-Oxford-

In May, I believed that Intuit (NASDAQ:INTU) was a stable firm, however that it appeared pretty valued. I adopted that up in July, saying the corporate’s early foray into AI may assist it achieve investor consideration, however that it was buying and selling at ranges above its massive software program friends. With the refill about 45% since my preliminary write-up, let’s catch-up on the identify.

Firm Profile

As a refresher, INTU supplies monetary administration and compliance software program for each small companies and shoppers. Its Small Enterprise & Self-Employed Section is its largest phase at over 50% of its working earnings and consists of QuickBooks and Mailchimp. The previous is used for duties equivalent to payroll options, time monitoring, and service provider cost processing options. Mailchimp, in the meantime, supplies e-commerce, advertising automation, and buyer relationship administration options.

INTU’s Shopper phase is headlined by shopper earnings tax preparation software program Turbo Tax and accounts for over a 3rd of its enterprise. Private finance web site Credit score Karma, which identified for its credit score and monetary administration platform, and ProTax, are its two smallest segments, every representing underneath 10% of its enterprise.

Fiscal Q1 Outcomes

INTU begin its fiscal yr on the fitting foot with a powerful fiscal first quarter when it reported its outcomes on the end of November.

For the quarter, income rose 15% to $2.98 billion. That topped analyst estimates calling for income of $2.86 billion.

Its Small Enterprise and Self-Employed phase noticed income climb 18% to $2.3 billion. Throughout the phase, QuickBooks income jumped 19% led greater by buyer progress, greater costs, and blend shift. On-line Service income rose 20%, led by Mailchimp and progress in payroll and funds. Worldwide income grew 16% on a continuing foreign money foundation. Section working earnings rose almost 26% to $1.49 million.

INTU’s two tax segments each noticed stable progress throughout what’s the tax extension interval. Shopper income surged 25% to $187 million, whereas ProTax income climbed 24% to $42 million. Shopper working earnings rose 31% to $67 million, whereas ProTax working earnings was $14 million, a 56% improve.

Income in its Credit score Karma phase sank -5% to $405 million. The corporate mentioned it noticed headwinds associated to non-public loans, auto insurance coverage, house loans, and auto loans. Credit score Karma working earnings, nonetheless, rose 13% to $106 million.

Adjusted EPS rose 49% to $2.47. That simply topped the consensus by 47 cents.

Working money move for the quarter was -$97 million, whereas free money move was -$181 million.

Turning to the steadiness sheet, INTU ended Q3 with almost $2.3 billion in money and short-term investments. It had almost $5.9 billion in debt.

Wanting forward, INTU forecast Q2 income to develop between 11-12%. It’s searching for adjusted EPS of between $2.25-2.31.

For the total yr, the corporate is projecting income to develop by 11-12% to between $15.89-$16.105 billion. It expects its Small Enterprise and Self-Employed phase to develop income by 16-17%, whereas it’s searching for its Shopper Section to see gross sales progress of 7-8%. Credit score Karma is forecast to see between -3% to +3% progress, whereas ProTax is projected to develop by 3-4%.

INTU guided for full-year adjusted EPS of between $16.17-16.47, representing progress of 12-14%. The analyst consensus on the time was for adjusted EPS of $16.39.

Administration famous that it was being prudent with steering given the uncertainty with the macroenvironment. On its FQ1 convention name, the corporate famous additionally that it’s testing GenAI throughout its merchandise to raised serve clients.

At a Nasdaq Investor convention earlier this month, CEO Sasan Goodarzi talked in regards to the levers the corporate is utilizing to drive progress, saying:

“There are 3 big levers that we have. One is new customer growth because our goal is to make it so simple and so easy that you’re willing to switch from your manual method to be able to run your business. … The second is breakthrough adoption. So if you think about the capabilities that we provide for small businesses, like growing your business with Mailchimp, like managing your money with payments, managing our workforce with payroll. Now with Intuit Assist, which is what we’re calling the assistant in your pocket, in essence, at the moment of truth, we’re engaging small businesses. And so we’re letting them know, hey, it looks like by 30 days from now, you’re going to run out of cash. You have 3 options. We can help you follow through with these 10 overdue invoices. You can click here, and we’ll give you access to capital. By the way, you can get a loan based on these 10 outstanding invoices. These are real examples, but these things drive benefit for the customer and use of our services. So penetration of services is a huge opportunity for us. And then the third element is what I mentioned earlier, which is it’s a connection to live expertise. So this is a great opportunity where we can share with the customer, hey, we can connect you to a human expert to be able to get advice on whether or not you should hire more employees, whether or not you should buy more inventory. That’s a monetizeable event for us because it’s a higher paid SKU. And last but not least, we’re also testing with offerings and SKUs that are just about what AI, particularly GenAI can offer, which is we’ll do it for you and with you.”

INTU has been performing effectively, led by sturdy outcomes from QuickBooks. This comes regardless of a troublesome macro atmosphere for SMBs, which has seen corporations tied to smaller corporations lately stumble, equivalent to BILL Holdings (BILL), and Paycom (PAYC).

Among the profit QuickBooks is seeing is from the corporate transitioning clients away from desktop. It’s also persevering with to push value on Desktop merchandise throughout this course of. The corporate is two-thirds of the best way by way of this course of, so this needs to be the final fiscal yr the place it advantages from this transition.

Nonetheless, extra importantly, it’s gaining extra clients and seeing extra of the purchasers undertake payroll and cost options. Given its stable progress, it seems to be gaining some market share in these areas. Its continued innovation in GenAI and connections to dwell consultants ought to assist to proceed to energy it going ahead.

Credit score Karma continues to be a little bit of a income drag, nevertheless it did present indicators of stabilizing, bettering upon current outcomes over the previous few quarters. The corporate is within the means of attempting to maneuver customers from its free Mint service, which it’s shutting down, to Credit score Karma. This might assist the phase because the yr progresses.

Valuation

INTU inventory at the moment trades round 27.4x the FY2024 (ending July) consensus EBITDA of $6.46 billion and 24x the FY2025 consensus of $7.40 billion.

It trades at a ahead PE of almost 38x the FY24 consensus of $16.40, and almost 33x the FY25 consensus of $18.80.

Income progress is anticipated to be up over 11.6% in fiscal 2024 and up a 12.5% in fiscal yr 2025.

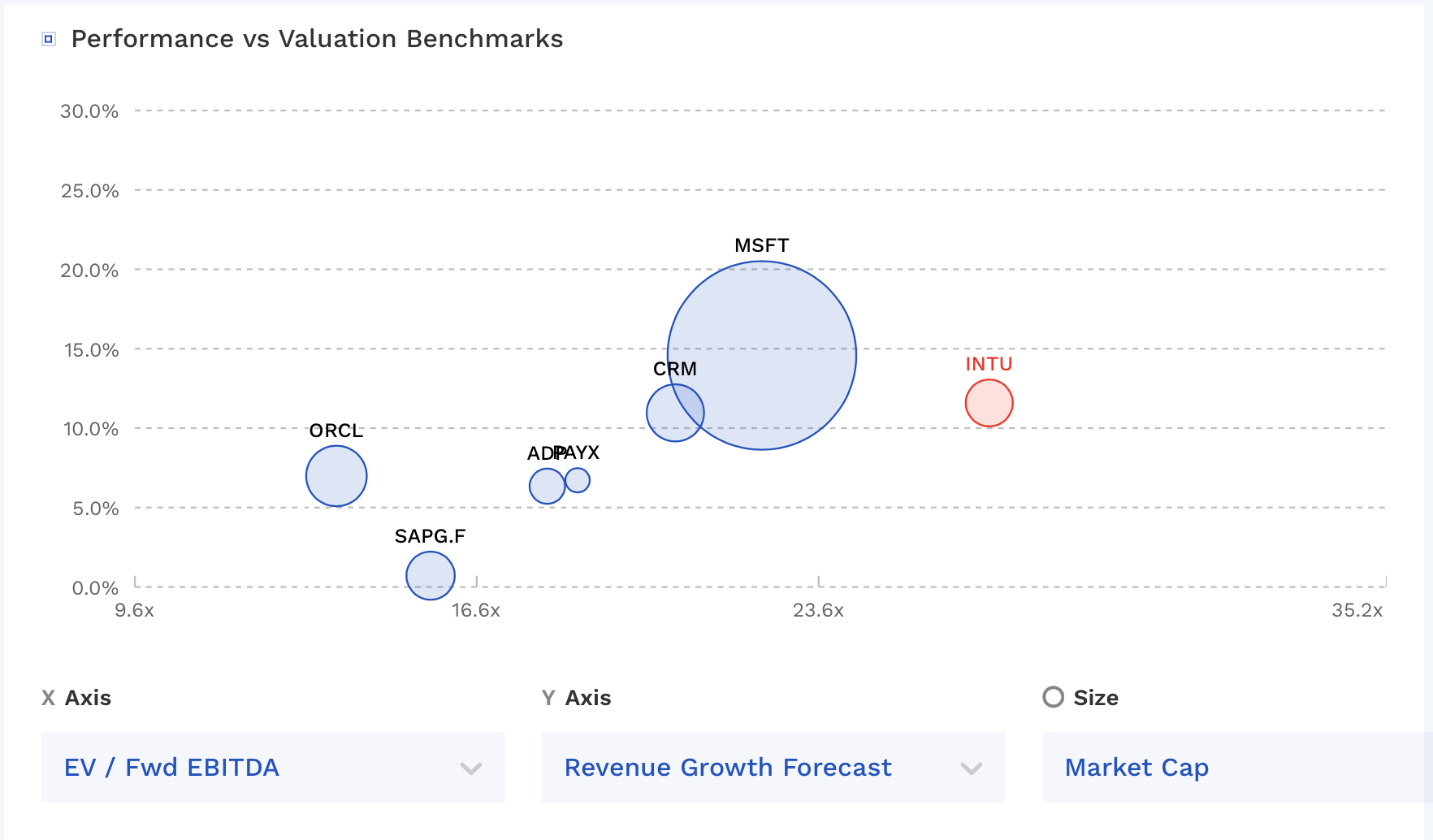

The inventory trades in the direction of the excessive finish of the place different massive software program companies commerce.

INTU Valuation Vs Friends (FinBox)

A 20-22x a number of on FY25 income, which is the place Microsoft (MSFT) and Salesforce.com (CRM) commerce with related or higher progress, can be $500-560 inventory.

Conclusion

INTU is performing very effectively, and seems to be taking share with its QuickBook product, in addition to benefiting from its ongoing transition away from Desktop. On the identical time, Credit score Karma is stabilizing, and its Tax choices are stable.

That mentioned, with the inventory buying and selling at a a number of effectively above friends, even these with higher income progress equivalent to MSFT, I really feel INTU’s inventory has gotten a little bit forward of itself by way of valuation. As such, I’m impartial on the identify with a $550 goal value.