Peach_iStock

The inventory market, led by the Dow, goes parabolic because it inflates on helium compelled into the monetary system by the Fed. The bubble has turn into extra manic and all-encompassing than the late Nineties dot.com/tech bubble, which was led by the Nasdaq. This time across the Dow is main the pack and has turn into irrationally exuberant.

Whereas this might turn into much more insane to the upside, the sentiment and degree of speculative exercise are again to ranges traditionally indicative of a prime. Wednesday’s (December twentieth) sudden, sharp reversal within the inventory market is probably going a warning shot – tremors earlier than an even bigger earthquake. Retail buying and selling accounted for 30% of the entire buying and selling quantity on Friday, in comparison with the 30-day common of 10%. Quantity in sub-$1 shares is surging, reflecting an excessive diploma of risk-taking. Nevertheless it’s not simply the penny shares. The meme shares like CVNA and SNAP are going parabolic.

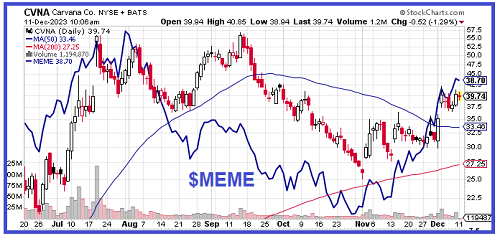

A protracted-time subscriber requested me how I clarify the large transfer greater in CVNA as a result of it’s fairly clear CVNA will ultimately must file for chapter. I requested him to have a look at this chart to inform me:

The chart plots CVNA (candlesticks) vs the MEME inventory ETF (MEME) (blue line). Observe the robust correlation between MEME and CVNA. In truth, what does it say about CVNA that it has been underperforming MEME within the transfer greater that started in early November. Each retail fool buying and selling on this market is chasing the worst rubbish shares greater. A lot of the shares in MEME have a really excessive quick curiosity. Most can be bankrupt throughout the subsequent three years.

Lengthy positioning by CTAs is at its most excessive degree in at the least eight years. Excessive lengthy or quick positioning by CTAs is a extremely dependable contrarian indicator. The VIX is at its lowest degree since mid-January 2020. Additionally, the weekly survey by the Affiliation of American Particular person Buyers (excessive internet price, retail) exhibits that bullish sentiment jumped as much as 51.3% by means of Wednesday, its highest degree since July nineteenth. At 19.3%, the share of bears is at its lowest over that very same interval.

Nobody can say for sure when this insanity will reverse. However we will say for sure that it’s going to, and when it does, the following sell-off will probably be brutal. Although I took a beating over the past three weeks in my put portfolio and closed out many of the positions. I proceed to carry January CVNA $50 places, AN January $125 and $130 places, NVDA March $435 places and TSLA April $220 places. As well as, on Friday I began a place in IWM (Russell 2000 ETF) late December $195 places. Earlier within the week I began shopping for late January SNAP $16.5 places. Check out SNAP’s chart [next page] to grasp why. Oh, I additionally maintain January GDDY $100 places.

C’mon, man. For its Q3, SNAP’s operations misplaced $380 million. By means of 9 months, it’s incurred a $1.14 billion working loss. The one purpose this Firm remains to be in enterprise is that the capital markets have enabled it to lift over $4.8 billion by way of convertible bonds between 2019 and 2022. It didn’t problem any debt in 2023. However the one factor conserving SNAP from going out of enterprise is the $3.4 billion in money it had on the finish of Q3 2023.

The inventory gapped up on November 14th when it was reported that SNAP signed a take care of AMZN that permits AMZN to run advertisements on SNAP which lets SNAP customers store on AMZN and take a look at with out exiting the SNAP app. The financial phrases related to the settlement weren’t disclosed, which implies that the phrases don’t immediately generate revenues from the settlement for SNAP. By way of the monetary advantage of this deal for SNAP, the one factor I may dig up after scouring articles and studies is that the deal may enhance common consumer time on the SNAP app which could allow SNAP to cost greater promoting charges.

In my view, SNAP is price not more than the worth per share of the money on its stability sheet, which is able to deplete over time. At present, it has $2.42/share in money. In some unspecified time in the future, I plan to extend my capital dedication to SNAP places past the January $15.50 places I’ve now.

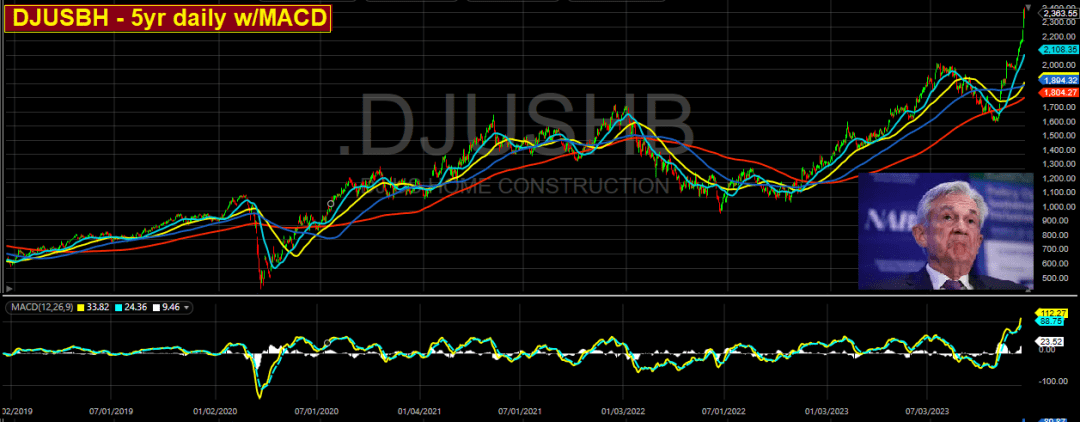

Housing market replace – The homebuilder and residential building shares have gone completely parabolic:

The Dow Jones Dwelling Development Index has soared 17% because the finish of November. The MACD momentum indicator is by far at its most overbought studying within the historical past of the index (2000).

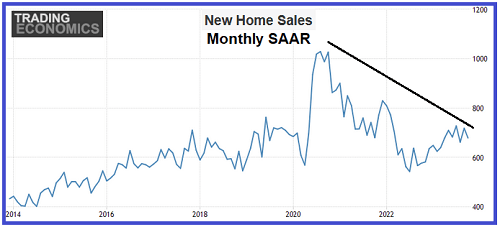

However whereas the homebuilders have been growing deliveries by way of the usage of heavy worth reductions and different incentives, they aren’t reporting file ranges of revenues and profitability. And the contract worth of their order backlogs is plummeting. And right here’s the 10-year image of the month-to-month seasonal adjusted annualized charge for brand new residence gross sales:

Whereas new residence gross sales bounced after declining for almost two years, total, the speed of recent residence gross sales has been in a steep downtrend since late 2020. In different phrases, the differential between the market cap of the homebuilders and their profitability could also be on the widest in inventory market historical past. The DJUSHB is 2.4x greater than it was on the peak of the early 2000s housing bubble whereas the SAAR peaked at over 700k again then in comparison with the present SAAR of 679k. I consider that actuality will hit the inventory market arduous in 2024 accompanied by a swift sell-off within the homebuilder shares.

Lennar (LEN – $149) reported its FY This fall and full-year numbers on Thursday after the shut. Regardless of “beating” income and EPS consensus, in addition to the anticipated FY Q1 2024 forecast, the inventory dropped 3.6% Friday. It’s because it was obvious to the market that LEN sacrificed margins by reducing costs and providing fats incentives.

Whereas This fall revenues rose YoY 7.9%, working earnings rose simply 4.8%. Ordinarily, in a wholesome working setting, homebuilders would profit from economies of scale and working earnings would rise percentage-wise greater than revenues. However the ASP declined 8.7%. This doesn’t embody incentives like charge buy-down loans and architectural upgrades.

LEN’s share worth has soared 42% because the finish of October. I’d be an fool if I didn’t admit that I want I had purchased calls 7 weeks in the past. However the enhance in market cap shouldn’t be in any means remotely justified by fundamentals.

The worth of LEN’s backlog, regardless of a 4.3% enhance in new unit orders, plunged 24%. The ratio of LEN’s market cap to the worth of the backlog is 6.4. A yr in the past, this ratio was 2.98. This illustrates the diploma to which LEN’s market worth has turn into utterly unhinged from actuality.

Whereas the builders loved a bounce in gross sales throughout 2023 due to charge buy-down gimmicks in addition to different tweaks to mortgage phrases that decrease the associated fee for the primary two years, with the “savings” added to the back-end price of the mortgage, plus big worth, and improve incentives, I’ve little doubt that homebuilders face a tricky 2024.

Editor’s Observe: The abstract bullets for this text have been chosen by Looking for Alpha editors.