Hwangdaesung

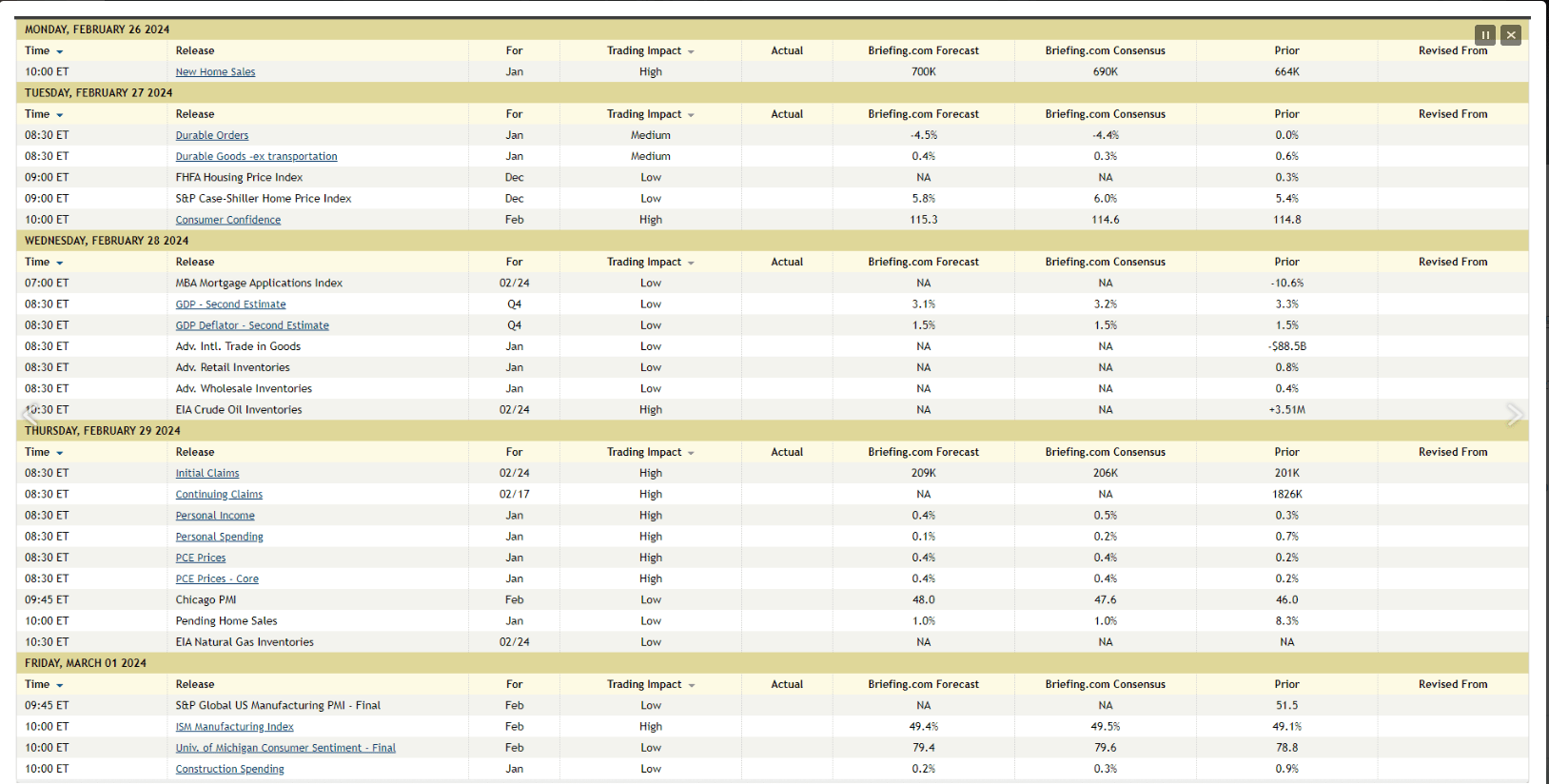

This complete financial calendar from Briefing.com exhibits the anticipated financial knowledge releases for the approaching week. Given the bounce in CPI and PPI knowledge for January ’24, there’s a whole lot of curiosity in what the January PCE knowledge will present Thursday morning, February twenty ninth.

Consensus expectations are searching for +0.4% for total PCE and +0.4% for PCE Core, per the above desk.

Financial measurements fascinate me within the sense that the monetary media headlines can differ enormously from what the assorted releases truly measure. All the time watch the inventory and bond market’s response to the information, in addition to the information itself.

Why so many inflation measures? With a $27 trillion financial system, I’m glad there are numerous methods or measures to trace inflation. The CPI and PPI knowledge are referred to as “fixed weight” measures, that means that the CPI and PPI monitor two apples and two oranges over time, and make no adjustment for adjustments in client buying patterns. The CPI’s “fixed-weight” measures items just for the final 24 months, and are modified or adjusted in January of even calendar years. Might that designate the warmer January CPI and PPI in ’24? Uncertain, provided that the stress in January ’24 CPI and PPI appeared to originate from “shelter”, one of many largest parts of the CPI.

PCE, alternatively, contains authorities knowledge (similar to Medicare) and appears to account for adjustments in buying patterns over time.

Here is a good article from the CEA (Council of Financial Advisers) from Sept ’23 evaluating or contrasting CPI / PPI vs the PCE knowledge.

Don’t overlook about “inflation expectations” too. It isn’t essentially what the inflation fee is at present that issues, however what inflation’s anticipated to do over the subsequent 3-6 months.

Personally, I do suppose inflation continues to say no, however the underlying energy in financial knowledge, significantly companies, is making it troublesome to get inflation all the way down to the two% degree the Fed wishes.

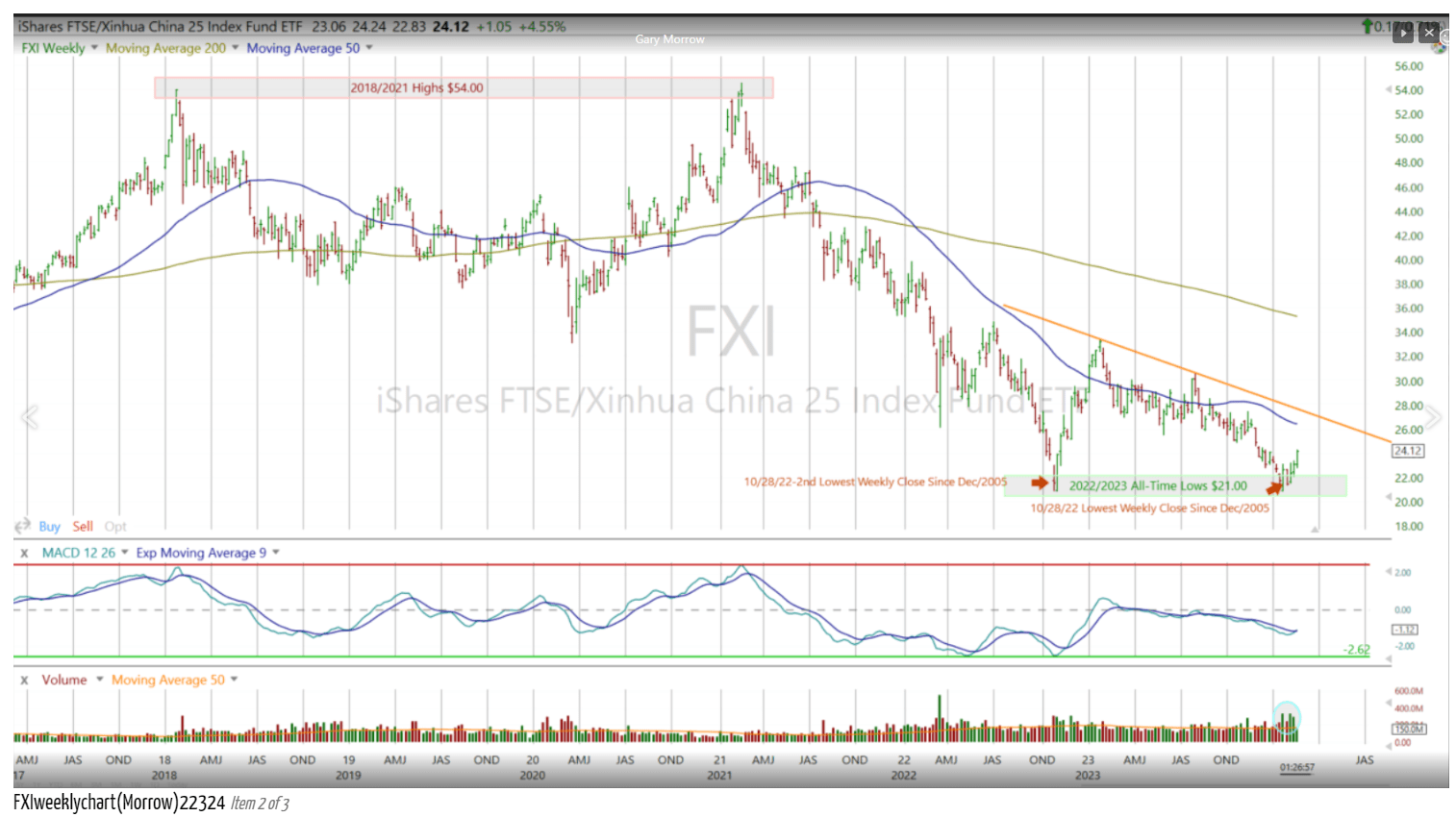

FXI Chart

A protracted-time supply of fine technical evaluation for this weblog, Gary Morrow (@garysmorrow), shot this over to me Friday, highlighting the double-bottom within the FXI (iShares FTSE / Xinhua China 25 Index Fund ETF) chart. The China central financial institution lower their 5-year prime mortgage rate of interest final weekend, purportedly to assist struggling property values. This weblog up to date worldwide / Non-US returns final week as of January 31, 24 here.

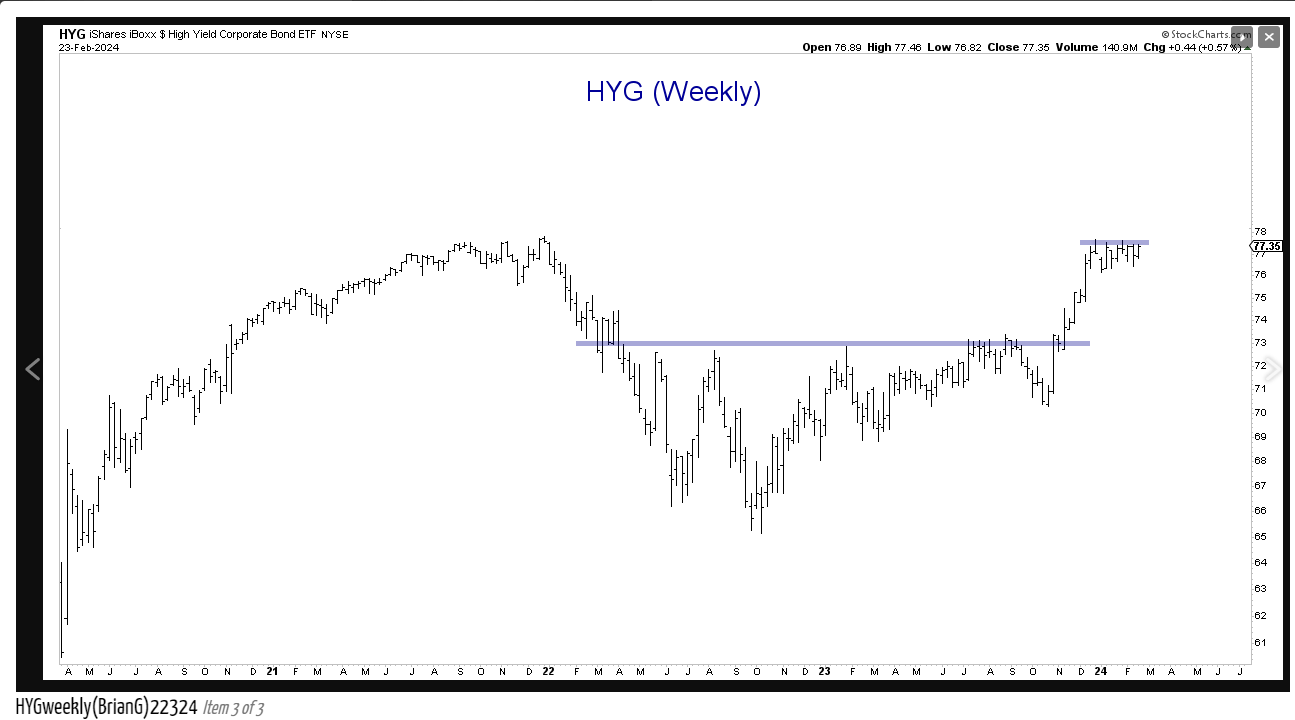

Excessive-Yield Credit score

Love this chart from BrianG over at AlphaCharts, revealed this weekend.

If HYG breaks above this consolidation, it’s powerful to make a bearish case for shares. Company high-yield is at all times the early warning indicator for fairness issues.

Ultimate observe: Good interview by Compound & Pals, Josh Brown lately of Ryan Detrick of Carson Group. Loved Josh’s “crabs” story (no, not these sort of crabs) too. Couldn’t hearken to the entire 90 minutes. Stayed for the primary half-hour.

None of any of the above is recommendation or a advice. Previous efficiency isn’t any assure or suggestion of future outcomes. Investing can contain lack of principal, even for brief time durations. All earnings associated knowledge is usually sourced from LSEG except in any other case famous. Readers ought to gauge their very own consolation with portfolio volatility and modify accordingly.

Thanks for studying.

Editor’s Notice: The abstract bullets for this text have been chosen by Looking for Alpha editors.