PeopleImages

JPMorgan Chase & Co. (NYSE:JPM) buyers who braved the pessimistic selloffs in March and October have been duly rewarded, as JPM led the restoration towards its monetary sector (XLF) friends. Primarily based on my Purchase scores on JPM in March and September, they’ve considerably outperformed the S&P 500 (SPX, SPY), however JPM not being a development play. Regardless of that, JPM has proved its resilience, as its 10Y whole return CAGR of 14.4% outperformed its XLF friends considerably (10%) over the identical interval.

Given the normalization in JPM’s earnings a number of, I imagine it is well timed for me to replace JPM buyers on whether or not it is acceptable to attend for a wholesome pullback earlier than shopping for extra shares.

JPM remains to be anticipated to maintain its 17% RoTCE goal, however an anticipated 20% to 25% increase in capital necessities. Given the power of JPM’s market-leading deposit franchise and well-diversified income segments, it is affordable to anticipate the preeminent U.S. financial institution to “optimize its business in response.”

In an early November 2023 convention, CFO Jeremy Barnum harassed that the financial institution is “over-earning” towards its normalized NII development cadence. Consequently, JPM reminds its buyers to stay targeted on a “through-the-cycle” method and “not becoming accustomed to unusually high returns.” In different phrases, I imagine JPMorgan has began getting ready its buyers for a a lot slower earnings development cadence in 2024, because the Fed telegraphed three fee cuts.

Wall Avenue analysts have already penciled in a development normalization part in 2024. Accordingly, JPMorgan is estimated to put up an adjusted EPS of $15.43, down 7% from this yr’s $16.66 estimates. As well as, development in 2025 can also be anticipated to stay languid, with a 1.6% YoY enhance in adjusted EPS. Subsequently, JPMorgan buyers are reminded to organize for a peak in JPMorgan’s earnings development cycle that would lengthen previous 2025.

Apparently, the resurgence in JPM shares, because it broke decisively above its early August 2023 highs, probably surprised the naysayers. The crucial query is, given its over-earning part if the market is anticipated to cost in steep development normalization headwinds, why did JPM nonetheless put up such a big surge?

I imagine the reply is simple. The market allowed JPM’s valuation to revert towards its long-term common because it unleashed the shackles on JPM, anticipating the height within the Fed’s fee hikes. However the current restoration, JPM final traded at a ahead adjusted EPS a number of of 11x. It is nonetheless barely beneath its 10Y common of 11.6x. In different phrases, JPM nonetheless is not within the implied overvaluation zone. Subsequently, the market re-rated JPM’s valuation, suggesting it believes the worst in JPMorgan’s headwinds are over.

Nevertheless, it is also crucial to notice that we aren’t anticipated to return to the low rate of interest pre-COVID days that would spur a surge in lending development. As well as, the robust comps towards JPMorgan’s earnings development in 2024 may put a lid on additional potential upside because the market assesses the end result of the rise in capital necessities. In different phrases, it is affordable to imagine that JPMorgan Chase & Co. inventory should not be anticipated to commerce properly above its 10Y common within the close to time period, regardless that JPM’s value motion stays bullish. Let me clarify.

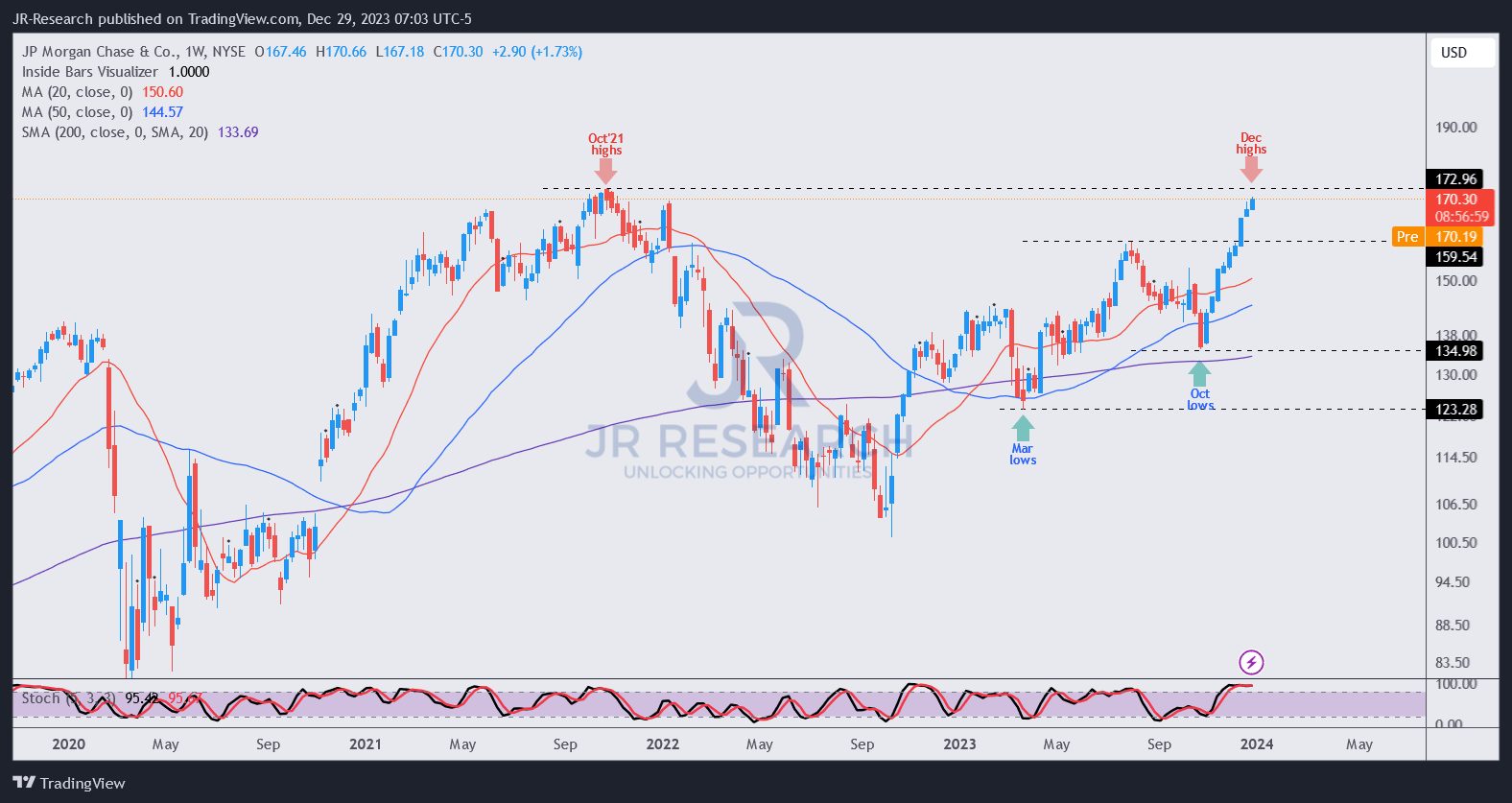

JPM value chart (weekly) (TradingView)

JPM’s almost vertical surge because it closes in towards its October 2021 highs remains to be bullish, as there is not any bull entice assessed. The breakout towards its August highs was additionally profitable and decisive (no false traps). As well as, it may proceed to grind greater to re-test its 2021 highs earlier than discovering promoting resistance.

The present breakout additionally indicated a better excessive and better low value construction, ascertaining JPM’s medium-term uptrend bias. In different phrases, JPM’s subsequent pullback must be capitalized by buyers who failed so as to add on its March and October 2023 lows.

JPM’s surge has probably attracted momentum buyers into the fray. Nevertheless, my evaluation suggests the chance/reward upside is way much less engaging on the present ranges when you’ve got not added it.

With my bullish thesis on JPMorgan Chase & Co. enjoying out because the market re-rated and normalized its valuation towards its 10Y common, I imagine shifting to the sidelines from right here is well timed.

Score: Downgraded to Maintain.

Vital notice: Buyers are reminded to do their due diligence and never depend on the data supplied as monetary recommendation. Please at all times apply impartial pondering and notice that the ranking isn’t supposed to time a selected entry/exit on the level of writing except in any other case specified.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a crucial hole in our view? Noticed one thing essential that we didn’t? Agree or disagree? Remark beneath with the intention of serving to everybody in the neighborhood to study higher!