buzbuzzer/E+ by way of Getty Photos

We have owned International Companions LP (NYSE:GLP) widespread shares for the reason that Monetary Disaster, after we had been lucky sufficient to have the ability to purchase them at a vastly diminished value. In case you can grit your tooth arduous sufficient, and keep calm sufficient to choose up some very excessive yield bargains throughout meltdowns, it may be very rewarding.

Along with its widespread items, GLP additionally presents 2 preferreds, however they’re redeeming the floating charge A shares on April 15, 2024. Its B collection preferreds are promoting at $24.24, properly above their $25.00 name worth. It additionally presents Senior Notes.

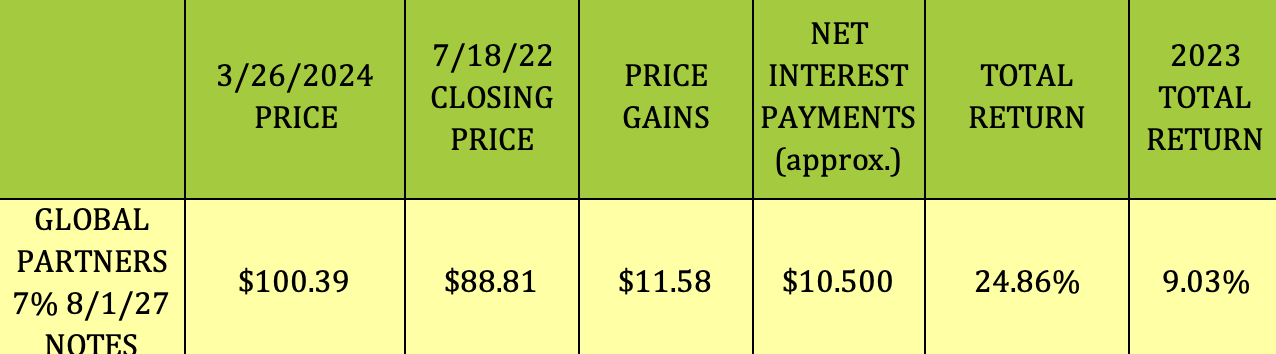

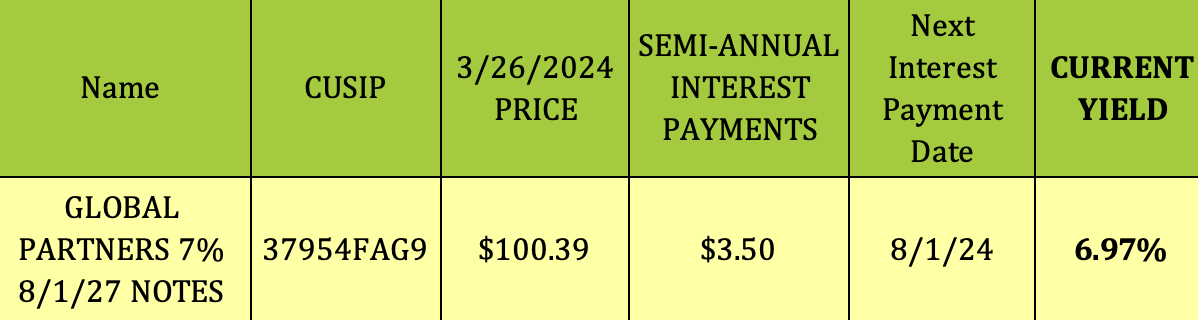

We added the International Companions 7% 8/1/27 Senior Notes to our portfolio on 7/18/22. Since then, they’ve delivered a 24.86% return to subscribers, comprised of $11.58 in value features and $10.50 in curiosity funds:

Hidden Dividend Shares Plus

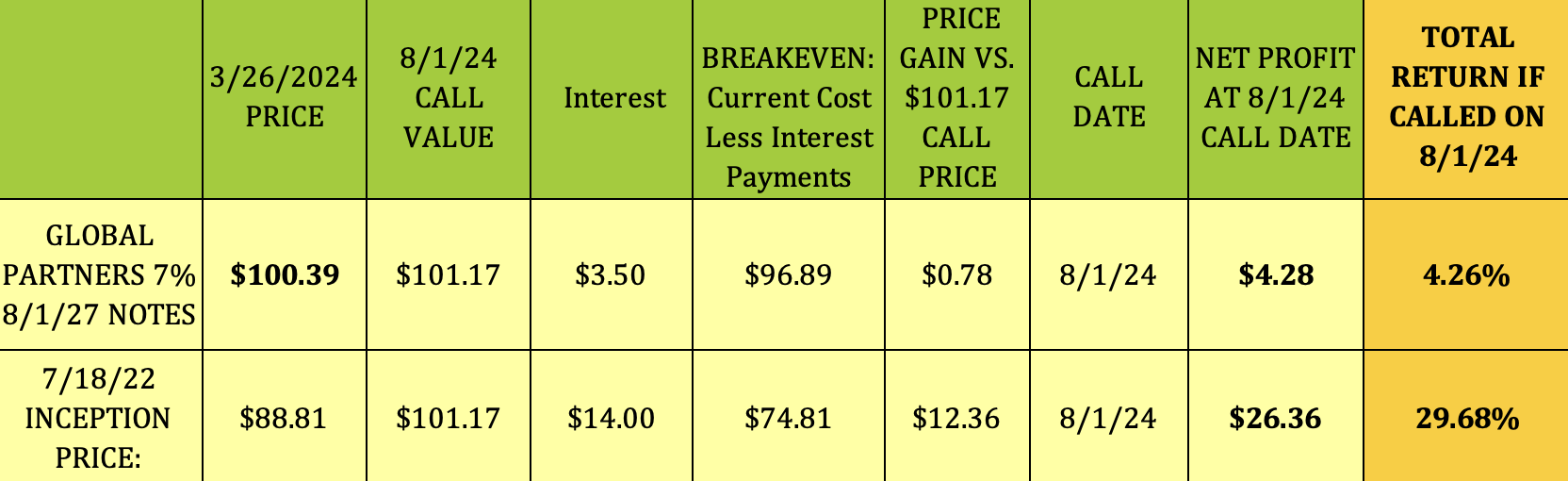

These notes have annual redemption costs on August 1st. For patrons who purchased in July 2022 at $88.81, the full revenue if these notes are redeemed on 8/1/24 could be $26.36, comprised of a $12.36 capital achieve, and ~$14.00 in curiosity, for a 29.68% complete return. GLP should notify noteholders 15 days previous to redemption.

Hidden Dividend Shares Plus

Firm Profile:

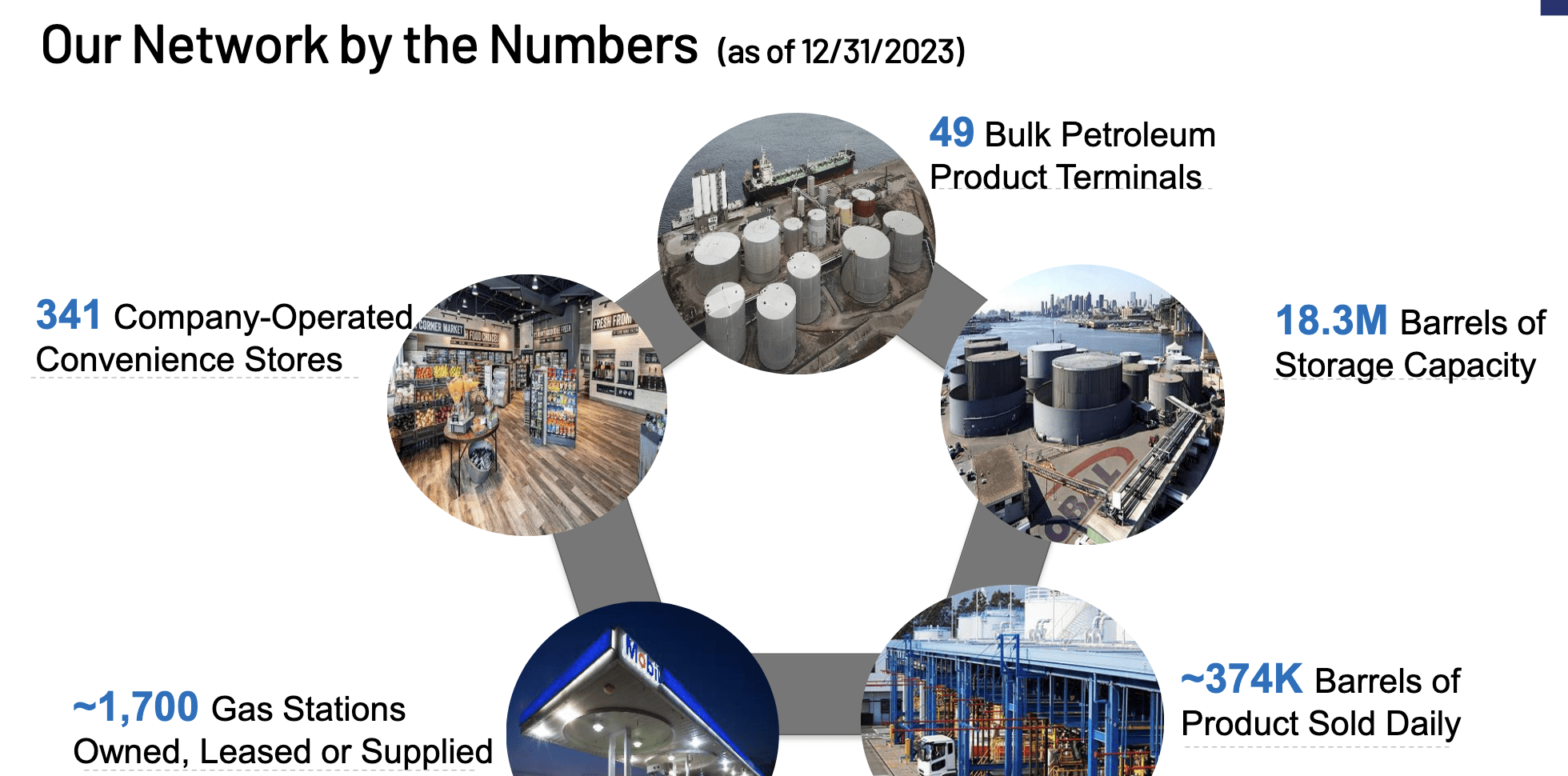

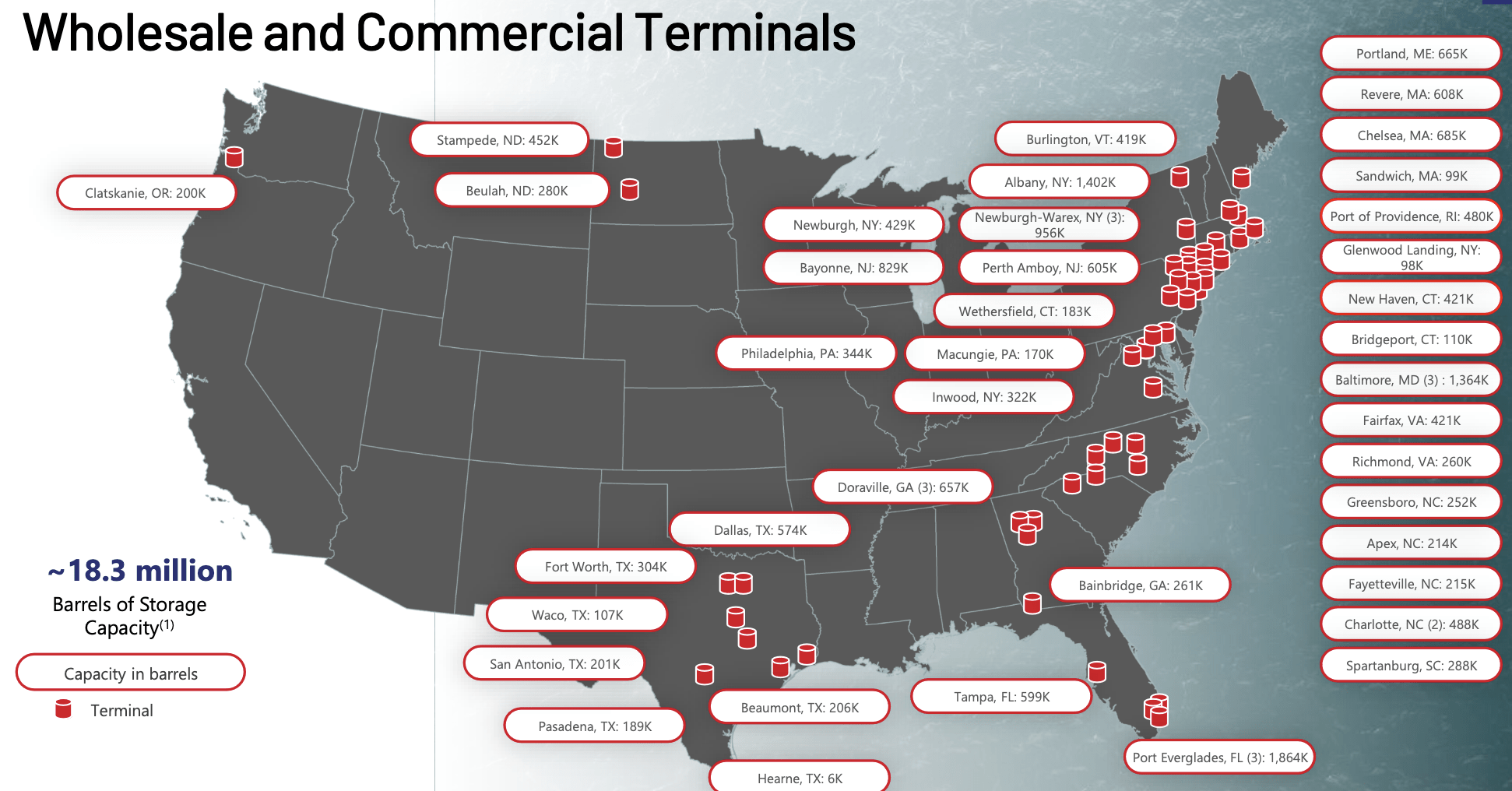

GLP is a significant presence in gasoline distribution within the Northeastern US, promoting by way of retail and wholesale divisions. It is also concerned within the transportation of petroleum merchandise and renewable fuels by way of rail from the mid-continent area of america and Canada, and has a rail and waterborne terminal on the West Coast, in Oregon. GLP additionally owns 49 petroleum terminals, with 18M barrels of capability, and distributes a median of 374K barrels each day:

GLP website

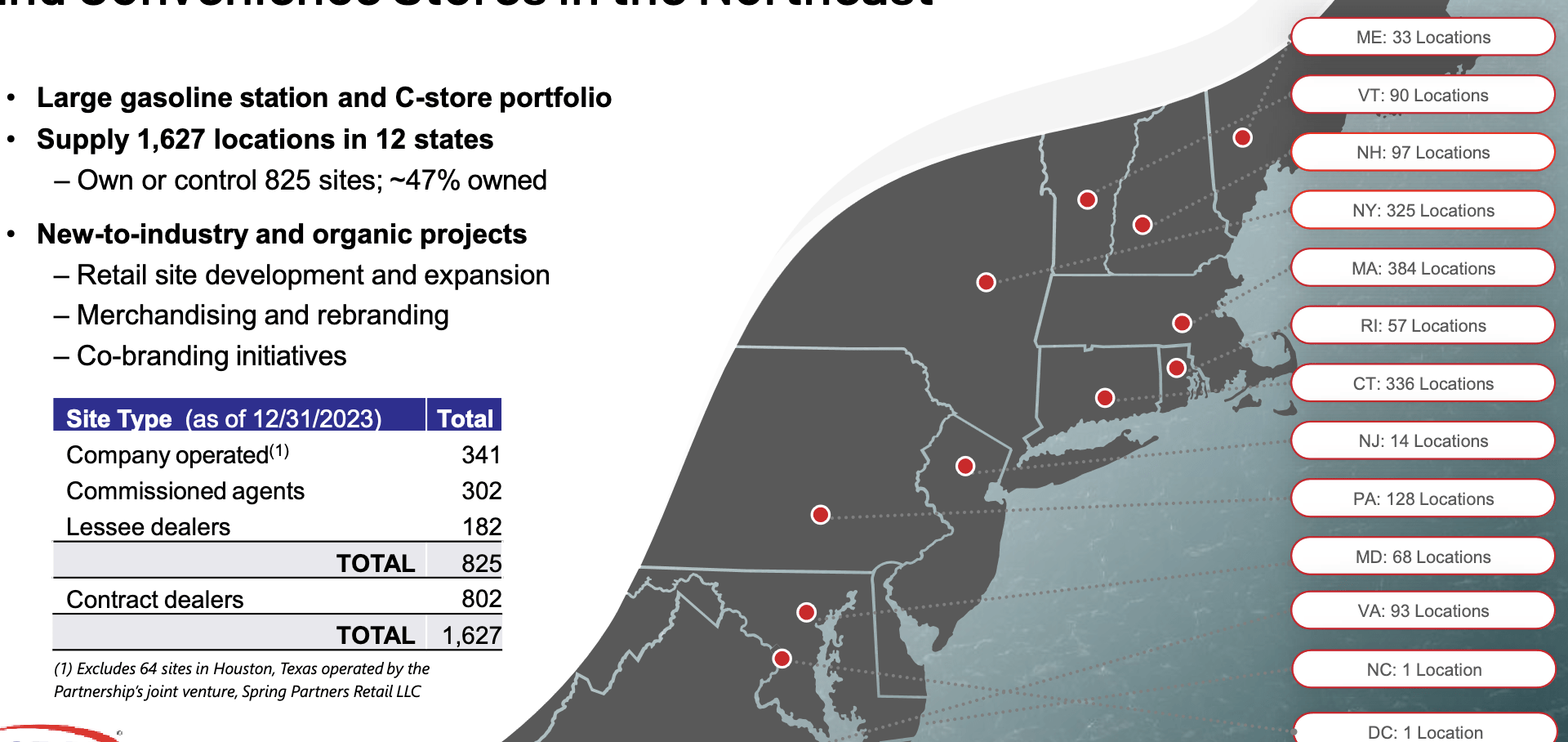

GLP’s GDSO (gasoline distribution and station operations) portfolio consists of 1700 websites comprised of 341 firm operated websites, 302 fee brokers, 182 leasing sellers, and 802 contract sellers.

GLP website

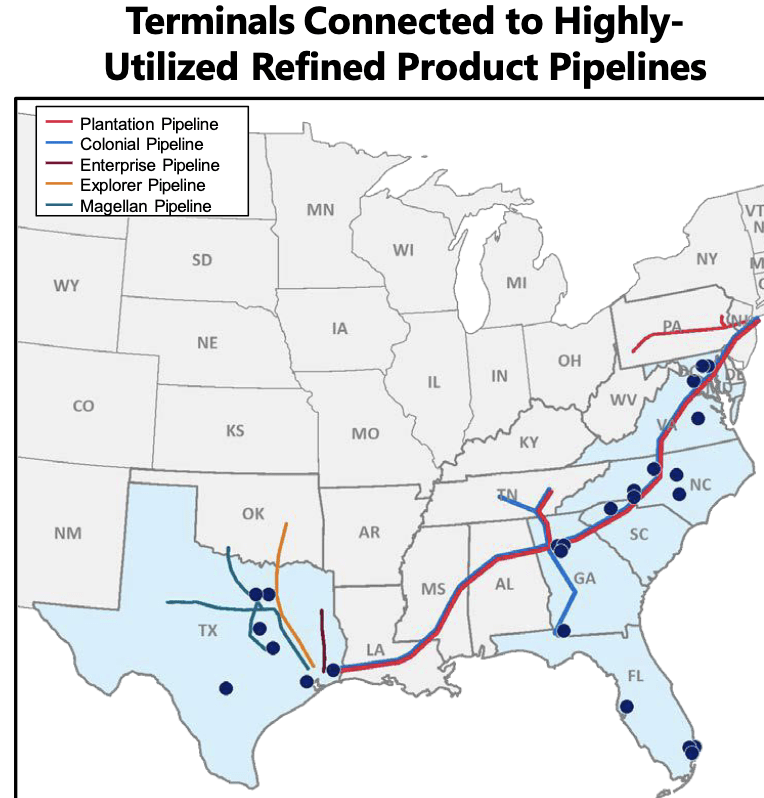

It has terminals all alongside the Japanese Seaboard, and in Texas, along with N. Dakota and Oregon:

GLP website

There was fairly a debate about the way forward for fossil gasoline distribution companies like GLP, because the US is transitioning to renewables. Whereas electrical autos have been rising in quantity and acceptance over the previous few years, we’re nonetheless in a protracted transitional section, which ought to help GLP’s operations for a few years to return.

Acquisitions:

Administration continues to make vital acquisitions so as to develop the enterprise.

They accomplished the acquisition of 25 refined product terminals from Motiva Enterprises for $313.2M in money in December. The transaction is underpinned by a 25-year take-or-pay throughput settlement with Motiva, the anchor tenant on the terminals, that features minimal annual income commitments.

“The addition of these terminals supports the growth of our integrated supply, storage and retail network in rapidly growing areas of the country—Florida, Georgia, Texas and the Carolinas—providing customers with gasoline, diesel and other liquid fuels essential to their daily lives.” (GLP website)

Hidden Dividend Shares Plus

In Q2 ’23, GLP did a three way partnership with Exxon Mobil to amass 64 Houston-area comfort and fueling amenities from the Landmark Group.

Earnings:

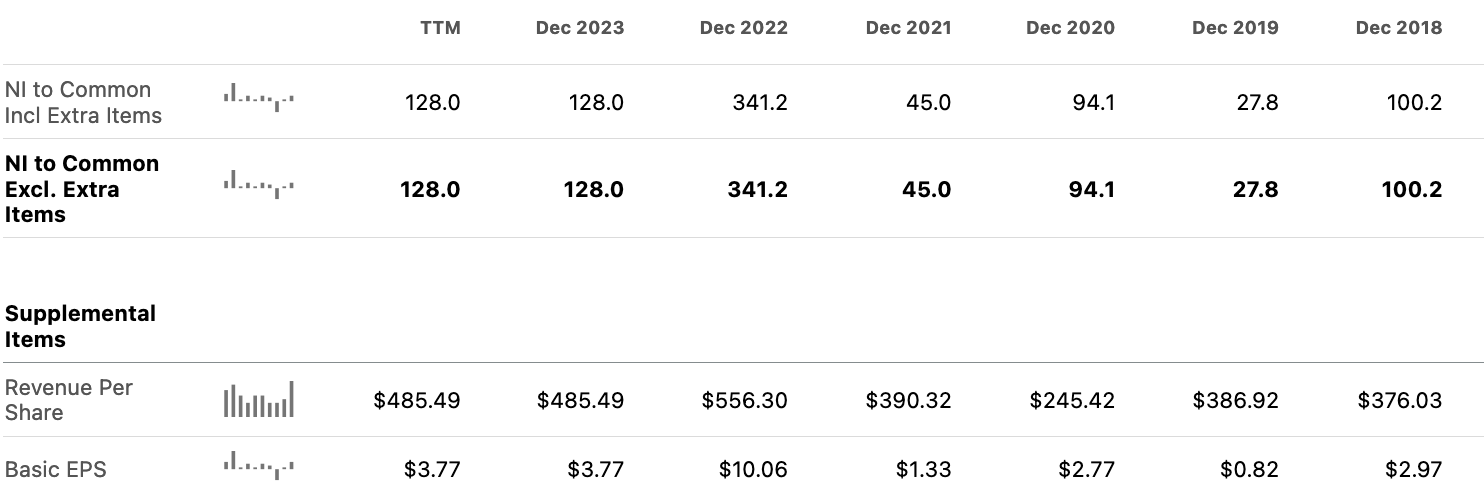

2022 was a file 12 months for GLP, with increased gasoline costs and quantity, which has consequently given it powerful comps for 2023 to beat.

Nonetheless, check out 2023 vs. GLP’s pre-COVID Internet Earnings and Income in 2018-2020 – whereas 2023 Internet Earnings and Income had been a lot decrease than in 2022, an distinctive 12 months, they had been nonetheless a lot increased than in 2021, 2020, 2019, and 2018:

SA

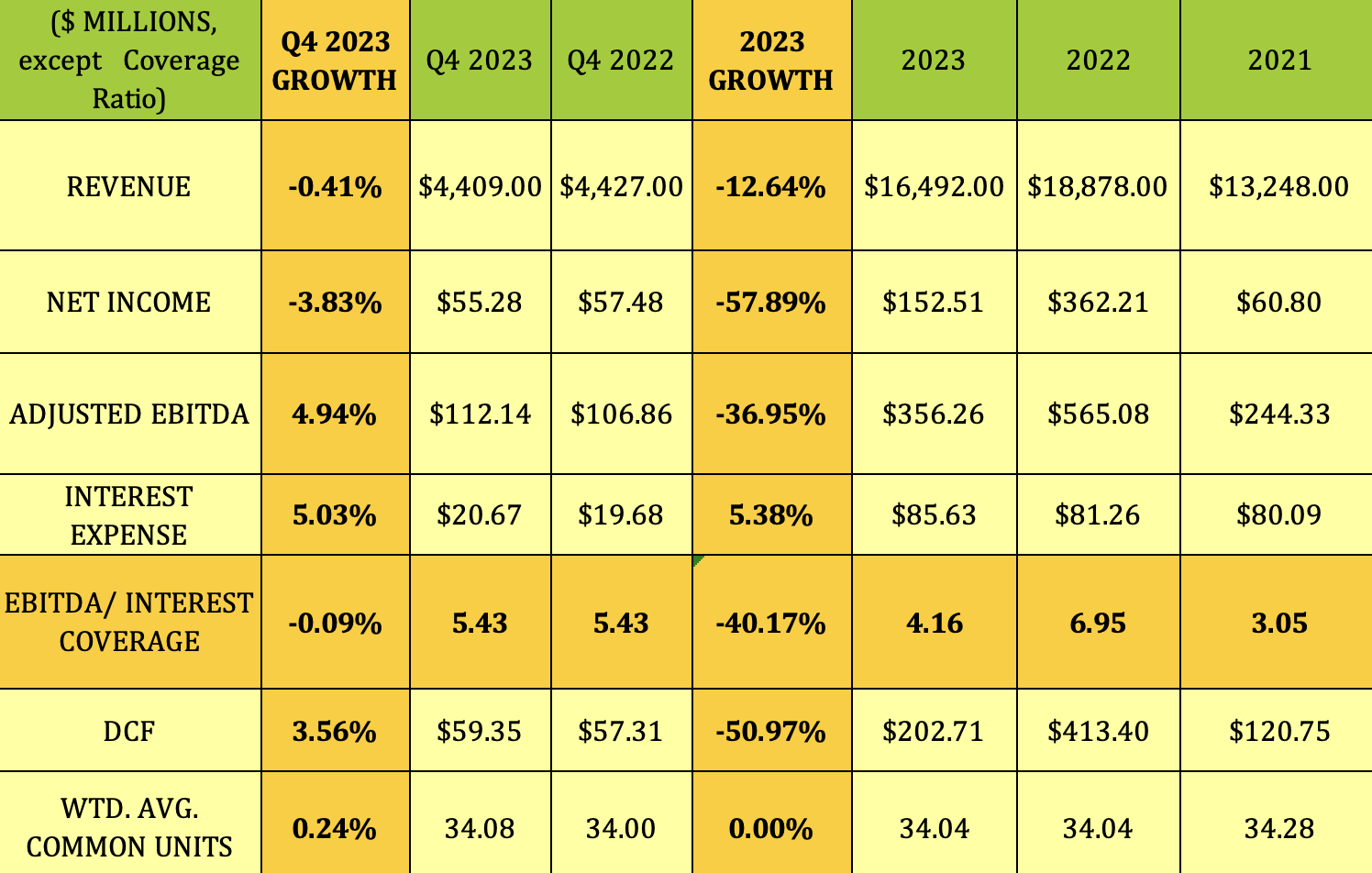

This fall ’23 was roughly in step with This fall ’22, with flat revenues, Internet Earnings down 5%, EBITDA up ~5%, and Distributable Money Movement (DCF) up 3.6%. Curiosity expense was up 5%, a gentle enhance vs. many different corporations’ bills in This fall ’23; and EBITDA/Curiosity protection, the important thing determine for us note-holders, was steady, at 5.43X.

As famous above, 2022 had a lot increased gasoline costs, which elevated GLP’s revenues and earnings. As well as, GLP accomplished the sale of its terminal situated on Boston Harbor in Revere for $150M.

However check out how 2023 compares to 2021 – Income, Internet Earnings, EBITDA, and DCF had been all up considerably. Granted, in 2021, the US was nonetheless digging its method out of the COVID mess, however our predominant level right here is that GLP, removed from struggling, is a enterprise with long run property and earnings.

Hidden Dividend Shares Plus

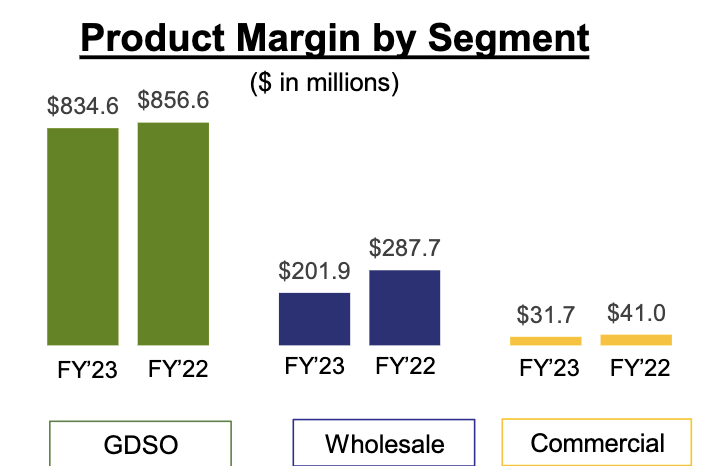

GLP’s GDSO, (gasoline distribution and station operations) phase had $22M much less in Product Margin in 2023, down 2.6% at $834.6M; whereas its Wholesale margin fell by ~30%, to $202M, and its Industrial phase margin fell by ~20%, to $31.7M in 2023 vs. 2022:

GLP website

Present Observe Yield:

These notes pay $3.50 in semi-annual curiosity on February 1st and August 1st. At $100.39, their present yield is 6.97%.

Hidden Dividend Shares Plus

Frequent Dividend:

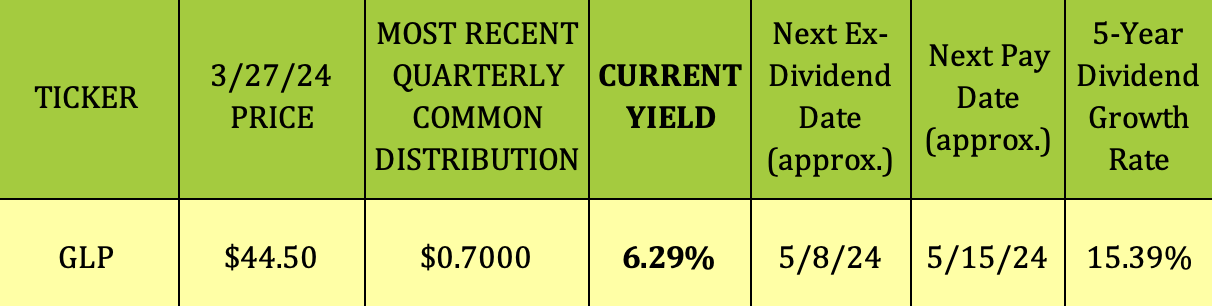

Along with its Notes and Preferreds, GLP additionally has a standard dividend. Its most up-to-date quarterly payout was $.70/unit, which supplies GLP a 6.3% dividend yield, at its $44.50 value degree.

GLP has a formidable 5-year dividend development charge of 15.39%, with its 2 greatest dividend will increase coming in 2021 and 2023. Administration fuel raised the widespread distribution for 9 straight quarters.

Trailing 12-month distribution protection as of 12/31/23 was 1.85X after factoring in distributions to most well-liked unit holders.

Hidden Dividend Shares Plus

Taxes:

GLP is an LP – it points a Ok-1 at tax time for its widespread and most well-liked items.

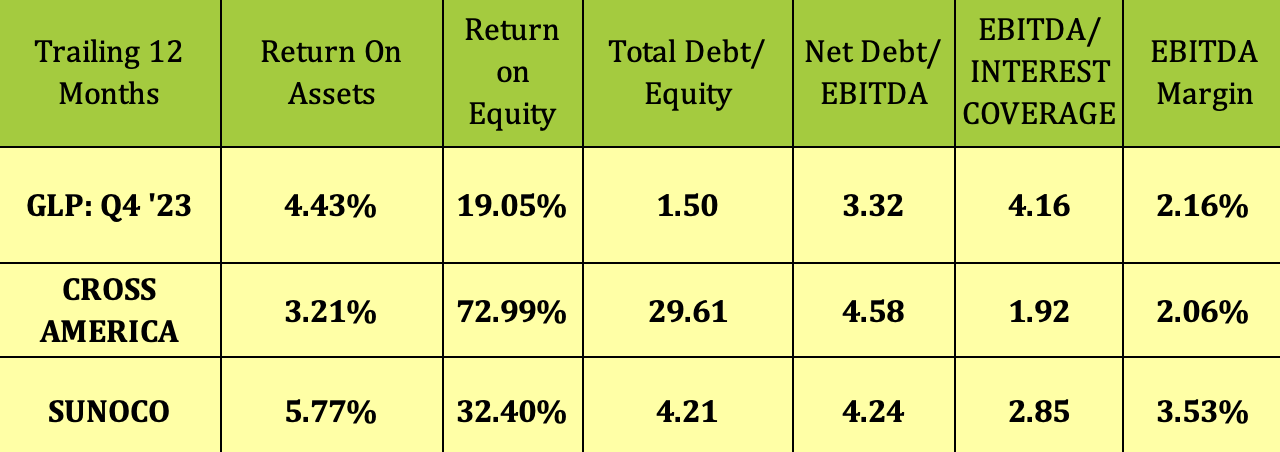

Profitability & Leverage:

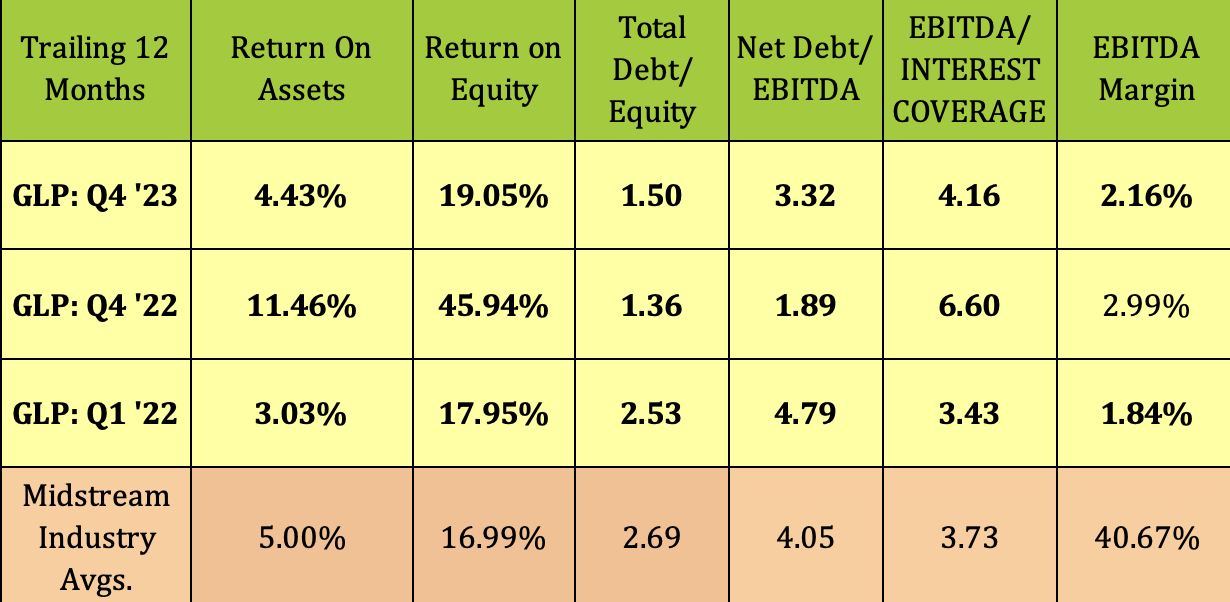

Once more, 2023 figures pale vs. these of 2022, with ROA and ROE down, and debt leverage up. Nonetheless, they evaluate properly vs. Q1 ’22, and vs. broad midstream averages, aside from EBITDA Margin.

Hidden Dividend Shares Plus

We checked out 2 considerably comparable corporations, Sunoco Logistics LP and Cross America Companions LP, each of whom even have C-Shops, and are lively in gasoline distribution.

All 3 corporations have very low EBITDA Margins, starting from 2.06% for CAPL, to three.53% for Sunoco. GLP’s ROA is in the midst of the group, whereas its ROE is decrease than the opposite 2 corporations.

On the plus aspect, GLP’s debt leverage ratios are a lot decrease, and its Curiosity protection is way increased than SUN and CAPL.

Hidden Dividend Shares Plus

Debt & Liquidity:

In January ’24, GLP accomplished a non-public providing of $450M in combination principal quantity of 8.250% senior unsecured notes due 2032. Administration intends to make use of the online proceeds used to repay a portion of the borrowings excellent beneath the credit score settlement and for common company functions.

In February ’24, GLP and its lender agreed to a reallocation of $300M of GLP’s revolving credit score facility to the working capital revolving credit score, to scale back the accordion characteristic from $200M. After the accordion discount, the working capital revolving credit score facility is $950M, and the revolving credit score facility is $600M, for a complete dedication of $1.55B, efficient February 8, 2024.

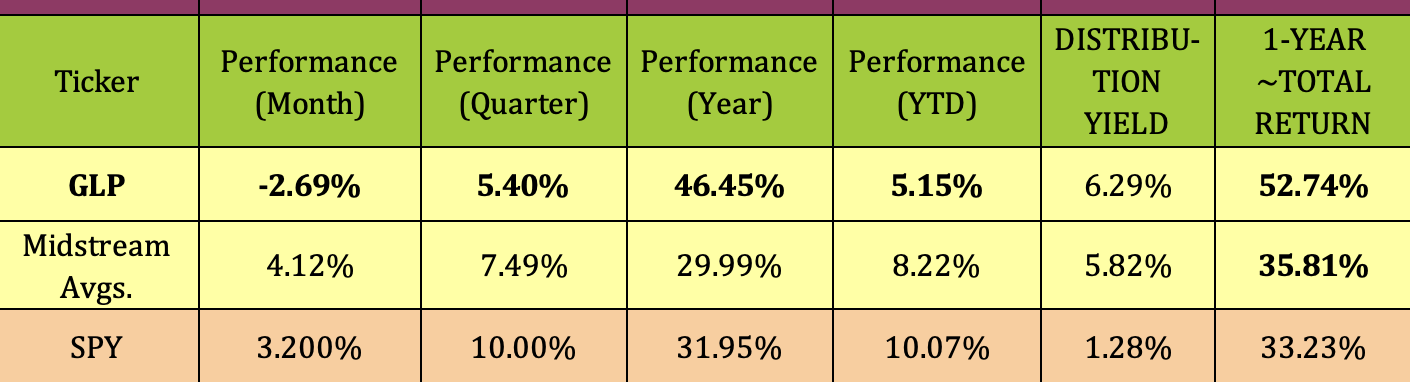

Efficiency:

GLP’s widespread items have had fairly a run over the previous 12 months, outperforming the Midstream Business and the S&P 500 on a value and complete return foundation.

Hidden Dividend Shares Plus

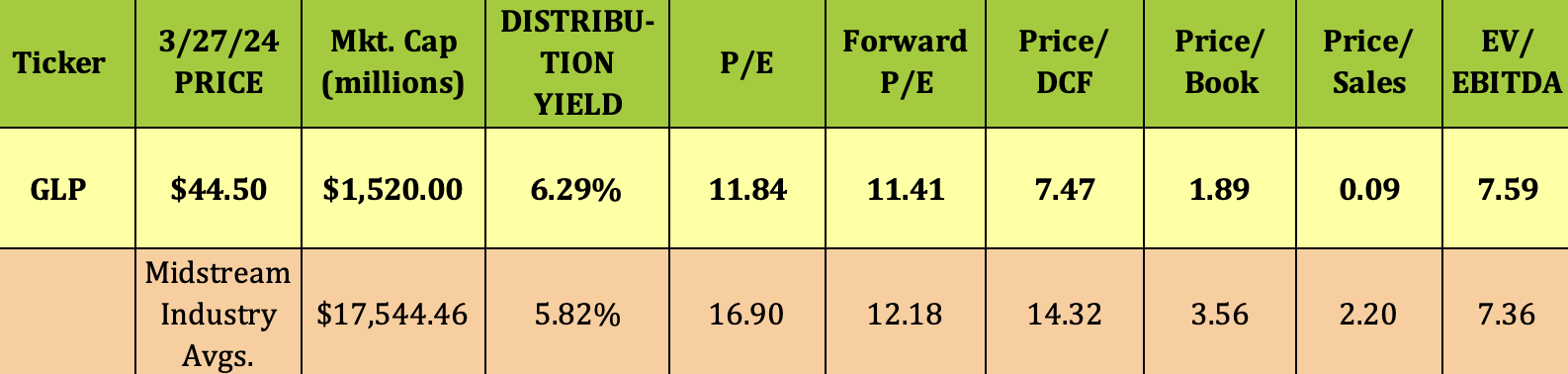

Frequent Unit Valuations:

At $44.50, GLP’s trailing P/E of 11.84X is way decrease than the 16.9X midstream business common, whereas its 2024 ahead P/E is roughly in step with the business common.

Nonetheless, GLP seems less expensive than midstream business averages on a Worth/DCF, P/Ebook, and P/Gross sales foundation. Its 6.29% dividend yield is a bit above common.

Hidden Dividend Shares Plus

Parting Ideas:

GLP seems oversold on its gradual stochastic chart, and is 10% under its 52-week excessive. The widespread items are 11% under avenue analysts’ $50.00 common value goal. We charge the GLP widespread items a Purchase, primarily based upon their engaging dividend yield, and GLP’s strong positioning in regional US gasoline distribution.