Feverpitched

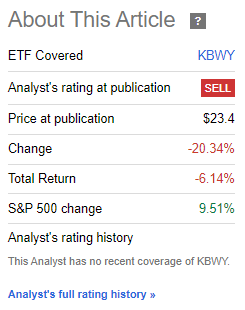

I final covered the Invesco KBW Premium Yield Fairness REIT ETF (NASDAQ:KBWY), an index ETF investing in high-yield small-cap U.S. REITs, in late 2021. In that article, I argued that KBWY’s undiversified small-cap holdings have been excessively dangerous, making the fund a promote. Since then, KBWY has underperformed within the S&P 500, as a consequence of unfavorable circumstances in the actual property trade and a number of other underperforming investments.

KBWY Earlier Article

Though circumstances in the actual property trade will seemingly enhance because the Federal Reserve slashes charges, KBWY stays an excessively dangerous, underperforming funding. As such, I might not put money into the fund.

KBWY – Fund Fundamentals

- Sponsor: Invesco.

- Underlying Index: KBW Nasdaq Premium Yield Equity REIT Index.

- Dividend Yield: 8.55%.

- Expense Ratio: 0.35%.

- Complete Returns CAGR 10Y: 3.41%.

KBWY – Overview and Evaluation

Index and Portfolio

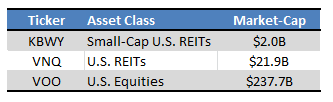

KBWY is a small-cap U.S. REIT index ETF, monitoring the KBW Nasdaq Premium Yield Fairness REIT Index. Stated index contains all related REITs assembly a fundamental set of standards, and explicitly excludes large-cap and worldwide securities. KBWY focuses on small-cap REITs, with a mean market cap of simply $2.0B billion, lower than 10% of the REIT common, and 1% of the fairness common.

Morningstar – Desk by Writer

For the fund, securities are weighted in keeping with their dividend yield: the upper the yield the higher the burden. Stated weighting scheme serves to extend the fund’s yield, but in addition its dangers, volatility, and potential losses throughout downturns. Diversification is considerably lowered as effectively, with KBWY investing in simply 31 completely different securities, in comparison with lots of for many broad-based REIT and fairness ETFs.

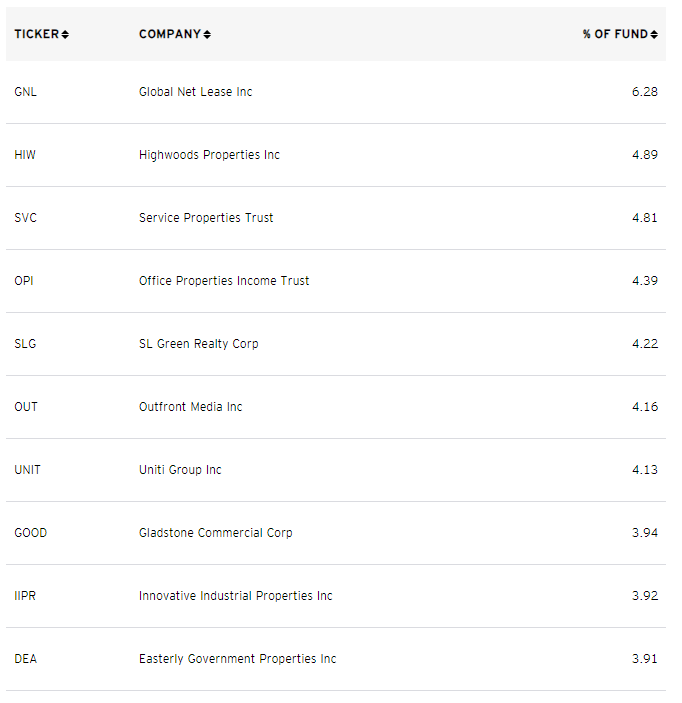

The fund’s portfolio is simply reasonably concentrated, with the fund’s high ten holdings accounting for 45% of its worth.

KBWY

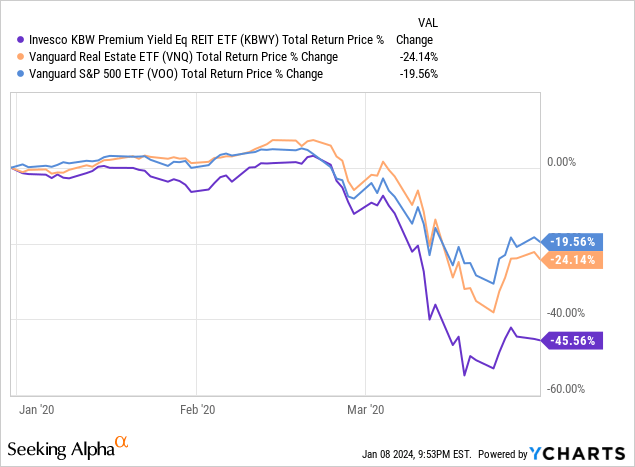

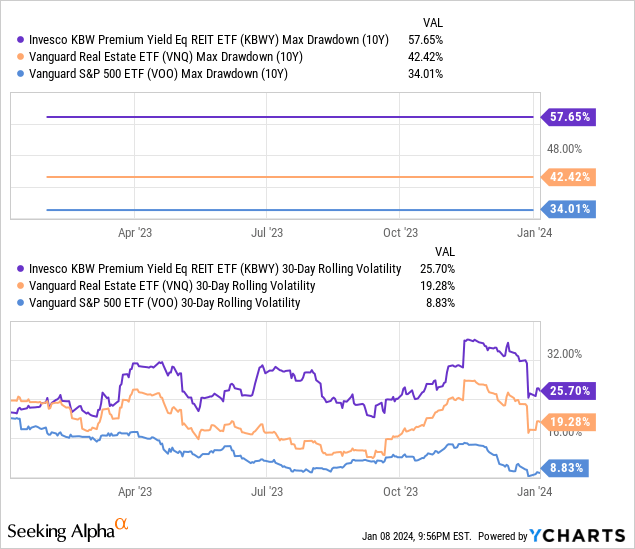

General, I’ve discovered KBWY’s portfolio to be a lot much less diversified and riskier than common. Anticipate vital losses and underperformance throughout downturns and bear markets, as was the case in early 2020.

Knowledge by YCharts

Drawdowns and volatility are each a lot greater too.

Knowledge by YCharts

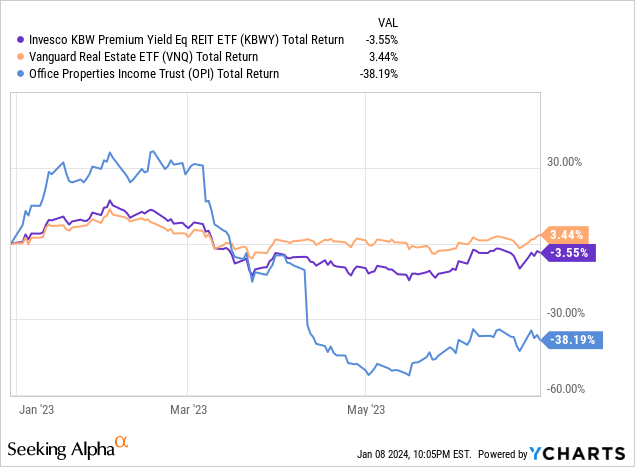

I’ve additionally discovered that KBWY’s lack of diversification typically results in idiosyncratic dangers and losses. For instance, the fund’s sizable place within the Workplace Properties Revenue Belief (OPI) led to underperformance through the first half of 2022. OPI is presently the fund’s fourth-largest holding, however weights have been greater prior to now.

Knowledge by YCharts

One other place in The GEO Group, Inc. (GEO) led to losses a few years back. No fund can keep away from underperforming investments endlessly, however extra diversified funds endure considerably decrease losses from losses in any particular person place. The alternative is true for much less diversified, extra concentrated funds like KBWY.

For my part and expertise, focus is typically a constructive for extra aggressive actively managed funds, assuming a reliable administration workforce. For instance, the Saba Closed-Finish Funds ETF’s (CEFS) technique of amassing vital positions in discounted CEFs, after which pressuring administration to slim the low cost by share buybacks or different initiatives, has led to vital good points prior to now.

However, focus is usually a unfavorable for index funds, as these hardly ever have interaction in comparable methods, nor do in-depth evaluation of their holdings. There’s little or no thought given to KBWY’s vital investments in OPI, previous to that in GEO, so place sizes needs to be stored small, to reduce losses from these.

General, I’ve discovered that KBWY’s low diversification and lack of focus have led to losses prior to now, making me cautious of investing within the fund.

Dividend Evaluation

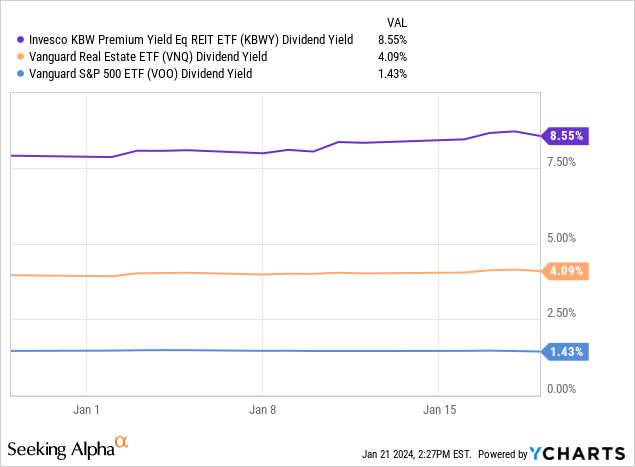

KBWY weights its portfolio on dividend yields, which leads to a powerful general 8.6% yield for the fund. It’s a sturdy yield on an absolute foundation, and far greater than that of the typical REIT, fairness, and bond ETF.

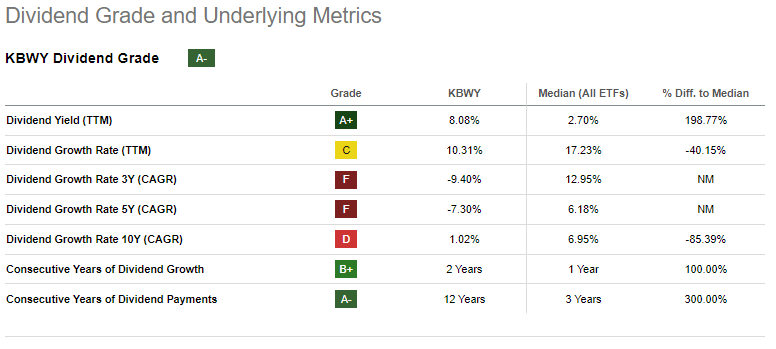

On a extra unfavorable notice, the fund’s dividend development monitor document is sort of mediocre, with dividends declining long-term amidst excessive volatility. Dividends have seen some development these previous twelve months, however a few of that appears to have been as a consequence of regular ETF dividend volatility.

In search of Alpha

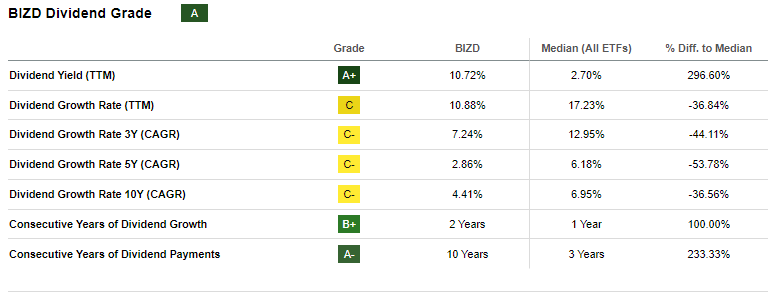

For my part, KBWY’s sturdy dividends are an vital profit for shareholders, however an general mediocre dividend development monitor document. However, there are a number of different ETFs focusing on different area of interest earnings sub-asset lessons with each greater yields and stronger development. These embrace the VanEck BDC Revenue ETF (NYSEARCA: BIZD), with a ten.8% dividend yield and powerful development.

In search of Alpha

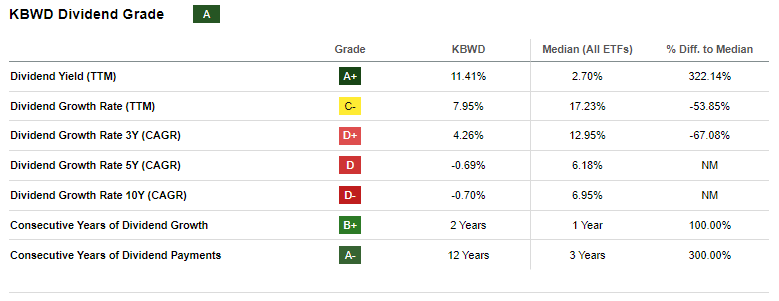

And the Invesco KBW Excessive Dividend Yield Monetary ETF (KBWD), with a secure 11.5% yield:

In search of Alpha

Thoughts you these are all very completely different funds, focusing on completely different asset lessons, however they do provide greater, extra sustainable yields. It appears to me that if buyers are going to put money into among the smaller, extra area of interest earnings sub-asset lessons on the market, they need to select the very best.

Efficiency Monitor-Document

KBWY’s efficiency monitor document is below-average, at finest. Lengthy-term returns are considerably decrease than these of the S&P 500 and reasonably decrease than these of broader U.S. REIT indexes. Returns have considerably improved since after the pandemic, largely as a consequence of vital losses throughout the pandemic. Volatility and threat are excessive.

In search of Alpha – Desk by Writer

General, the fund’s monitor document is below-average, and is a unfavorable for the fund and its shareholders.

Fast Market Evaluation

KBWY is an actual property fund, and the actual property trade as an entire has a fairly compelling funding thesis: decrease charges. Prior fee hikes led to a major contraction in actual property demand, costs and exercise, as a consequence of expensive financing and better alternative prices. Actual property merely appears to be like much less interesting when t-bills yield +5.0%, and unaffordable when mortgage charges climb to eight.0%.

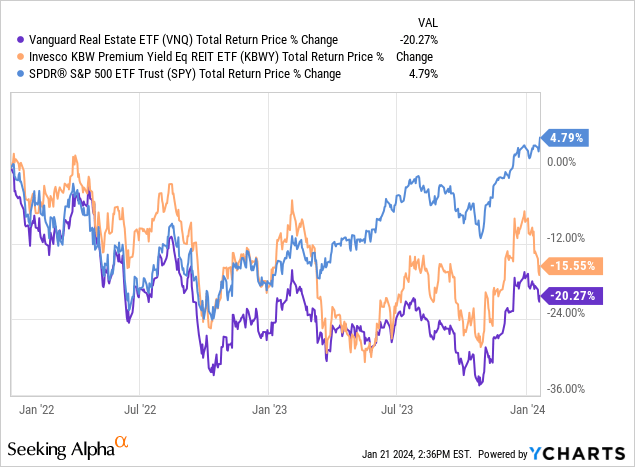

Federal Reserve hikes have led to actual property underperformance since early 2022, and that features KBWY.

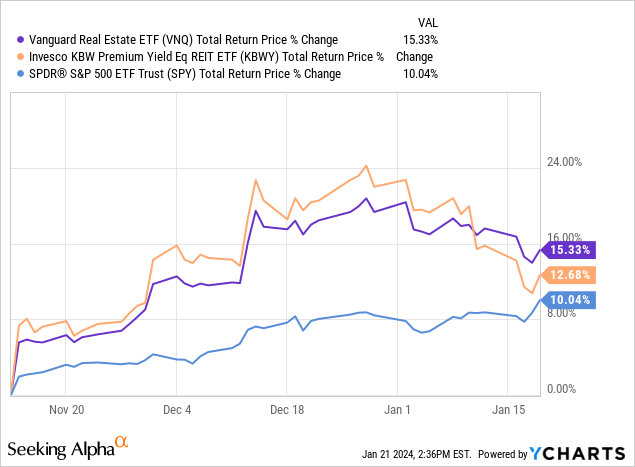

The flip aspect of the above is that actual property and REITs ought to outperform as charges decline subsequent yr. The market appears to assume so too, with REIT indexes and funds outperforming for the reason that charges peaked in November, and after dovish Fed guidance in December.

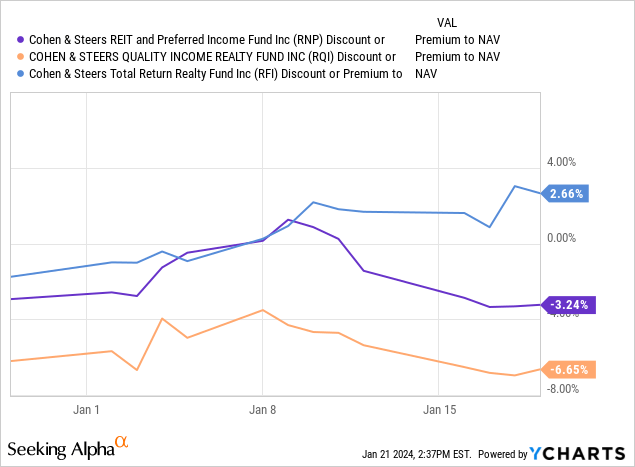

Because of the above, I believe the actual property trade has a really compelling funding thesis proper now. On the identical time, I believe there are a lot higher methods to play that than an funding in KBWY, as a consequence of its extreme threat and mediocre efficiency monitor document. Particularly, Cohen & Steers has a set of implausible, high-yield REIT CEFs. Of those, the Cohen & Steers High quality Revenue Realty Fund (RQI) trades with the widest 6.7% low cost. Reductions are typically greater, so ready for higher timing is perhaps finest.

Conclusion

KBWY is an excessively dangerous, underperforming funding. As such, I might not put money into the fund.