kadmy/iStock by way of Getty Pictures

I final wrote at In search of Alpha about some of the in style hashish shares on the earth, Cover Development (NASDAQ:CGC) nearly a yr in the past in late January, calling it not a good stock for cannabis investors. The inventory has declined 82.6% since then, and it is a lot greater than the market. The New Hashish Ventures World Hashish Inventory Index has dropped 19.6% since then.

Once I reviewed the corporate, I identified that the corporate was executing a plan to maintain its NASDAQ itemizing whereas reworking its enterprise to an American hashish operator by means of closing sure acquisitions that weren’t possible to assist the inventory. I instructed that if it failed to take action, then traders can be caught with a poorly performing firm with a excessive valuation. This hasn’t but been resolved, however the inventory has fallen much more than the 48% decline I predicted.

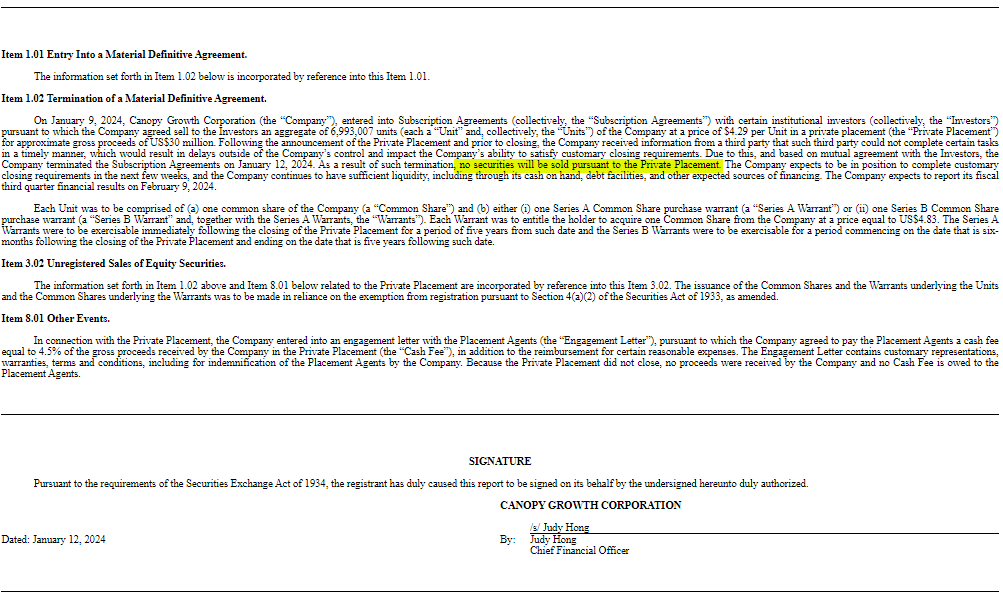

Final week, the inventory dropped 4.8% and is down 11.5% in 2024. The World Hashish Inventory Index is up 4.9% up to now. The explanation for the decline was an fairness providing that was introduced on Tuesday morning, with the corporate selling 7 million shares at $4.29 to institutional traders in a non-public placement. On Friday, very late within the day after the shut, Cover Development revealed that the deal has been cancelled, no less than for now.

SEC Submitting

On this fast assessment, I focus on why traders ought to proceed to keep away from the inventory.

The Fundamentals

Cover Development continues to have monetary challenges. In that 8-Okay above, it said that it expects to report its Q3 ending 12/31 on February ninth. In accordance with Sentieo, analysts challenge that income will drop almost 25% from a yr in the past to $75 million. Adjusted EBITDA is predicted to be -$14 million.

The outlook stays fairly dim, as analysts count on FY24 income to say no 18% to C$329 million with adjusted EBITDA of -C$101 million. For FY25, they challenge income will rise 2% to C$336 million with adjusted EBITDA of -C$16 million. Within the article a yr in the past, the FY25 outlook was for income of C$619 million with adjusted EBITDA of -C$84 million, so issues are shifting in the direction of decrease income and smaller losses.

As dangerous as its operations have been, this isn’t the most important downside. The corporate’s steadiness sheet stays an enormous problem. After its Q2, the corporate reported tangible e book worth of C$517 million. Money was C$270 million, however debt was C$681 million. The corporate used C$227 million to fund its operations in H1.

Cover Development has been making an attempt to maintain its NASDAQ itemizing whereas closing on the acquisitions of Acreage Holdings (OTCQX:ACRHF), Wana Manufacturers, and Jetty, but it surely hasn’t but made progress with the trade. As I mentioned a yr in the past, this won’t save the corporate, as American hashish operators will pursue an uplisting technique whether it is attainable.

The Valuation

The share depend has gone up quite a bit. The corporate reverse-split 10 shares for 1 just lately. On the time they filed the 10-Q for Q2, they’d successfully 83 million shares. Including within the RSUs and PSUs, the full was 84.5 million. This was up from 72 million three months earlier. At C$6.01, the market cap is C$507 million, which is about tangible e book worth. A yr in the past, it was buying and selling at 1.3X. Word that the three Canadian LPs that I embody in my mannequin portfolio all have higher steadiness sheets and commerce at a reduction to tangible e book worth.

The enterprise worth works out to be C$918 million, or 2.7X projected income for FY25 ending March 31. This isn’t interesting in any respect! My favourite hashish inventory, Organigram (OGI), which trades at simply 0.7X tangible e book worth, has a market cap of C$189 million and an enterprise worth of C$155 million. It trades at simply 0.8X projected FY25 income. Not like Cover Development, Organigram has constructive projected adjusted EBITDA.

Regardless of the plunging worth, I see the inventory as a promote nonetheless. Constellation Manufacturers (STZ) is deeply underwater in its funding and will step in and purchase them, however the present state of affairs with the corporate making an attempt to maintain its itemizing whereas closing U.S. acquisitions will get in the way in which. I believe the inventory ought to commerce at 50% of tangible e book worth given its giant debt, continued working losses, and use of money movement. If it had been to commerce there now, that may be C$3.06, which might be US$2.28, down one other 50%.

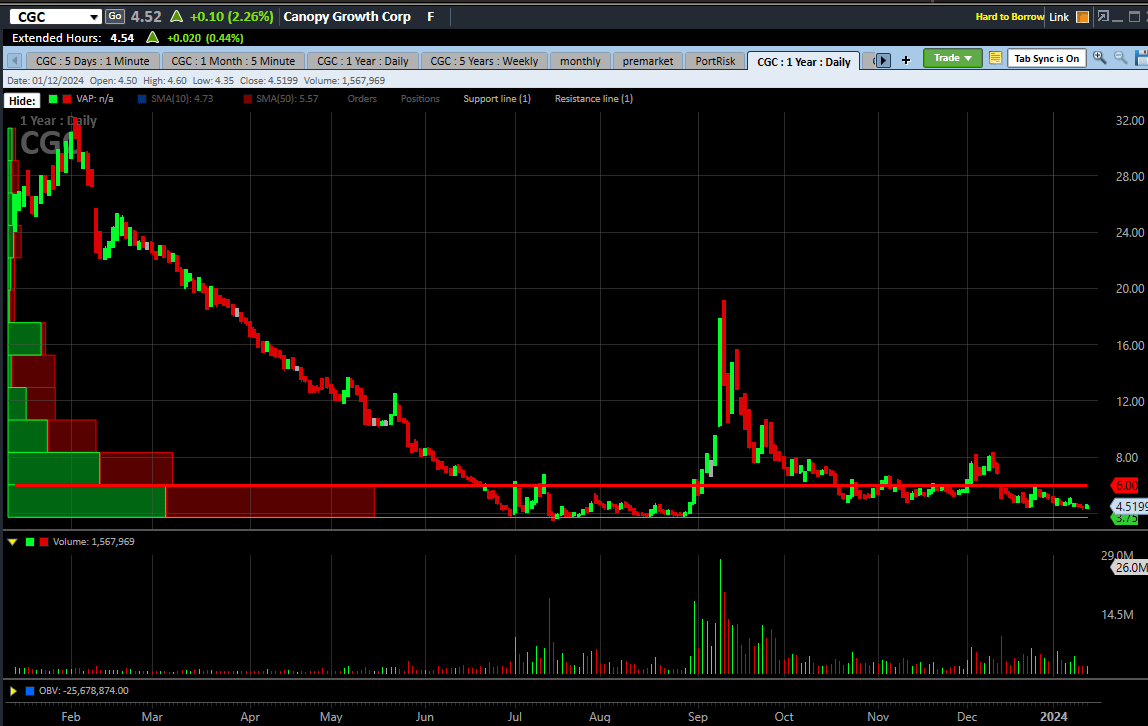

The Chart

Cover Development put in an all-time low of $3.46 in mid-July when it closed at a record-low $3.74, and this might get examined in my opinion:

Charles Schwab

The run-up in September was an error by traders who received excited in regards to the U.S. probably rescheduling. I see $3.75 as potential help on the chart and $6.00 as resistance.

Conclusion

I typically like to purchase the dips, however I’m not in any respect inquisitive about including Cover Development to my Beat the World Hashish Inventory Index mannequin portfolio. I believe the inventory needs to be buying and selling 50% decrease. It has a variety of debt and damaging working money movement.

The fairness sale, which is critical to repair their monetary situation and which is prone to occur within the close to future, was cancelled. Maybe the inventory will bounce on this information, giving shareholders an opportunity to exit at a better worth.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.