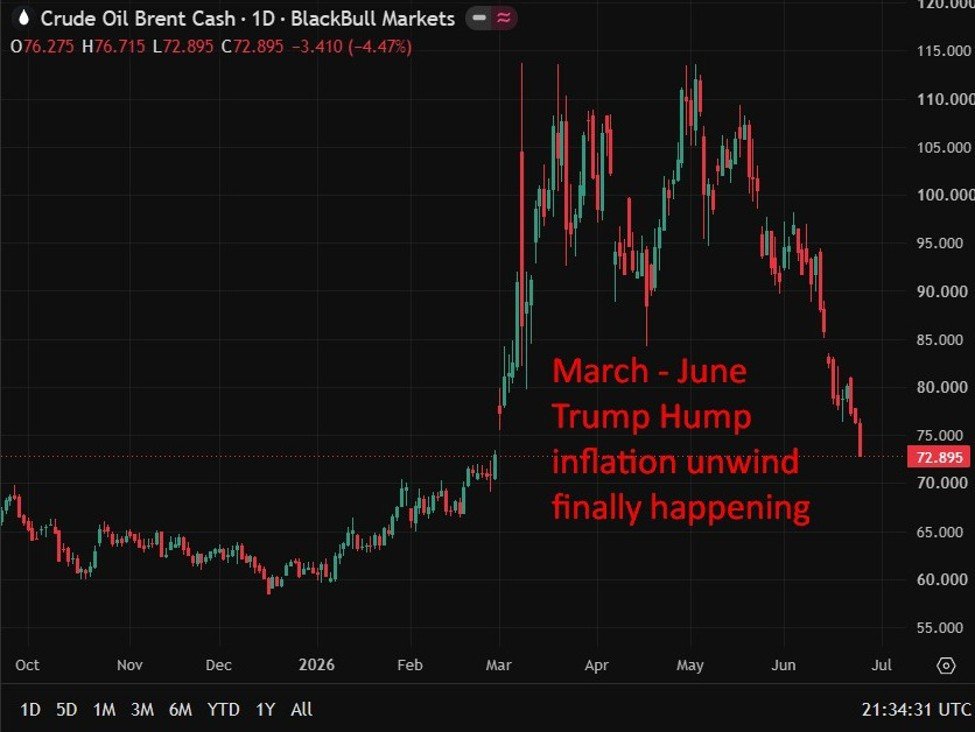

A year-end Brent target of $78 from JP Morgan suggest a directional anchor for the market, reinforcing the bearish H2 drift that has been building in consensus since the Iran ceasefire removed the geopolitical premium. The detail on private operators refusing to draw commercial stocks is particularly significant for price structure: it means the apparent tightness being engineered by SPR releases is masking underlying market softness, and once government reserve injections slow or reverse, the cushion disappears. The projected oversupply in Q4 2026 and H1 2027 suggests the OPEC+ production management question, specifically whether members can credibly curtail output in early 2027, will be the dominant price driver heading into year-end. The constructive supply outlook for Venezuela, Iran, Brazil, Guyana, Argentina, Canada and the United States compounds the bearish 2027 setup and raises the bar for any sustained price recovery.

—

JP Morgan cut its H2 2026 Brent forecast to $86/bbl in Q3 and $80 in Q4, targeting a year-end exit at $78, citing weaker-than-expected demand and below-forecast OECD inventory draws.

Summary:

- JP Morgan lowered its H2 2026 Brent crude price forecasts on Wednesday, now projecting Q3 at $86 per barrel, Q4 at $80 per barrel, and a year-end exit price of $78

- The bank cited below-forecast OECD commercial inventory draws and larger-than-expected demand losses as the drivers of reduced upward price pressure, per the research note

- JP Morgan said the oil market has rebalanced through a materially different combination of demand losses and inventory withdrawals than originally modelled, per the note

- Oil flows are currently running at approximately 8.6 million barrels per day and have averaged 6.3 million barrels per day in June, above April and May levels, according to JPM

- Private operators have largely declined to draw down commercial oil stocks, relying almost entirely on government Strategic Petroleum Reserve releases to keep refineries supplied

- The bank expects OECD inventories to draw by an additional 50 million barrels between April and July, and said production will likely need to be curtailed in early 2027 following a period of maximised output in late 2026

- JP Morgan said the market will enter 2027 with a constructive supply outlook from Venezuela and Iran alongside expected production growth from Brazil, Guyana, Argentina, Canada and the United States

JP Morgan cut its Brent crude oil price forecasts for the second half of 2026 on Wednesday, projecting a year-end exit price of $78 per barrel and flagging a structural oversupply building into 2027 that may force production cutbacks from major producers early in the new year.

In a research note, the bank set Q3 2026 Brent at $86 per barrel and Q4 at $80, trimming its previous targets on the back of weaker commercial inventory draws across OECD economies and demand losses that have run larger than the bank had anticipated when its prior forecasts were constructed. The combination has reduced the upward pressure on prices that JP Morgan had expected to materialise through the middle of the year.

The bank described the oil market’s rebalancing process as having played out through a meaningfully different mix of forces than originally assumed, with demand weakness doing more of the heavy lifting than inventory dynamics. OECD commercial inventory draws have fallen short of expectations, while the demand side has deteriorated by more than modelled. JP Morgan expects OECD inventories to draw by a further 50 million barrels between April and July, but the pace and composition of that process has shifted the bank’s confidence in the price recovery it had previously anticipated for the back half of the year.

One of the more structurally significant findings in the note concerns the behaviour of private oil operators. JP Morgan said private sector participants have largely declined to draw down their own commercial stocks, instead relying almost entirely on government Strategic Petroleum Reserve releases to maintain refinery throughput. That pattern suggests underlying commercial market tightness is less robust than headline supply-demand balances might indicate, since SPR releases represent a finite and politically managed source of supply rather than a market-driven response to price signals.

On the flow side, the bank noted that oil shipments are currently running at approximately 8.6 million barrels per day, with the June average so far coming in at around 6.3 million barrels per day, a level materially above what was recorded in April and May.

Looking further ahead, JP Morgan flagged that the scale of projected oversupply in Q4 2026 and the first half of 2027 points toward the need for production curtailments in early 2027, following a period of maximised output late this year. The bank added that the market will move into 2027 with a constructive supply-side outlook, incorporating expected production growth from Venezuela, Iran, Brazil, Guyana, Argentina, Canada and the United States, a combination that compounds the bearish pressure on the price trajectory and raises the stakes for OPEC+ cohesion heading into the new year.