Yuji Sakai

Kaiser Aluminum Company (NASDAQ:KALU) just lately reported higher than anticipated quarterly earnings, and the outlook for 2024 consists of web gross sales development and EBITDA development. With a diversified product providing, KALU additionally promised web debt/EBITDA discount, lean manufacturing, and different operational effectivity efforts, which can deliver web revenue development and dividend development within the coming years. There are clear dangers coming from opponents, various manufacturing choices, and supplies. As well as, delivered web gross sales could possibly be decrease than anticipated. Regardless of all this, I imagine that Kaiser Aluminum seems undervalued at this cut-off date.

Kaiser Aluminum Presents Technically Difficult Functions With International Distribution

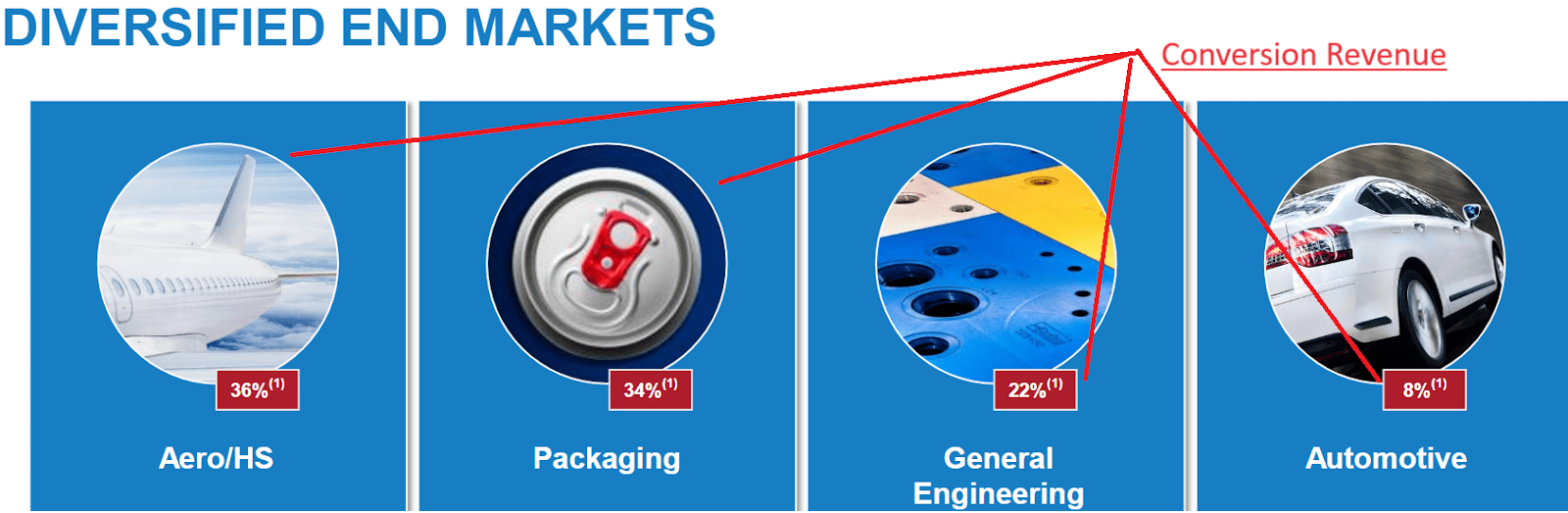

Kaiser Aluminum specializes within the manufacture and sale of semifinished aluminum merchandise for varied finish purposes, together with Aero/HS Merchandise, Packaging, GE Merchandise, Automotive Extrusions, and other products.

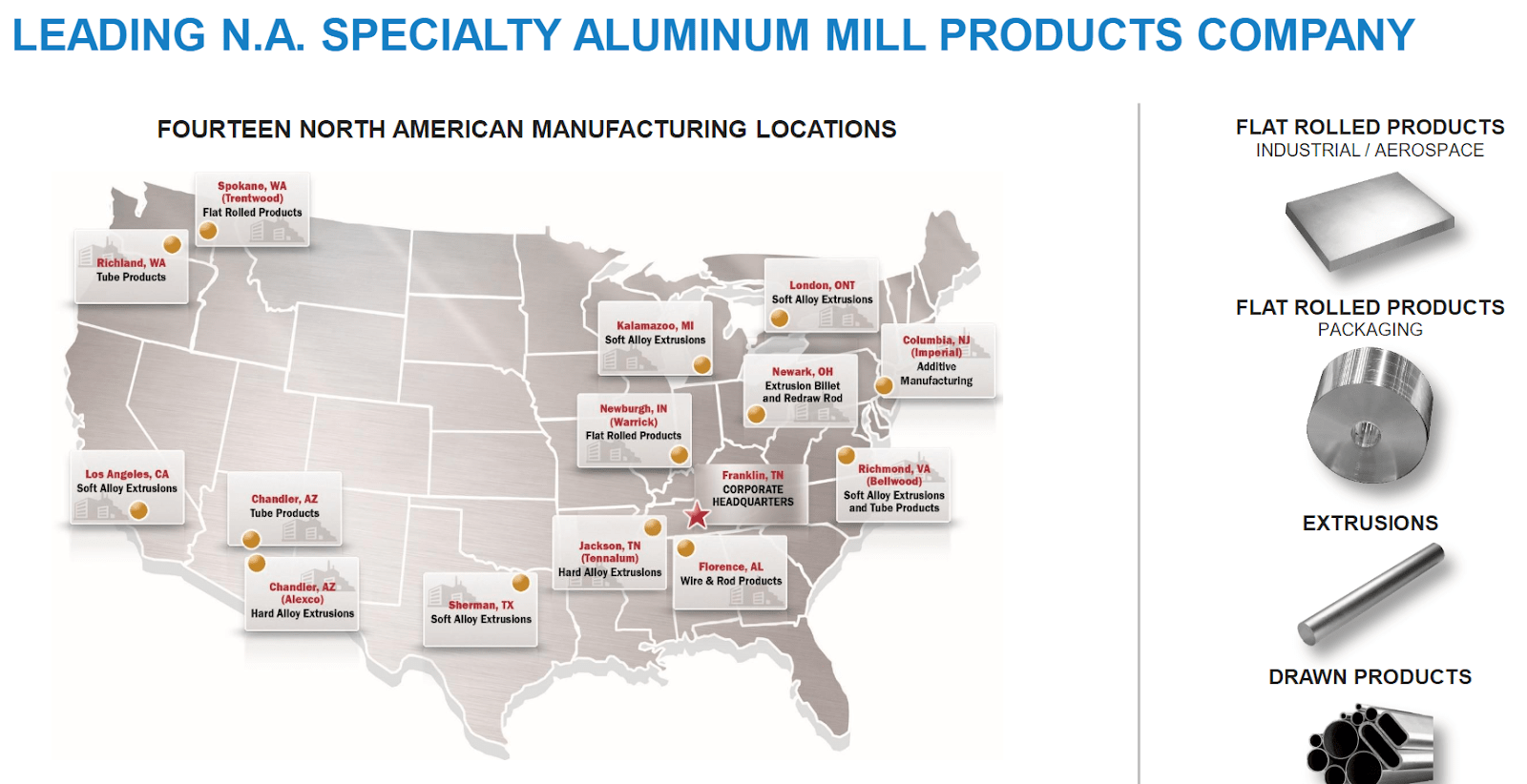

For my part, the corporate doesn’t solely appear to supply diversification of actions, but additionally a geographically diversified enterprise profile. Manufacturing services are situated everywhere in the nation.

Supply: Kaiser Aluminum Enterprise Replace February 2024 Supply: Kaiser Aluminum Enterprise Replace February 2024

The corporate’s focus is on technically difficult purposes requiring particular metallic properties, the place it might probably deploy its technological and metallurgical capabilities to provide extremely engineered and differentiated merchandise.

Working neutrally to the worth of aluminum available in the market, the corporate earns earnings primarily from changing aluminum into semifinished merchandise. Its product portfolio consists of heat-treated plates and sheets in addition to naked and coated aluminum coils, serving varied international industries akin to aerospace, meals and beverage packaging, and normal engineering.

The corporate markets its semifinished aluminum merchandise for varied finish purposes. Its gross sales are made on to prospects by gross sales personnel in america, Canada, and Western Europe. Gross sales are additionally made by impartial gross sales brokers in different areas of the world. By way of long-term agreements and a spotlight to market tendencies, the corporate seeks to keep up sturdy relationships with its roughly 520 purchasers.

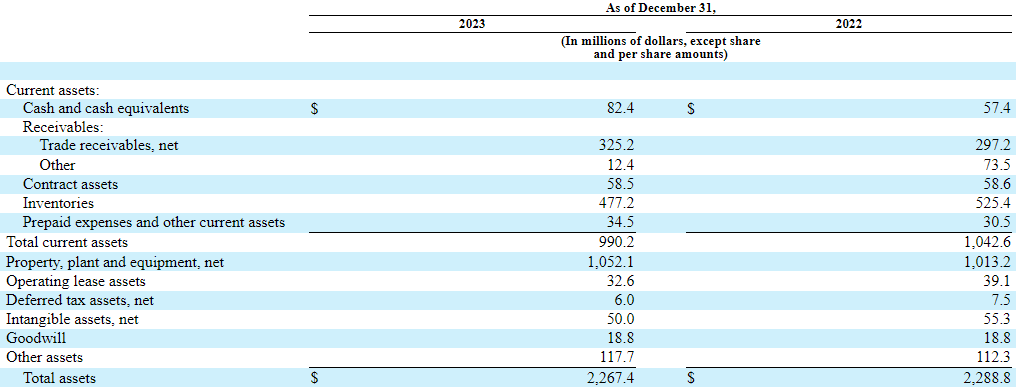

Stability Sheet

As of December 31, 2023, Kaiser reported money of $82 million, accounts receivable of $325 million, and inventories of $477 million, which implied present property of $990 million. The present ratio stands at greater than 2x, so I imagine that the corporate doesn’t report a liquidity subject.

As well as, given the full quantity of property and gear of $1.052 billion, whole property of $2.26 billion, and asset/legal responsibility ratio of greater than 2x, I imagine that Kaiser experiences a wholesome steadiness sheet.

Supply: 10-k

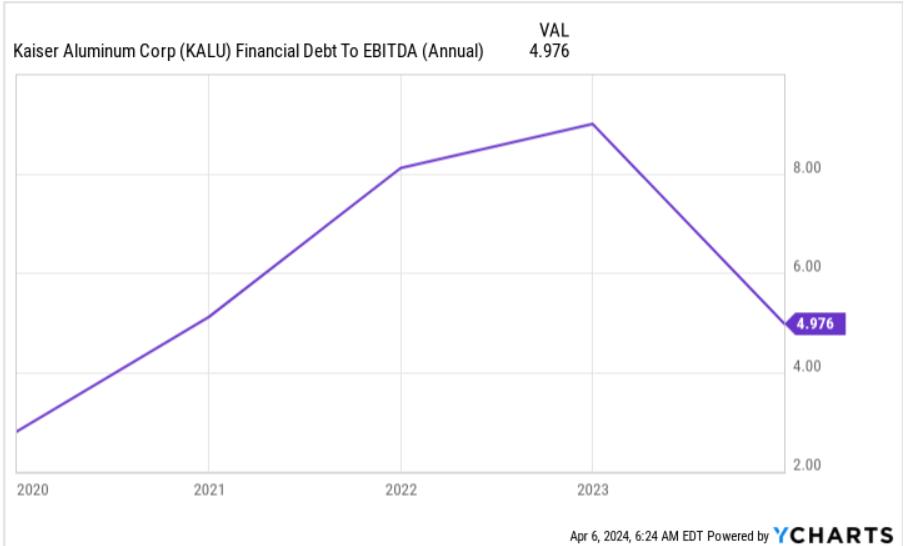

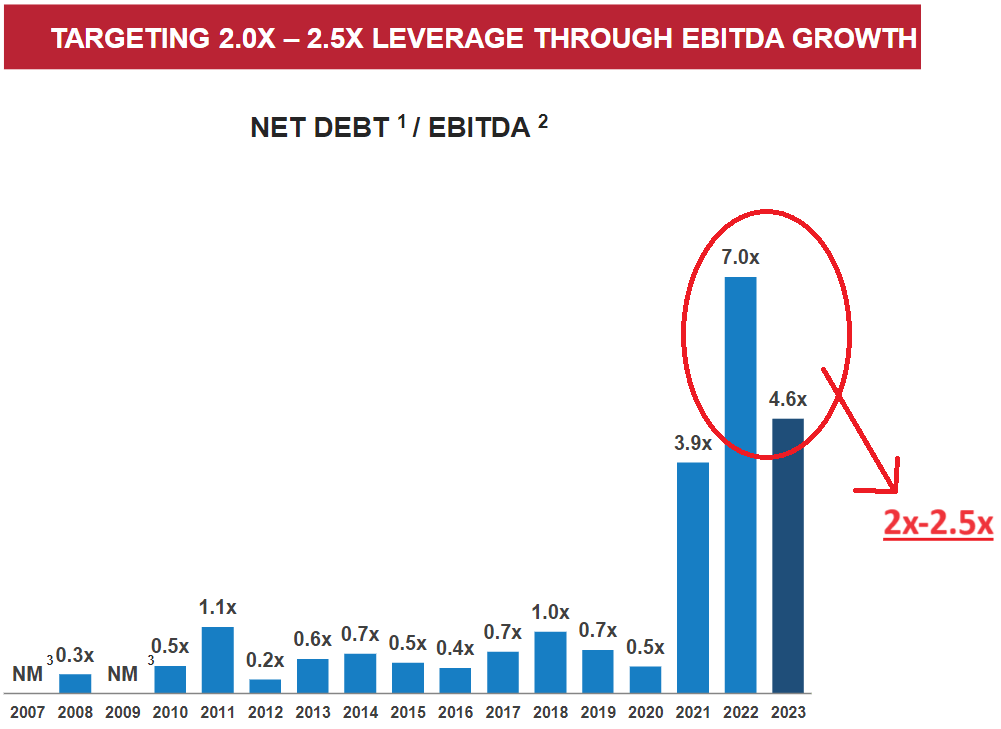

With long-term debt near $1 billion, Kaiser Aluminum doesn’t have numerous debt. Nonetheless, the monetary debt/EBITDA appeared to lower just lately from shut to eight.5x to lower than 5x. On this regard, I imagine {that a} additional lower within the whole variety of property might result in increased buying and selling multiples.

Supply: Ycharts

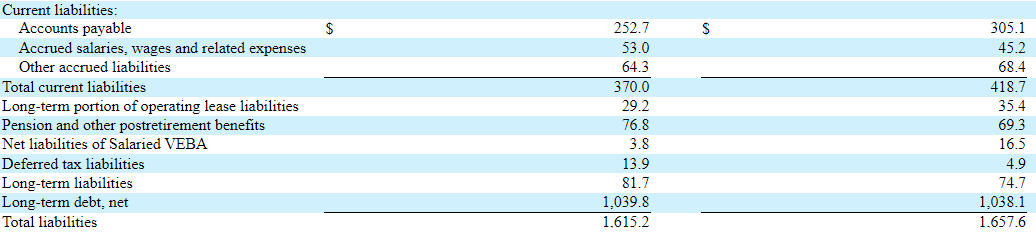

The whole quantity of liabilities stands at about $1.61 billion, and present liabilities are near $370 million. In 2023, the corporate did report a lower within the whole quantity of liabilities and present property.

Supply: 10-k

Price Of Debt Stands At Shut To 4.6%-4.5%

As of December 31, 2023, and 2022, Kaiser Aluminum had fastened fee senior unsecured notes excellent, with completely different maturity dates and rates of interest. Moreover, the corporate entered right into a Revolving Credit score Facility, rising the dedication and lengthening the maturity date to April 2022. The rates of interest included within the debt agreements are near 4.5% and 4.625%, so I imagine that the price of debt could also be shut to those figures within the close to future. The WACC could also be increased than 4.5%-4.625%.

Supply: 10-k

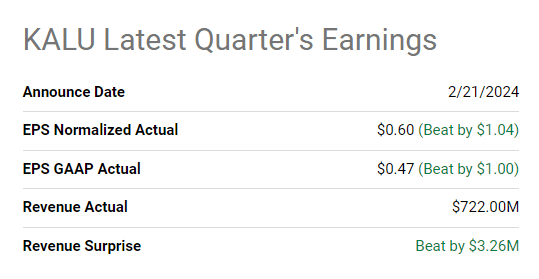

Assumption 1: Latest Earnings And Outlook Might Lead To Demand For The Inventory

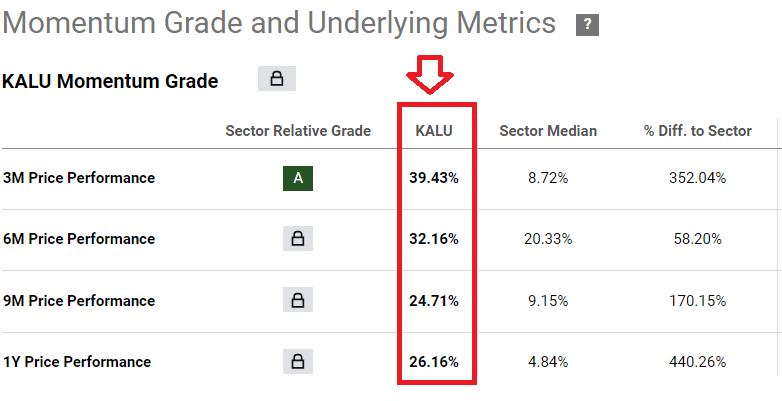

I imagine that the latest quarterly earnings reported in February had been useful as a result of they had been higher than what the market anticipated. Each the EPS GAAP and quarterly income had been higher than prevised. The latest improve in earnings might additionally partially clarify latest worth momentum will increase, which gave the impression to be bigger than worth momentum within the sector. In sum, evidently each the earnings and the inventory worth are transferring up.

Supply: Searching for Alpha Supply: Searching for Alpha

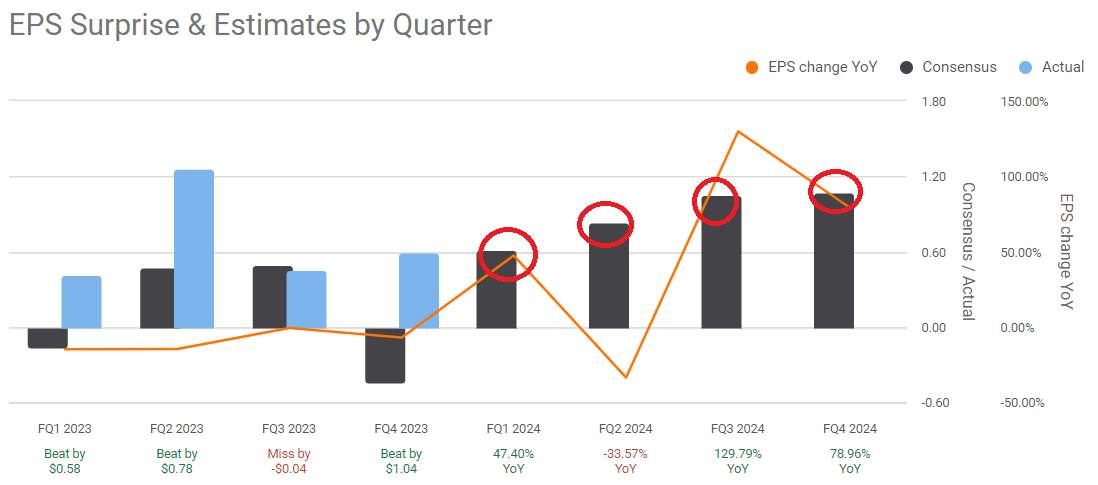

On the highest of it, analysts on the market predict EPS increases in future quarterly earnings in 2024. For my part, if Kaiser presents as soon as once more higher than anticipated earnings, we might see additional worth will increase.

Supply: Searching for Alpha

With all that being stated about earlier earnings and expectations, the outlook given by Kaiser within the final annual report was useful. The corporate expects demand to proceed in 2024. The demand for protection, area, and enterprise jets in addition to the packaging purposes are anticipated to deliver web gross sales development near 2%-3% in 2024, with adjusted EBITDA margins enhancements.

We imagine Kaiser stays properly positioned within the present demand atmosphere as a key provider in numerous finish markets with multi-year contracts with strategic companions and anticipate demand will proceed to enhance throughout key markets all through 2024.

Consequently, conversion income for the total 12 months 2024 is predicted to enhance 2% – 3% with adjusted EBITDA margins to enhance 70 – 170 foundation factors over 2023. Supply: 10-Okay

I imagine that the expectations from different analysts might deliver demand for the inventory. Consequently, Kaiser Aluminum could get pleasure from a decrease value of capital. Underneath my best-case state of affairs in my dividend discount model, I assumed a WACC near 7%.

Assumption 2: Lean Manufacturing, Six Sigma, And Different Operational Effectivity Efforts Might Lead To Web Earnings Development

Kaiser Aluminum Company’s future technique focuses on sustaining its key place in markets akin to Aero/HS Merchandise and Packaging by long-term contracts. As well as, it is going to search to enhance operational effectivity, spend money on strategic development, and adapt to market tendencies. On this regard, it’s also price noting that Kaiser expects to speed up operational effectivity due to the combination of administration groups, enchancment of provider choice, and integration of a number of instruments because of Lean Manufacturing, Six Sigma, and Whole Productive Manufacturing. Underneath my best-case state of affairs, I assumed that these efforts might result in web revenue development.

We additional attempt to boost the effectivity of product circulate to our prospects and our standing as a provider of alternative by tightly integrating the administration of our operations throughout a number of manufacturing services, product strains and goal markets. Moreover, our technique to be the provider of alternative and a low-cost producer is enabled by a tradition of steady enchancment that’s facilitated by the Kaiser Manufacturing System, an built-in software of instruments akin to Lean Manufacturing, Six Sigma, and Whole Productive Manufacturing. Utilizing KPS, we search to repeatedly cut back our personal manufacturing prices and eradicate waste all through the worth chain. Supply: 10-Okay

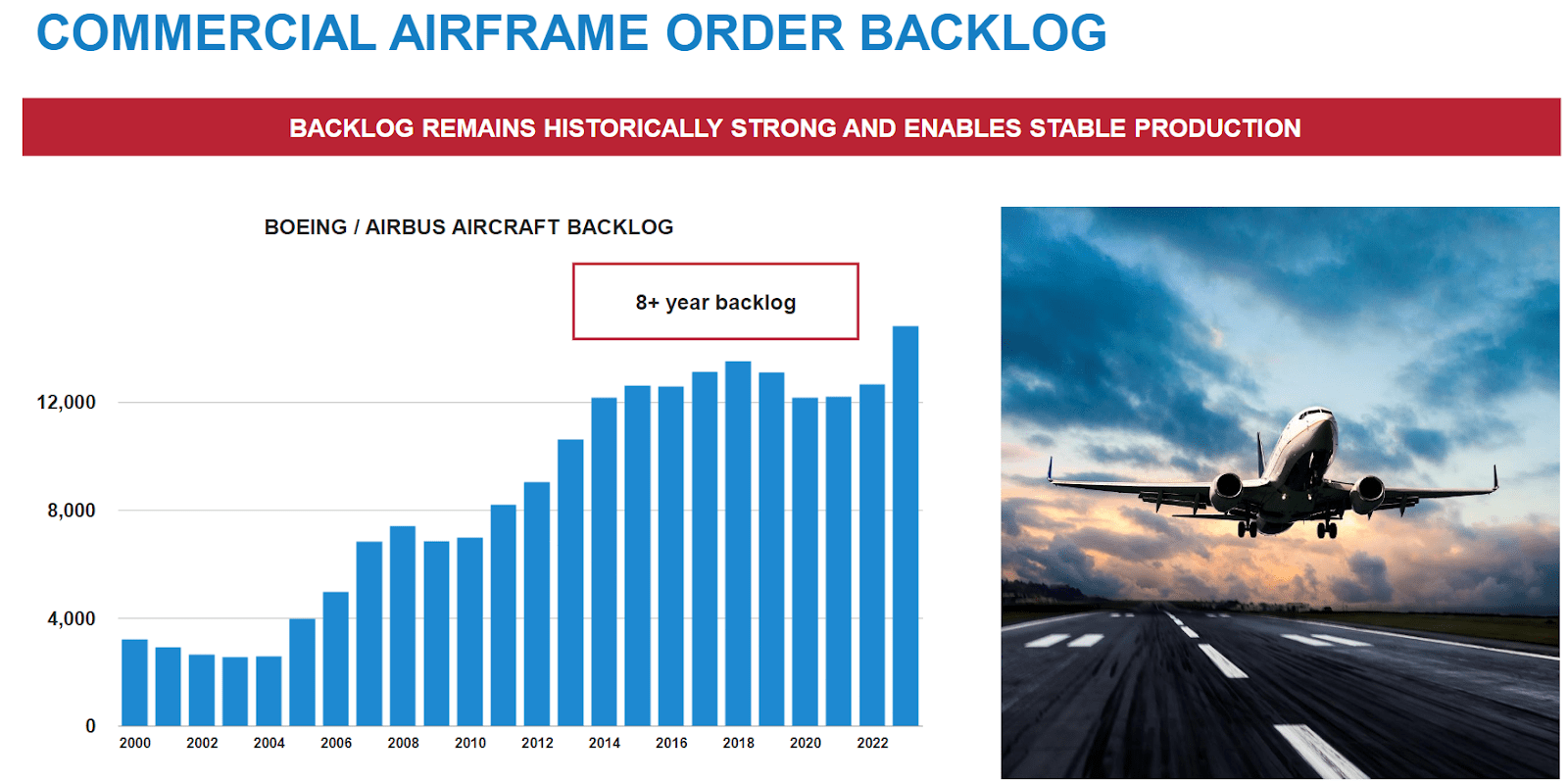

Assumption 3: Backlog Development With Orders From The Boeing Firm (BA) And Airbus SE (OTCPK:EADSF) Indicate Future Steady Web Gross sales

Given the full variety of orders collected from Boeing and Airbus, I imagine that we will anticipate considerably secure web gross sales within the coming years. In a latest presentation, the corporate talked about an eight-year backlog collected with these huge firms. It’s price noting that aerospace represents near one-third of the full quantity of income. In sum, future manufacturing won’t cease any time quickly.

Supply: Kaiser Aluminum Enterprise Replace February 2024

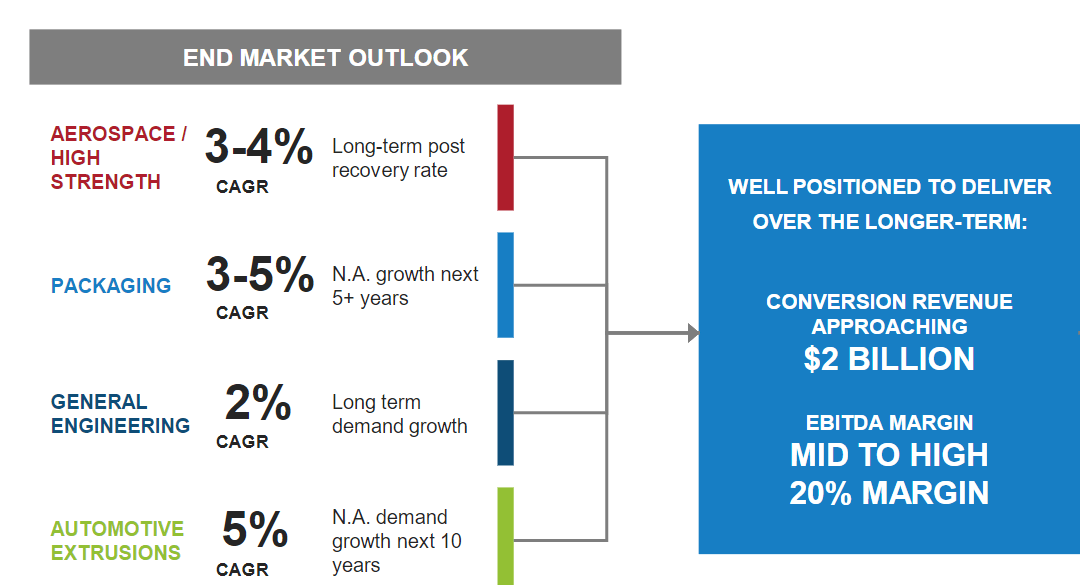

Assumption 4: Market Development Shut To 2%-5% Would Indicate Web Gross sales Development Shut To 2%-5%

For the evaluation of my monetary fashions, I took a cautious have a look at the market expectations of various finish markets wherein Kaiser sells merchandise. Aerospace, packaging, normal engineering, and automotive extrusion markets are anticipated to ship development near 2%, 3%, and even 5%. With these numbers in thoughts, I imagine that assuming median gross sales development near 4% in my best-case state of affairs is sensible.

Supply: Kaiser Aluminum Enterprise Replace February 2024

Assumption 5: Debt Discount Might Speed up Demand For The Inventory, Decrease The WACC, And Improve The Valuation.

In 2022, Kaiser Aluminum reported web debt near 7x. In 2023, the ratio was near 4x, and administration just lately introduced that it targets a leverage of 2x-2.5x.

For my part, additional discount in web leverage due to EBITDA development or debt discount will almost definitely deliver extra demand for the inventory. Consequently, the inventory valuation could improve.

Supply: Kaiser Aluminum Enterprise Replace February 2024

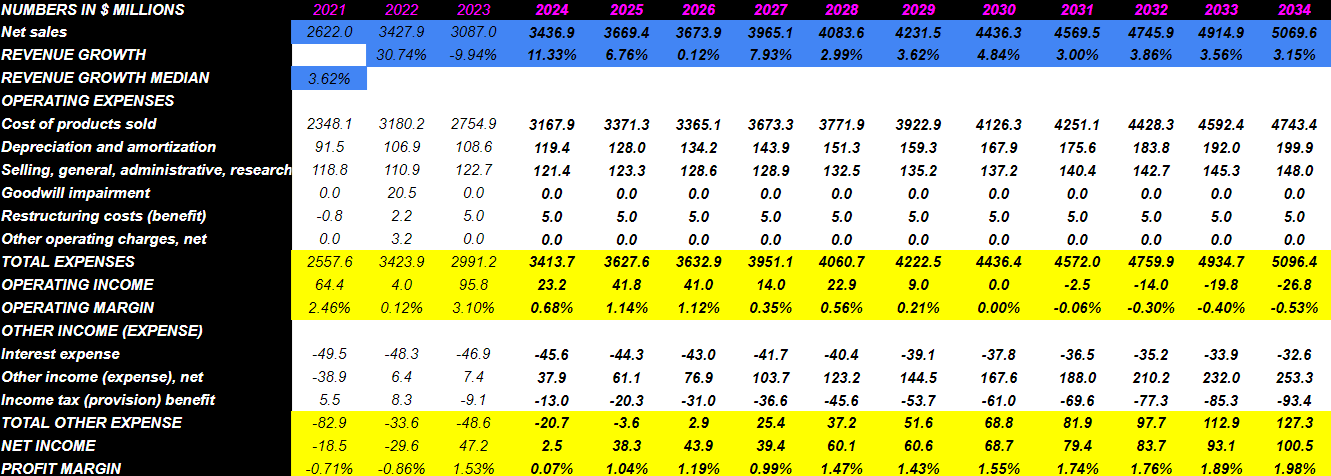

My Greatest-Case State of affairs Implied A Valuation Of $163 Per Share

Underneath my best-case state of affairs, Kaiser Aluminum will get pleasure from web gross sales development due to its rising finish goal markets. Backlog collected will almost definitely proceed to develop, the web debt/EBITDA a number of could decrease, and working effectivity may even enhance. In sum, my earlier assumptions can be profitable.

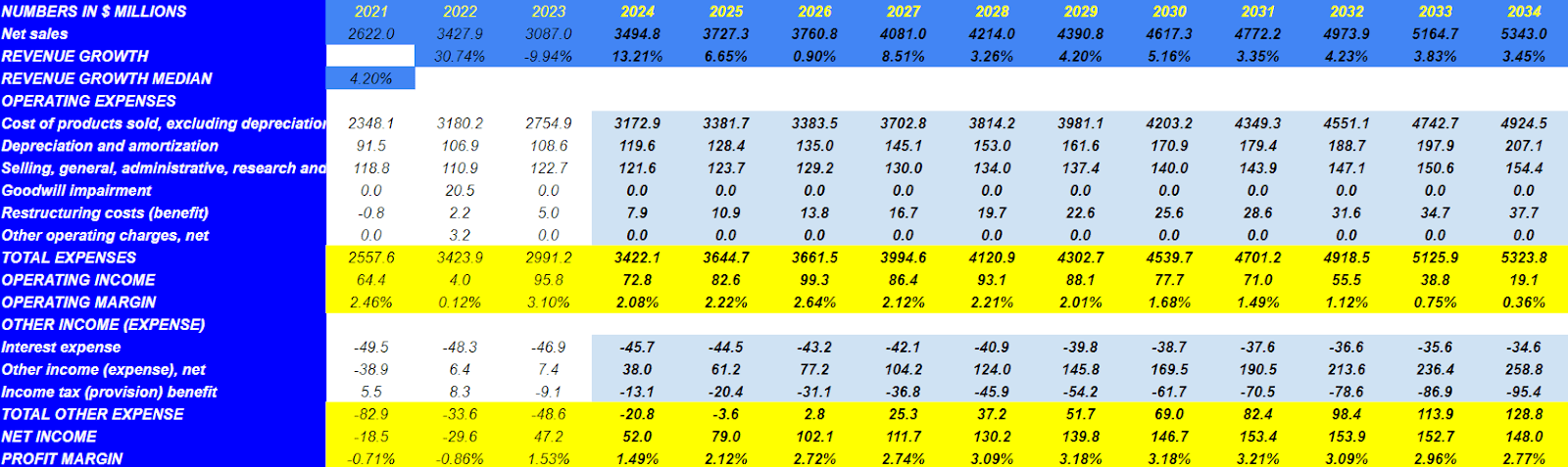

Within the best-case state of affairs, 2034 web gross sales can be $5,343 million, with income development of three.45%, giving a median income development of near 4.20% from 2024 to 2034.

However, working bills would come with the price of merchandise bought, excluding depreciation and amortization round $4,924.5 million, and having a depreciation and amortization of $207.1 million.

As well as, I took under consideration promoting, normal, administrative, analysis, and improvement prices, that are round $154.4 million. If we additionally think about restructuring prices of $37.7 million, whole bills could possibly be round $5,323.8 million, which is able to lead to an working revenue near $19.1 million and an working margin of 0.36%.

Lastly, with curiosity expense of -$34.6 million by 2034, if we add the opposite revenue web near $258.8 million and the revenue tax profit near -$95.4 million, 2034 web revenue can be near $148 million, with revenue margin near 2.77%.

Supply: My Dividend Mannequin

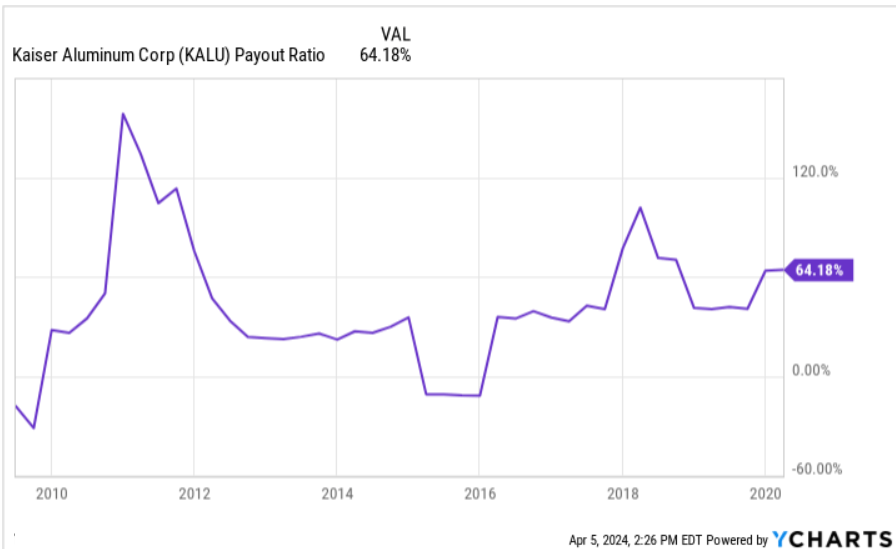

I estimate that the payout can be 54%, giving a dividend cost of $79.9 million. With a WACC of seven.2%, the NPV of future dividend funds would lead to near $472.16 million. Word that the payout ratio was bigger than 54% prior to now. I imagine that my numbers are conservative.

Supply: Ycharts

If we assume an Exit PE ratio of 31.08x, which is near the present PE, the terminal worth can be $4,599.5 million, and the NPV of TV can be $2,141 million.

Supply: Searching for Alpha

Lastly, the full valuation would stand at a minimum of $2,613 million, and making an allowance for the share depend of 16.02 million, the truthful worth would stand at $163 per share.

Supply: My Dividend Mannequin

Dangers And Opponents

Kaiser Aluminum Company’s merchandise compete with different supplies in varied purposes. Within the aerospace trade, they face competitors from titanium, composites, and carbon fiber to scale back weight and improve gas effectivity. Within the automotive trade, using aluminum competes with metal and different supplies, whereas in packaging they face options akin to metal, plastic, and glass, influenced by prices and recyclability. Modifications in buyer choice might have an effect on demand, resultantly affecting the monetary place and outcomes of Kaiser Aluminum Company.

The semifinished aluminum trade is extremely aggressive. Kaiser Aluminum Company differentiates itself with continued investments in high quality and machinability, providing distinctive choose attributes and buyer assist. KALU competes with Arconic, Constellium, Novelis, and Tri-Arrows in Aero/HS Merchandise, and with Arconic and Norsk Hydro ASA (OTCQX:NHYDY) in GE Merchandise and Automotive Extrusions.

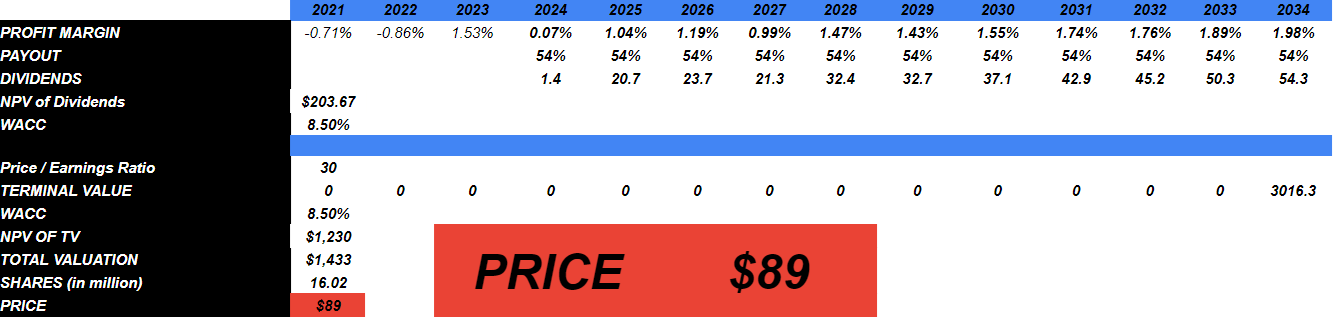

My Bearish Case Dividend Mannequin Contains Failed Effectivity Efforts, Decrease Finish Goal Market Development, And Failed Assumptions

Within the worst-case state of affairs, web gross sales for 2034 are anticipated to be round $5,069.6 million, with income development of three.15%.

The next working bills may be generated, with the primary expense being the price of merchandise bought of round $4,743.4 million, accompanied by a depreciation and amortization of $199.9 million. To this, we will add a promoting, normal, administrative, analysis, and improvement expense of near $148 million.

On this state of affairs, there is no such thing as a anticipated goodwill impairment, and the restructuring prices would stand at $5 million, giving whole anticipated bills of $5,096.4 million.

However, we bear in mind curiosity expense of -$32.6 million, with different revenue of $253.3 million, which might suggest web revenue near $100.5 million.

Supply: My Dividend Mannequin

Underneath this case state of affairs, the payout is expected to be 54%, with dividends very near $54.3 million, offering a NPV of dividends of $203.67 million. The WACC is estimated to be 8.5%. Concerning the worth / earnings ratio, it’s anticipated to be 30x, producing a terminal worth of a minimum of $3,016.3 million. Lastly, I obtained an NPV of a terminal worth of $1,230 million, which might point out a good worth of $89 per share.

Supply: My Dividend Mannequin

My Opinion

For my part, Kaiser Aluminum Company reveals a powerful enterprise technique, diversified product choices and geographic diversification. Its give attention to key markets and long-term contracts gives stability and development potential and can deliver web gross sales development near 4% over the approaching years. As well as, with guarantees concerning web debt/EBITDA discount, lean manufacturing, Six Sigma, and different operational effectivity efforts, I’d anticipate important web revenue development. The corporate faces aggressive dangers in a dynamic and extremely aggressive market and will endure from various manufacturing choices and completely different supplies. With that, I imagine that Kaiser might commerce at higher marks.