tigerstrawberry

Funding Thesis

Photo voltaic Shares haven’t loved an amazing run recently, partly as a result of traders’ worry for the “Higher for Longer” rate of interest backdrop and uncertainties concerning slowing financial development in 2024 within the US and Europe, which has resulted in mounting pessimism for the outlook of the photo voltaic sector, as the price of financing photo voltaic modules set up has change into extra elevated and costly. In consequence, most photo voltaic firms have seen their inventories piling up with decrease backlog orders as manufacturing outpaces set up. This has resulted in a lot disdain from Wall Road and traders, inflicting a large sell-off throughout the broad market.

However, JinkoSolar (NYSE:JKS) was the outlier of all. Regardless of the cyclical slowdown of the photo voltaic market, JKS nonetheless delivered a sturdy quarter in Q3 2023. Income was $4.36 billion in Q3 2023, up 63% YoY. Diluted EPS elevated by 188.7% YoY to $0.63, and the gross margin expanded from 15.7% to 19.3%.

This promising YoY development was primarily attributable to the will increase within the cargo of photo voltaic modules. Whole module shipments had been up roughly 21.4 gigawatts, a rise of 107.9% yr over yr. With the enlargement of its N-Sort Wafer Photo voltaic Modules Manufacturing Services in Shanxi, China will set to begin manufacturing in 2024, including an incremental manufacturing capability of 28GW.

Jinko has some primary aggressive benefits that embrace its giant manufacturing capability, international community, excessive power conversion modules, and fixed expertise innovation. In the meantime, Jinko’s long-term prospect stays shiny, that can probably profit from the Inflation Discount Act within the US, and low carbon power transition efforts each in China and EU, which raises downstream and photo voltaic set up demand.

Given its stable financials and unreasonably low valuations (3x PE), JKS has the potential to outperform the market within the long-term, I price JKS as a “Strong Buy”.

Enterprise Overview

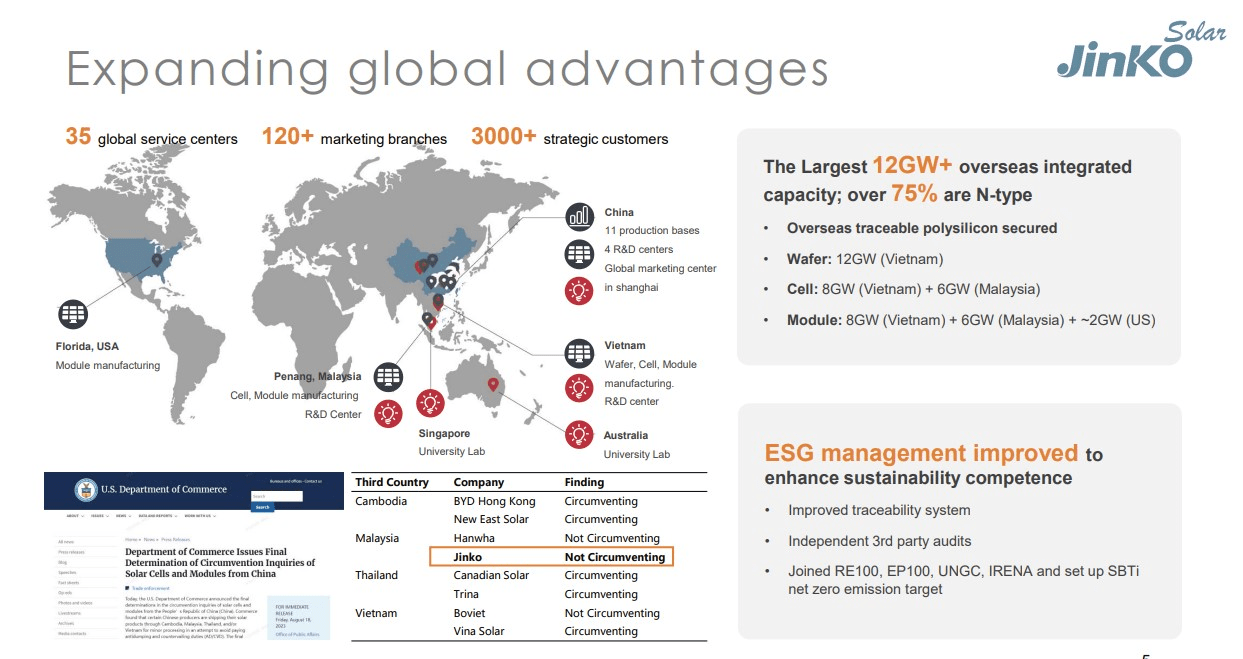

Jinko Enterprise Overview (Traders Presentation)

JinkoSolar (JKS) is a Chinese language Photo voltaic Firm based since 2006 that engages within the design, improvement, manufacturing, and advertising and marketing of photovoltaic (PV) merchandise. The corporate provides photo voltaic modules, silicon wafers, photo voltaic cells, recovered silicon supplies, and silicon ingots. It additionally gives photo voltaic system integration providers; and develops industrial solar energy initiatives.

JinkoSolar has intensive enterprise operations within the Individuals’s Republic of China, america, Mexico, Australia, Japan, Vietnam, and EU. The corporate produces Wafer Photo voltaic Modules primarily in its manufacturing facility in China, Vietnam, Malaysia and Jacksonville, Florida.

JinkoSolar manufactures two varieties of Photo voltaic Modules, together with the P-Sort and N-Sort (Greater Vitality Conversion Charges and Energy Outputs)

Management in Chopping-edge N-Sort Expertise

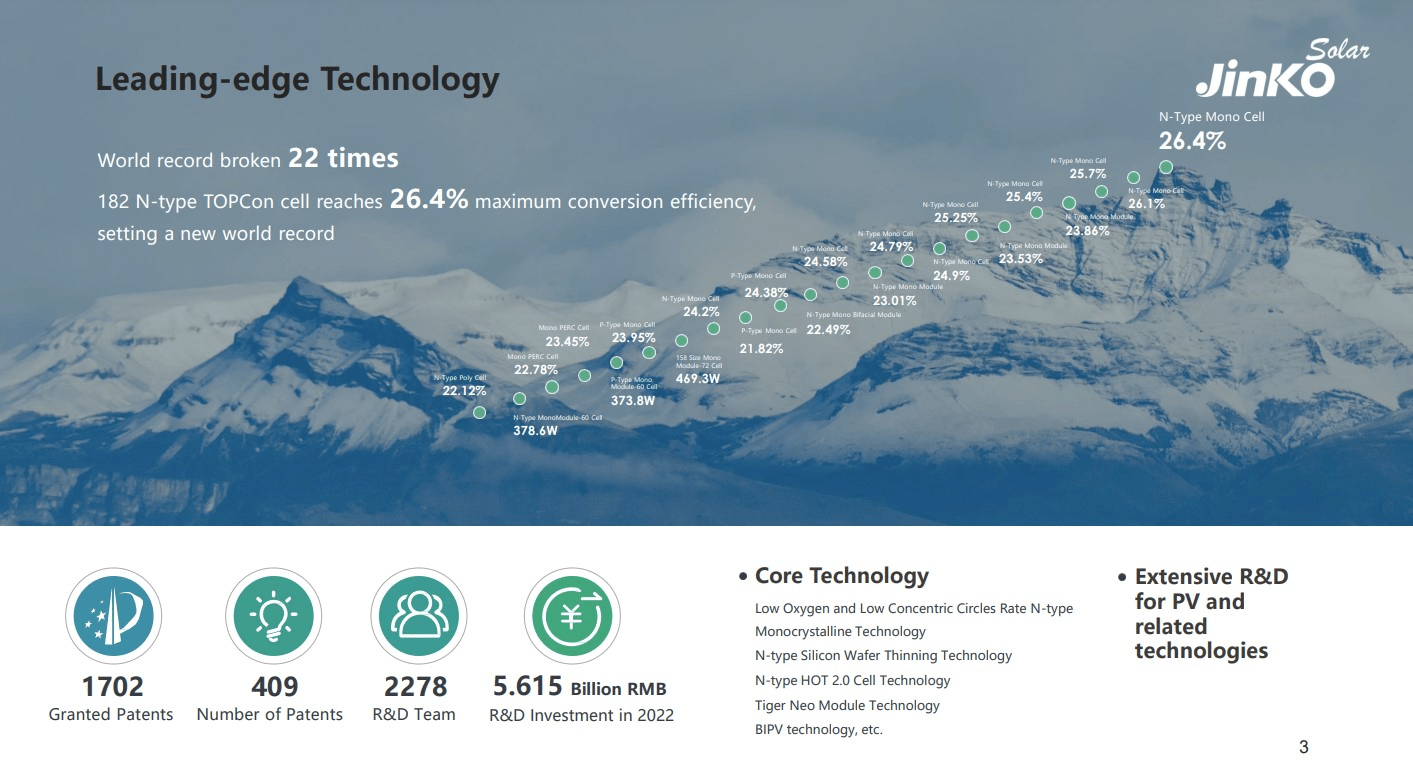

Photo voltaic Tech Development (JKS Traders Presentation)

One of many main aggressive benefits that JinkoSolar differentiates itself from its opponents is the cutting-edge and {industry} main N-type TOPCon cells expertise it possesses. The power conversion price of its N-Sort Wafer Photo voltaic Cells has been enhancing progressively, hitting a world report of 26.4% in Q2 2023 and 26.89% in Q3 2023 by way of most Lab conversion effectivity, whereas mass manufacturing effectivity reached 25.6%.

This stays marginally increased than its opponents like First Photo voltaic (FSLR), Daqo New Vitality (DQ), and Canadian Photo voltaic (CSIQ), which has panel efficiency of 22-23% on average. Trying ahead, power conversion price for Jinko’s N-type photo voltaic cells is anticipated to hit 27% in 2024, which signifies the robust technological moat that Jinko possesses.

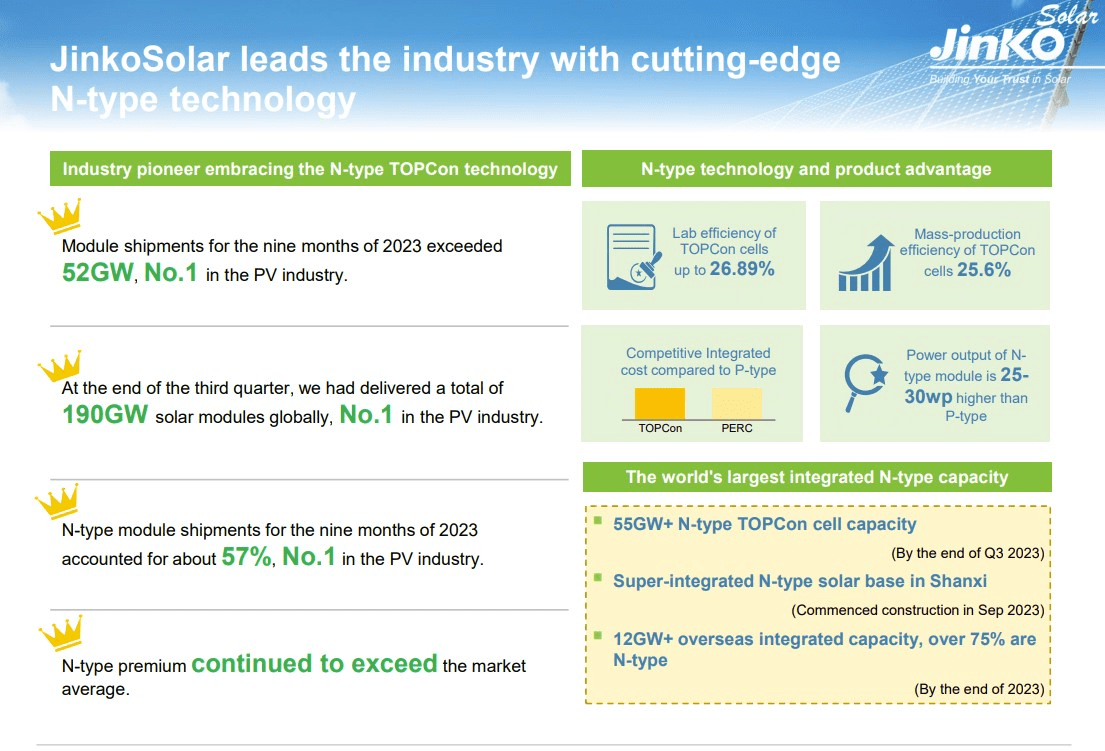

Jinko Photo voltaic N-Sort Expertise (Q3 2023 Traders Presentation)

Moreover, JinkoSolar additionally delivered 52 GW in Module Shipments for its N-Sort TopCon Photo voltaic Modules, which accounts for 57% of N-Sort Module Shipments within the photo voltaic {industry}. This locations JinkoSolar 1st globally by way of Photo voltaic Module cargo supply, reflecting its prime place and its means to exceed the market averages.

JinkoSolar will probably retain its dominant and {industry} main place within the Photo voltaic Sector given its robust dedication to product management and R&D improvement. Actually, JKS now owns greater than 400 patents for its proprietary applied sciences. This makes it formidable for its opponents to repeat and creates an financial moat across the enterprise.

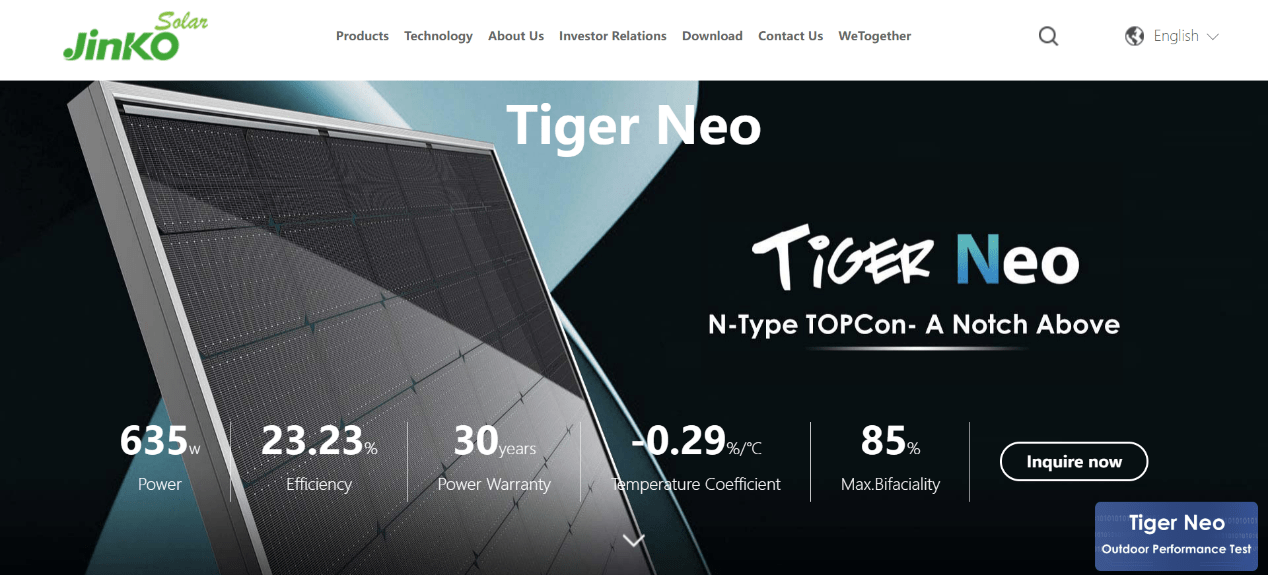

Widespread Reputation of Tiger Neo Photo voltaic Panels

Tiger Neo Photo voltaic Module (Jinko Photo voltaic Web site )

See we are able to see, Jinko has just lately launched its newest product Tiger Neo Photo voltaic Modules utilizing its proprietary N-Sort TOPCon photo voltaic cell expertise, which produces 635w of Energy with an power conversion effectivity of 23.23% and has outperformed its predecessor – Tiger Professional Photo voltaic Module – which has an influence output of 585w and power conversion price of 21.4%. This manifests the truth that T-type cell expertise delivers 25~30Wp greater than P-type photo voltaic modules.

Actually, Tiger Neo has just lately gained recognition globally with larger market penetration, particularly in China, the Center East, and APAC areas. For one, JKS gained the bid to supply 3.2GW N-type modules for China’s CHN Vitality Funding Group initiatives for Nationwide Vitality Transition initiatives. For one more, Jinko signed a 3.8GW module provide settlement of N-type Tiger Neo with Saudi Arabia Utilities Firm – ACWA Energy. This manifests the sturdy product demand for JKS’ N-Sort Merchandise. At the moment, N-type merchandise accounts for 60% of module shipments globally in Q3 2023.

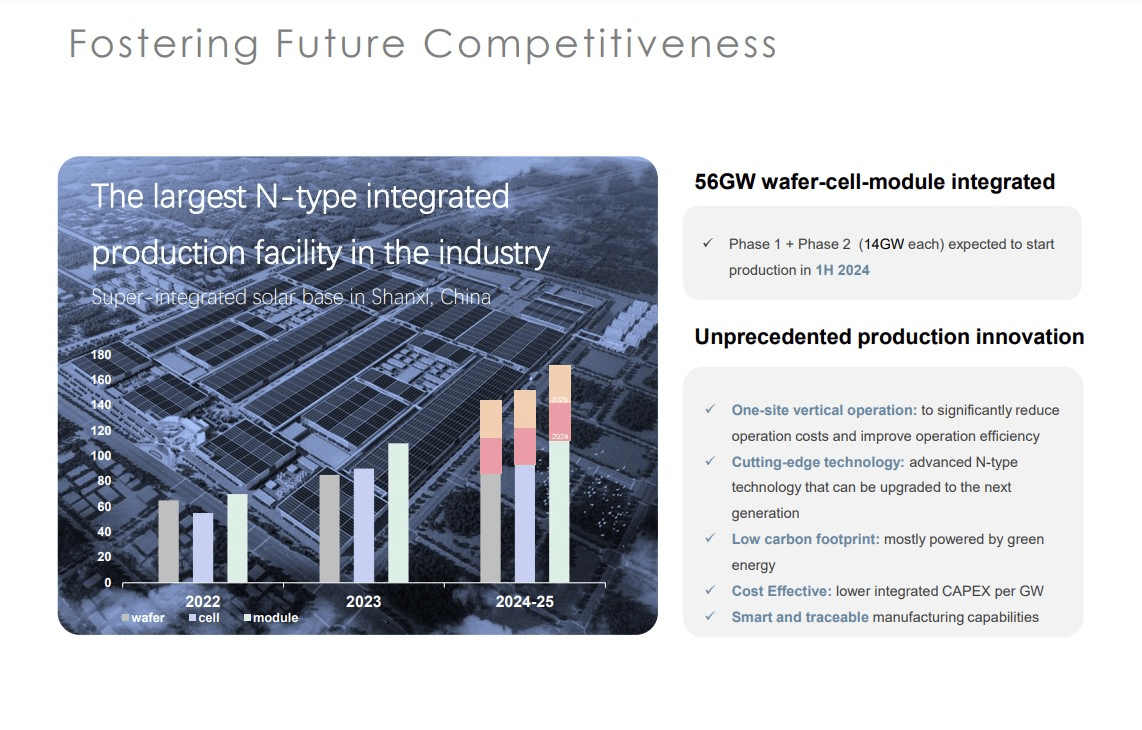

Enhanced Manufacturing Capability

Shanxi Manufacturing Plant (Traders Presentation)

By the top of Q3 2023, JKS already had over 55GW of N-type cell manufacturing capability. And by the top of this yr, N-type cell manufacturing capability is anticipated to achieve about 70GW, a aggressive capability construction main the {industry}.

Jinko has just lately began building for built-in initiatives in Shanxi, China, for Section 1 and Section 2 to handle the rising demand for its photo voltaic modules. Mixed, a complete of 28 GW wafer cell and module built-in capability are anticipated to start out manufacturing within the first half of 2024. Moreover, wafer and module abroad manufacturing is anticipated to ramp up in 2024, including an incremental 12GW of manufacturing capability (US Florida: 2GW). 75% of abroad capability can be used to provide N-type photo voltaic Cell Applied sciences

With increasing manufacturing services, I believe that Jinko can simply elevate its international module shipments capability in 2024, thus bringing in additional income and money stream to the agency.

Sturdy International Distribution Community

Whereas Jinko has a large distribution community not solely in China, but in addition has operations within the US, Europe, Center East, and ASEAN areas. Its upstream (Polysilicon Provide) and downstream provide chains is effectively diversified globally.

On the finish of Q3 2023, Jinko turned the world’s first module producer to have delivered 190GW photo voltaic modules, protecting over 190 international locations and areas. In Q3 alone, shipments had been 22,597 MW (21,384 MW for photo voltaic modules, and 1,213 MW for cells and wafers), up 21.4% QoQ, and up 108.2% YoY.

Administration workforce even promised shareholders that annual module shipments in 2023 will exceed its earlier targets of 70-75GW, and 23 GW alone for This fall 2023. This shall be excellent news for shareholders given the corporate has already delivered greater than one-third of historic shipments in 2023 alone. I believe that this displays the astonishing manufacturing quantity and powerful demand for its photo voltaic panels.

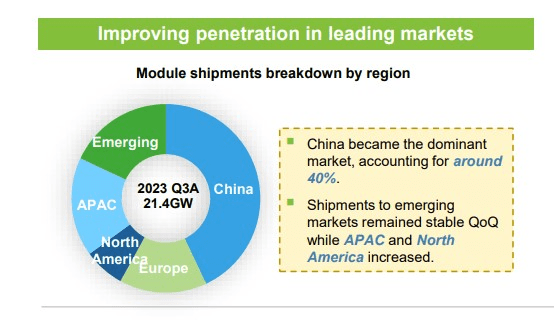

JKS Geographical Module Cargo Breakdown (Q3 2023 Traders Presentation)

At the moment, China takes up 40% of module shipments, which stays to be the most important marketplace for JinkoSolar. In the meantime, the administration count on a brand new set up report in China this yr given the broader renewable power adoption pattern in China. We can even probably see an rising demand within the US market because of the

Inflation Reduction Act (IRA), which entails the U.S. Authorities giving US residents subsidies to buy photo voltaic panels. Rising photo voltaic demand in Saudi Arabia and MENA can be anticipated to assist power transition. This may probably open up extra enterprise alternatives and complete addressable market (TAM) for Jinko sooner or later, thus bringing in additional income and money stream to the enterprise amidst the photo voltaic transition sooner or later.

Business tailwind: Rising renewable power transition demand in China

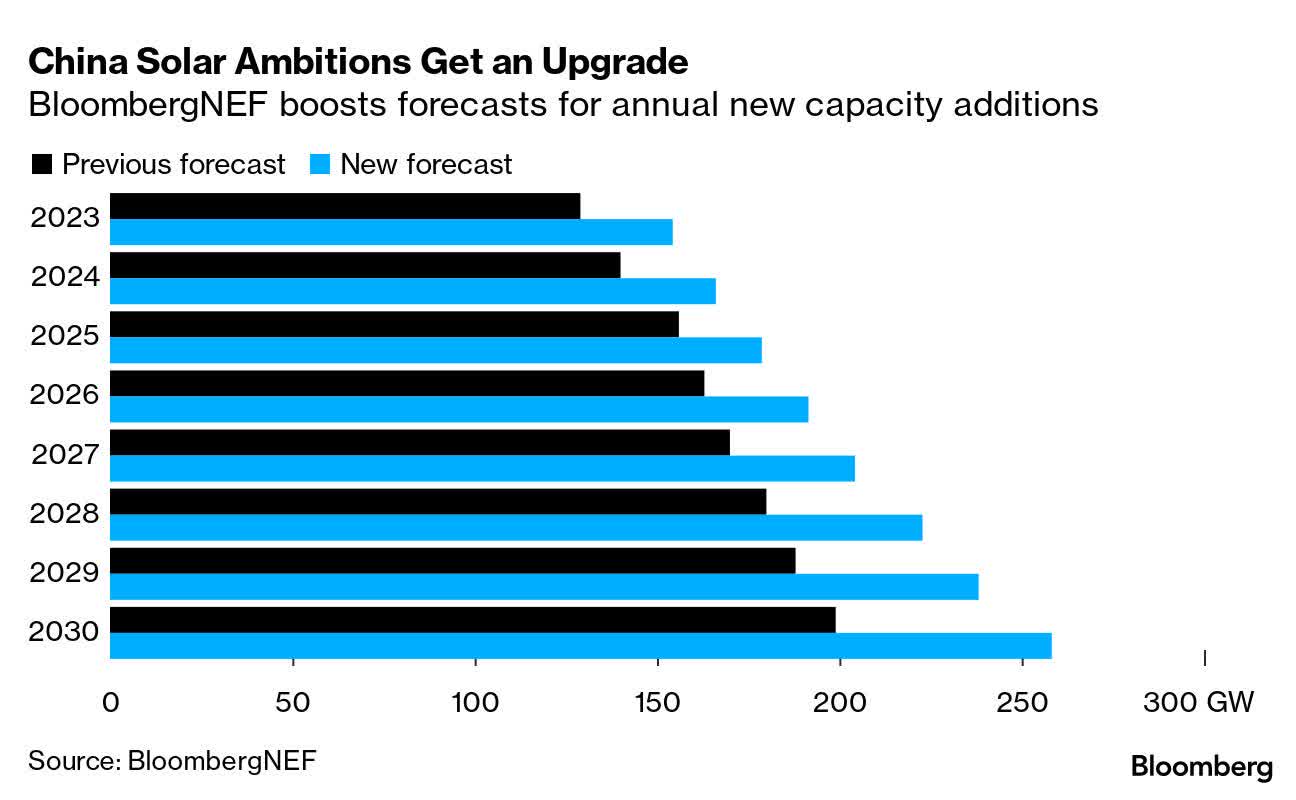

China Photo voltaic Sector New Capability Additions (Bloomberg NEF)

In keeping with Rystad Energy, China’s photo voltaic capability anticipated to hit 1,000 GW by 2026. And China had already put in 365 GW of wind energy capability and 392 GW of photo voltaic capability by the top of final yr – a few third of the world’s complete. The nation’s put in capability is anticipated to prime 500 GW by the top of 2023.

In the meantime, Bloomberg Estimates that China will see 175-200GW of latest photo voltaic capability additions in 2025-26 alone in China. Because of the Chinese language authorities’s 14th 5-year Plan, substantial subsidies, tax incentives, and beneficial insurance policies have been supplied to encourage the expansion of solar energy. These insurance policies created a conducive atmosphere for innovation and funding, positioning China as the worldwide photo voltaic expertise, manufacturing, and deployment chief. It provides a beneficial backdrop for Jinko to proceed its photo voltaic module shipments and set up in China, which gives an enormous addressable marketplace for Jinko to take advantage of.

Moreover, China will likely enter a interval of consolidation for its photo voltaic {industry} in 2024, which might see its Tier 2 and Tier 3 native photo voltaic producers dissipate because of the declining ASP of photo voltaic modules for a rise in manufacturing output. This could enable mega gamers like Jinko to seize their market share and stay dominant within the Chinese language and international market fields.

Monetary Evaluation

1. Respectable income and margins

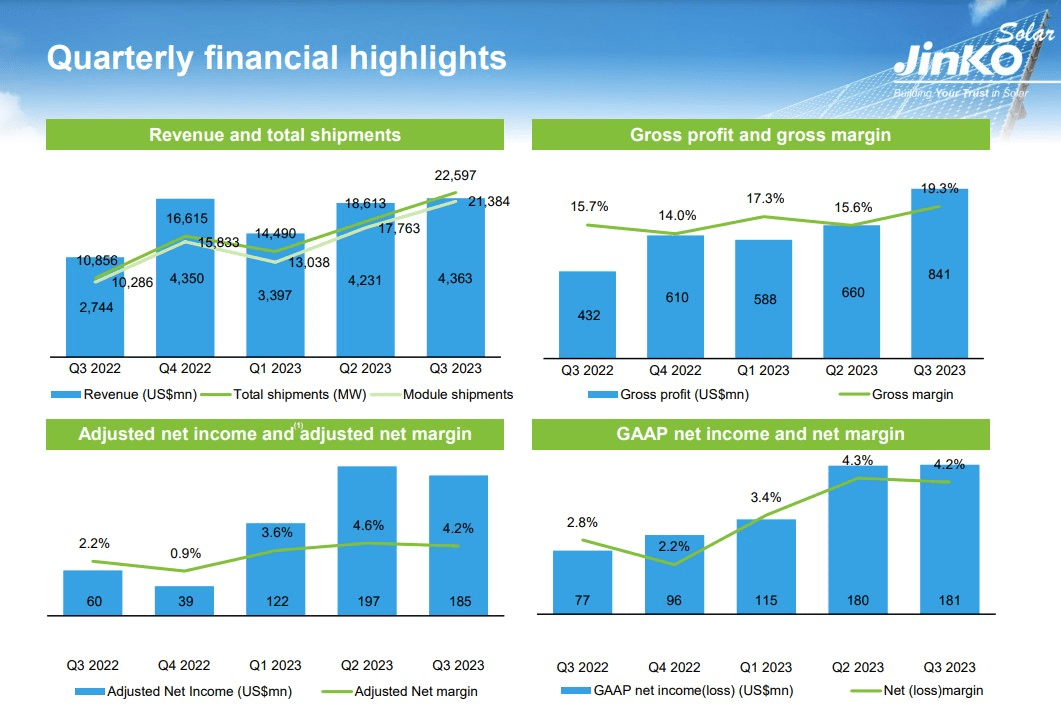

JKS Financials (Q3 2023 Traders Presentation)

General, Q3 2023 has been a fruitful quarter for JinkoSolar. Whole revenues had been US$4.36 bn, up 3.7% QoQ and up 63.1% YoY, in comparison with US $2.74bn in Q3 2022. We’ve got additionally seen nice margin expansions, which has seen 360 bps (3.6%) YoY enlargement from 15.7% in Q3 2022 to 19.3% in Q3 2023. That is stunning given the extreme competitors and the declining value of photo voltaic wavers. However, I believe this displays the price self-discipline and synergies created by its vertical integration mannequin, which has seen Jinko securing low-cost provides of Polysilicon from its suppliers from the US and Germany by way of its strategic investments in them.

Moreover, Web revenue was US$181.4 Mn, up 140.7% YoY, whereas Web Margins expanded 2% (200 bps) from 2.2% in Q3 2022 to 4.2% in Q3 2023.

Whereas Traders are frightened concerning the attainable cut-throat competitors out there, the administration workforce reiterated their stance to not minimize its Common Promoting Value (ASP) simply throughout a Bloomberg Interview regardless of the rising manufacturing competitors. This shall protect margins for Jinko within the coming years. Trying ahead, with extra photo voltaic module shipments anticipated and prudent value administration, this shall catalyze top-line and bottom-line development.

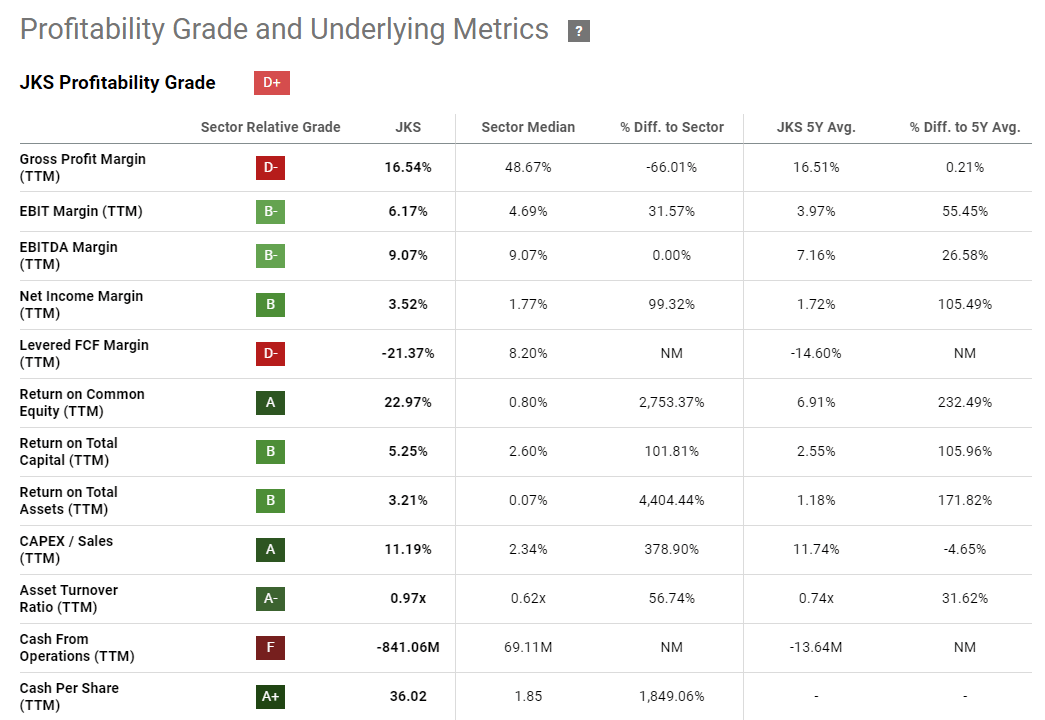

JKS Profitability Grade (Looking for Alpha)

Whereas I disagree with Looking for Alpha’s score for Jinko’s profitability rating as a D+, as I believe that’s too harsh, its ROE reached 22.97%, which is spectacular. One other factor price contemplating is its detrimental free money stream margin, which could possibly be a possible danger for the enterprise.

2. Steadiness Sheet Evaluation

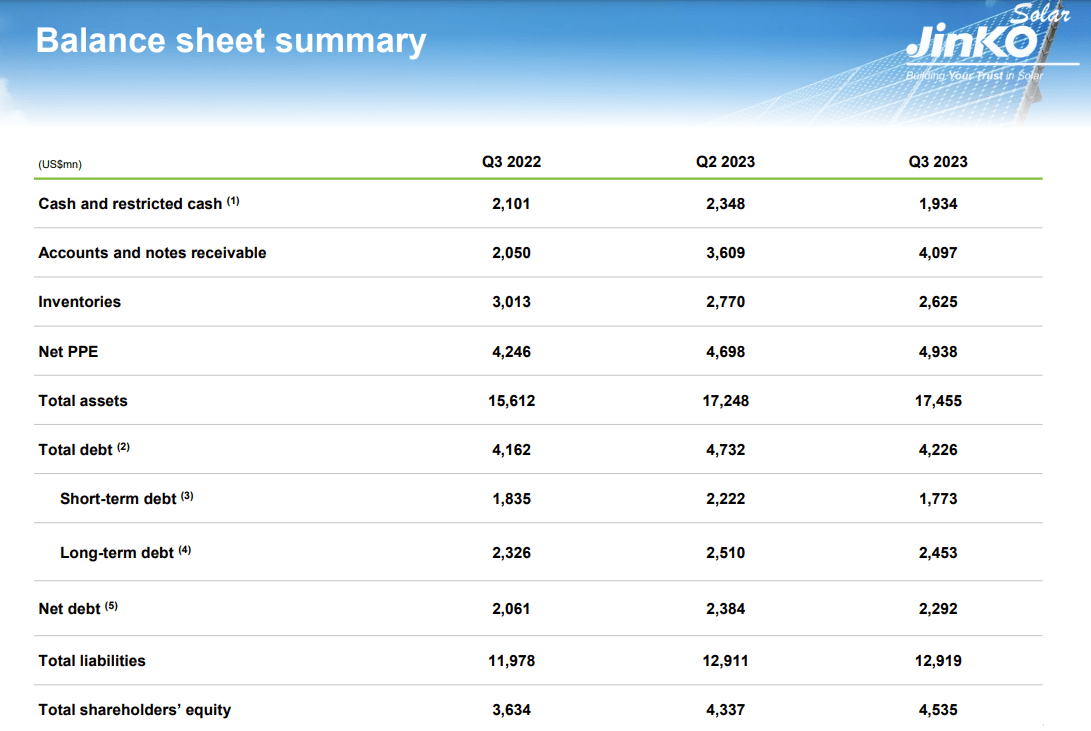

JKS Steadiness Sheet (Q3 2023 Traders Presentation)

Granted, JinkoSolar’s Steadiness Sheet wasn’t probably the most spectacular one which I’ve seen. Jinko had Money and short-term restricted money of US$1.93 bn as of finish of Q3 2023 vs US$2.35 bn as of finish of Q2 2023, representing a fall in money stage of US $42Mn within the area of 1 quarter largely as a result of dividend payouts. Whereas Web Debt reached US $2.29 Bn, EBIDTA amounted to US $607.4 Mn, this provides Jinko a Web Debt/EBIDTA ratio of round 3.77x, which can look a bit shaky and dangerous.

In the meantime, Present ratio sits at 1.1x as of Q3 2023. This means Jinko doesn’t have the chance of going bankrupt imminently. Whereas Debt to Fairness Ratio is 0.93x, which sits healthily under 1x. This displays the debt burden could look manageable for JinkoSolar. Hopefully, extra deleveraging campaigns can be launched by administration workforce to maximise shareholders’ long-term worth and reduce exterior leverage dependence.

However, the good information for shareholders is that the administration workforce was prepared to make use of its money to distribute dividends. In Sep 2023, the administration introduced a $1.5 dividend/share payout to shareholders, which has an ex-dividend date on twenty fourth Nov and a distribution date on sixth Dec.

I believe this illustrates that the administration workforce acknowledges and rewards shareholders. Nonetheless, I believe share buybacks and repurchase program launches sooner or later would additional add worth to shareholders over the long term.

Monetary Valuation: Undervalued

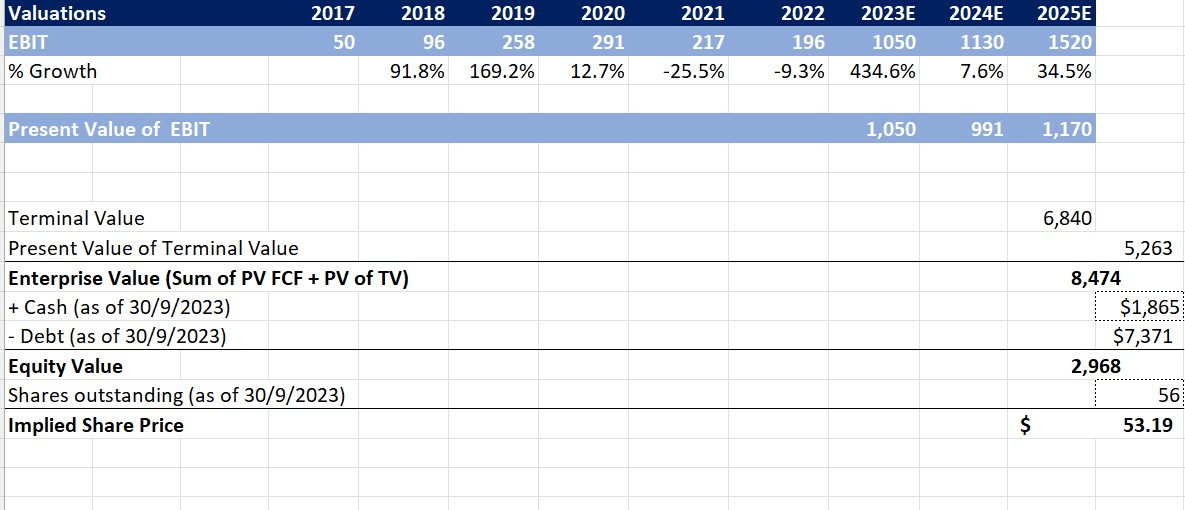

Valuations (KL Analysis)

For the reason that firm doesn’t produce optimistic FCF, I might use EV/EBIT (fwd) as my valuation instrument.

Based mostly on Analysts’ estimates, JKS’s EBIT is anticipated to be round $1.05B, $1.13B and $1.52B for this yr, 2024 and 2025 respectively.

Whereas JKS is now buying and selling at an EV/EBIT a number of of seven.5x, I are typically tremendous conservative and worth JKS at an EV/EBIT A number of of 4.5x, given the rising photo voltaic competitors in China. This provides JKS an Enterprise Worth of round $8.47B. By including again $1.87B price of money and subtracting $7.37B price of debt. I’ve arrived at an implied fairness worth for JKS of $2.97B

Dividing it by the variety of weighted common shares of 56 million, I’ve arrived an estimated truthful worth for JKS at round $53.19/share, implying a possible 66% upside.

To offer one other perspective, Morningstar values JKS at an estimated intrinsic worth of round $66/share.

This implies a good potential upside for JKS! Looks as if Mr Market is discounting JinkoSolar by a considerable margin.

Multiples Valuation: Grime Low cost

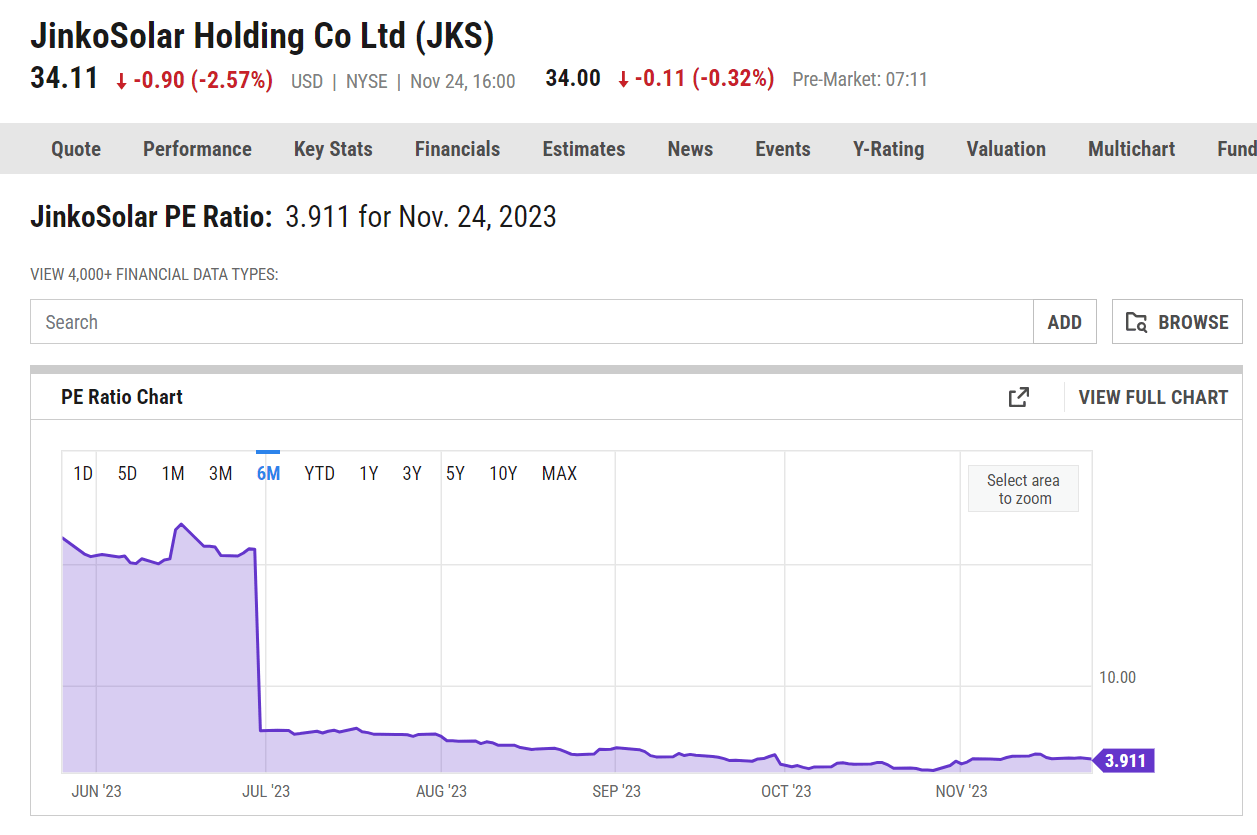

JKS PE (YCharts)

As we are able to see, JinkoSolar (JKS) is now buying and selling at a deep low cost, with its P/E ratio trending downwards and is now buying and selling at practically 3 – 4x earnings, which stays effectively under its opponents like First Photo voltaic (FSLR) and Enphase Vitality (ENPH) of round 25 – 35 x. Maybe JKS is a typical Ben Graham-style cigar-butt-style Deep Worth play.

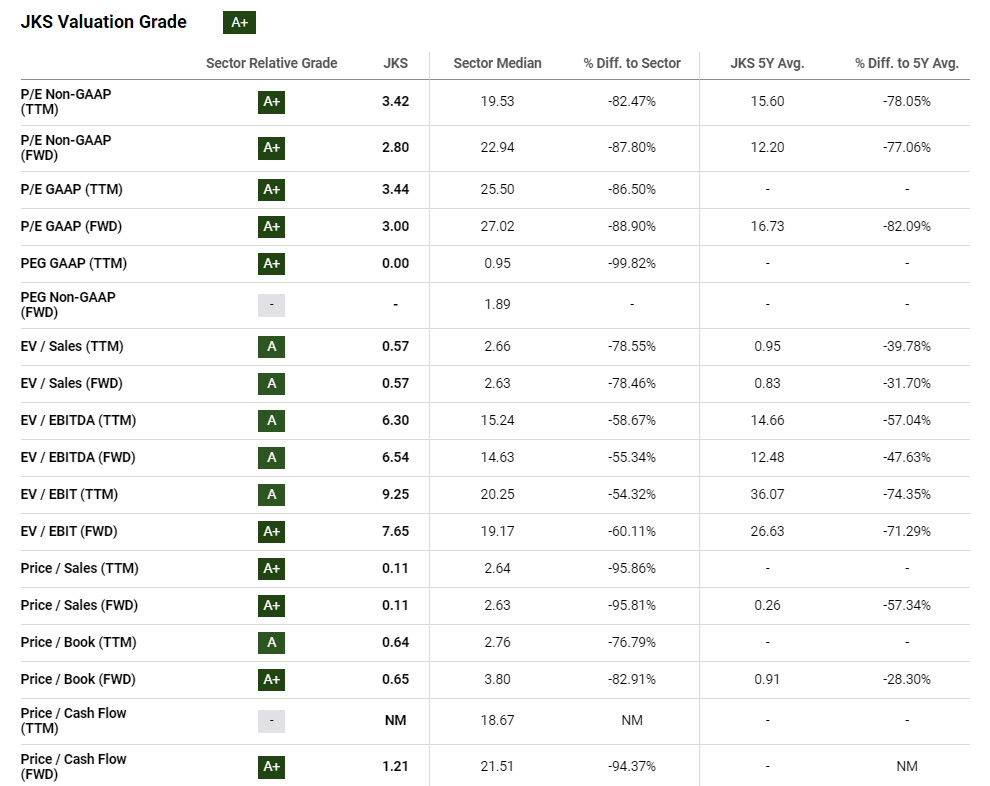

JKS Valuation Grade (Looking for Alpha)

Moreover, it’s nonetheless buying and selling at an enormous low cost in all multiples relative to its friends. For instance, it’s buying and selling at a whopping P/B a number of of simply 0.64x ebook worth and 0.7x tangible ebook worth, which has a ebook worth (BV) per share of $53.2 and tangible ebook worth (TBV) per share of $48.4 in line with Looking for Alpha.

As well as, its P/Money Circulate ratio sits at a whopping 1.21x, which doesn’t actually make a lot sense in any respect. Apparently, traders and Mr. Market are deeply discounting the upside potential of this inventory, and the shares look extraordinarily undervalued, which gives a golden shopping for alternative for traders looking for to achieve some publicity to deep worth play.

Potential Dangers

Regardless of its stable financials and underappreciated valuation, there are nonetheless some underlying dangers behind the enterprise which can be price contemplating earlier than you make investments.

1. Dwindling Photo voltaic Modules Costs

Initially, the extreme provide and manufacturing of Photo voltaic Modules and Cells in China has led to an enormous drop within the ASP of photo voltaic panels. In consequence, most traders are frightened concerning the potential “Race to the Bottom Price War” and margin contraction of photo voltaic firms in China, which might in flip undermine the long-term profitability of JKS.

Whereas it’s true that almost all Chinese language small photo voltaic producer can be pushed out of enterprise, this is not going to be the case of Jinko. Jinko leverages its aggressive benefit of getting economies of scale in its manufacturing, this can solely result in a interval of consolidation, the place Jinko stays well-positioned to take market share from small companies who couldn’t compete at a low value. Mixed with its built-in vertical manufacturing synergies, rising photo voltaic modules cargo and industry-leading photo voltaic applied sciences, I’m assured that JinkoSolar will navigate by way of the short-term headwinds.

2. Escalating US – China Geopolitical Tensions

Whereas its noteworthy that the elevated geopolitical tensions and rising financial fragmentation between China and the US will probably hamper JinkoSolar’s potential improvement. As an example, JKS acquired scrutinized by the US Authorities. The U.S. Division of Homeland Safety this yr raided a manufacturing unit and gross sales workplace operated by Jinko in Florida. This displays the rising mistrust between US and China, and Jinko, lamentably, would be the scapegoat of it.

However, regardless of its geopolitical headwinds, Jinko will probably proceed to increase within the US market. Below the Inflation Discount Act proposed by the US Authorities, Photo voltaic Firms can take pleasure in tax credit for photo voltaic manufacturing, whereas US residents will take pleasure in subsidies for photo voltaic modules set up. This may probably create extra downstream demand for Jinko for its photo voltaic modules’ cargo within the US.

In the meantime, Photo voltaic Cells and Modules produced by Jinko should not subjected to US excessive tariffs as most of them are made both within the US regionally (Florida), Malaysia and Vietnam. This provides JKS a pricing and price edge in comparison with its opponents within the US Market.

Conclusion

Upon researching the corporate’s fundamentals, I believe that JinkoSolar (JKS) is a Ben Graham Type Deep Worth play that apparently stays well-positioned for future development, because of the worldwide renewable power transition, {industry} consolidation, superior cutting-edge applied sciences, and diversified international enterprise operations. I additionally love the truth that the corporate enjoys secular development and enlargement on its income and margins over time.

Given its buying and selling at a closely discounted P/E a number of of 3x, with triple digits upside potential based mostly on the possession stake in its Chinese language subsidiary firm, I price JinkoSolar (JKS) as a good “Strong Buy”, providing a robust danger to reward perspective.