Johannes Simon/Getty Photos Information

Introduction

There’s one thing particular about an organization with a one-letter inventory ticker.

The Wall Avenue Journal wrote an attention-grabbing article in regards to the recognition of one-letter inventory tickers; for no matter purpose, the administration of many firms gravitate in direction of them.

A few of the most effective companies have one-letter-long inventory tickers; firms like Agilent (A), Realty Revenue (O), and Visa (V) all come to thoughts. So, as superficial as it’d sound, after I noticed Jacobs Options (NYSE:J), it instantly sparked my curiosity.

Whatever the ticker, and whatever the title, at this time I am right here to speak to you about Jacobs Options, an engineering {and professional} providers agency, noteworthy for rather more than its ticker.

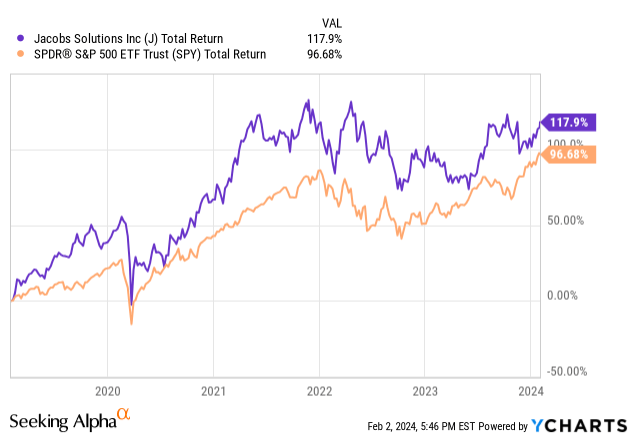

Past the brief inventory ticker, the corporate managed to outperform the S&P over the previous 5 years by about 20%; at that time, I knew this was a agency I needed to achieve a greater understanding of.

Context

Jacobs Options Inc., primarily based within the US of A, is dominant within the technical skilled providers business. Established in 1947 by Joseph “J.” Jacobs, the agency has solidified its standing by constantly delivering within the fields of engineering, skilled consultancy, building, and scientific and specialty consulting. Serving an intensive international clientele, Jacobs addresses the technical wants of companies, establishments, and authorities entities throughout many fields.

The corporate’s evolution is characterised by its periodic acquisitions, successfully broadening its operational scope and enhancing its market affect. Vital acquisitions have seen the incorporation of worldwide entities like Sir Alexander Gibb & Companions and Carter and Burgess, coupled with impactful mergers such because the amalgamation with Sinclair Knight Merz in 2014. The procurement of CH2M Hill in 2017 and Wooden Nuclear in 2020 additional underscores Jacobs’ strategic method to capital funding, aimed toward augmenting its proficiency and footprint, particularly inside infrastructure, governmental service sectors, and nuclear service industries.

Furthermore, Jacobs’ investments, exemplified by buying a considerable share in PA Consulting and initiating a three way partnership with the Qatar-based Locus Engineering Administration and Providers Co. in 2022, showcase the corporate’s method to getting into new markets aggressively.

Monetary Outcomes

On account of its technique of delivering top-tier technical providers mixed with enlargement by means of acquisition into new areas and verticals, the corporate has scaled up massively over the previous years.

Income and EPS

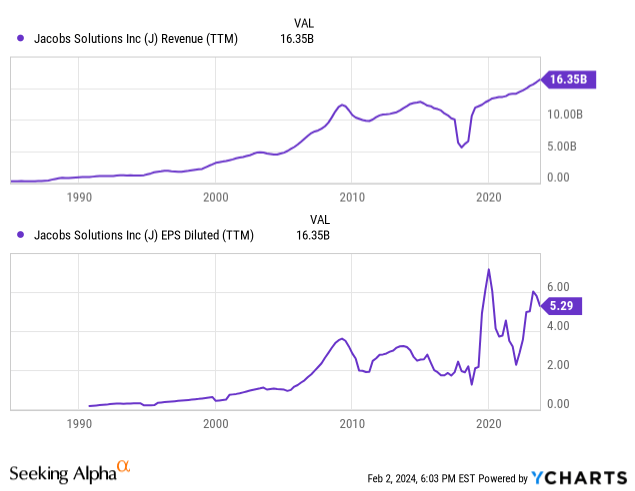

These investments, each inside and exterior, have yielded huge enhancements to revenues and EPS since its founding. Over the previous 12 months, administration delivered an EPS of $5.29, which is greater than double what the corporate achieved within the years earlier than the coronavirus.

Whereas the corporate has skilled years of low progress (2010-2019) and a few years with huge drops in earnings and revenues, for probably the most half, the overall trajectory of this enterprise is upward. Maybe much more spectacular is that revenues and EPS progress seem like accelerating because it scales, not slowing down.

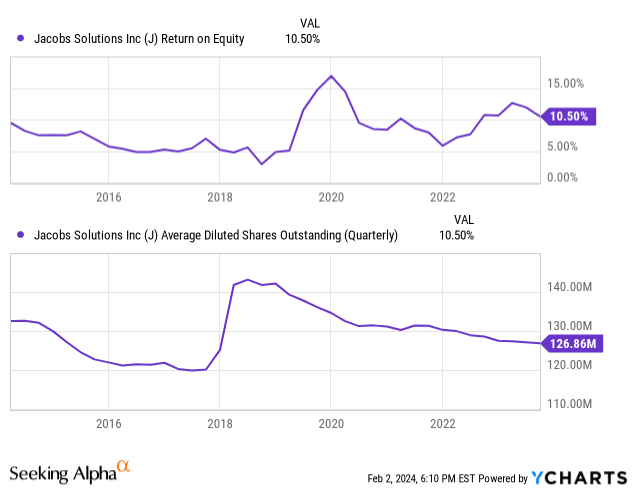

Capital Deployment Effectivity

Wanting on the administration’s monitor document of deploying capital, we are able to see that over the previous 12 months, they delivered a ten.5% return on fairness, which has been roughly regular over the previous decade, osculating between 5-15%. I would think about that stage to be roughly common inside the area, commendable, positive, however not notably excellent.

On the optimistic facet, alongside a ~1% dividend yield, the corporate returns capital to shareholders by means of buybacks. These buybacks have let the corporate use fairness to amass different firms now and again, which they then should buy again with future earnings. This will increase the pool of potential targets, a few of which can demand fairness to promote their enterprise.

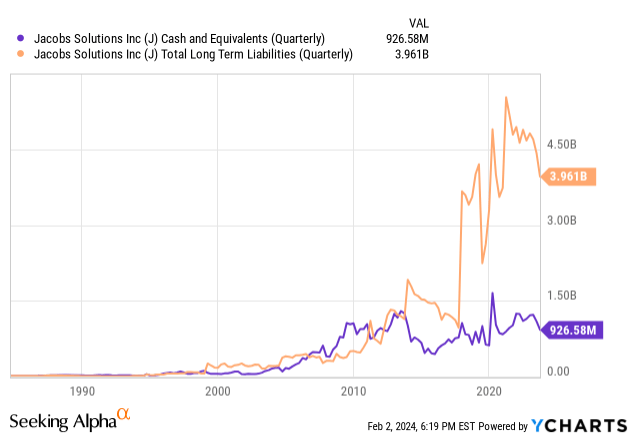

Stability Sheet

One space of concern is the corporate’s rising urge for food for debt. In years previous, the corporate ran its enterprise at a roughly debt/money impartial stage; because the late 2010s, it has taken out rather more debt. Whereas these ranges have decreased over the previous 12 months, they’re nonetheless markedly above their historic ranges at a time when rates of interest are a lot larger than they had been during the last decade. As the corporate pays again this debt and/or refinances at larger rates of interest, it will eat away on the money circulate that can be utilized for acquisitions, buybacks, and dividends.

Catalysts for Development in 2024

Wanting ahead, I consider 2024 is prone to be an enormous 12 months of progress for Jacobs. Here is why… Jacobs is positioned to capitalize as international threats escalate, pushed by its publicity to protection and nuclear sectors. The geopolitical local weather, marked by a resurgent Russia, a extra assertive Iran, and broader worldwide tensions, is prompting nations to prioritize protection spending and vitality safety.

The elevated concentrate on collective protection and the heightened danger in key commerce areas just like the Purple Sea have underscored the necessity for enhanced army capabilities within the protection sector. Current incidents, reminiscent of assaults on American-owned ships and Iranian missile strikes, have prompted calls from international protection leaders, together with the UK Protection Secretary Grant Shapps, for allied nations to bolster their protection expenditure. This shift, away from the period of the peace dividend, as discussed in a latest SA new article, highlights the urgency of making ready for potential conflicts involving main international powers.

With its experience and providers catering to the protection business, Jacobs is well-positioned to learn from the elevated protection budgets and the corresponding demand for its providers.

On the vitality entrance, the push in direction of nuclear vitality to fight inflationary pressures on electrical energy is gaining momentum. Jacobs’ latest partnership with the French start-up Naarea to develop a brand new nuclear energy reactor is a testomony to the corporate’s dedication to and capabilities within the nuclear sector.

This collaboration, aimed toward selling vitality safety by offering protected, clear, and sustainable nuclear vitality, aligns completely with the worldwide pivot in direction of atomic energy as a dependable and environment friendly vitality supply. As international locations think about better funding in atomic vitality as a strategic resolution to their vitality wants, Jacobs’ experience and ongoing initiatives on this area will possible be a big catalyst for its progress in 2024.

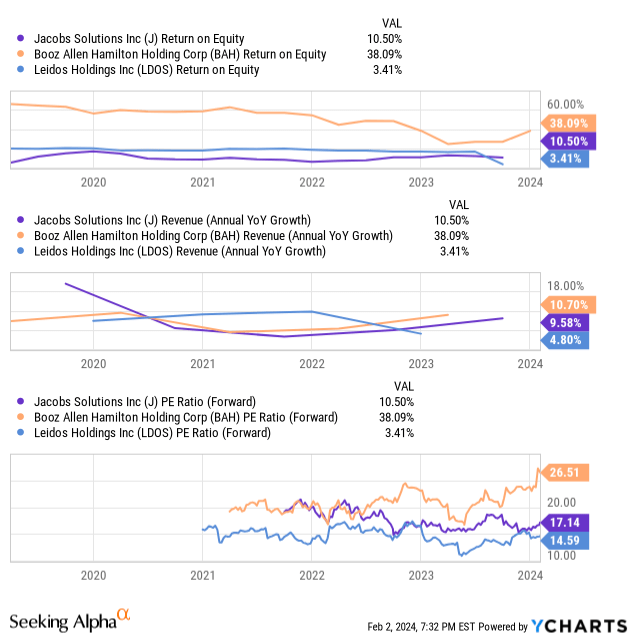

Valuation and Efficiency vs. Friends

Evaluating Jacobs to different friends, Booz Allen Hamilton (BAH) and Leidos (LDOS), we are able to see that Jacobs’ is kind of in the course of the pack, each when it comes to efficiency and when it comes to valuation at 10% income progress with a 17x ahead PE ratio.

That mentioned, Jacobs could have the worst mixture of progress and worth of those three firms. Positive, you’ve got Booz Allen with sky-high returns on fairness and a lofty PE ratio, however the extra attention-grabbing comparability is definitely Leidos. In comparison with Jacobs, Leidos has traditionally had marginally quicker income progress and better returns on fairness aside from its efficiency final 12 months, regardless of buying and selling at a decrease PE ratio (14.6X) in comparison with Jacobs’s 17.1X.

Conclusion

In abstract, I consider Jacobs Options is a strong “Hold.” Whereas its progress charges and capital returns are commendable, they do not fairly attain distinctive ranges, particularly when juxtaposed with counterparts like Leidos, which presents a comparable progress story at a extra compelling valuation. However, Jacobs stands on the cusp of potential tailwinds, notably within the protection and nuclear arenas, as 2024 unfolds. These catalysts could provide the leverage wanted for Jacobs to outpace its present projections and obtain a efficiency that distinguishes it from the pack.