Eva-Katalin/E+ via Getty Images

Investment Thesis

Intuit (NASDAQ:INTU) stock sold off, as the company’s guidance was weaker than expected. That’s the thing that the market has latched onto.

But details matter. For one, yes, the market saw that Intuit’s EPS for the next 90 days was weaker than expected and investors ran for cover.

Moreover, although Intuit’s balance sheet carries $6 billion of debt, Intuit also carries slightly over $4.5 billion of cash, which given that Intuit is so cash flow generative, supports my argument that this company’s balance sheet is on solid footing.

But the crux of this thesis is that I argue that Intuit is still a robust growth company. And given its strong upward revised revenue growth outlook for fiscal Q4 2024, this implies that its momentum bodes well for its growth rates to continue into fiscal 2025.

In sum, I believe that paying 32x forward non-GAAP EPS is entirely justified for this high-quality company.

Why Intuit? Why Now?

Intuit provides financial management tools for individuals and small businesses. Its popular products include TurboTax for tax preparation, QuickBooks for accounting, and Credit Karma for credit monitoring and financial planning. Intuit uses user-friendly digital solutions to simplify financial tasks, making it easier for users to manage their money, file taxes, and grow their businesses.

During its earnings call, Intuit highlighted its Small Business and Self-Employed Group, a key growth driver, which saw an 18% y/y revenue increase, underscoring the platform’s essential role in empowering small businesses, even amid macroeconomic uncertainties.

This growth is bolstered by successful innovation within its products, such as TurboTax and Credit Karma, which have seen significant user engagement and financial performance improvements. Also, Intuit once again makes the case that its AI-driven platform strategy is central to its growth, with innovations like TurboTax Live expected to grow by 17% in fiscal 2024.

And yet, Intuit also faces some headwinds. For example, one challenge lies in the competitive landscape of tax preparation, with various free alternatives available. To which, Intuit retorts that it’s actively choosing to focus on higher-value customers over pay-nothing budget-conscious users, even if that reduces its total addressable market.

Given this background, let’s now get to why the stock moved down on the back of its earnings results.

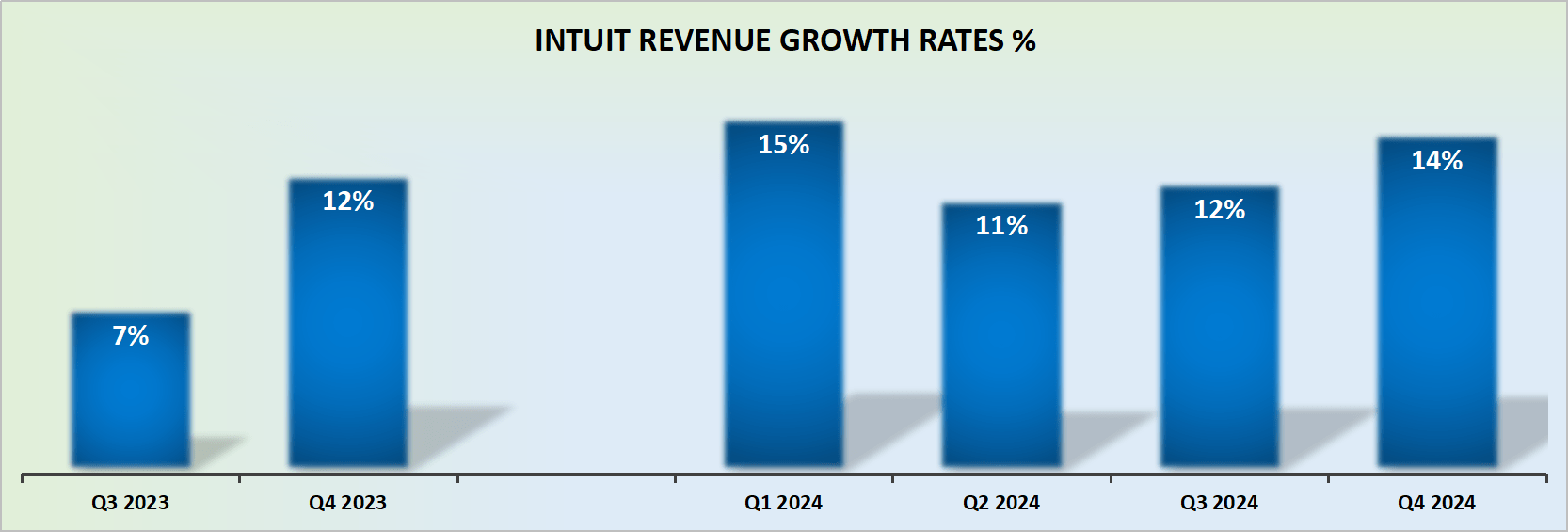

Revenue Growth Rates Remain Strong

INTU revenue growth rates

Intuit’s share price dropped on the back of a very poor trading session. Yes, the stock is far from cheap and investors were looking for any reason to sell and take profits off the table, and this earnings report was the catalyst.

But over the medium term, there’s still a lot to like about Intuit. For one, despite being on a path toward $17 billion of annualized revenues, this business is still delivering very stable low teen growth rates, a feat that few companies achieve.

Furthermore, despite going against a tough comparable with the prior year, Intuit’s fiscal Q4 guidance points to 14% y/y growth rates.

Consequently, it appears possible that at the present run-rate, Intuit’s revenue growth rates in fiscal 2025 could reach around 12% to 13% CAGR. Admittedly, this isn’t all that different from analysts’ expectations for next year, but at the same time, this should reassure investors that there’s no ‘actual’ bad news in this report.

So why did the stock sell-off? That’s what we discuss next.

INTU Stock Valuation — 32x Forward EPS

Here’s the thing, Intuit’s EPS guidance for fiscal Q4 2024 points to $1.85 of EPS at the high end, which is lower than what analysts were expecting to see around $1.92.

However, if rather than getting overly caught up on how the next 90 days are performing, we take a more holistic look at fiscal 2025 (starting August 2024), I believe that Intuit could be on a path towards $19.55 of EPS.

This would leave its stock priced at 32x forward non-GAAP EPS. Yes, this isn’t the cheapest stock in the market. Indeed, there are plenty of cheaper small-cap stocks that are worthwhile considering.

But for investors don’t want to put up with significant volatility, parking their capital with Intuit isn’t such a bad suggestion.

The Bottom Line

In conclusion, I believe Intuit’s stock is reasonably priced at 32x forward non-GAAP EPS due to several key financial strengths.

Despite a weaker-than-expected EPS forecast for the next 90 days, it delivers robust cash flow plus has a solid balance sheet, underscoring its financial stability.

Furthermore, looking ahead, its revenue growth rate is expected to be around 12-13% in fiscal 2025, supporting the argument that its current valuation reflects its medium-term growth potential. I believe there’s a lot to like here and that the market reaction was unjustified.