SolStock

Alnylam (NASDAQ:ALNY) stunned buyers with the announcement of pushing again the HELIOS-B information readout from early 2024 to June/July 2024. Analysts and buyers have been left making an attempt to learn the tea leaves of what this delay means for the percentages of scientific success. It’s uncommon for a Section 3 trial endpoint to be abruptly modified at a time when buyers have been imminently anticipating the information readout based mostly on what the corporate acknowledged just some months prior. The uncertainty created a sizeable drop within the inventory worth. The query that must be answered is whether or not this alteration is a pink flag or just a wise transfer by administration. This text will element the modifications being made within the trial and whether or not it warrants trigger for concern.

When investing in biotech, it is necessary to restrict downsize publicity, and I imagine this most up-to-date change provides a level of threat to the inventory. Whereas I stay long-term bullish on the inventory, I’ve trimmed some publicity and altered my inventory suggestion from a Purchase to a Maintain.

HELIOS-B Modifications

In my earlier article, Alnylam’s Huge Opportunity, I mentioned intimately Alnylam’s method to treating Transthyretin Amyloidosis (ATTR) in cardiomyopathy and the way their Section 3 trial, HELIOS-B, if profitable, is a recreation changer for the corporate. Briefly, therapies for ATTR-cardiomyopathy are a steadily rising, multi-billion greenback market in determined want of innovation and new therapy paradigms to cease/reverse this progressive, lethal illness. Because the article’s publication in early January 2024, the inventory has retreated roughly 20%, largely because of the confusion round modifications and changes within the HELIOS-B trial. In the newest convention name, the corporate did announce some shocking modifications to HELIOS-B that warrant an in-depth evaluate for present and potential buyers of Alnylam.

For fast background, Alnylam’s HELIOS-B trial is a Section 3 scientific trial evaluating vutrisiran in sufferers with ATTR-Cardiomyopathy (CM). The corporate took the data discovered from its failed APOLLO-B trial (ATTR-CM) and utilized it to its HELIOS-B trial. First, HELIOS-B enrolled round twice as many sufferers (665) as APOLLO-B and adopted their outcomes for practically 3 instances as lengthy, or 36 months, in most sufferers. By way of data gathered in APOLLO-B and Pfizer’s tafamidis Section 3 trial, Alnylam discovered nearly all of cardiovascular occasions and all-cause mortality started to point out up within the information after 18-24 months. Consequently, Alnylam set the preliminary HELIOS-B’s research length for 36 months, with major evaluation carried out when the final affected person reaches month 30.

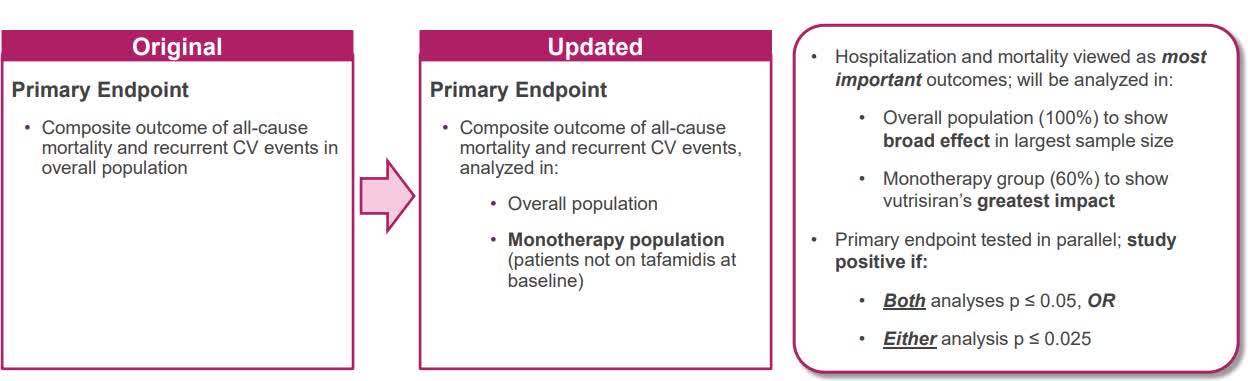

On the newest conference call, administration introduced a change to HELIOS-B’s research length, major endpoint and secondary endpoints. The research length added an additional 3 months for major evaluation to when the final affected person reaches month 33. The corporate expects the extra 3 months will end in 60% of sufferers remaining actively enrolled within the research could have longer follow-up, and a further 20% of sufferers will hit the complete 36 months of follow-up.

Maybe extra importantly, the corporate modified the first endpoint from a composite final result of all-cause mortality and cardiovascular occasions within the total inhabitants into 2 separate endpoints. The unique endpoint will keep the identical (vutrisiran vs. placebo), however the firm will now examine sufferers who obtained vutrisiran to sufferers on placebo AND not on tafamidis at baseline.

Alnylam This fall Earnings Presentation

Bear in mind, ATTR-CM is a progressive and sometimes lethal illness, so many sufferers take Pfizer’s tafamidis to assist cease the development of the illness. Of the 665 sufferers enrolled in HELIOS-B, 40% take tafamidis at baseline. Which means that sufferers will fall into 4 buckets within the research: sufferers receiving solely vutrisiran, vutrisiran and tafamidis, solely tafamidis and no remedy in any respect. Right here is the place the corporate desires to drill down additional into the affected person populations. Alnylam desires to get a clearer image of how their drug, vutrisiran, performs in opposition to a real placebo. The corporate has acknowledged that 90% of business insurance policy limit using mixture remedy, so it’s unlikely sufferers would obtain each tafamidis and vutrisiran regardless of potential synergies. A generic model of tafamidis isn’t anticipated till late 2028. Consequently, Alnylam desires to make sure insurers and regulators get a transparent image of vutrisiran as a monotherapy. On the This fall convention name, Alnylam CEO, Pushkal Garg, stated,

the evaluation within the monotherapy inhabitants permits us to exhibit the true affect of vutrisiran because the standalone therapy, offering a dataset that will probably be notably related to sufferers, prescribers and others because it intently aligns with the place we see the therapy panorama over the subsequent a number of years.

Studying the Tea Leaves

The query that continues to be is why change the research now? The corporate already knew that tafamidis wouldn’t lose exclusivity till late 2028 and insurers have been unlikely to help mixture remedy because of extreme prices. So, did Alnylam see one thing within the information that spurred them to increase the research and add a monotherapy endpoint?

Throughout the convention name, analysts tried to parse out as many particulars as potential, however administration regularly claimed the change has come from what their workforce has discovered from the APOLLO-B trial and the way an additional 3 months provides to the trial’s statistical energy.

When pressed by an analyst on the convention name if the trial design change was pushed by blinded occasion charges monitoring beneath their expectations, CEO Garg, stated,

We’ve got groups which can be wanting on the blinded information primarily to make sure wonderful research conduct and execution, make certain the appropriate sufferers are enrolled, make it possible for the information are clear, make it possible for we have now obtained an entire seize of all of the occasions, etcetera. And naturally, they’re occasion charges. However we’re not going to be sharing dribs and drabs the information, and that’s not the driving force right here. These sorts of occasions charges are extraordinarily variable – topic to plenty of variability and interpretation.

Clearly the corporate was involved that the ultimate evaluation could fail similarly as APOLLO-B and never present a powerful sufficient statistical consequence to warrant FDA approval. This was why they moved the purpose put up on the final minute to incorporate the first endpoint of vutrisiran vs. placebo and take away tafamidis from that evaluation. As a result of many ATTR-CM sufferers see profit from tafamidis, an ongoing fear in ATTR-CM trial design isn’t getting as many occasion charges as anticipated, which in flip makes attaining scientific meaningfulness of the drug’s therapy results tough.

When Alnylam designed HELIOS-B, they selected to solely embody sufferers with extra delicate classifications of coronary heart failure (NYHA I & II). The corporate selected to do that based mostly on prior outcomes which present these sufferers are probably to learn from therapy. In trial design, this generally is a double-edged sword when your major endpoint depends on displaying a statistically significant enchancment in all-cause mortality and cardiovascular occasions. The sufferers with much less developed coronary heart failure from ATTR are additionally much less more likely to expertise these occasions, particularly as they start to point out signs and start taking the present front-line therapy for ATTR-CM, tafamidis.

This fall Outcomes

Alnylam continues to develop their ATTR franchise in polyneuropathy. Quarterly income from ONPATTRO and AMVUTTRA (vutrisiran) grew 33% year-over-year to $254 million and whole sufferers on remedy went from 2,975 to over 4,060. This regular growth is an effective signal of medical doctors changing into extra acquainted and cozy with the therapy, and likewise sufferers craving a simpler and environment friendly therapy. In one other good signal of Alnylam’s innovation, sufferers are quickly switching from the corporate’s preliminary therapy, ONPATTRO, to the second-generation drug, AMVUTTRA (vutrisiran). AMVUTTRA is run as soon as each 3 months, in comparison with ONPATTRO’s as soon as each 3 weeks.

For FY2024, the corporate expects to develop web product income from $1,241 million to $1,400 – $1,500 million, or 17% at midpoint of steerage. Importantly, this determine doesn’t embody any potential income for ATTR-CM sufferers in a probably profitable HELIOS-B trial.

The corporate stays nicely capitalized, with $2.44 billion in money available. Attributable to its massive money stability and increasing income base, it is unlikely the corporate would increase funds via share choices at this level.

Take Away

I don’t essentially imagine Alnylam extending the HELIOS-B trial by 3 months and including one other major endpoint is an indication of a doomed Section 3 trial, however it ought to trigger some concern for buyers. Making these modifications this late in a trial doesn’t come from a place of power. It possible comes from a more healthy affected person inhabitants not having as many cardiac occasions as anticipated. It is usually possible the extra endpoint was added as a result of the 40% of sufferers on tafamidis at baseline made the preliminary major composite final result of all-cause mortality and recurrent cardiovascular occasions within the total inhabitants tough to point out statistical significance.

It could possibly be potential that HELIOS-B achieves scientific success, however on the identical time doesn’t present a big profit over tafamidis. If this state of affairs performs out, buyers will probably be left questioning how a lot market share vutrisiran can steal from tafamidis. Bear in mind, tafamidis has been in the marketplace for ATTR-CM for a number of years and if a transparent profit isn’t seen in HELIOS-B over tafamidis, what number of medical doctors could be keen to modify their sufferers to a brand new drug they aren’t as acquainted with prescribing? It’s potential a constructive final result may end in approval of vutrisiran for ATTR-CM, however its gross sales obtain a slower ramp than anticipated by the market, which in flip may damage the inventory.

At this level, all of that is hypothesis, however when a biotech firm modifications their largest Section 3 trial on the final minute, it warrants additional examination of the potential outcomes. As I’ve written earlier than, Alnylam has a large alternative to capitalize on the ATTR-CM market. I stay optimistic the corporate can convey a brand new useful therapy to market, however I’m way more cautious in regards to the varied potential outcomes than I used to be earlier than this announcement.

Valuing biotech shares is a unending course of because of frequent important modifications in future earnings potential based mostly on scientific trial information. A wildly profitable HELIOS-B trial may add $3-4 billion {dollars} to Alnylam’s income base over the subsequent 3-5 years. Alternatively, a modest success may end in an extended product ramp the place the corporate solely provides $1-2 billion in income in 3-5 years. A failed trial, much like APOLLO-B, could be completely devasting to the corporate. The consequence from this scientific trial is huge and will end in great volatility within the inventory worth.

By way of valuing the inventory because it stands immediately, it presently trades at 10x gross sales when together with royalties and income from collaborations. At its present worth of $150/share, the corporate has a market cap simply shy of $19 billion. In my opinion, it is presently pretty valued. It is positively a greater entry worth in comparison with once I wrote my first article again in January and the inventory was $190/share. I alter my score from a purchase at $190/share to a maintain at $150/share as a result of we now have extra data. Taking in all the data offered throughout Alnylam’s convention name, I imagine the HELIOS-B trial will probably be a reasonable success. Which means, it could present success over placebo however could not present superiority over tafamidis.

Investing in biotechnology firms is notoriously tough as a result of it usually comes all the way down to a binary final result. When new data turns into accessible, buyers want to have the ability to regulate and never sit idly by. Buyers ought to hope for a wildly constructive HELIOS-B however ought to put together for a combined consequence. Whether or not that’s via cutting down positions or shopping for draw back safety via choices, buyers ought to proceed with warning till Alnylam proclaims their ultimate HELIOS-B information in late June to early July.