Leila Melhado/iStock Editorial by way of Getty Photographs

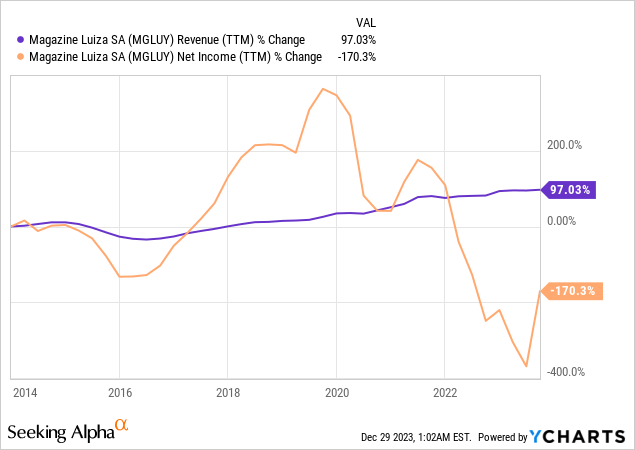

Journal Luiza (OTCPK:MGLUY), also referred to as “Magalu,” has undergone a major transformation in its efficiency over the previous a number of years. Between 2015 and 2020, the corporate’s inventory soared by a formidable 93,000%, reaching a valuation of R$160 billion, equal to round $32 billion.

Nevertheless, within the subsequent three years, the inventory skilled a downturn: a decline of 71% in 2021, adopted by a 62% drop in 2022 and an additional 41% lower in 2023.

TradingView

Regardless of the difficult financial surroundings for the retail sector, Journal Luiza’s shares have proven resilience. Elements akin to accounting inconsistencies within the third quarter and struggles amongst its Brazilian retail friends haven’t considerably shaken confidence in Magalu’s future. Notably, in December 2023, coinciding with Brazil’s fourth rate of interest lower (Selic), the shares surged by 29.21%, regardless of comparatively high-interest charges at 11.25% and a decline in client spending.

Whereas particular indicators of the corporate’s operations have proven enchancment, the latest revelation of accounting inconsistencies on this quarter provides a layer of elevated danger to the funding thesis.

Journal Luiza is traded on pink sheet markets outdoors Brazil via an unsponsored ADR, with a ratio of 4:1. Buyers needs to be cautious about potential illiquidity points and restricted info.

Journal Luiza’s Enterprise Mannequin Overview

Journal Luiza, one in all Brazil’s main retailers, has undergone numerous improvement cycles, together with increasing into the inside, coming into the São Paulo market, and embracing digital transformation. In 2019, the corporate shifted its focus to positioning itself as a digital retail platform and ecosystem.

5 pillars help this technique: (1) exponential development, (2) quicker supply, (3) the Superapp, (4) providing new product classes via {the marketplace}, and (5) “Magalu at your Service” (or Magalu as a Service).

With over 35,000 staff, the corporate operates over 1,100 bodily shops throughout 819 cities and 21 states in Brazil. It has 17 distribution facilities and makes use of Malha Luiza, comprising round 2,500 truck drivers, for logistics. The acquisition of Logbee, a logistics know-how firm, was an important milestone that considerably improved the person expertise by enhancing parcel supply effectivity. In 2020, greater than 50% of sunshine deliveries had been dealt with by Logbee, decreasing dependence on the Submit Workplace and minimizing the danger of delayed deliveries.

Magalu additionally operates Luizacred, a three way partnership with Itaú Unibanco (ITUB) since 2001. Luizacred, a 50/50 partnership, is significant in constructing buyer loyalty, enhancing gross sales efficiency, and enhancing profitability. It provides merchandise such because the Luiza Card (bank card), private loans, and payroll loans, contributing to elevated buyer purchases and total profitability.

The built-in nature of Journal Luiza, with its logistics and credit score segments, has positively impacted the profitability of its gross sales, solidifying its place as a key retailer in Brazil. Over the previous 4 years, the corporate’s initiatives have diluted working bills, substantial EBITDA and Web Revenue development, and highly effective working money era.

The Rise and Fall and Liquidity Issues

The interval from late 2015 to the height in 2020 marked a outstanding journey for Journal Luiza. Throughout this difficult interval, which included the troublesome years of 2015 and 2016, the retail sector in Brazil confronted elevated competitors from a number of home retailers. Right now, the market is strongly represented by world gamers akin to MercadoLibre (MELI) and Amazon (AMZN).

Magalu, focusing primarily on merchandise like stoves, fridges, smartphones, and televisions, survived and thrived whereas different firms struggled. Established manufacturers like Ricardo Eletro, Lojas do Baú, and even Grupo Casas Bahia (OTCPK:VIAYY) misplaced market share to Magalu. Via strategic partnerships, together with one with an insurance coverage firm for debt administration, Magalu emerged stronger.

Since then, the corporate has undergone vital adjustments. Capitalizing on falling rates of interest and a extra favorable credit score surroundings, Magalu invested in digitalization and enterprise diversification. CEO Fred Trajano performed an important position in main this transformation, bringing a digital focus to the corporate. The institution of Luiza Labs, a suppose tank devoted to retaining the corporate technologically superior, proved pioneering, positioning Magalu forward of many conventional retailers in the course of the transition to the digital surroundings.

Regardless of experiencing strong and euphoric preliminary income development and web revenue, the pandemic additional accelerated the corporate’s constructive trajectory. Within the “new normal,” the place folks sought merchandise to boost their dwelling experiences, Magalu stood out with its well-established on-line service. The pandemic, initially seen as a possible setback, turned out to be a chance for firms with a strong on-line presence.

Nevertheless, the optimistic section of on-line retail was adopted by a hangover. Overly optimistic expectations for the way forward for e-commerce and retail have been shattered. This underscores the complexity and dynamics of the market, the place adaptability and steady innovation are important to maintain success.

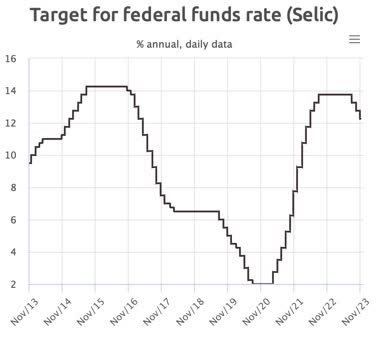

The predominant issue, for my part, was the rate of interest. In 2020, Brazil had an rate of interest of two%. On this situation, there are inherent dangers, and traders are prepared to pay a premium for retailers and the potential future earnings they’ll ship.

Banco Central do Brasil

Nevertheless, this rate of interest rose to virtually 14% in 2022 and continued till 2023. Despite the fact that it’s now in an interest rate cut situation in Brazil, it’s anticipated to stay above 9% for 2024, which ought to proceed to make traders extra selective. Firms that require intensive funding and closely depend on capital could start to undergo in the event that they lack strong monetary administration, and this has been the case with Journal Luiza since 2020.

It’s essential to notice that a number of firms are beginning to really feel the impacts of this abrupt change in rates of interest in Brazil. This phenomenon has affected one firm and a number of other others throughout the sector.

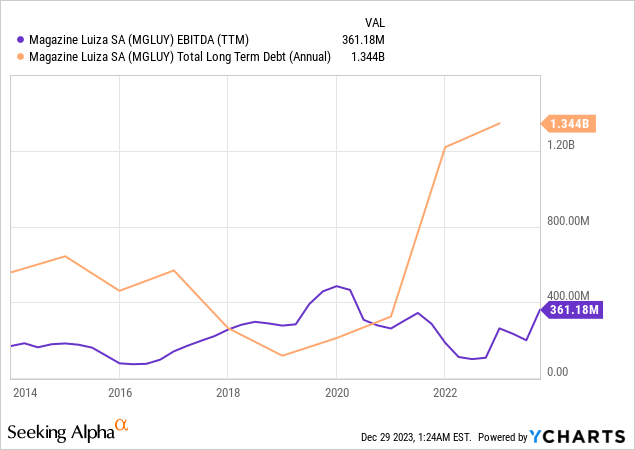

Because of the traits of the retail sector, which calls for a major quantity of working capital, Journal Luiza’s debt has been steadily rising since 2021. EBITDA has been oscillating downwards, with slight enhancements all through this 12 months, however nonetheless at ranges a lot decrease than these seen in 2020.

This example has positioned Journal Luiza in a precarious place. To maintain its development, the corporate requires investments, and if it can not generate adequate money, it’s compelled to tackle rising ranges of debt. Consequently, the corporate has made fairness choices to fortify its steadiness sheet. Nevertheless, this strategy comes at a value – it dilutes its shareholders and considerably impacts the corporate’s share value.

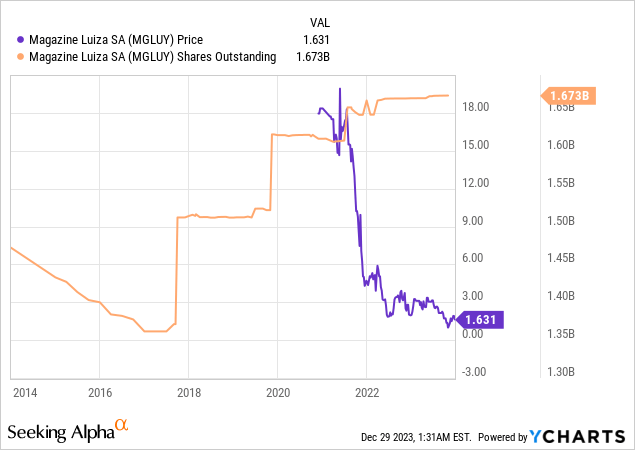

Since 2017, the corporate has issued roughly 270 million new shares, leading to a pointy decline in Journal Luiza’s share value. Presently, its ADR trades at simply over $1 per share.

For Journal Luiza, a fast ratio of 0.64 means that the corporate could encounter challenges in fulfilling its short-term obligations with its most liquid belongings. Having $0.64 in extremely liquid belongings obtainable for each $1 of present liabilities, the ratio signifies a possible liquidity concern. Nevertheless, the corporate additionally maintains a present ratio of 1.14.

The truth that the short ratio is decrease than the present ratio means that a good portion of the present belongings could encompass much less liquid objects, akin to inventories. This suggests that the corporate could have to depend on promoting these much less liquid belongings to fulfill its short-term obligations.

There is a cautionary sign in case there isn’t any vital restoration within the Brazilian retail sector, leading to improved money era for Journal Luiza. The long run won’t be promising for the corporate.

Journal Luiza’s Newest Outcomes: Making Progress

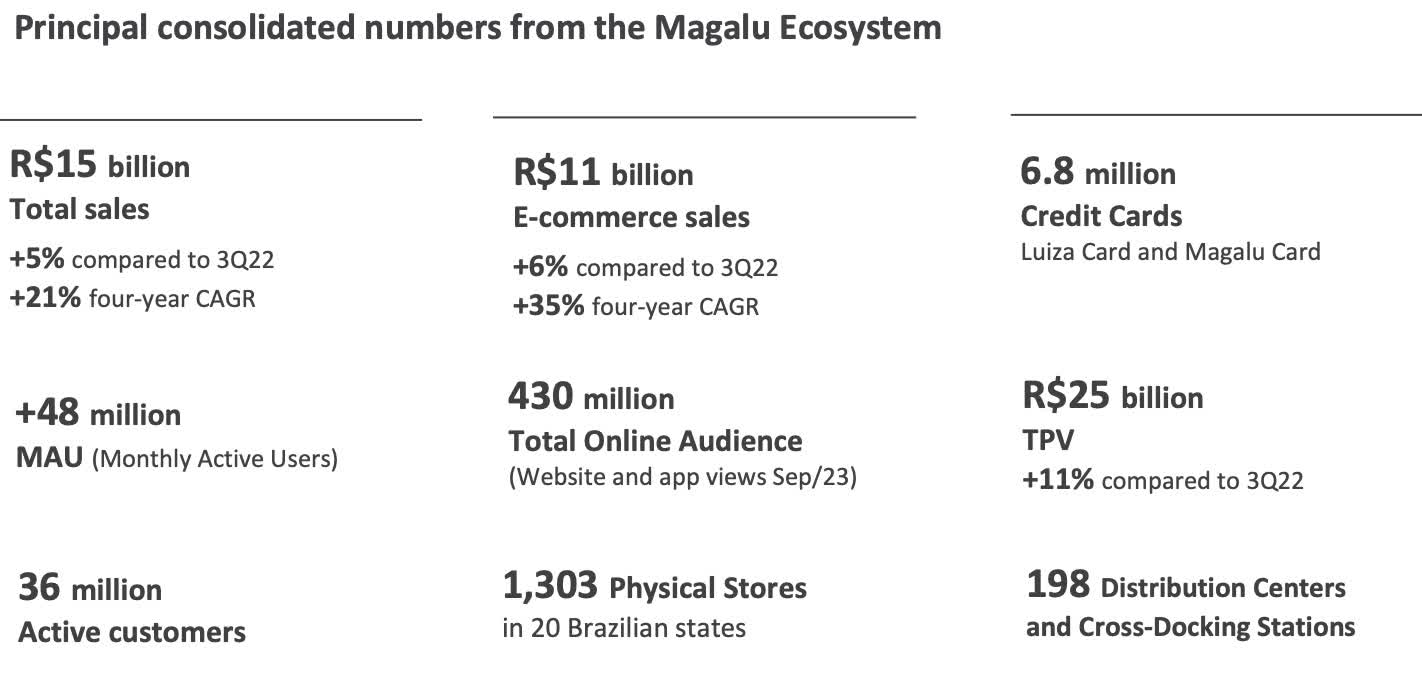

Within the third quarter of 2023, whole gross sales amounted to R$14.8 billion, representing a 4.8% year-over-year (YoY) improve. Bodily shops maintained practically the identical gross sales stage YoY (+2.3% YoY), whereas on-line gross sales with personal inventory (1P) declined by 4.2% YoY, and market gross sales (3P) elevated by 24.8% YoY.

Magalu’s IR

Though the expansion in Gross Merchandise Quantity (GMV) was pushed by market gross sales, which impression income by recognizing solely the fee charged to the vendor (take price), web income skilled a 2.6% YoY decline.

Adjusted EBITDA mirrored the decline in web income, falling 2.7% YoY. The rise in promoting, common, and administrative bills as a proportion of web income by 3.1 p.p. YoY was offset by the rise in gross margin, sustaining the Adjusted EBITDA margin at 5.3% YoY.

The online consequence for the quarter benefited from the popularity of tax credit amounting to R$523.8 million. This non-recurring occasion led to a web revenue of R$331 million in 3Q23, in comparison with a lack of R$191 million in the identical interval the earlier 12 months.

Excluding this occasion, Journal Luiza would have reported a lack of R$143 million, emphasizing the discount within the unfavourable impression of the online monetary consequence as a proportion of web income by 1.0 p.p. YoY.

Concerning monetary leverage, there was a rise of R$255.3 million in gross debt YoY however a discount of R$923.4 million in web debt. Consequently, the corporate ended the quarter with R$4.1 billion in web debt, equal to 2.1x Adjusted EBITDA over the past 12 months, with 40.6% of the debt maturing within the brief time period.

Notably, there was a constructive era of R$926 million in free money circulation within the quarter, with the spotlight being the era of R$1 billion in working exercise. Within the first 9 months of 2023, free money circulation totaled R$2.4 billion, a major enchancment in comparison with the consumption of R$754 million in the identical interval of 2022.

Accounting Practices and Tax Credit Increase a Yellow Flag

Journal Luiza issued a material fact after releasing its third-quarter outcomes, revealing recognized inaccuracies in accounting entries associated to bonuses in particular industrial transactions. These inaccuracies stemmed from recording gross sales marketing campaign launches on steadiness sheets earlier than the conclusion of those campaigns.

To rectify this error, the corporate adjusted the corresponding accounting entries, resulting in a discount in shareholders’ fairness of R$829.5 million as of June 30, 2013. Notably, this adjustment didn’t impression money circulation and was web of taxes.

Concurrently, the corporate reported the popularity of tax credit amounting to R$507.4 million (web of taxes). This recognition was based mostly on a latest ruling by the Brazilian Superior Courtroom of Justice (“STJ”), which clarified that PIS/COFINS shouldn’t be levied on suppliers’ reductions, bonuses, and rebates. Contemplating these changes, the online shareholder fairness discount amounted to R$322.1 million.

This unfavourable improvement indicates accounting inconsistencies inside Journal Luiza’s practices. These inconsistencies had been recognized after an investigation triggered by an nameless criticism.

Whereas the criticism was in the end deemed unfounded, the need to revise accounting entries and implement measures to boost inside management mechanisms introduces uncertainties relating to the presence of undisclosed inconsistencies. This, coupled with considerations in regards to the firm’s company governance, provides danger to the funding thesis, paying homage to Brazilian retailers’ challenges, exemplified by the Americanas case.

Journal Luiza, managed by the Trajano and Garcia household (58%), has its shares on Ibovespa (MGLU3) listed on the Novo Mercado, representing the very best normal of company governance within the Brazilian market. An encouraging side is Magalu’s Board of Administrators, which boasts an impartial majority with 4 out of seven members, aligning with constructive facets of the Environmental, Social, and Governance (“ESG”) framework.

One other essential side to contemplate is that, from Journal Luiza’s perspective, the accounts receivable from installment gross sales (a typical follow in Brazil) – although not money owed within the conventional sense – symbolize a major side of financing for the corporate. These receivables mirror extending credit score to clients and deferring the receipt of installment gross sales.

Whereas they don’t incur direct monetary prices, accounts receivable impression Magalu’s money circulation, as they tie up capital quickly till these receivables are transformed into liquid sources. This underscores the significance of efficient money cycle administration and the need for working capital to maintain operations whereas the corporate awaits cost for these installment gross sales.

Magalu experiences a complete debt of $2.18 billion however has $1.22 billion in accounts receivables. In follow, if vital default issues happen in its accounts receivable, these may symbolize the same magnitude of debt. Defaults may threaten working money circulation, necessitating loss provisions and harming the corporate’s web revenue and total monetary well being.

Valuation: Low cost or “Value Trap”?

Undoubtedly, Journal Luiza is buying and selling at valuations that align extra with its enterprise’s actuality than the final two years.

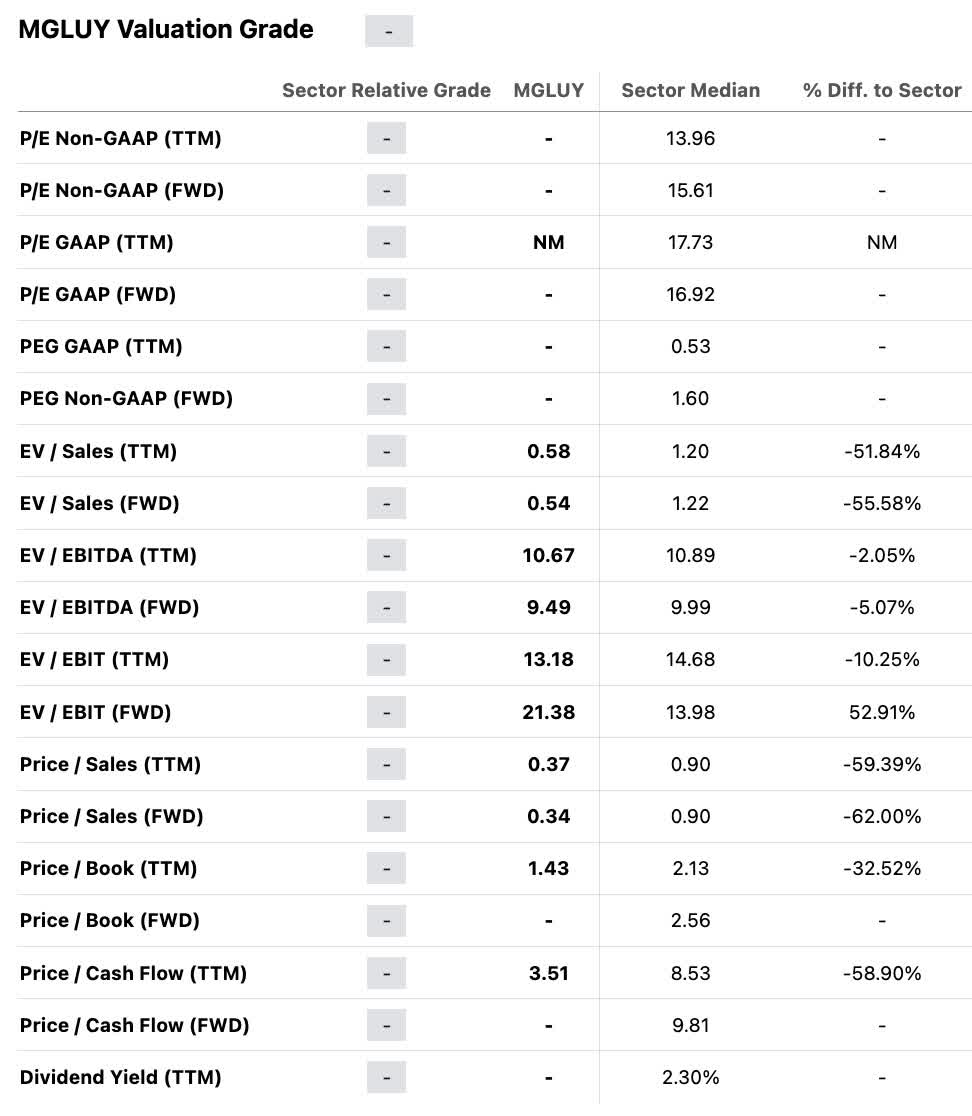

Journal Luiza trades at a price-to-book ratio of 1.43, 75% under its historic common over the past decade. Moreover, it has a ahead EV/EBITDA of 9.49x, which is 55% under its historic common over the identical interval. These valuations are very a lot according to the retail sector common.

In search of Alpha

Nevertheless, is Journal Luiza, together with the retail sector in Brazil, genuinely cheap?

With year-to-date declines of just about 80% for main firms within the sector—particularly Grupo Casas Bahia—reaching the standing of penny shares, taking a place in these belongings is likely to be falling right into a “value trap” (i.e., when a inventory seems to be at a reduction however is definitely undervalued as a result of it is a unhealthy deal).

As depicted within the chart under, Ibovespa at the moment displays a considerable brief curiosity within the retail sector, with a 12.2% brief curiosity in Journal Luiza’s shares. This displays the prevailing pessimism in direction of the business, significantly following the accounting scandal involving Americanas.

XP Inc.

Regardless of having a brief curiosity of 12.2%, Journal Luiza’s lending price is 8%. This means that the supply of shares to borrow shouldn’t be very excessive, particularly in comparison with Americanas. This could possibly be attributed to Journal Luiza’s already extensively diluted float. Theoretically, this issue makes the thesis much less inclined to a turnaround or a brief squeeze.

The Backside Line

Journal Luiza ought to proceed strengthening its on-line presence as the corporate solidifies a better stage of maturity within the digital channel and an more and more strong ecosystem relating to product selection and infrastructure to help gross sales.

With a extra developed digital channel contributing to the corporate’s working leverage and the top of the rate of interest hike cycle assuaging stress on monetary bills, Journal Luiza’s outlook for the long run seems extra constructive within the coming months.

I foresee extra constructive indicators for the e-commerce sector in anticipation of financial enchancment. Following a difficult interval with high-interest charges and inflation impacting client buying energy, I consider the inhabitants will progressively return to consumption patterns in 2024, offering the e-commerce sector extra momentum.

Due to this fact, Journal Luiza is well-positioned to capitalize on this improved situation. The ecosystem created by the corporate is predicted to proceed driving the expansion of digital operations, enabling the corporate to realize market share additional regardless of the heavy presence of MercadoLibre in Brazil.

Furthermore, the conclusion of the rate of interest hike cycle ought to profit Magalu, facilitating a gradual discount in monetary bills and assuaging stress on the corporate’s revenue.

Whereas acknowledging the corporate’s development potential, I acknowledge that Magalu could face short-term pressures resulting from its excessive leverage, with practically $600 million in debt due within the brief time period, and the potential repercussions of the accounting inconsistencies disclosed within the press launch. It would not be stunning to see an announcement of a Journal Luiza follow-on within the coming months to cut back leverage and handle liquidity to facilitate the corporate’s development within the coming years. Nevertheless, regardless of the corporate’s trace that, after the gross margin restoration within the third quarter of 2023, the plan is to settle operations with its personal money, I stay fairly skeptical.

Till Journal Luiza addresses these points, I preserve my impartial advice for the corporate.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.