Grace Cary/Second by way of Getty Pictures

Abstract

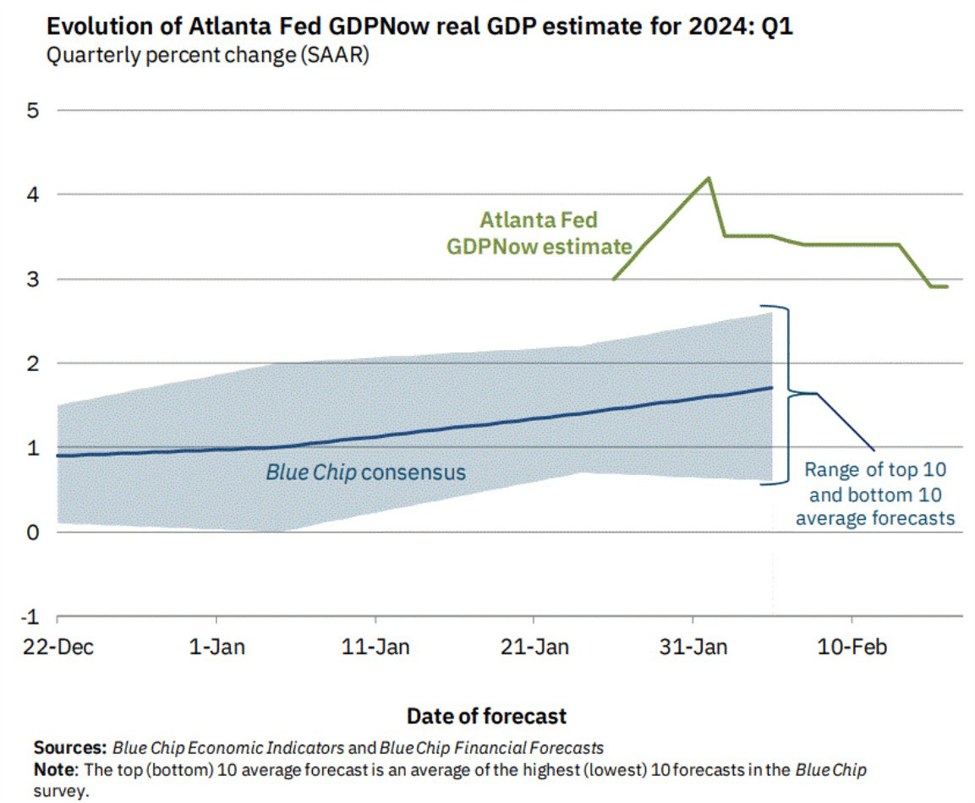

The shares have been largely rangebound since our preliminary report on Invitation Houses (NYSE:INVH). The shares barely registered to an in-line This autumn ’23 earnings report and are actually buying and selling barely under the place we gave our Promote score. This report gives our ideas on the quarter, revised valuation, and outlook for the 12 months forward. Total, we stay bullish on SFH fundamentals and really feel a little bit bit higher about Invitation’s valuation. Nonetheless, we nonetheless don’t see an ample margin of security and imagine there are much more enticing danger/return profiles inside REITs. We’re upgrading to an ambivalent Maintain.

Earnings Replace

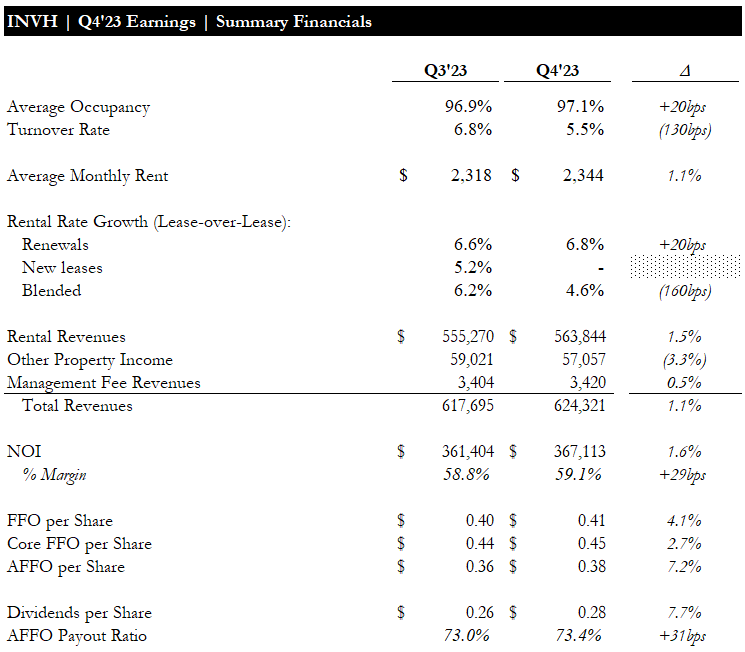

Within the earnings name, administration defined that they had been targeted on rising occupancy all through the quarter to place themselves favorably going into the seasonally stronger leasing season in Q1. We’re a bit skeptical about this, given occupancy solely elevated ~20bps, and are involved that it’s an excuse for weaker than anticipated lease progress. Whereas renewal lease progress throughout the quarter accelerated QoQ, charges on new leases had been flat and truly declined ~1.5% in Jan-24. Whereas administration says new lease charges have turned constructive this month (Feb-24), we’ll solely know for certain as soon as they launch Q1. Turnover was decrease than Q3, which noticed an abnormally excessive turnover associated to delinquent tenants.

AMR grew ~1.1% QoQ, notably slower than the prior quarter’s ~1.5% sequential progress. That is doubtless attributable to weaker market lease progress and administration’s concentrate on occupancy (i.e., being much less aggressive on pricing to drive leasing).

Notably, FFO, Core FFO, and AFFO all elevated QoQ and allowed administration to extend the dividend by ~8% whereas sustaining an affordable payout ratio.

This autumn Earnings – Abstract Financials (Empyrean; INVH)

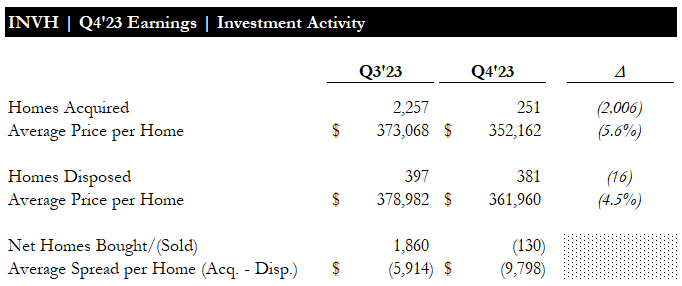

Acquisition exercise declined considerably, whereas disposition exercise was similar to the PQ, resulting in a slight decline within the general portfolio dimension. Whereas Invitation didn’t disclose the common cap charge for acquisitions and inclinations, we are able to infer that the funding unfold improved considerably QoQ based mostly on the common value per residence.

This autumn Earnings – Funding Exercise (Empyrean; INVH)

Total, the outcomes appeared constructive, however we can be intently monitoring lease progress within the coming quarter for indicators of additional weak spot.

Valuation

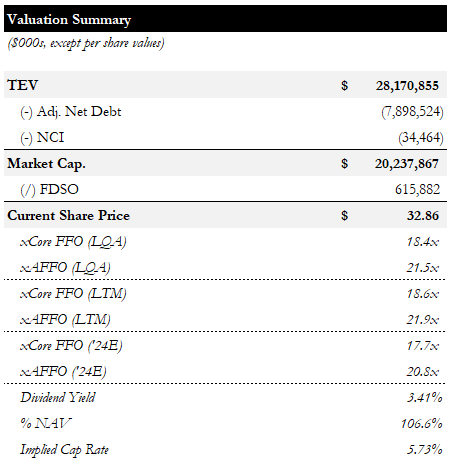

Invitation is buying and selling for 18.4x / 21.5x LQA Core FFO / AFFO and 17.7x / 20.8x the steerage midpoint for FY24 Core FFO / AFFO. Following the latest ~8% dividend enhance, it’s yielding ~3.4%. Present costs indicate a ~7% premium to our NAV estimate and a ~5.7% cap charge.

Valuation Abstract (Empyrean; INVH)

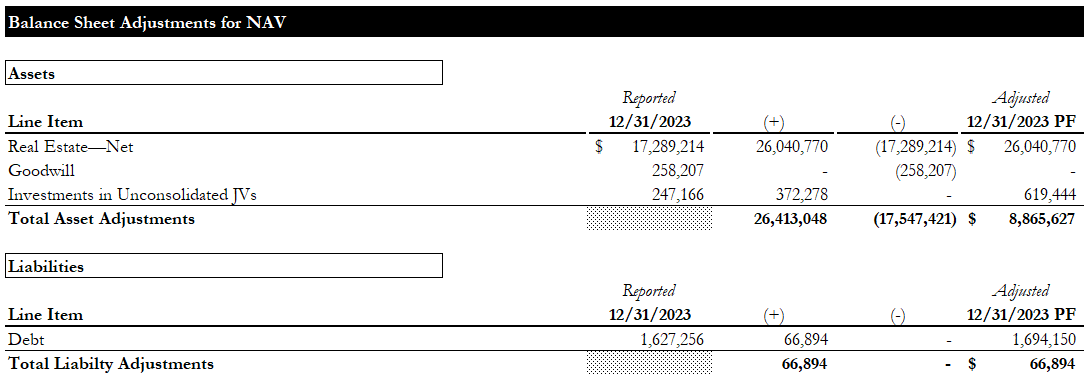

The main stability sheet changes for our up to date NAV estimate are proven under. We’re making use of a 6% cap charge to a stabilized NOI ~8% larger than LTM NOI (n.b., not same-store).

Steadiness Sheet Changes (Empyrean; INVH)

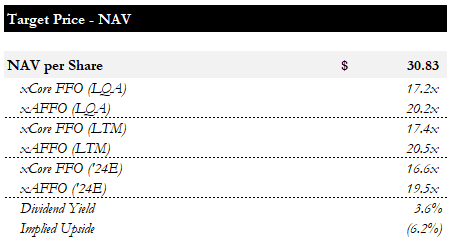

Our up to date goal value/NAV per share of ~$30.8 per share implies ~6% draw back and ~17x / ~20x FY24 midpoint steerage Core FFO / AFFO.

Goal Value (Empyrean; INVH)

Whereas our TP elevated ~$0.8 per share, and the implied return improved to ~-6% from ~-11%, we nonetheless have to see a decrease valuation earlier than getting bullish. Two information factors from the earnings name stood out to us as affirmation that Invitation’s present value doesn’t compensate for its danger profile: 1) in Aug-23, Invitation issued $800MM of senior notes at 5.5%, and a pair of) Invitation is at the moment incomes ~5.3% on its extra money. With present costs implying a portfolio cap charge of ~5.7%, buyers within the widespread inventory are solely incomes a ~20bps premium to the brand new senior noteholders and a ~40bps premium to Invitation’s charge of return on money. Whereas the bonds and money stability do not supply progress potential, these figures reveal how a lot progress the market has already given the corporate credit score for. Assuming the lease progress weak spot is transient, we see few good causes for Invitation to massively underperform. Nonetheless, we see much more interesting alternatives elsewhere.

Conclusion

Invitation’s This autumn was comparatively consistent with expectations. Most of its key metrics moved in the proper path, regardless of some indicators of slowing lease progress. Steering for FY24 implies ~5% YoY progress in Core FFO and AFFO per share and features a +$0.02 per share impression from its recently announced expansion into skilled property and asset administration providers. We’re upgrading Invitation to a Maintain, reflecting the upward revision of our goal value and a modest decline from our preliminary Promote score. We’re ready for a extra important margin of security earlier than getting bullish.