Olivier Le Moal

Funding Overview

The share value of Intra-Mobile Therapies (NASDAQ:ITCI) – the New York primarily based central nervous system targeted biotech – is up by 450% throughout a five-year interval, and >50% over a 12-month interval.

The corporate completed its preliminary public providing (“IPO”) again in 2014, elevating ~$100m through the issuance of ~$6.15m shares priced at $17.5 per share. In brief, Intra-Mobile has rewarded its shareholders handsomely since turning into a public firm.

Intra-Mobile’s success is essentially all the way down to its solely authorised drug to this point, Caplyta (lumateperone). Previous to the drug’s first approval in late 2019, Intra-Mobile shares had sunk to a low of $7.5, a close to 60% low cost to IPO value.

In response to the corporate’s 2022 10K submission / annual report:

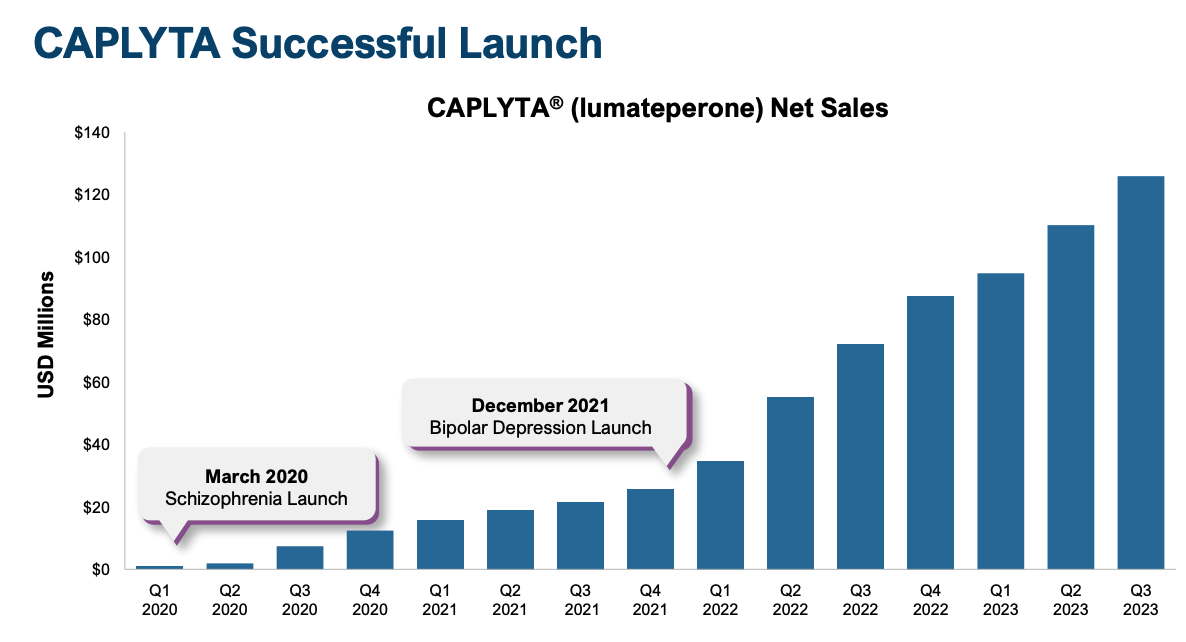

In December 2019, CAPLYTA was authorised by the FDA for the remedy of schizophrenia in adults (42mg/day) and we initiated the industrial launch of CAPLYTA in March 2020. In assist of our commercialization efforts, we make use of a nationwide salesforce consisting of roughly 370 gross sales representatives.

In December 2021, CAPLYTA was authorised by the FDA for the remedy of bipolar despair in adults (42mg/day). CAPLYTA is the one FDA-approved remedy for depressive episodes related to bipolar I or II dysfunction (bipolar despair) in adults as monotherapy and as adjunctive remedy with lithium or valproate.

We initiated the industrial launch of CAPLYTA for the remedy of bipolar despair in December 2021. As well as, the FDA authorised new dosage strengths, 10.5mg and 21mg, for particular populations of sufferers, in April 2022. We initiated the industrial launch for these particular inhabitants doses in August 2022.

In 2020, Caplyta drove revenues of $22.4m, in 2021, $81.7m, and in 2022, $249m. As spectacular as the expansion in revenues is, and the expansion within the share value over the identical interval – it ought to be famous that web losses in 2020, 2021, and 2022 respectively have been $(227m), $(284m), and $(256m).

Throughout the primary 9 months of 2023, Caplyta revenues have been $331m, however the firm reported a web lack of $(111m). In the end, if Intra-Mobile shares are to maintain monitoring upward, these losses will finally have to be transformed into earnings. However, it is clear that in lumateperone, Intra-Mobile has a strong and essential drug in its secure.

Lumateperone’s Journey To Pre-Eminence In CNS Issues

Not unusually for a drug addressing tough to diagnose, not to mention deal with, a situation akin to Schizophrenia, lumateperone’s path to approval concerned quite a few setbacks – a failed Part 3 research in 2016, which administration blamed on an unusually excessive placebo response (though risperidone, a drug authorised to deal with Schizophrenia since 1993 was in a position to outperform placebo), a cancelled FDA Advisory Committee assembly, and a 3-month postponement to the preliminary Prescription Drug Person Price Act (“PDUFA”) date – when the FDA declares its resolution on whether or not the drug has been authorised or rejected for industrial use.

The drug – licensed from Bristol Myers Squibb in 2014 – was finally authorised in December 2019 – in accordance with a press release on the time:

The efficacy of CAPLYTA 42 mg was demonstrated in two placebo-controlled trials, displaying a statistically important separation from placebo on the first endpoint, the Constructive and Damaging Syndrome Scale (PANSS) whole rating. The most typical hostile reactions (≥5% and twice the speed of placebo) for the really helpful dose of CAPLYTA vs placebo have been somnolence/sedation (24% vs.10%) and dry mouth (6% vs. 2%).

The efficacy of the drug is defined as follows in Intra-Mobile’s 2022 10K:

The efficacy of lumateperone may very well be mediated by means of a mixture of antagonist exercise at central serotonin 5-HT2A receptors and postsynaptic antagonist exercise at central dopamine D2 receptors.

By way of pharmacodynamics, lumateperone has excessive binding affinity for serotonin 5-HT2A receptors and reasonable binding affinity for dopamine D2 receptors, serotonin transporters, dopamine D1 receptors, dopamine D4 receptors and adrenergic alpha 1A and alpha 1B receptors.

It lacks biologically related interactions with different receptors together with muscarinic and histaminergic receptors. Consequently, we consider lumateperone might signify a possible remedy throughout a number of therapeutic indications.

For these (like me) who discover the above evaluation considerably technical and difficult to familiarize yourself with, I got here throughout a extra layman-friendly evaluation supplied by an article in Psychiatry Online in an article from 2020:

The agent (lumateperone) has attracted some optimism as a potential breakthrough in schizophrenia remedy as a result of it acts on glutamate receptors within the mind in addition to dopamine and serotonin receptors.

Most of the so-called “me-too” second-generation antipsychotics (“SGAS”) manufactured lately have acted on serotonin and dopamine solely; consultants agree that what is required to make a dramatic enchancment within the lives of individuals with schizophrenia are medicines that work on the mind in totally novel methods.

Clearly, prescribing physicians have seen constructive leads to sufferers, as, in accordance with a January investor presentation launched by Intra-Mobile, Caplyta skilled “exceptional Rx growth of ~85% in ’23 versus ’22”, and its gross sales efficiency since launch has additionally been distinctive, with progress in each consecutive quarter since launch.

Caplyta gross sales progress since launch (Intra-Mobile presentation)

The expansion has been supercharged by the next approvals the drug was in a position to safe in bi-polar dysfunction. In its approval statement, the FDA famous:

the efficacy of Caplyta 42 mg was established by demonstrating statistically important enhancements over placebo for the change from baseline within the Montgomery-Asberg Melancholy Score scale (MADRS) whole rating at week 6. Caplyta 42 mg additionally confirmed a statistically important enchancment in the important thing secondary endpoint regarding scientific world impression of bipolar dysfunction in every research.

Main Depressive Dysfunction – A Probability To Develop Label, Chase “Blockbuster” Gross sales

Administration’s guidance for full-year 2024 Caplyta revenues issued as of Q3 was for $460m – $470m of revenues, that means This autumn revenues ought to come back in ~$135m, representing one other sequential achieve, albeit solely by ~$10m, as revenues reported in Q3 have been $126.2m.

Full-year 2023 SG&A steerage was lowered to $405 – $420m, and R&D expense steerage to $185 – $200m, that means general losses will probably exceed $(150m), however will at the least be an enchancment on prior years.

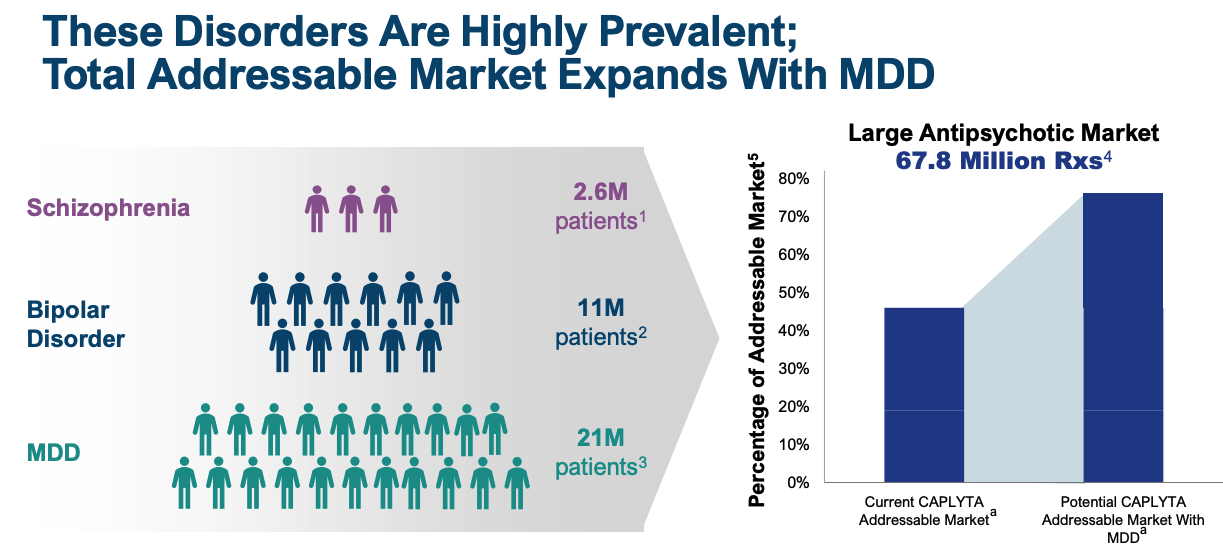

Intra-Mobile administration will probably really feel the SG&A spend is justified, given that there’s intense competitors within the schizophrenia area and nationwide promoting campaigns are required to keep up consciousness and hold tempo with the competitors. The R&D spend is even simpler to justify, as administration runs research supposed to safe approval in main depressive dysfunction (“MDD”), a sign and market that’s an order of magnitude bigger than Schizophrenia and Bipolar.

addressable market enlargement with MDD (intra-cellular presentation)

Intra-Mobile is working three Part 3 research supposed to gather the information required for a label enlargement into MDD, and knowledge from these three, whose endpoints are all the identical, being change in Montgomery–Åsberg Melancholy Score Scale (“MADRS”) whole rating at week 6, shall be out there this quarter and subsequent, administration has promised, introducing an intriguing near-term knowledge catalyst for potential buyers to think about.

Final 12 months, Intra-Mobile secured a notable win in a research evaluating lumateperone as a monotherapy in sufferers with MDD, with combined options and bi-polar despair with combined options, recording a statistically important enchancment on its main endpoint of enchancment on MADRS, and on the secondary endpoint of International Impression of Severity Scale (CGI-S).

Wall Road was delighted with the information, and the market despatched Intra-Mobile inventory surging from ~$45, to $65, when it was introduced final March. Analysts have speculated that Caplyta has peak gross sales potential of $4.3bn, with $1.3bn out there in MDD alone.

Aggressive Threats – Deep-Pocketed Rivals Might Hamper Development, Problem On Efficacy

With its present market cap of ~$7bn, it is clear that, if Caplyta fulfils Wall Road’s expectations and turn out to be a multi-billion promoting asset, the corporate would nearly actually benefit a double-digit billion valuation, and at last realise some earnings. For instance, a ten% web revenue margin on $4.3bn of revenues could be $430m, and if we speculate round a value to earnings ratio of 25x, we’re taking a look at a market cap of near $11bn.

The despair market is estimated to be price ~$16bn by 2030, subsequently Caplyta would want a 25% share to be able to fulfil optimist’s expectations, however is that this a real risk?

In its 2022 10K, Intra-Mobile lists its closest rivals as Vanda Prescription drugs (VNDA), and its schizophrenia drug Fanapt, Alkermes (ALKS) (my Searching for Alpha note here), and schizophrenia / bipolar drug Lybalvi, Otsuka Pharma’s Rexulti, and AbbVie’s (ABBV) Vraylar, indicated for MDD, schizophrenia, and bipolar.

Vraylar racked up almost $2.7bn of revenues in 2023, up 29% from the $1.97bn earned within the prior 12 months. AbbVie administration is assured Vraylar can obtain peak revenues of ~$5bn every year, and with its a lot bigger gross sales and advertising infrastructure, the Huge Pharma will probably have the ability to considerably outspend Intra-Mobile with regards to TV advert campaigns, doctor and affected person consciousness applications and many others.

Moreover, AbbVie lately spent $8.7bn buying Cerevel Therapeutics and its portfolio of CBS medicine, together with emraclidine, which AbbVie refers to as “a positive allosteric modulator (PAM) of the muscarinic M4 receptor, a potential best-in-class, next-generation antipsychotic that may be effective in treating schizophrenia patients”.

Sage Therapeutics (SAGE), regardless of a number of late-stage mishaps, continues to be making an attempt to deliver zuranolone to market in MDD, whereas Axsome Therapeutics’ (AXSM) auvelity was authorised in late 2022 for remedy of despair.

Lastly, decrease priced generic competitors stays a menace to Caplyta gross sales (and certainly Vraylar gross sales) – Intra-Mobile mentions in its 10K that “lumateperone has five years of new chemical entity data exclusivity with the FDA, until December 2024”, which suggests generic variations of the drug might turn out to be out there subsequent 12 months, though the corporate has many extra patents, with the earliest expiration talked about being 2028.

Both method, finally, Intra-Mobile might want to various away from its extremely profitable drug Caplyta, and that shall be extraordinarily difficult.

Intra-Mobile’s Pipeline – No Apparent Close to-Time period Help For Lead Drug

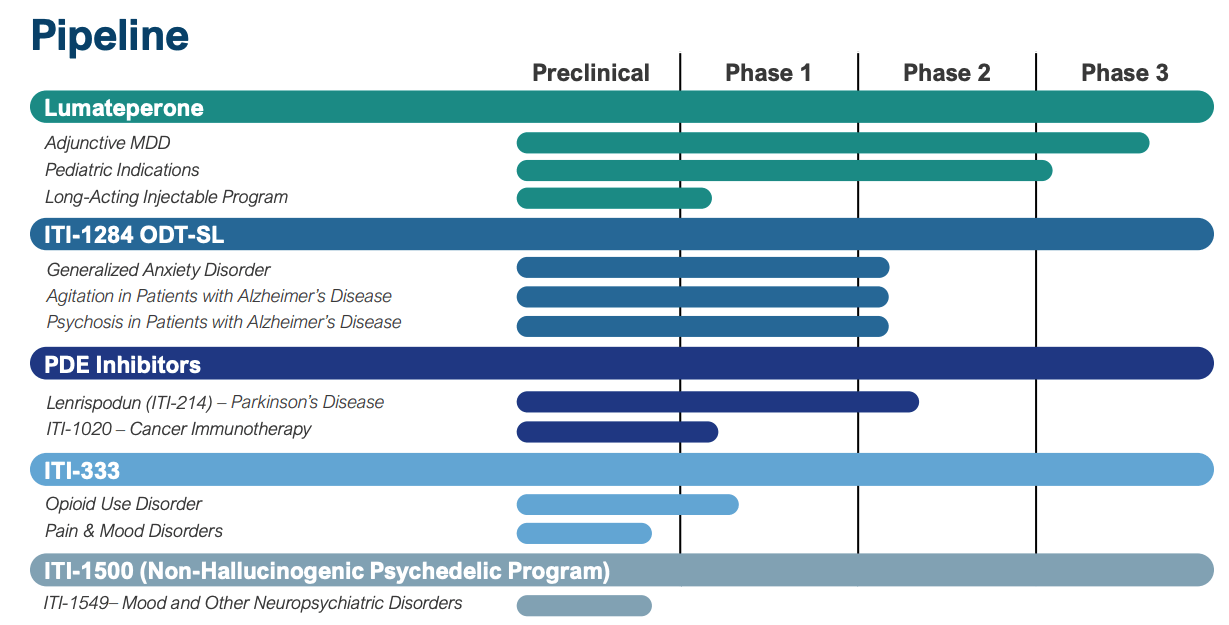

Intra-Mobile does have a various drug improvement pipeline, as we are able to see under:

Intra-Mobile pipeline (presentation)

There are undoubtedly some intriguing belongings right here – my consideration is drawn to its PDE inhibitors, and Parkinson’s Illness – an space the place present remedy choices are broadly unsatisfactory – nevertheless it should be acknowledged that none of Intra-Mobile’s belongings are present process pivotal research, and lots of the goal indications are extraordinarily difficult to deal with e.g. Alzheimer’s agitation and psychosis and most cancers – a discipline by which the corporate has restricted expertise.

Maybe probably the most intriguing asset in Intra-Mobile’s pipeline is its long-acting model of lumateperone, which, if authorised, wouldn’t solely enhance on its current drug, which is run orally each day, but in addition open up the potential for a recent interval of patent exclusivity, defending Caplyta revenues long-term.

Concluding Ideas – A Purchase Right now On Approval Catalysts, Rising Gross sales, However Lengthy-Time period Future Appears to be like Unsure

One pivotal trial miss in 2016 apart, Caplyta has carried out nicely in a number of late stage scientific research which has resulted in a number of main approvals and a market alternative that raises the prospect not solely of “blockbuster” gross sales (>$1bn every year), however in Wall Road’s eyes, annual revenues within the multi-billions of {dollars}.

It is clear that Intra-Mobile is struggling to unlock profitability from an asset that’s delivering robust progress in its goal markets, though losses are narrowing, and if an approval in MDD is secured, the enhance to revenues shall be much more important than that supplied by the bipolar approval.

Competitors is fierce, however Caplyta seems to be as if it may well maintain its personal in opposition to all authorised present challengers in its market, even when which means sustaining a excessive advertising spend, and with MDD research readouts imminent, this doesn’t look a foul time to be holding Intra-Mobile inventory. With its observe report of constructive knowledge readouts, there’s a good likelihood that shares can discover much more upside as Wall Road celebrates a transparent path to market in MDD.

Longer-term, I harbour some doubts about Intra-Mobile’s capacity to information its pipeline belongings by means of the approval course of, and stay aggressive into the following decade, and plainly, from an M&A perspective, Huge Pharma has shied away from making a bid for the corporate, preferring the likes of Cerevel, or Biohaven, for instance (acquired for $12bn by Pfizer final 12 months), which could recommend it doesn’t see long-term blockbuster income potential, maybe after patents expire.

Within the right here and now, nevertheless, bolstered by almost $500m in money and no debt, the temptation to take a place within the firm because it prepares to launch MDD knowledge is excessive – though I’m not positive I might fee the corporate as a long-term “buy and hold”.