Melpomenem

By Bradley Krom

The potential for cussed inflation, a higher-for-longer coverage from the Federal Reserve, and structural $1 trillion deficits have all contributed to an irregular form within the U.S. Treasury curve. On this piece, we glance to different durations of curve inversion and conclude that inverted yield curves are usually not an obstacle to fairness returns. For mounted earnings, the affect is extra nuanced and is dependent upon when the Fed stops mountaineering charges.

In a “normal” bond market, the yield curve slopes upward. The structural driver of this yield premium is that investing turns into riskier the additional you get into the long run. In right this moment’s markets, short-term charges want to stay excessive to tamp down inflation, however sooner or later, the Fed is more likely to lower charges as soon as the storm has handed.

At the moment, traders can lock in the next price of return in alternate for the chance that charges might fall sooner or later. During the last 35 years, the U.S. skilled an inverted yield curve in 5 distinct durations, which we’ve reviewed from the preliminary inversion of the two-year versus the 10-year Treasury till that a part of the curve in the end shifted again into optimistic territory on a sustained foundation.

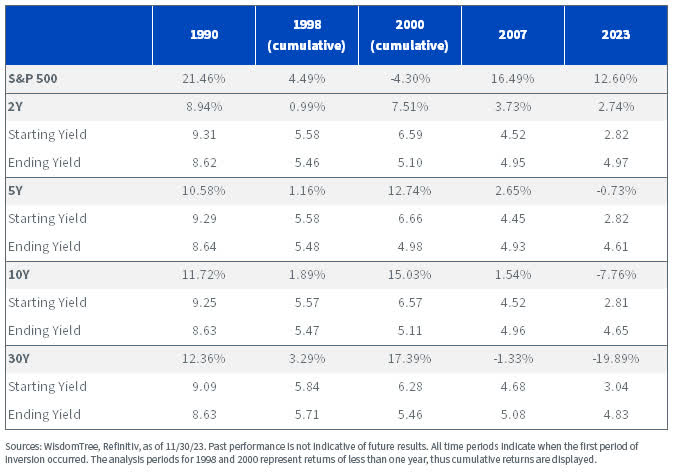

Whole Returns vs. Bond Yields

Massive Image

In each episode of yield curve inversion besides 2007 and the present episode (2023), bonds delivered optimistic complete returns because of falling charges. The problem right this moment is that not solely have bond yields risen dramatically throughout the curve, however they had been at a lot decrease ranges when the inversion occurred.

Aside from 2000, equities considerably outperformed mounted earnings on this surroundings regardless of the implication that inverted yield curves sign a looming recession.

The clear implication for 2023 is that longer period has underperformed quick period whereas the curve has been inverted due primarily to rising charges versus decrease ranges of carry. Nevertheless, until traders count on this atypical interval to persist, they should take into account when to start out positioning for the final word pivot from the Fed.

In our view, the important thing issue that is driving inversion is that short-term rates of interest are too excessive. Any alerts from the Fed that it might be inclined to start out chopping charges have resulted in large rallies for the lengthy finish, which has boosted complete returns. Whereas this may occasionally not lead to an upward-sloping curve instantly, traders can have locked-in charges not seen because the early 2000s.

We additionally distinction this with above-average fairness efficiency throughout an inverted yield curve surroundings as a chance to de-risk. Nevertheless, this view additionally is dependent upon timing, which we focus on throughout particular durations of curve inversion under.

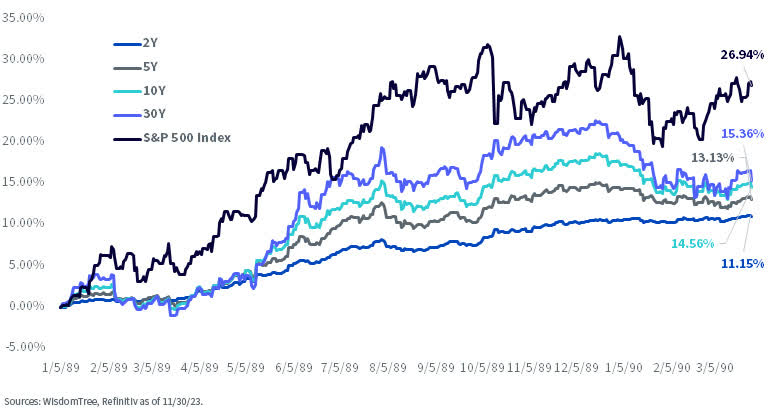

Cumulative Returns: 1/5/89-3/29/90

Throughout this era with a flat/inverted curve, mounted earnings skilled much less important drawdowns on account of upper beginning yields. Because the Fed began chopping charges in July 1989, period began to outperform in a giant approach. The fairness market additionally rallied strongly because the Fed moved away from restrictive coverage. Nevertheless, the U.S. tipped into recession in July 1990, which additional favored allocations to mounted earnings versus equities.

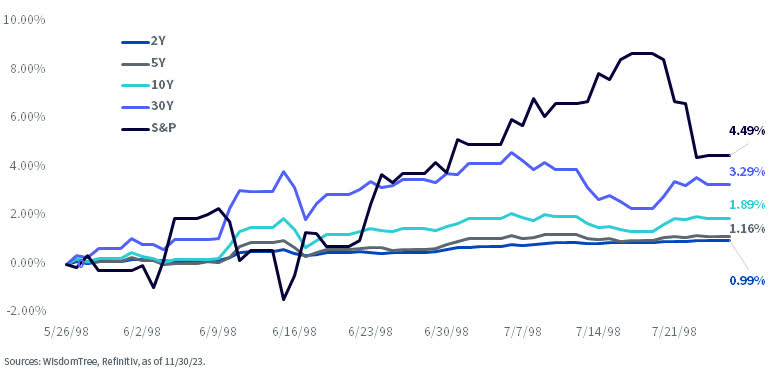

Cumulative Returns: 5/26/98-7/26/98

It is exhausting to attract too many conclusions from this era of inversion on account of the quick interval (two months), however mounted earnings delivered optimistic complete returns over the complete interval, albeit at a lot smaller ranges since modifications in yields had been the first driver versus earnings. Whereas equities delivered the very best complete returns, this got here at the price of a way more risky trip.

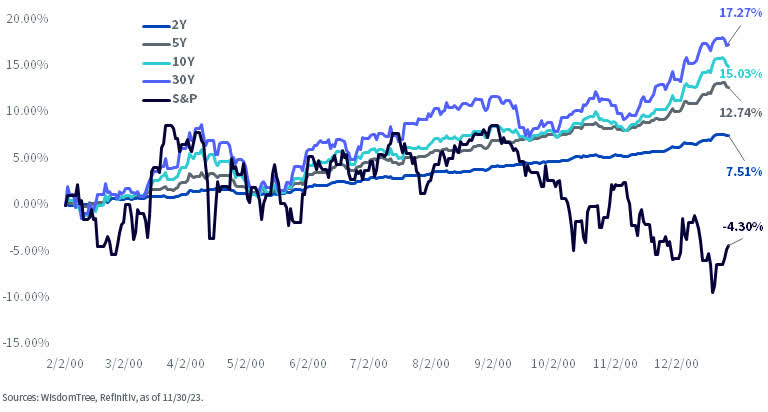

Cumulative Returns: 2/2/2000-12/28/2000

This era coincided with the height of the dot com bubble in March 2000 and is probably essentially the most anomalous for the present surroundings. Frothy fairness markets in the end resulted in a pullback for shares whereas longer-term Treasuries rallied. After a ultimate price hike in July 2000, Treasuries then proceeded to rally because the Fed switched to a impartial coverage. It could be doable that we see an identical response in December 2023.

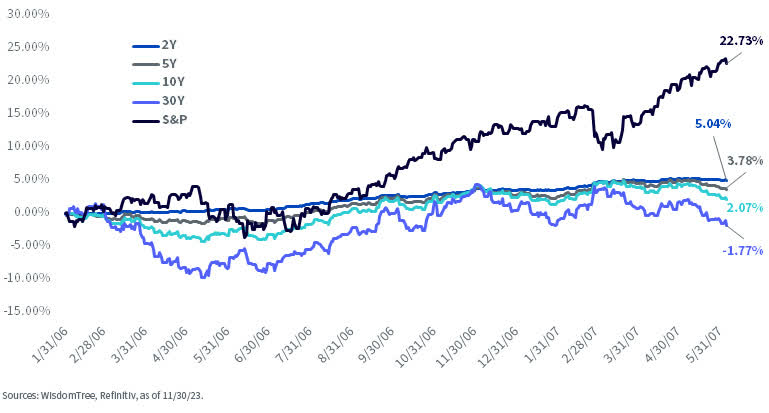

Cumulative Returns: 1/31/06-6/5/07

This era is marked by the most important outperformance for equities mixed with normal underperformance within the bond market, significantly within the lengthy finish. The Fed has been steadily tightening coverage since 2004 in a measured, predictable style. In response, bonds usually languished whereas equities continued to run.

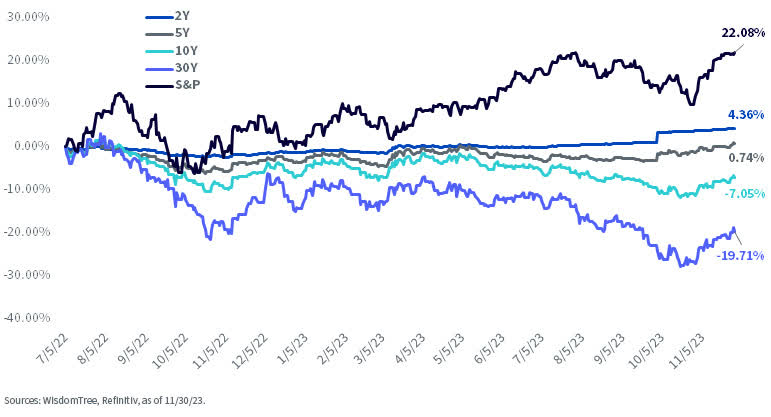

2022-2023

As most traders have been painfully conscious, the lengthy finish of the Treasury curve has massively underperformed. The large distinction throughout this era is that regardless of a modest steepening within the yield curve, the unfold between 2-year and 10-year charges has remained inverted at 35 foundation factors, which contrasts with the opposite historic analyses.

For relative worth traders, the important thing query comes right down to how way more divergence can happen between long-term bonds and equities. Whereas the timing of that imply reversion is open for debate, given the practically unprecedented dislocation, it might make sense to make this commerce earlier than the Fed absolutely alerts that charges might be falling.

Locking in a complete return of practically 4.5% for 10 years with the added upside potential of falling charges is turning into a extra engaging commerce, significantly if inflation falls sooner fairly than later.

Cumulative Returns: 7/5/22-11/30/23

Conclusion

When the yield curve inverts, assumptions in regards to the bond market get turned on their heads. Whereas equities can usually tolerate inversion higher than bonds, we all know that markets are dynamic and nothing lasts eternally. In gentle of latest underperformance, it might make sense to start out shifting the period of investor portfolios to reap the benefits of an eventual shift from the Fed.

In our view, any investor with publicity to a 60/40 allocation ought to take into account the WisdomTree U.S. Efficient Core Strategy (NTSX) as a substitute. With mounted earnings offering a lot greater yields, we’re extra optimistic in regards to the capability of the technique to generate returns that differ from a 100% fairness allocation given the unsure outlook for equities heading into 2024.

Necessary Dangers Associated to this Article

There are dangers related to investing, together with the doable lack of principal. Whereas the Fund is actively managed, the Fund’s funding course of is predicted to be closely depending on quantitative fashions and the fashions might not carry out as meant. Fairness securities, similar to widespread shares, are topic to market, financial, and enterprise dangers which will trigger their costs to fluctuate. The Fund invests in derivatives to realize publicity to U.S. Treasuries. The return on a spinoff instrument might not correlate with the return of its underlying reference asset. The Fund’s use of derivatives will give rise to leverage and derivatives may be risky and could also be much less liquid than different securities. Consequently, the worth of an funding within the Fund might change rapidly and with out warning and you might lose cash. Rate of interest threat is the chance that fixed-income securities, and monetary devices associated to fixed-income securities will decline in worth due to a rise in rates of interest and modifications to different components, similar to notion of an issuer’s creditworthiness. Please learn the Fund’s prospectus for particular particulars relating to the Fund’s threat profile.

Bradley Krom, U.S. Head of Analysis

Bradley Krom joined WisdomTree as a member of the analysis workforce in December 2010. He’s concerned in creating and speaking WisdomTree’s ideas on world markets, in addition to analyzing present and new fund methods. Previous to becoming a member of WisdomTree, Bradley served as a senior dealer on a proprietary buying and selling desk at TransMarket Group. Bradley is a graduate of the Wharton College, College of Pennsylvania.

Editor’s Observe: The abstract bullets for this text had been chosen by Looking for Alpha editors.