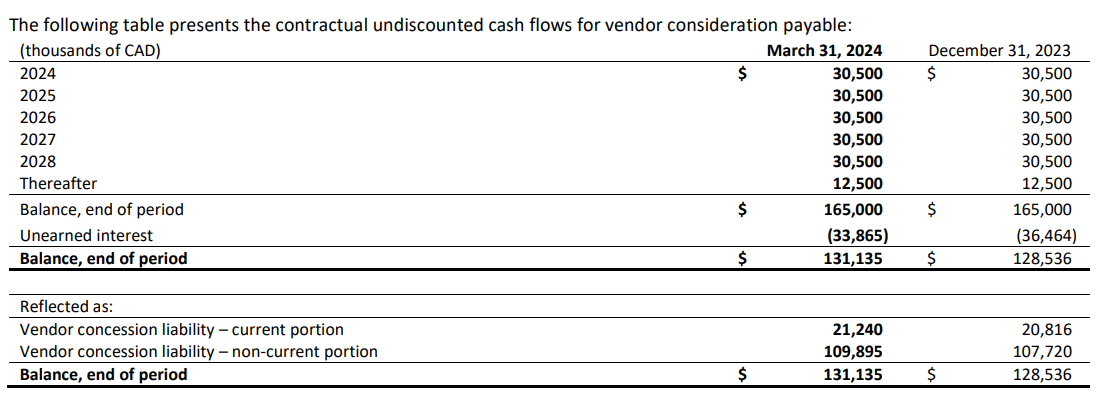

The vendor concession interest arises because part of the Saskatchewan contract renewal was structured as five annual payments of $30 million from July 2024 to July 2028 (Figure 4).

Figure 4 – Vendor concession details (company reports)

In effect, the Government of Saskatchewan is financing the renewal of ISV’s contract by spreading the payments over 5 years. While there is an imputed interest cost associated with these payments, there is no ‘cash interest’ expense paid by ISV.

Similarly, ISV had capitalized the extension of the right to manage and operate the Saskatchewan Registries in accordance with international accounting rules. However, the amortization of this ‘right’ is not a cash expense and there were no similar expenses in the prior year.

So in my opinion, a fairer YoY comparison should be adj. net income of $4.0 million compared to $6.9 million last year, with most of the declines due to higher share-based compensation.

Share-based Compensation Looks Excessive

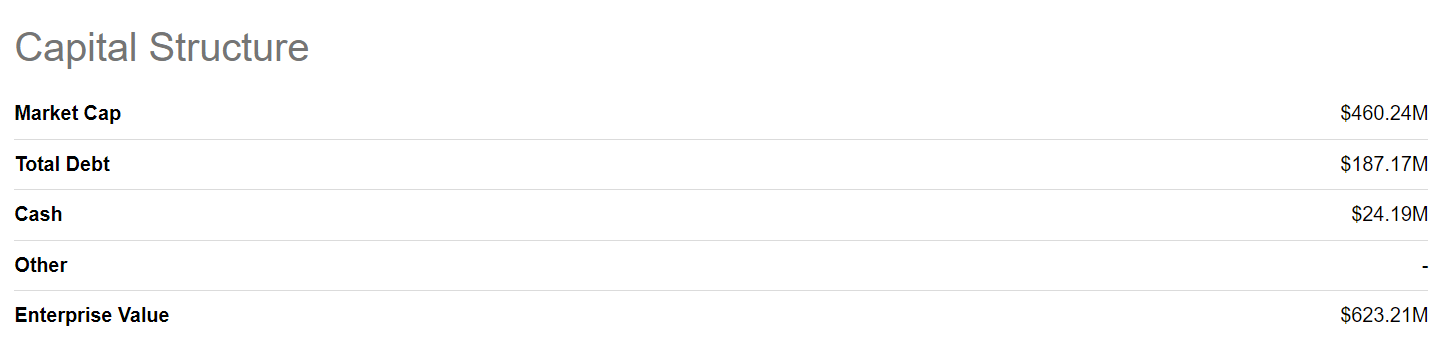

For a company with $460 million in market cap and $623 million in enterprise value, the pre-tax share-based compensation expense of $4.6 million looks excessive, as it represents more than 1% of the market cap of the company (Figure 5).

Figure 5 – ISV enterprise value (Seeking Alpha)

If this becomes a recurring quarterly expense, then investors could be looking at a ~4% annual dilution from share-based compensation, which is a high hurdle.

Land Registry Business Surge On Price Increase

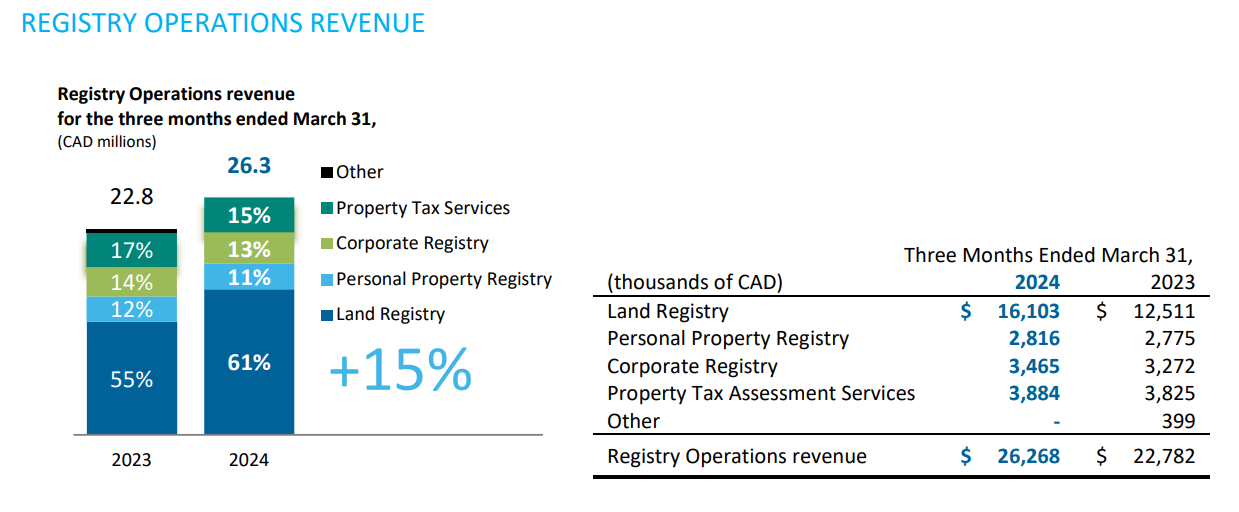

Moving on to a review of the business segments, as I mentioned above, ISV saw improvements in its financial performance mostly as price increases from Q3 last year have begun to flow through the financial statements, with the Registry segment seeing a 15% YoY increase in revenues (Figure 6).

Figure 6 – Registry segment YoY comparison (company reports)

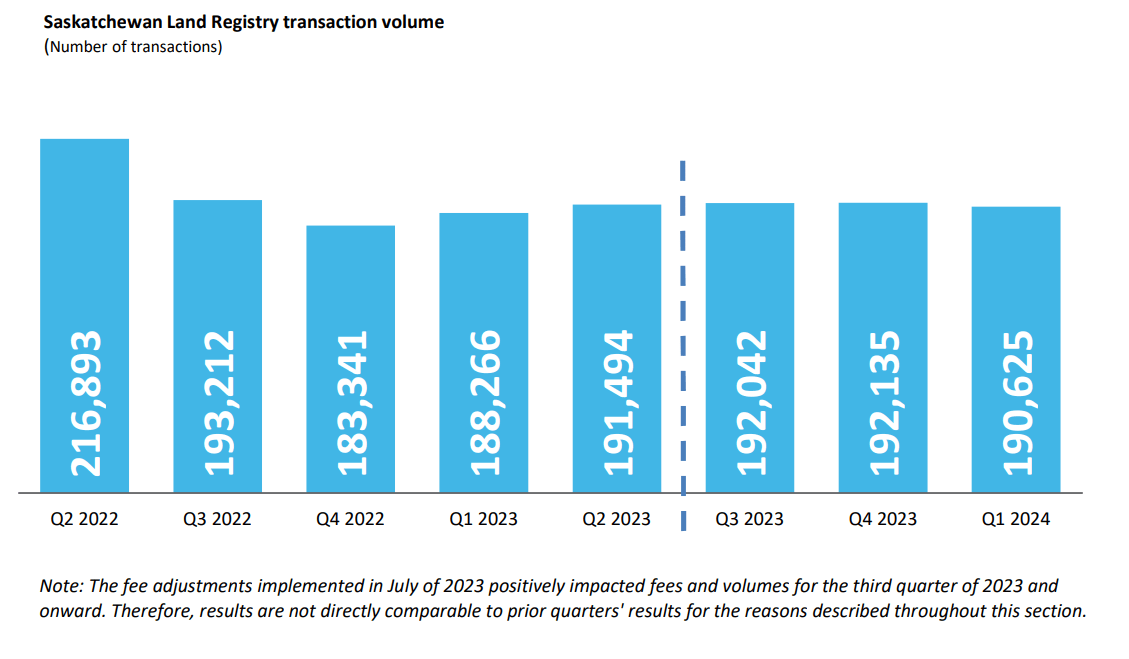

Looking at the details, the increase in Registry revenues was primarily driven by a 39% increase in Land Registry revenues, which benefited from price increases and CPI adjustments. Transaction volumes were up nominally in Q1/24 due to the introduction of a mortgage discharge fee in July 2023. Excluding this new transaction fee, volume would have decreased by 3% YoY as title searches (which make up more than 70% of transaction volumes) declined by 4% YoY (Figure 7). Other Registry sub-segments were mostly flat YoY.

Figure 7 – Saskatchewan land registry transaction volumes (company reports)

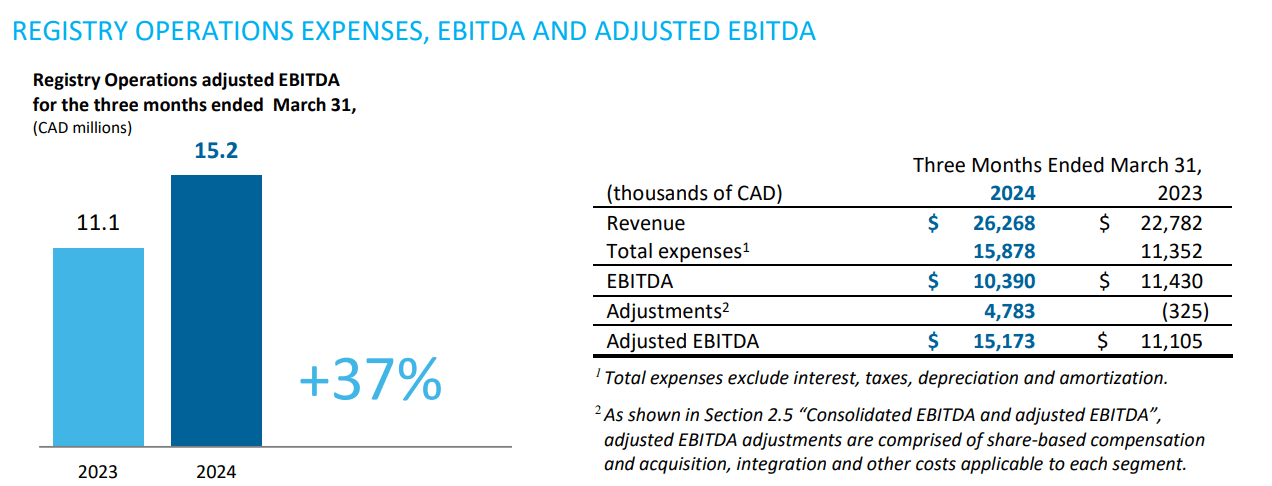

Adjusted EBITDA for the Registry segment, excluding share-based compensation, grew 36.9% YoY as revenues grew faster than expenses (Figure 8).

Figure 8 – Registry segment saw strong growth in adj. EBITDA (company reports)

Services Growth Was More Modest

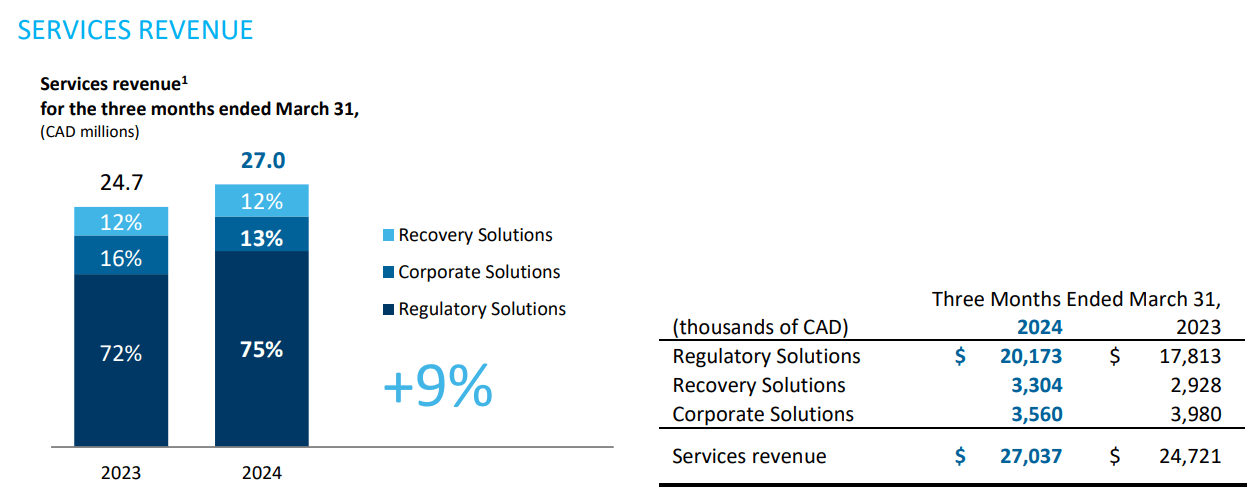

Revenue growth in the Services segment was more modest at 9% YoY, but broader, with both Regulatory and Recovery Solutions growing revenues 10%+ as financial institutions and auto finance customers continued to enhance their due diligence processes in an environment of higher interest rates and increased regulatory oversight (Figure 9).

Figure 9 – Services segment YoY comparison (company reports)

A decline in Corporate Solutions revenue was due to reduced Ontario corporate filing transactions in the quarter.

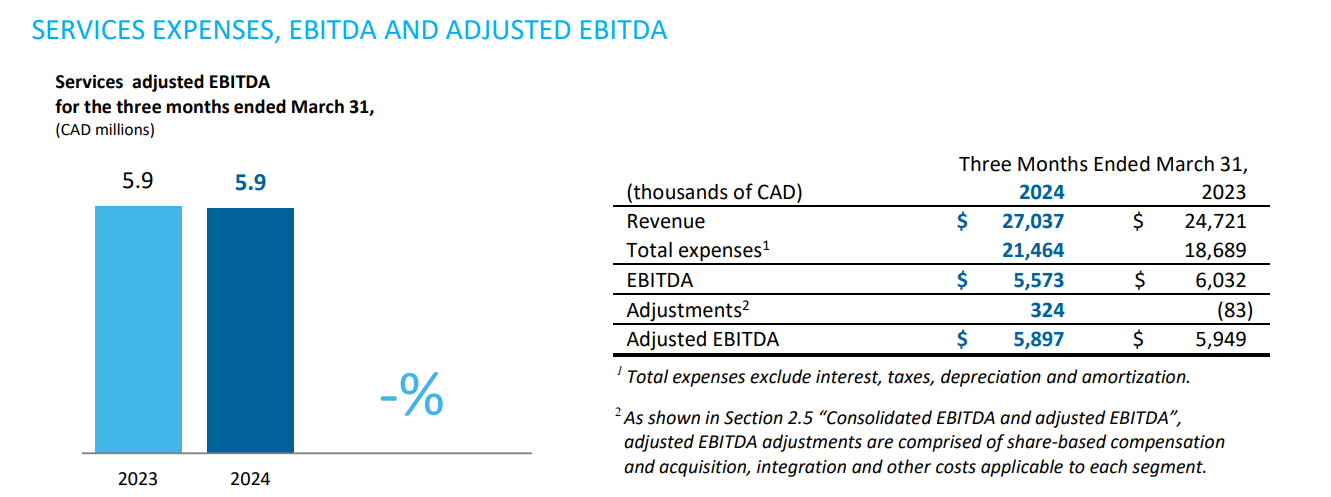

However, profitability in the Services segment declined YoY as increases in costs outpaced the rise in revenues (Figure ).

Figure 10 – Services segment saw a decrease in EBITDA (company reports)

Technology Solutions Turn A Modest Profit

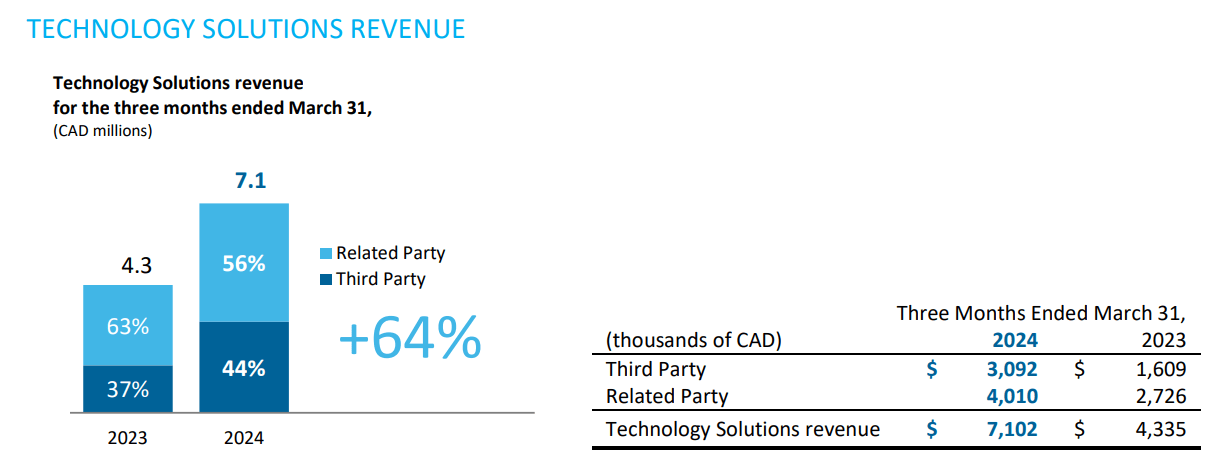

Finally, the Technology Solutions segment saw a surge in revenues due to the advancement of existing and new implementation contracts (Figure 11).

Figure 11 – Technology solutions segment YoY comparison (company reports)

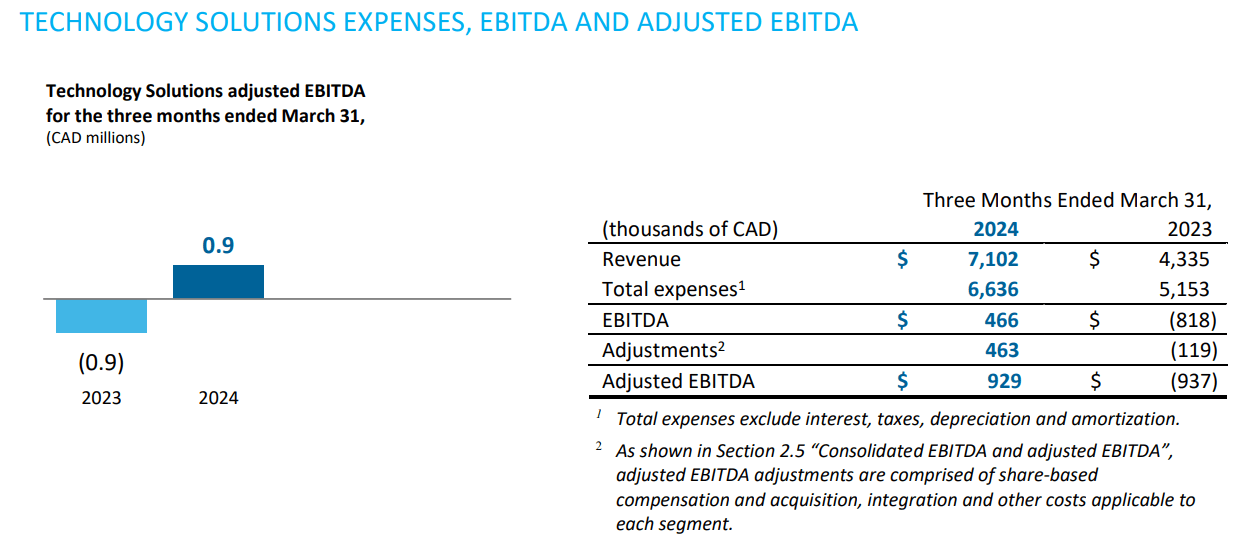

The increase in Technology Solutions revenues was able to turn the segment slightly profitable for the quarter (Figure 12).

Figure 12 – Technology Solutions was profitable in Q1 (company reports)

Valuation Remains Attractive

Although ISV’s stock price has increased 18% since my last article, the company actually got cheaper. Based on forward adj. EBITDA guidance of $87 million, the company is currently trading at a Fwd EV/adj. EBITDA of 7.2x, less than the 8.0x previously.

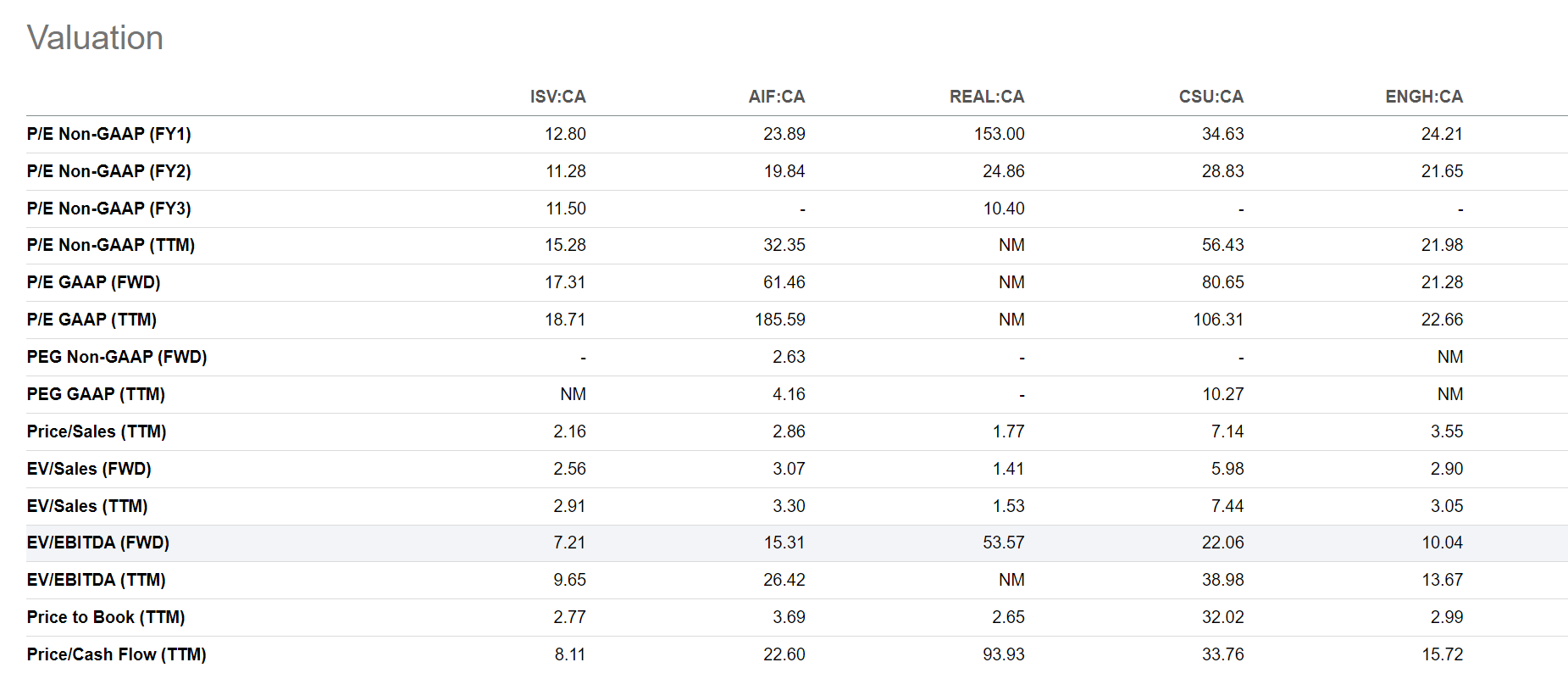

I continue to believe ISV should trade at a higher valuation multiple, in line with its technology and real estate service peers that trade between 10 to 53x Fwd EV/EBITDA (Figure 13).

Figure 13 – ISV vs. peer valuations (Seeking Alpha)

Using a 10x Fwd EV/EBITDA, ISV’s equity should be worth $700 million, or $39 / share.

Sets Ambitious Growth Targets

Having doubled the size of ISV on a revenue and adj. EBITDA basis over the last 10 years, ISV management recently announced an ambitious goal of doubling the size of the company again by 2028. ISV hopes to achieve this through both organic growth and M&A.

If management is successful, then by 2028, ISV could have run-rate adj. EBITDA north of $170 million, which could propel the company onto the radar of many institutional investors that cannot invest in sub-$1 billion market cap companies. This could further improve ISV’s valuation multiple compared to its larger technology / real estate service peers.

Risks To ISV

The Saskatchewan economy remains the key revenue driver for ISV, as ~40% of the company’s revenues are tied to registry services for Saskatchewan real estate and businesses. If Saskatchewan’s economy deteriorates, it will undoubtedly have a negative impact on ISV.

Further, as the company took on significant leverage to complete the Saskatchewan contract renewal, profitability has been reduced. If interest rates remain high, it could lengthen the time it takes for ISV to reduce leverage.

Conclusion

Information Services Corp. saw a sharp increase in registry revenues, as price increases implemented in Q3/2023 flow through the financial statements.

Despite the stock rising by 18% since my last update, it is actually cheaper, trading at just 7.2x Fwd EV/adj. EBITDA as we roll onto 2024 estimates that include the improved registry pricing.

One fly in the ointment with ISV is its heavily adjusted financials, which make historical comparisons more difficult. I am also concerned with the recent surge in share-based compensation.

ISV continues to look cheap compared to real estate services and technology peers, so I maintain my buy recommendation.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.