Andrew Burton

Context & Background Info

China and Grasp Seng shares have been mired in deep malaise for a lot of 2023, and there have been few survivors of this 12 months’s enduring bear marketplace for China ADRs and H-Shares. On the root of the issue for many firms inside Grasp Seng is the truth that the ailing property sector in mainland China has deeply dented shopper confidence to a level that traders have largely de-rated the e-commerce sector’s valuation in a structural method.

Outdoors of some brilliant spots inside China shares akin to PDD Holdings (PDD) and New Oriental (EDU), most firms on this 12 months’s setting have been unable to develop gross margins or information concretely on additional EBITDA growth. This subdued outlook for many firms throughout the Grasp Seng (to which JD is a crucial part) has saved a lid on any advance and has resulted in most rallies being offered and selloffs gaining momentum.

That being stated, JD’s newest earnings quarter – whereas not good – gives a window of alternative the place traders might take into account that in the end the inventory (together with the remainder of China’s ECOM sector constituents Alibaba and Meituan) has seen the ultimate leg decrease and should enter the primary phases of a uneven bottoming course of.

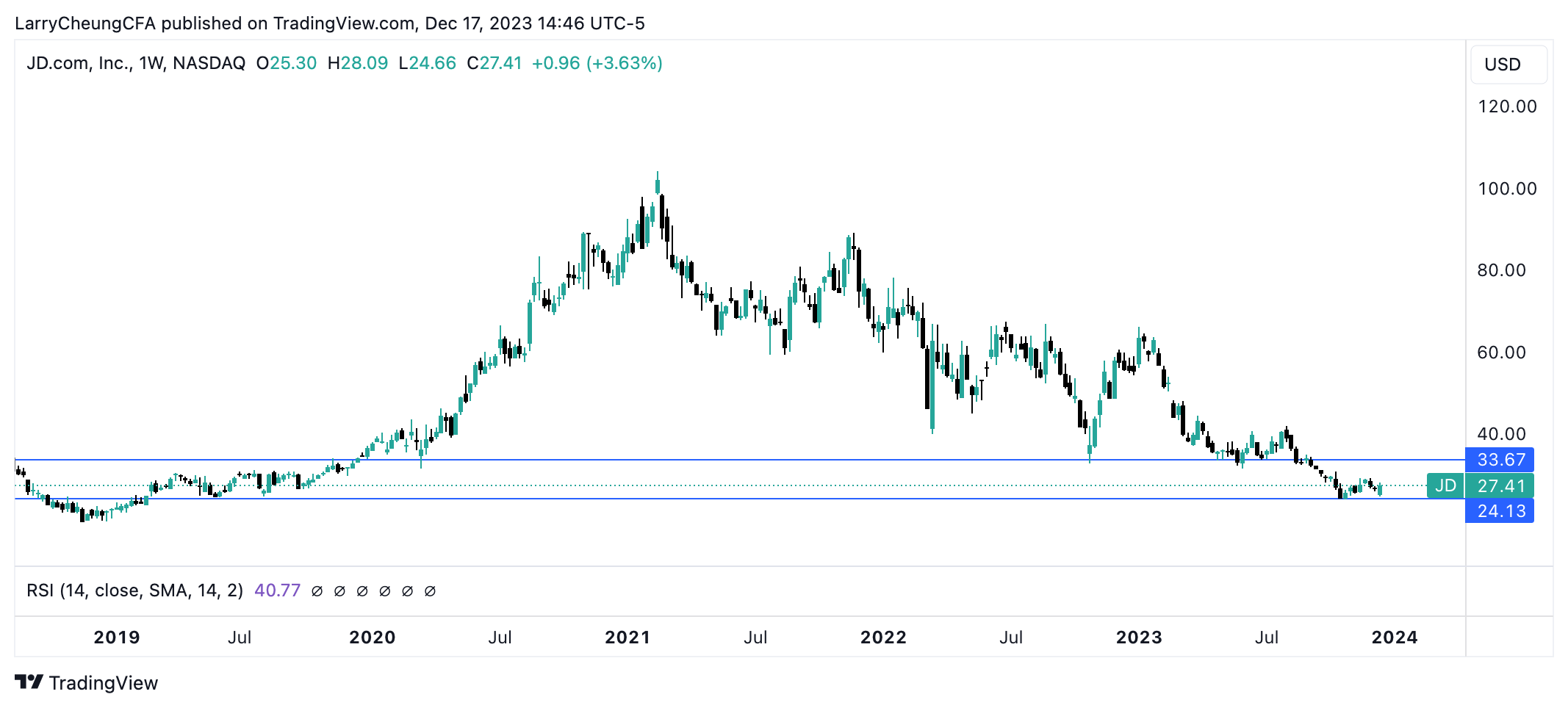

My major view for JD is that if the latest 24/share degree lows can maintain, the corporate has a first-stage advance alternative to revisit the neckline technical construction of 33-34/share sooner or later in 2024. The 24/share degree is a vital line in sand and it’s my perception that a number of day by day closes beneath this degree will end result out there looking for decrease lows.

JD Technical Market Construction (YCharts)

The Catalysts for JD and Basic Outlook

One of the necessary occasions for JD within the latest few weeks is that founder Richard Liu mentioned that the corporate has develop into bloated and should search change within the face of Pinduoduo’s rise. Mr. Liu has seen his internet value minimize in half from $10 billion to $4.9 billion as its H-Shares (HK-9618) have fallen by a dramatic 55% in 2023. China’s financial droop has compelled all e-commerce gamers to struggle for customers who at the moment are extra price-conscious than ever, however regardless of JD’s razor-thin margins after discounting, its worth cuts nonetheless have not been perceived as sufficient to woo buyers.

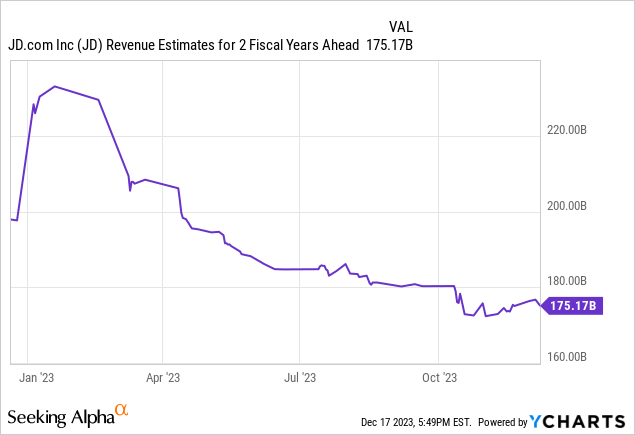

On this previous quarter, revenues rose a better-than-expected 1.7% to $34 billion from a 12 months in the past, whereas internet earnings rose 32% to $1.1 billion. These figures largely beat expectations as JD’s decrease first-party enterprise sourcing prices allowed it to marginally improve profitability as a consequence of its operations. Within the years between 2017 and 2022, JD grew income at a 24-25% compounded annual progress fee and its newest 12 months progress figures of low single digits have brought on a really massive reset within the inventory.

Many Promote Aspect Analysts on the Avenue imagine that the ahead outlook for income can obtain 4-5% given the structurally modified panorama for shopper conduct and spending. The constructive information is that administration guided gross merchandise quantity and its grocery store class progress to be above that of retail gross sales of shopper items in China.

As of now, JD’s enterprise mannequin is characterised by the next segments:

- JD Retail: 89% of complete income (on-line direct gross sales, market, promoting)

- JD Logistics: 13.1% (inside and exterior logistics enterprise)

- Dada: .8% (native on-demand supply and retail platform in China)

- New Enterprise: 2.1% (JD Property, Jingxi, and different tech initiatives)

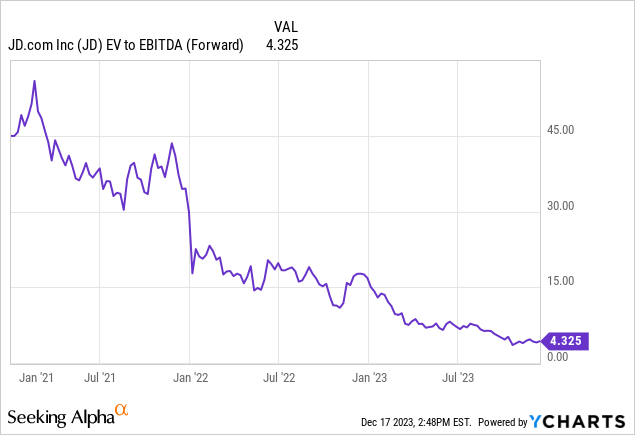

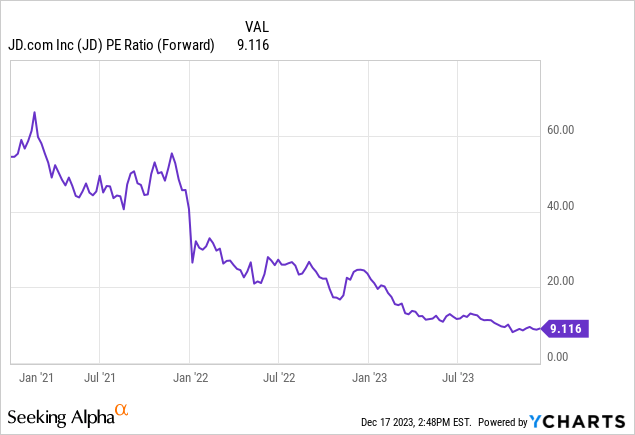

Provided that a lot of the slowdown in JD’s retail enterprise has tremendously and adversely impacted their ahead outlook, a number of valuation metrics replicate this with their EV/EBITDA a number of and ahead P/E multiples approaching multi-year troughs.

JD’s ahead earnings a number of of 9.1X is extremely much like that of BABA, which trades at 8X. The corporate’s valuation has been structurally de-rated as a consequence of its poor basic efficiency however an upward revision in its outlook later in 2024 can carry its valuation and inventory off present lows.

Dangers, ideas on Entry & Valuation

Though China shares have a historical past of buying and selling on sentiment and home political affairs surrounding investor notion in direction of authorities regulation, we will additionally witness that the corporate’s shares additionally broadly comply with its basic trajectory.

In JD’s case, we noticed a 25% income progress profile from 2017 to 2022 shrink to a 2-4% single-digit progress story this 12 months in 2023 with 4-5% progress being the bottom case outlook in 2024. This collapse in prime line progress has basically reclassified the corporate from being a progress inventory to a worth inventory primarily based on its basic traits and valuation multiples now clearly reflecting it.

As a result of China’s structural slowdown in shopper spending, Analysts have continued to chop income estimates for the ahead two years, which has saved a basic cap on any share worth beneficial properties. This basic understanding of its enterprise explains why rallies are offered and selloffs worsen as traders have to see profitability or margin growth earlier than treating the inventory as an funding moderately than only a buying and selling car.

That being stated, policymakers in China at the moment are seeking to reinvigorate its financial system with a 5% GDP Development goal in 2024, and which means extra stimulus is probably going in play for the approaching 12 months to assist the property sector discover its footing.

If we assume a 5% GDP Development goal for China’s macroeconomic panorama and imagine that JD can preserve a barely increased single-digit progress profile at 4-6% per 12 months, the corporate can see a modest carry off its valuation trough of 4.3X EV/EBITDA and 9X Ahead P/E to start a gradual strategy in direction of the technical neckline of 33-34/share later in 2024.

Sentiment surrounding Grasp Seng firms is extremely fickle, however on a person firm foundation, JD’s working mannequin is probably going getting into a bottoming section for its progress outlook and which means the inventory has basically extra upside than draw back from right here.

Web/internet, I believe JD falls within the class of a 2:1 danger/reward profile the place the corporate gives about 20% upside potential to its subsequent resistance degree relative to 10% draw back again to latest lows. Given its volatility, conservative sizing will probably be useful in permitting traders to carry the identify via intensive vary growth.

Traders who assume JD has extra potential than a 4-6% income progress story in 2024 can discover out-of-the-money Name Choices at strategic strikes and lengthy length expirations.

Traders who imagine that JD (and its peer BABA) will proceed to be mired in an unescapable cycle of structural de-ratings might want to have a look at different China names or Pinduoduo throughout its subsequent corrective cycle.

For now, till there may be better stability in China’s property market, this can be very necessary to deal with China as an opportunistic buying and selling panorama moderately than a protected buy-and-hold funding panorama -no matter how low-cost the valuation of its shares turns into.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please pay attention to the dangers related to these shares.