ajr_images

We beforehand lined Intel (NASDAQ:NASDAQ:INTC) in January 2024, discussing why the inventory’s embedded progress premium supplied a minimal margin of security, with the underwhelming ahead steerage bringing forth the sobering correction in its inventory costs after the latest earnings name.

Whereas some would possibly choose to view the administration’s ahead commentary as a kitchen sink steerage, with a subsequent beat in estimates more likely to convey forth glorious upside potential, we had most well-liked to view it conservatively then, triggering our Maintain score.

On this article, we will focus on INTC’s underwhelming Foundry prospects after the discharge of its new phase reporting, because the IDM 2.0 naturally brings forth the unsure money burn and drag on its general profitability.

That is on high of its delayed node roadmap in comparison with its foundry peer, signaling Intel Foundry’s unsure prospects given its nascency.

Whereas we’re optimistic concerning the inventory’s US-made sentiments, it stays to be seen when INTC’s foundry phase will be capable of ship the crucial mixture of node development, quantity manufacturing, and profitability, leading to our reiterated Maintain score.

INTC’s Foundry Funding Thesis Is Speculative At This Level

INTC’s Rising Money Burn In The Foundry

INTC

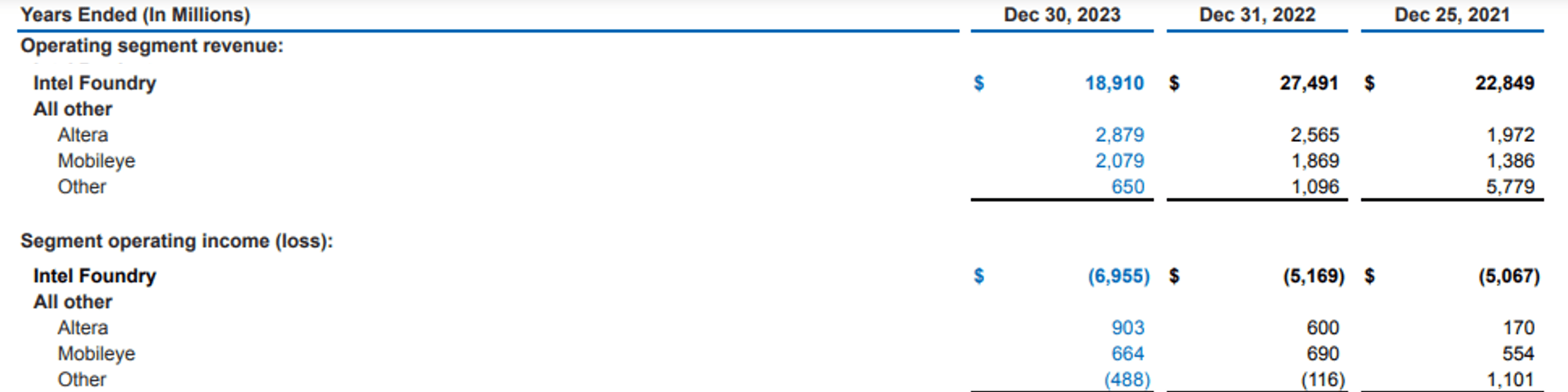

INTC has lately reported its new reporting segments by early April 2024, with the Intel Foundry notably being unprofitable at working losses of -$6.95B (-34.6% YoY) and margins of -36.7% (-18 factors YoY) in FY2023.

From these numbers, it’s obvious that the money burn has grown drastically on a YoY foundation, with 2024 supposedly being “the trough year for foundry working losses.“

On the similar time, the INTC administration has aggressively guided “breakeven operating margin” by roughly 2027 and “60% non-GAAP gross margins and 40% non-GAAP operating margins by 2030.“

It’s unsure how the administration goals to realize this, on condition that Intel Foundry at present solely studies a “lifetime deal value with external customers of more than $15B,” in comparison with the FY2023 revenues of $18.91B (-31.2% YoY).

When in comparison with the market chief, Taiwan Semiconductor Manufacturing Firm Restricted’s (TSM) FY2023 revenues of $69.29B (-8.1% YoY) and working margins of 42.6% (-6.9 factors YoY), INTC’s numbers seem like very aggressive given its nascency certainly.

On account of this improvement, we imagine that INTC’s long-term foundry prospects seem like unsure, particularly since TSM has already diversified its world footprints in Japan and Arizona, partly balancing the latter’s geopolitical headwinds.

INTC’s Node Roadmap

INTC, Tom’s {Hardware}

INTC’s latest roadmap has additionally prompt that the 14A node (the equal of 1.4nm) is predicted to enter manufacturing solely by 2026 and 10A node (the equal of 1nm) to start improvement by 2027, with it remaining to be seen when quantity manufacturing could happen.

That is in comparison with TSM’s current roadmap, with 3nm at present in quantity manufacturing/ 2nm by 2025 and no additional detailed supplied by the administration but.

If something, readers should additionally notice that whereas INTC’s Node Roadmap has highlighted that the 18A node is already in manufacturing, the fact is that 18A is barely “on-track and manufacturing ready on the finish of” 2024, with the long run 18A Xeon processor, Clearwater Forest, solely slated to be launched in 2025.

Consequently, we imagine that readers must mood their expectations for INTC’s superior nodes, for the reason that similar could very effectively happen for the 14A and 10A, with the “five new nodes in four years” seemingly loosely termed and quantity manufacturing more likely to happen over an extended time period.

And it is for that reason that we concur with TSM’s commentary within the FQ4’23 earnings name, in that it’s extra essential to “work with the client to offer them the perfect transistor know-how and the perfect power-efficient know-how and at an inexpensive value – the technology maturity that within the high-volume manufacturing.“

For now, it might be extra prudent to order judgment on the foundries’ technological launch timeline, particularly since INTC’s foundry phase is predicted to stay unprofitable over the subsequent few years, implying its lack of producing scale.

With INTC set to report its FQ1’24 earnings name on April 25, 2024, readers could need to pay attention to the Intel Foundry’s efficiency, particularly for the reason that phase is predicted to hit peak losses in FY2024.

For now, the market has additionally priced in underwhelming FQ1’24 revenues of $12.78B (-17% QoQ/ +9% YoY) and adj EPS of -$0.14 (-122.2% QoQ/ + 78.7% YoY), worse than the administration’s kitchen sink EPS guidance of $0.13 (-79.3% QoQ/ +181.2% YoY).

We imagine that the consensus estimates are usually not overly bearish certainly, with the latest acquire within the x86 CPU market share to 62.6% as of Q1’24 (+1.6 factors QoQ/ -0.1 YoY) possible attributed to the drastic value cuts and impacted revenue margins as mentioned in my earlier article here.

Mixed with the bloated working bills and capex, we may even see INTC’s stability sheet additional deteriorate from the web money owed of $21.94B reported in FQ4’23 (+134.6% YoY/ +81.1% from FQ4’19 ranges), with the administration seemingly financing its dividend payouts with debt.

Readers could need to take note of these metrics forward, for the reason that INTC inventory could expertise extra volatility within the coming weeks.

The Consensus Ahead Estimates

Tikr Terminal

Lastly, with INTC racing to broaden its world footprint throughout the US, Israel, Eire, Germany, and Mexico, amongst others, it goes with out saying its Free Money Move era can be impacted, as mirrored within the consensus ahead estimates, with the corporate more likely to be extremely reliant on authorities subsidies/ native incentives.

With INTC’s Ohio and Arizona plant completions already delayed, the ache could also be extended certainly, because the market priced in a flattish high/ backside line efficiency between FY2019 and FY2026.

INTC Valuations

Looking for Alpha

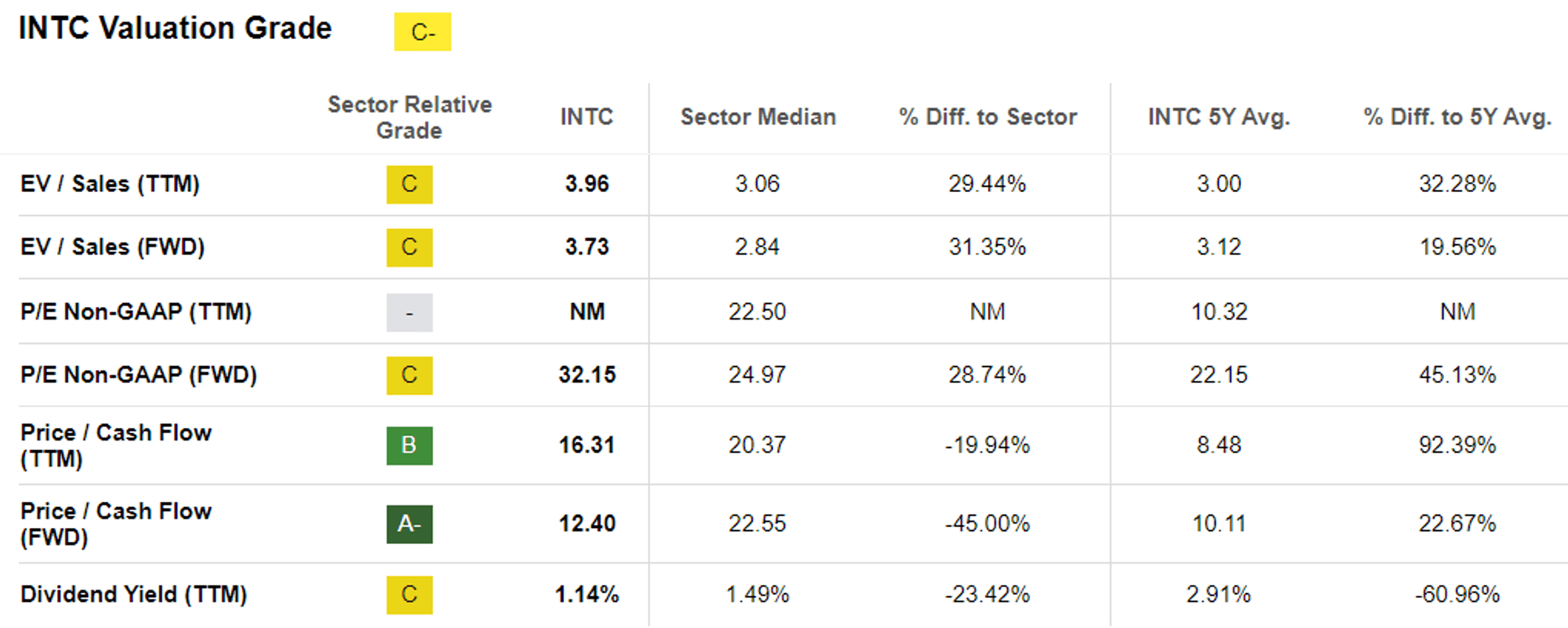

On account of its minimal progress prospects, we’re unsure about INTC’s premium FWD P/E valuation of 32.15x and FWD Value/ Money Move valuation of 12.40x, whereas moderated from the earlier article at 34.65x/ 12.45x nonetheless elevated in comparison with the 5Y imply of twenty-two.15x/ 10.11x and the sector median of 24.97x/ 22.55x, respectively.

So, Is INTC Inventory A Purchase, Promote, or Maintain?

INTC 2Y Inventory Value

Buying and selling View

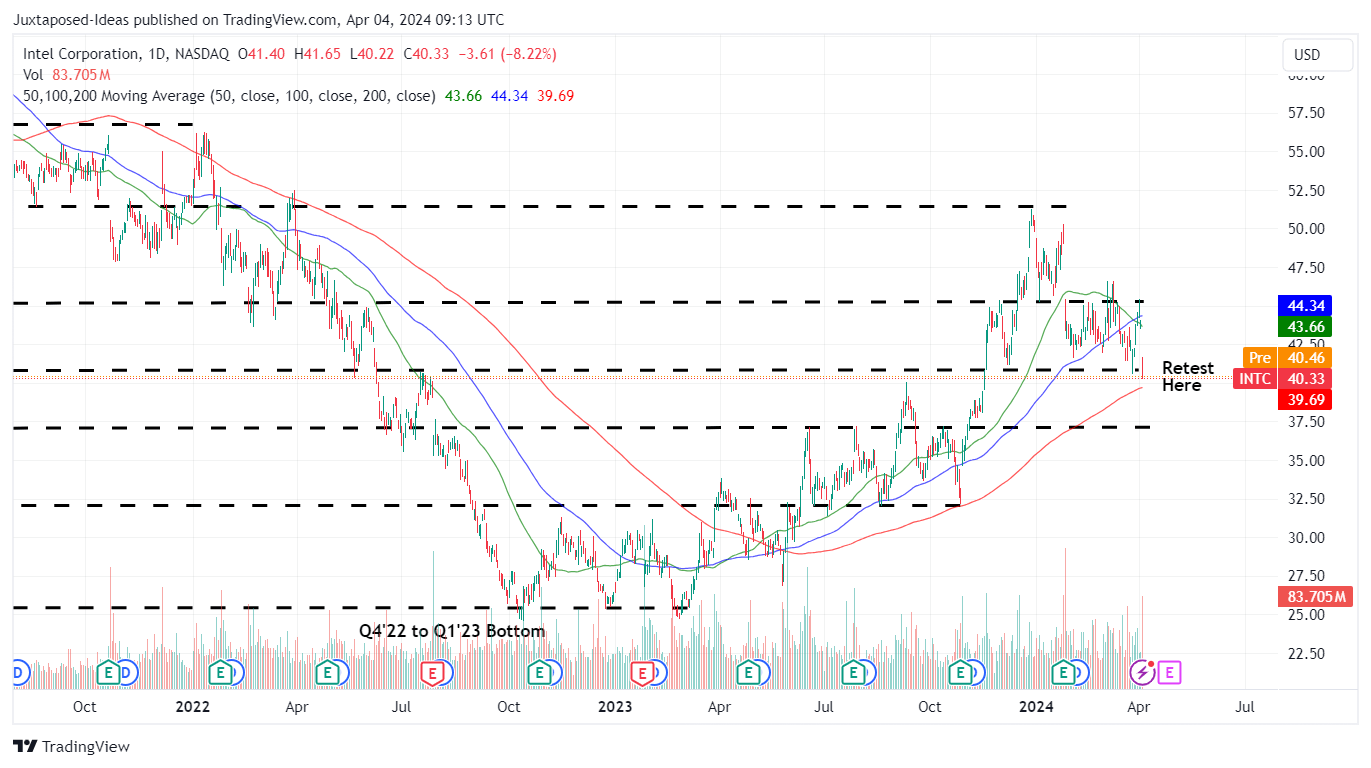

For now, INTC has returned a part of its latest features with the inventory showing to retest its earlier help ranges of $40s on the time of writing.

Based mostly on the annualized FQ4’23 adj EPS of $1.36 (after adjusting for the $1.2B litigation profit for improved accuracy, versus the reported sum of $2.52) and the 5Y P/E imply valuations of twenty-two.15x, it seems that the inventory is buying and selling means above our truthful worth estimate of $30.10.

We imagine that it’s extra prudent to seek advice from INTC’s 5Y P/E imply right here, given its projected lack of progress and impacted profitability between FY2019 and FY2026 as the corporate undergoes an unsure transition to IDM 2.0.

On the similar time, its dividends appear to be shaky primarily based on the Looking for Alpha Quant Score, with impacted TTM Curiosity Protection ratio of 0.04x and TTM Dividend Protection ratio of 0.55%, in comparison with the sector median of 10.97x and a pair of.82%, respectively.

Mixed with the quite a few elements mentioned above, we imagine that there stays nice uncertainty in INTC’s execution shifting ahead.

On account of the blended alerts, we desire to proceed score the INTC inventory as a Maintain right here. It might be extra prudent to look at the administration’s intermediate-term execution earlier than including at this perceived dip.